Architectural Rendering Software Market Size 2026-2030

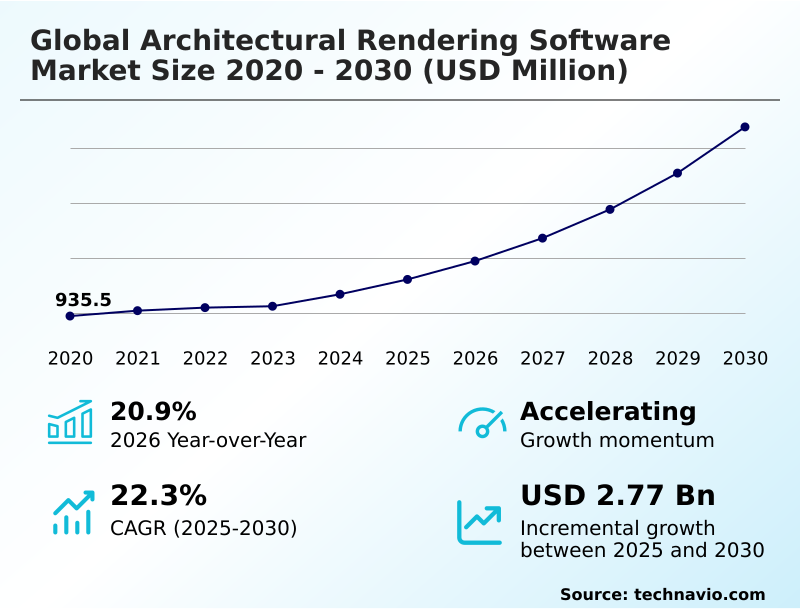

The architectural rendering software market size is valued to increase by USD 2.77 billion, at a CAGR of 22.3% from 2025 to 2030. Imperative for photorealistic visualization in project lifecycle management will drive the architectural rendering software market.

Major Market Trends & Insights

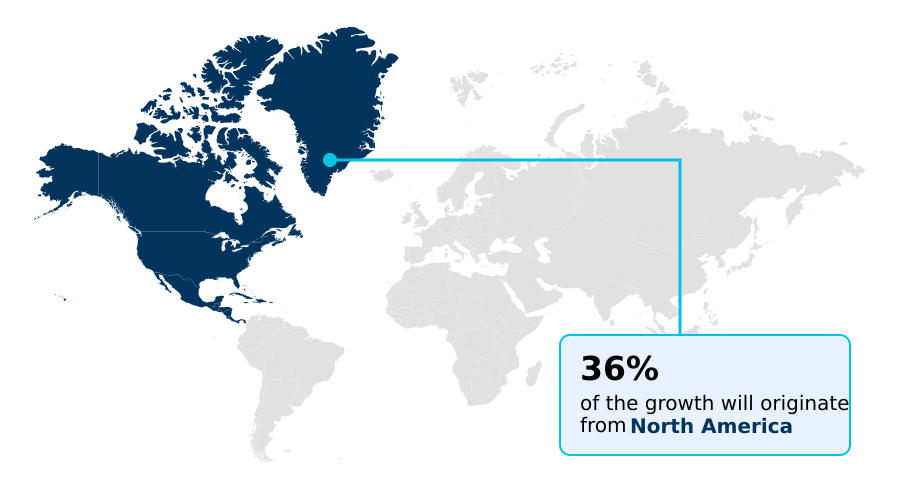

- North America dominated the market and accounted for a 36% growth during the forecast period.

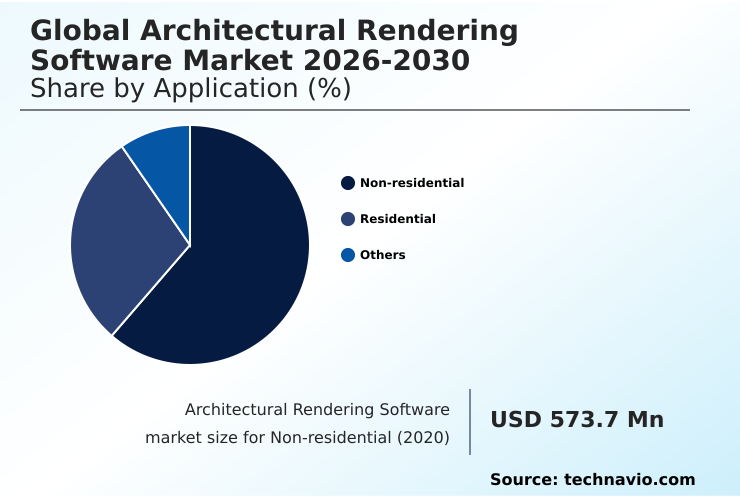

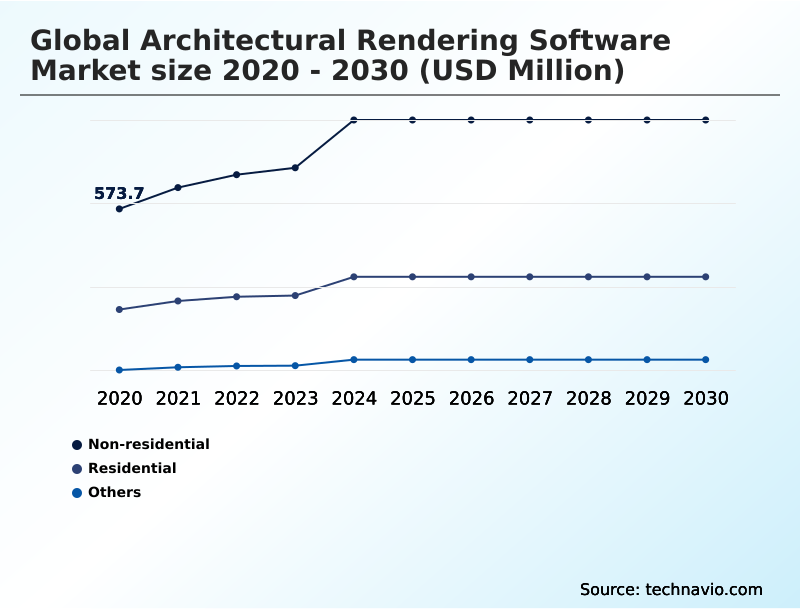

- By Application - Non-residential segment was valued at USD 840.6 million in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.44 billion

- Market Future Opportunities: USD 2.77 billion

- CAGR from 2025 to 2030 : 22.3%

Market Summary

- The architectural rendering software market is undergoing significant transformation, driven by the escalating demand for high-fidelity visualization tools in the architecture, engineering, and construction (AEC) industry. This demand extends beyond aesthetic enhancement to become a fundamental business necessity for design validation, stakeholder communication, and marketing.

- Key drivers include the widespread adoption of Building Information Modeling (BIM), which necessitates seamless workflow integration between design and visualization platforms. The convergence of real-time rendering capabilities with immersive technologies like virtual reality (VR) and augmented reality (AR) is reshaping design workflows, enabling interactive exploration and collaborative reviews.

- A common business scenario involves an architectural firm using VR walkthroughs to allow clients to experience a proposed commercial space, leading to faster design approvals and a reduction in late-stage changes. However, the market faces challenges from the substantial costs of software and high-performance hardware, as well as a persistent shortage of skilled professionals proficient in these complex tools.

- The shift towards cloud-based platforms and subscription models is helping to democratize access, but competition is intensifying from integrated real-time solutions that prioritize speed and ease of use for day-to-day design tasks.

What will be the Size of the Architectural Rendering Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Architectural Rendering Software Market Segmented?

The architectural rendering software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Non-residential

- Residential

- Others

- Deployment

- On-premises

- Cloud

- Component

- Software

- Services

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- APAC

- China

- Japan

- South Korea

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Application Insights

The non-residential segment is estimated to witness significant growth during the forecast period.

The non-residential segment is foundational to the architectural rendering software market, driven by the complexity and high financial stakes of commercial, industrial, and public infrastructure projects.

Clear, compelling communication is paramount among diverse stakeholders, where photorealistic visualization acts as a universal language. This segment heavily relies on a data-centric methodology for design validation and proactive error detection, using tools for environmental simulation and performance simulation.

Integrating these visualizations with Building Information Modeling (BIM) is crucial, ensuring data integrity and improving workflow integration. For example, firms using virtual design and construction (VDC) have reported a reduction in on-site rework by over 15%, showcasing the tangible ROI.

The demand is for solutions that facilitate stakeholder communication across the entire project lifecycle management.

The Non-residential segment was valued at USD 840.6 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Architectural Rendering Software Market Demand is Rising in North America Get Free Sample

The geographic landscape of the architectural rendering software market is characterized by mature, technologically advanced markets in North America and Europe, alongside rapidly expanding markets in APAC.

North America is expected to contribute approximately 36.0% of the market's incremental growth, driven by high adoption rates of cutting-edge technologies and stringent BIM integration requirements. In contrast, the APAC region's growth is fueled by massive urbanization and infrastructure investment.

Across regions, the adoption of cloud-based platforms is a unifying trend, democratizing access to powerful tools for 3D visualization and enabling cinematic animations.

For instance, firms in Europe leveraging advanced lighting simulation for sustainable design mandates have improved compliance reporting efficiency by over 20%.

The use of real-time rendering and virtual reality (VR) is prominent globally, enhancing design validation and client engagement from Toronto to Telosa.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions within the architectural rendering software market increasingly hinge on detailed comparisons of real-time rendering vs offline rendering, with firms evaluating the trade-offs between speed and ultimate photorealistic quality. The efficiency of BIM to rendering workflow integration is a critical factor, as seamless data transfer is paramount for large-scale projects.

- The rise of cloud rendering for small studios has democratized access to high-performance computing, leveling the competitive landscape. Use cases such as virtual reality architectural walkthroughs are now essential for client engagement and are a key differentiator. The application of generative AI in conceptual design is accelerating ideation, allowing architects to explore numerous options rapidly.

- Furthermore, using AR for construction verification provides tangible on-site benefits, reducing errors. Architectural rendering for real estate marketing remains a primary driver, where high-quality visuals directly impact sales velocity. Firms that leverage environmental analysis visualization tools find that data-driven design decisions are made twice as fast compared to traditional methods.

- The development of AI for architectural scene population automates tedious tasks, freeing up artists to focus on creativity. The benefits of SaaS in architectural software include predictable costs and continuous updates, contrasting with the high upfront cost of on-premise render farms. Addressing the skills gap in architectural visualization is crucial for firms to fully exploit these technologies.

- Ultimately, from photorealistic rendering for project approval to interactive 3D architectural presentations and lighting simulation for sustainable design, the market is evolving toward more integrated and intelligent solutions.

What are the key market drivers leading to the rise in the adoption of Architectural Rendering Software Industry?

- The imperative for photorealistic visualization throughout the project lifecycle management acts as a key driver for market expansion.

- The escalating demand for photorealistic visualization across the entire project lifecycle is a primary market driver.

- This has become a business necessity for communicating concepts and securing client buy-in, with high-quality renderings shown to improve project approval rates by up to 30%.

- A second powerful driver is the convergence of real-time rendering with immersive technologies like virtual reality (VR) and augmented reality (AR), which accelerate the design cycle.

- The integration of this capability with VR offers true one-to-one scale immersion, while AR aids in construction verification. The widespread adoption of building information modeling (BIM) is a third critical driver.

- Seamless BIM integration is paramount, with synchronized workflows reducing data management errors by over 25% and enhancing stakeholder communication through accurate, compelling visual narratives.

What are the market trends shaping the Architectural Rendering Software Industry?

- The integration of artificial intelligence and generative processes is emerging as a defining market trend. This is transforming visualization workflows from passive tools into intelligent design partners.

- A defining trend is the profound integration of artificial intelligence into visualization workflows, transforming software into an intelligent partner. AI-driven algorithms automate laborious tasks like populating scenes, with some systems reducing content creation time by up to 60%. Advanced models can generate physically accurate materials from simple text prompts, accelerating the design iteration cycle.

- Beyond automation, generative processes and generative AI are becoming powerful forces in conceptual design, enabling architects to explore a broader solution space. This symbiotic relationship between human creativity and machine intelligence is fostering new design methodologies. AI-powered denoising is another key advancement, producing clean images from partial renders 75% faster than traditional methods, allowing for more interactive design sessions.

- This shift positions the software as a central intelligence hub for 3D modeling and data-rich visualization.

What challenges does the Architectural Rendering Software Industry face during its growth?

- Prohibitive costs associated with software acquisition and hardware, combined with complex licensing structures, present a key challenge to industry growth.

- A primary market challenge is the substantial financial outlay for software and high-performance hardware, with total ownership costs for on-premise solutions being up to three times higher than cloud-based alternatives over a five-year period. This creates a significant barrier for smaller firms. Another formidable challenge is the steep learning curve and scarcity of skilled professionals.

- Firms report that it can take over 200 hours of dedicated training for an architect to master advanced digital asset libraries and procedural modeling techniques. This skills gap drives up labor costs and leads many to outsource visualization needs. Finally, the market faces a challenge from integrated real-time visualization solutions, which prioritize speed and workflow integration.

- These 'good enough' quality tools are capturing a significant portion of day-to-day visualization tasks, forcing traditional rendering software companies to further differentiate on realism.

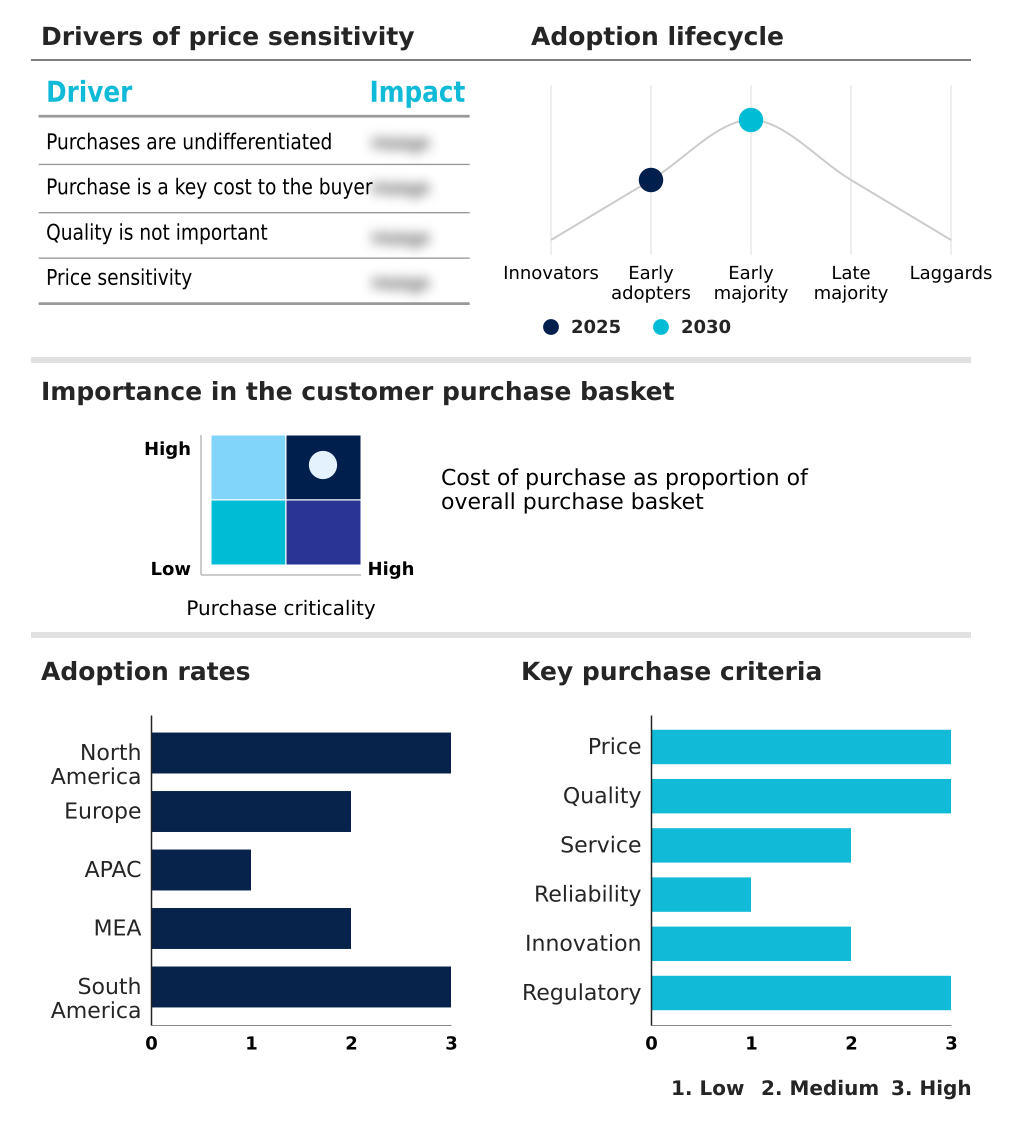

Exclusive Technavio Analysis on Customer Landscape

The architectural rendering software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the architectural rendering software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Architectural Rendering Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, architectural rendering software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Applet 3D - The company provides cloud-based 3D visualization and interactive presentation tools designed to enhance architectural communication and enable virtual staging for real estate development.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Applet 3D

- ArchiVinci

- Blender Foundation

- Chaos Software GmbH

- Daz Productions Inc.

- Epic Games Inc.

- KeyShot Inc.

- Lumion

- MyArchitectAI

- Next Limit SL

- NVIDIA Corp.

- RealSpace Vision Communication

- Robert McNeel and Associates

- Shapespark sp. Zoo

- Side Effects Software Inc.

- Snaptrude Inc.

- Trimble Inc.

- ZOA Studio

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Architectural rendering software market

- In August 2025, Chaos introduced Envision, a beta tool designed to simplify the creation of high-quality architectural animations and integrate with existing real-time rendering workflows like Enscape, making storytelling more accessible for architects.

- In October 2025, D5 Render gained prominence for its effective use of real-time ray tracing technology, which allows for the instantaneous generation of photorealistic images and animations, significantly accelerating the design iteration cycle.

- In March 2025, the Italian Ministry of Culture launched a government-funded program to create hyper-realistic, historically accurate digital archives of significant cultural heritage sites, including Pompeii, using advanced rendering and photogrammetry software.

- In May 2025, developers of the NEOM project in Saudi Arabia announced NEOM Synapse, a proprietary, real-time, city-scale digital twin platform, requiring all architectural and engineering partners to deliver dynamic, data-rich models for integrated simulation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Architectural Rendering Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 22.3% |

| Market growth 2026-2030 | USD 2772.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 20.9% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, Japan, South Korea, India, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Egypt, Kuwait, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The architectural rendering software market is defined by a relentless push for realism and workflow efficiency. The core technology is evolving from a visualization tool to an analytical partner, driven by advancements in photorealistic visualization and real-time rendering.

- This shift is compelling firms to make strategic boardroom decisions regarding investment in talent versus technology, especially with the rise of generative AI and procedural modeling which automate complex tasks like scene composition. Integration with a building information modeling (BIM) data-centric methodology is no longer optional but a baseline requirement, with tools for environmental simulation and performance simulation becoming standard.

- The hardware dependency on powerful GPUs for techniques like global illumination and texture mapping remains a key consideration. A pivotal development is the effectiveness of AI-powered denoising, which has been shown to boost artist productivity by over 50% in certain workflows by drastically reducing the time needed to produce clean final images.

- Technologies such as augmented reality (AR) and virtual home staging are expanding the software's application beyond design into sales and construction verification.

What are the Key Data Covered in this Architectural Rendering Software Market Research and Growth Report?

-

What is the expected growth of the Architectural Rendering Software Market between 2026 and 2030?

-

USD 2.77 billion, at a CAGR of 22.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Non-residential, Residential, and Others), Deployment (On-premises, and Cloud), Component (Software, and Services) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Imperative for photorealistic visualization in project lifecycle management, Prohibitive costs and complex licensing structures

-

-

Who are the major players in the Architectural Rendering Software Market?

-

Applet 3D, ArchiVinci, Blender Foundation, Chaos Software GmbH, Daz Productions Inc., Epic Games Inc., KeyShot Inc., Lumion, MyArchitectAI, Next Limit SL, NVIDIA Corp., RealSpace Vision Communication, Robert McNeel and Associates, Shapespark sp. Zoo, Side Effects Software Inc., Snaptrude Inc., Trimble Inc. and ZOA Studio

-

Market Research Insights

- Market dynamics are increasingly shaped by the need for efficiency and advanced communication, where immersive experiences are becoming standard. Firms leveraging collaborative platforms report project approval times shortening by as much as 30% compared to traditional methods.

- The move toward SaaS ecosystems is not only a financial shift but also an operational one, enhancing the design iteration cycle and enabling remote work. This digital transformation is critical, as integrated BIM to rendering workflows have demonstrated a capacity to reduce data-related errors by over 25%.

- The focus on data-rich visualization supports better stakeholder communication and decision-making throughout the project lifecycle management, solidifying the software's role as an indispensable tool.

We can help! Our analysts can customize this architectural rendering software market research report to meet your requirements.

RIA -

RIA -