Armored Civilian Vehicles Market Size 2026-2030

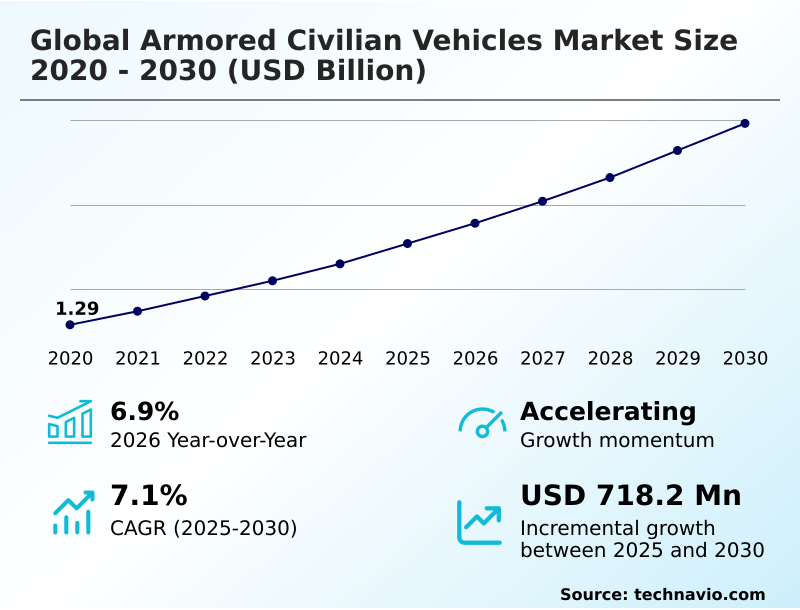

The armored civilian vehicles market size is valued to increase by USD 718.2 million, at a CAGR of 7.1% from 2025 to 2030. Increasing global security threats and personal risk perception will drive the armored civilian vehicles market.

Major Market Trends & Insights

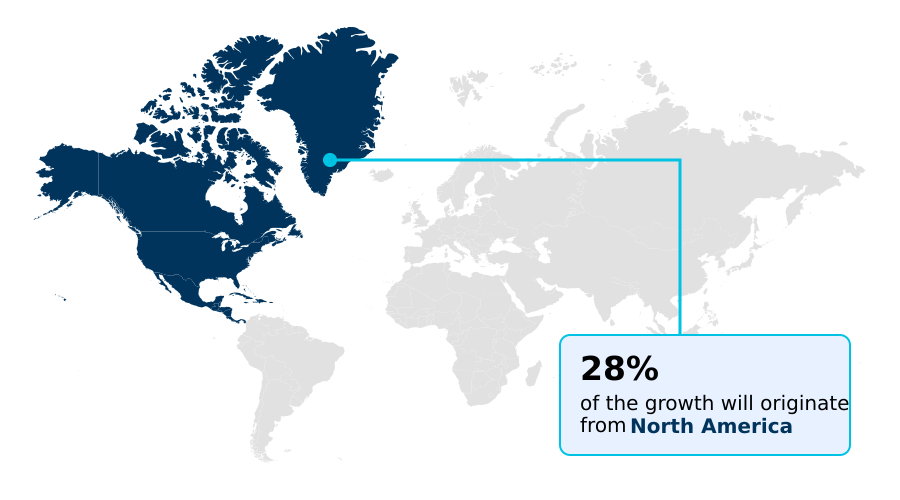

- North America dominated the market and accounted for a 28.4% growth during the forecast period.

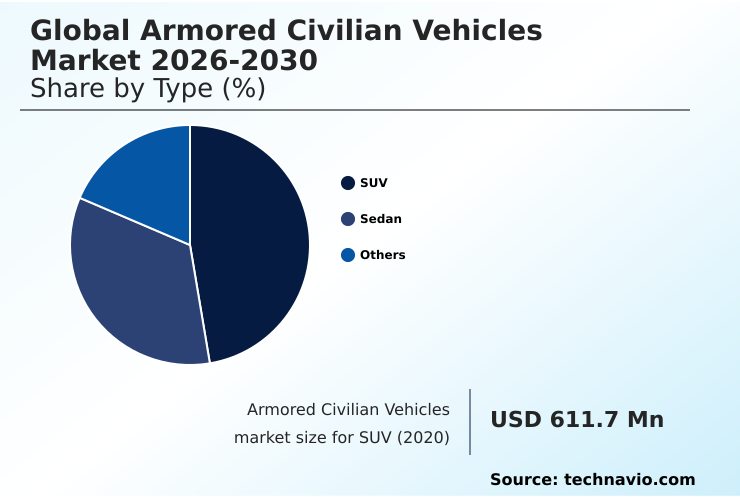

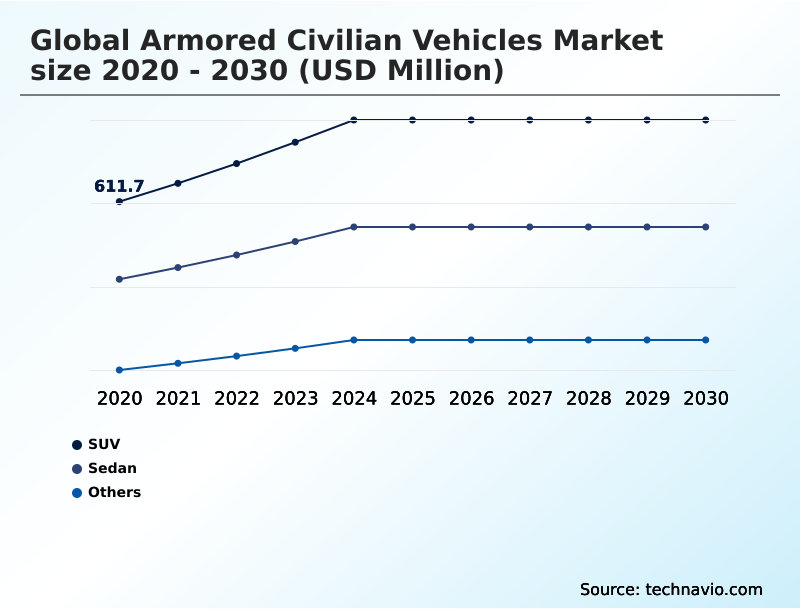

- By Type - SUV segment was valued at USD 791.9 million in 2024

- By End-user - Government segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.19 billion

- Market Future Opportunities: USD 718.2 million

- CAGR from 2025 to 2030 : 7.1%

Market Summary

- The armored civilian vehicles market is undergoing a significant transformation, driven by evolving security needs and technological advancements. No longer confined to government and diplomatic use, the market now caters to a growing civilian clientele demanding personal security vehicles.

- This shift is pushing manufacturers toward innovations in lightweight composite materials and discreet armoring solutions that preserve the aesthetics and vehicle performance dynamics of luxury platforms. A critical challenge remains in the realm of armored electric vehicles, where protecting the high-voltage battery pack from ballistic threats requires novel engineering approaches.

- For instance, a corporate security director must now evaluate not just traditional ballistic threat assessment data but also the complexities of armored vehicle maintenance for an EV fleet. This involves balancing certified ballistic protection with operational factors like range, charging infrastructure, and the specialized vehicle armoring process, ensuring executive protection transport is both secure and practical in modern operational environments.

What will be the Size of the Armored Civilian Vehicles Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Armored Civilian Vehicles Market Segmented?

The armored civilian vehicles industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- SUV

- Sedan

- Others

- End-user

- Government

- Civilian

- Vehicle type

- ICE

- Electric

- Hybrid

- Distribution channel

- Direct sales

- Distributors

- Online platforms

- Geography

- North America

- US

- Mexico

- Canada

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Colombia

- Middle East and Africa

- UAE

- South Africa

- Saudi Arabia

- Rest of World (ROW)

- North America

By Type Insights

The suv segment is estimated to witness significant growth during the forecast period.

The Sports Utility Vehicle (SUV) segment dominates the market, representing the preferred platform for armoring due to inherent design advantages.

Their body-on-frame construction, higher ground clearance, and powerful engines facilitate the integration of heavy ballistic materials with a reduced impact on vehicle performance dynamics.

This allows for comprehensive passenger compartment integrity and the addition of features like blast mitigation flooring and suspension reinforcement.

Demand for armored suvs spans government, corporate, and private clients, with a strong trend toward low-profile armoring to maintain a discreet appearance.

The segment accounts for over 48% of armored civilian vehicle sales, driven by its versatility and ability to combine high-security with luxury. Key offerings include tactical response vehicles and customized executive protection transport, featuring upgraded braking systems and advanced security.

The SUV segment was valued at USD 791.9 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 28.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Armored Civilian Vehicles Market Demand is Rising in North America Get Free Sample

The geographic landscape of the armored civilian vehicles market is diverse, with regional demands shaped by unique security and economic factors.

North America leads in technological sophistication, focusing on low-profile armoring and executive protection transport, and is expected to account for over 28% of the market's incremental growth.

In contrast, markets in South America are volume-driven, with a broader customer base seeking personal security vehicles due to regional safety concerns.

The APAC region is the fastest-growing, with a regional expansion rate of nearly 7.8%, fueled by rising wealth and the need for high-security transport. This global distribution necessitates complex armored transport logistics and adherence to varied armored vehicle export regulations.

Efficient supply chain management in this sector has been shown to reduce delivery lead times by up to 20% for international clients, a key competitive differentiator.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The decision-making process for acquiring a protected vehicle involves complex trade-offs, beginning with the core choice between lightweight composite armor versus ballistic steel. This decision directly influences the total cost of armoring a cadillac escalade and defines the engineering approach for a project like armoring a tesla model s, where the challenges of armoring electric vehicles are paramount.

- The critical task of protecting ev batteries from ballistic threats requires specialized materials and techniques. For those seeking the best armored suv for personal use, understanding the difference between vpam vr7 versus vr9 ballistic protection is essential.

- The armored vehicle manufacturing process explained to clients must cover key systems, including the details of upgrading brakes on an armored vehicle and the specifics of run-flat tire performance on armored suvs, which heavily impact armor on vehicle handling. For high-end platforms like an armored toyota land cruiser, features are extensive.

- The logistics of how to import an armored car are also a consideration for international buyers. For others, the focus is on discreet armoring for luxury sedans or anti-kidnapping features in civilian vehicles. Specialized applications such as an armored vehicle for cash in transit require robust suspension upgrades for armored trucks.

- The process of maintaining an armored mercedes-benz s-class differs from that of customizing an armored jeep wagoneer, reflecting the diverse needs met by the industry, including government procurement of armored civilian vehicles.

What are the key market drivers leading to the rise in the adoption of Armored Civilian Vehicles Industry?

- Increasing global security threats and a heightened perception of personal risk are primary drivers for the armored civilian vehicles market.

- Persistent global security concerns and an expanding private-sector client base are key market drivers. There is rising demand for discreet armoring solutions, particularly for armored luxury sedans and armored suvs, from executives and high-net-worth individuals.

- This has broadened the market for personal security vehicles, with the non-government segment growing by over 30% in recent years. This clientele demands certified ballistic protection that does not visibly alter the vehicle.

- Consequently, manufacturers are innovating with advanced ballistic glass technology and integrated armor. The ability to offer extensive armored car customization is a significant differentiator, with requests for bespoke interiors and specialized equipment increasing by 50%.

- This creates a robust market for both new armored suv for sale and aftermarket armored vehicle conversion services, all driven by a proactive approach to vehicle-borne threat mitigation.

What are the market trends shaping the Armored Civilian Vehicles Industry?

- The integration of advanced electronics and network-centric capabilities is a dominant trend. This transforms armored platforms from protected transport into mobile command centers.

- A primary trend is the rapid adoption of electric and hybrid drivetrains, presenting unique ev armoring challenges. The industry is focused on developing lightweight armor solutions to counteract the added mass of batteries, with new composite applications reducing overall weight by up to 15% without compromising protection.

- This shift is accompanied by the deep integration of network-centric capabilities, transforming vehicles into mobile command centers with secure communication suites. These electronic systems improve situational awareness by over 40% in urban environments. The rise of hybrid armored vehicle tech offers a bridge solution, combining silent electric-mode operation with the extended range of traditional engines.

- This focus on technological advancement is redefining the capabilities of personal security vehicles and tactical civilian vehicles, aligning with modern security demands and sustainability goals, while also influencing armored vehicle maintenance protocols.

What challenges does the Armored Civilian Vehicles Industry face during its growth?

- The prohibitive costs and inherent complexity of the manufacturing process present a significant challenge to the armored civilian vehicles market.

- The market's primary challenges are the high civilian armored vehicle cost and the engineering complexity of the vehicle armoring process. Integrating protection, which can increase a vehicle's base cost by over 200%, requires a complete vehicle disassembly for chassis reinforcement and the installation of materials that meet specific ballistic certification levels. This labor-intensive process makes scaling production difficult.

- A perpetual engineering challenge is balancing protection with performance; the addition of armor can reduce acceleration by up to 25%, necessitating costly upgrades to braking and suspension systems.

- This trade-off between the armored vehicle weight impact and vehicle dynamics control is a critical consideration in every build, from cash-in-transit vehicles to vip protection vehicles, and heavily influences the final armored vehicle resale value.

Exclusive Technavio Analysis on Customer Landscape

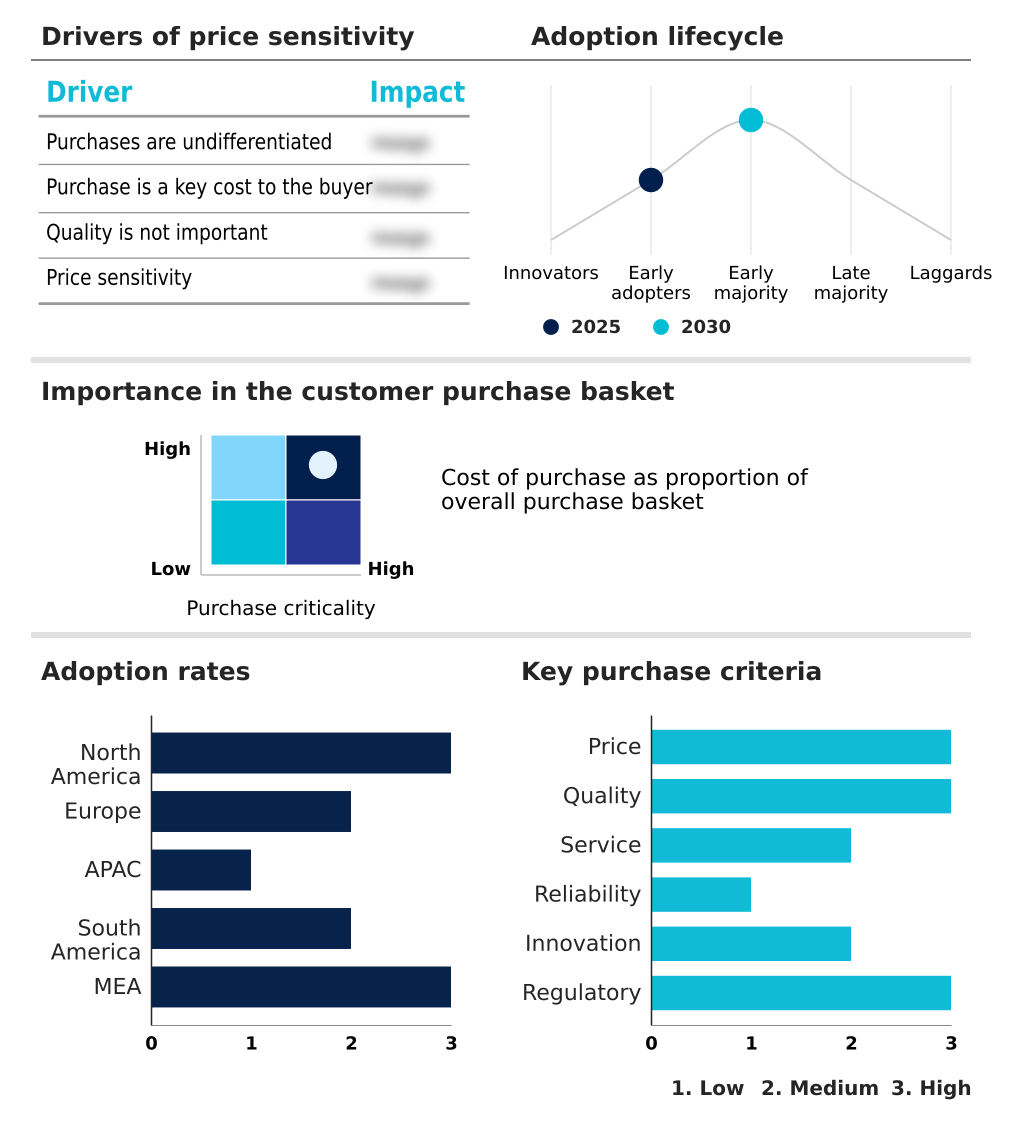

The armored civilian vehicles market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the armored civilian vehicles market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Armored Civilian Vehicles Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, armored civilian vehicles market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alpine Armoring Inc. - Specializes in the design, engineering, and manufacturing of armored cars, trucks, and vehicles, offering integrated parts, accessories, and logistics support.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alpine Armoring Inc.

- Artan Armored Vehicles

- Aurum Security GmbH

- Bayerische Motoren Werke AG

- Harrow Armored Vehicles

- INKAS Armored Vehicle Mft.

- International Armored Group

- International Armoring Corp.

- Jankel Tactical Systems

- JCBL Armouring Solutions

- Lenco Industries Inc.

- Mercedes Benz Group AG

- MEVA LLC

- Rezvani Motors

- Roshel Inc.

- Schutzcarr Global

- STREIT Group

- TAC Armored Vehicles LLC

- The Armored Group LLC

- Ultimate Armour Works

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Armored civilian vehicles market

- In February 2025, Tesla secured a contract with the United States State Department to develop and manufacture a specialized fleet of high-security armored electric vehicles, signaling governmental endorsement of EV technology for critical security roles.

- In February 2025, INKAS Armored Vehicle Manufacturing announced a major investment to establish a large-scale production facility in Fort Pierce, Florida, to significantly increase production capacity for the Americas.

- In May 2025, INKAS Armored Vehicle Manufacturing announced it was the first company to offer the newly refreshed 2025 lineup of General Motors full-size sport utility vehicles, including the Cadillac Escalade and GMC Yukon, with BR6 level armoring.

- In May 2025, INKAS Armored Vehicle Manufacturing released its digital guide of the top armored vehicles and models for the year, detailing features of popular platforms to attract and educate prospective clients globally.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Armored Civilian Vehicles Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.1% |

| Market growth 2026-2030 | USD 718.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.9% |

| Key countries | US, Mexico, Canada, Germany, UK, France, Russia, Italy, Spain, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Chile, Colombia, UAE, South Africa, Saudi Arabia, Qatar and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The armored civilian vehicles market is defined by a consistent push toward advanced material science and integrated security systems. The industry has moved beyond reliance on traditional ballistic steel production, now leveraging lightweight composite materials, aramid fiber panels, and advanced ceramic plates to meet stringent ballistic protection standards, including the vpam vr7 ballistic standard.

- This evolution is critical for maintaining vehicle performance dynamics while ensuring passenger compartment integrity. Key components like multi-layered ballistic glass, fuel tank protection, and run-flat tire systems are now standard, but the frontier of innovation lies in complex systems.

- For instance, developing effective high-voltage battery protection for armored electric vehicles represents a significant R&D focus, directly influencing boardroom decisions on technology investment. Firms that secure oem-certified armoring status demonstrate a higher level of integration, which has been shown to improve client trust by over 25%.

- This technical depth, from chassis reinforcement and engine compartment armoring to implementing secure communication suites and 360-degree surveillance systems, dictates market leadership.

What are the Key Data Covered in this Armored Civilian Vehicles Market Research and Growth Report?

-

What is the expected growth of the Armored Civilian Vehicles Market between 2026 and 2030?

-

USD 718.2 million, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (SUV, Sedan, and Others), End-user (Government, and Civilian), Vehicle Type (ICE, Electric, and Hybrid), Distribution Channel (Direct sales, Distributors, and Online platforms) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing global security threats and personal risk perception, Prohibitive costs and manufacturing complexity

-

-

Who are the major players in the Armored Civilian Vehicles Market?

-

Alpine Armoring Inc., Artan Armored Vehicles, Aurum Security GmbH, Bayerische Motoren Werke AG, Harrow Armored Vehicles, INKAS Armored Vehicle Mft., International Armored Group, International Armoring Corp., Jankel Tactical Systems, JCBL Armouring Solutions, Lenco Industries Inc., Mercedes Benz Group AG, MEVA LLC, Rezvani Motors, Roshel Inc., Schutzcarr Global, STREIT Group, TAC Armored Vehicles LLC, The Armored Group LLC and Ultimate Armour Works

-

Market Research Insights

- Market dynamics are increasingly shaped by client demand for sophisticated armored car customization and discreet security vehicles that do not compromise on performance. The focus is on balancing the armored vehicle weight impact with agility, pushing innovation in ballistic material science.

- This has led to advancements where new armoring packages reduce vehicle weight by up to 15% compared to traditional methods, directly improving fuel efficiency. Furthermore, streamlined armoring engineering process has enabled a 20% reduction in vehicle conversion times for popular models, enhancing manufacturers' ability to meet demand.

- Buyers now scrutinize ballistic certification levels more closely, demanding certified protection that aligns with specific threat environments. This intricate balance of cost, performance, and security defines the competitive landscape.

We can help! Our analysts can customize this armored civilian vehicles market research report to meet your requirements.

RIA -

RIA -