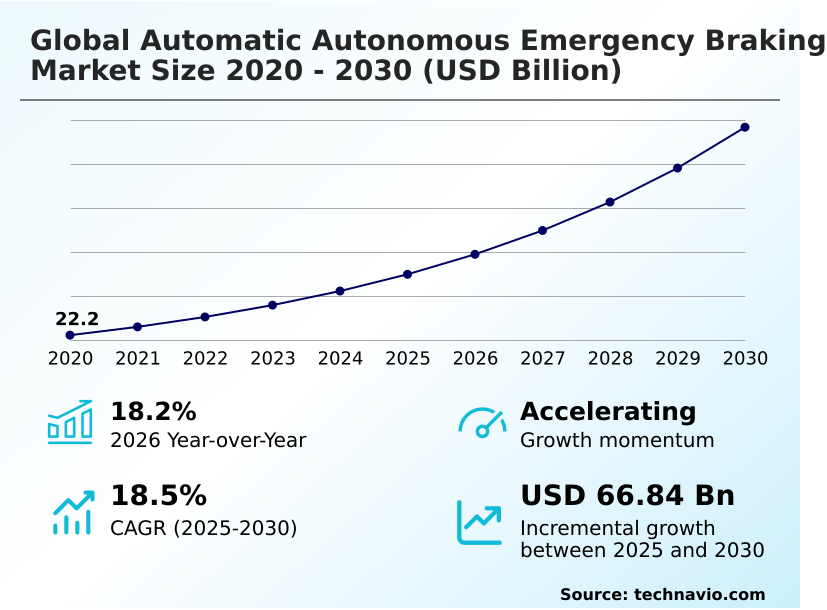

Automatic Autonomous Emergency Braking Market Size 2026-2030

The automatic autonomous emergency braking market size is valued to increase by USD 66.84 billion, at a CAGR of 18.5% from 2025 to 2030. Stringent government regulations and proactive safety mandates will drive the automatic autonomous emergency braking market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 39.6% growth during the forecast period.

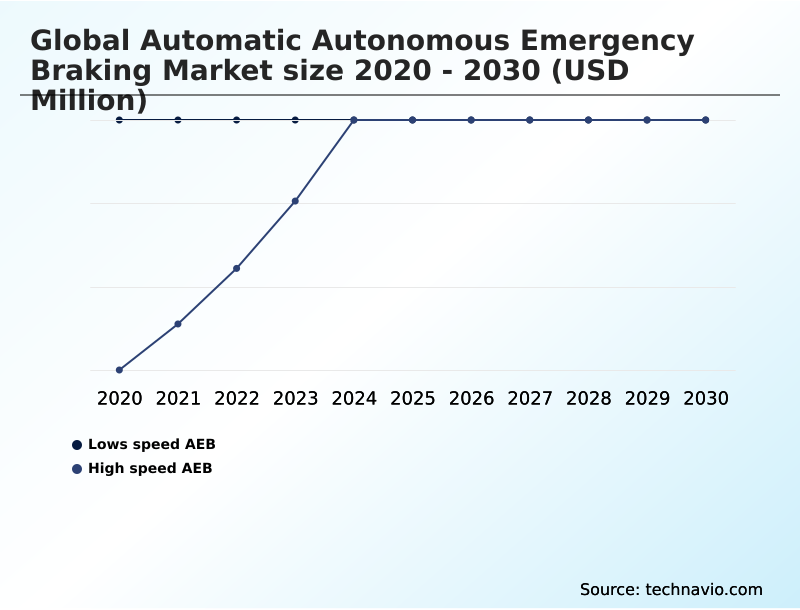

- By Type - Lows speed AEB segment was valued at in 2024

- By Technology - Radar based AEB segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 94.51 billion

- Market Future Opportunities: USD 66.84 billion

- CAGR from 2025 to 2030 : 18.5%

Market Summary

- The automatic autonomous emergency braking market is experiencing profound growth, driven by a powerful confluence of stringent global regulations, rapid technological innovation, and escalating consumer demand for safety. This expansion is transforming AEB from a standalone feature into a foundational element of the broader ecosystem of advanced driver assistance systems and the progression toward fully autonomous driving.

- The industry is witnessing a decisive shift toward sophisticated sensor fusion architectures, where data from high-resolution cameras, 4D imaging radar, and increasingly affordable solid-state LiDAR are intelligently combined. For instance, fleet management operations are leveraging these advancements to reduce accident rates, which directly lowers insurance premiums and vehicle downtime.

- This focus on tangible safety outcomes and operational efficiency underscores the technology's critical role in both new passenger vehicles and the rapidly expanding commercial vehicle sector, where mandates are creating a non-negotiable demand floor.

What will be the Size of the Automatic Autonomous Emergency Braking Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automatic Autonomous Emergency Braking Market Segmented?

The automatic autonomous emergency braking industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Low speed AEB

- High speed AEB

- Technology

- Radar based AEB

- Camera based AEB

- LiDAR based AEB

- Ultrasonic based AEB

- Others

- Vehicle type

- Passenger cars

- Commercial vehicles

- Others

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The low speed aeb segment is estimated to witness significant growth during the forecast period.

The low speed AEB segment is crucial for mitigating collisions in urban settings, where systems are optimized for speeds where most accidents with vulnerable road users occur.

These systems utilize a multi-sensor redundancy approach, fusing data from radar based AEB, camera based AEB, and ultrasonic based AEB, with LiDAR based AEB becoming more common in premium applications.

This architecture is essential for improving autonomous braking performance metrics and avoiding false activations in cluttered environments.

A recent pilot program demonstrated a 60% reduction in near-miss incidents with cyclists by incorporating vehicle to everything communication, highlighting a future where connected infrastructure provides another critical layer of safety and enhances system effectiveness.

The Low speed AEB segment was valued at in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

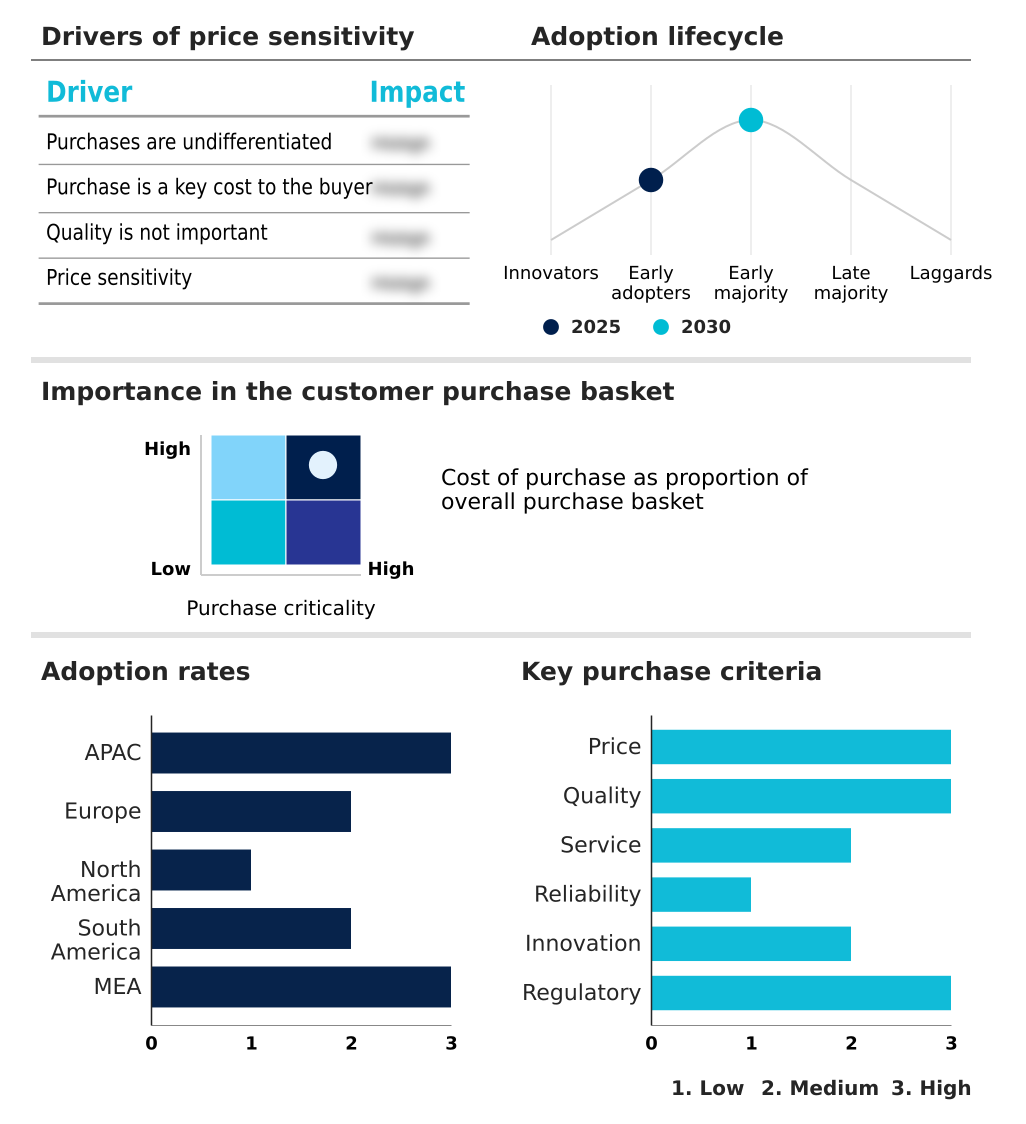

APAC is estimated to contribute 39.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automatic Autonomous Emergency Braking Market Demand is Rising in APAC Get Free Sample

The geographic landscape for automatic autonomous emergency braking is diverse, with APAC poised to contribute nearly 40% of the market's incremental growth.

Mature markets in Europe and North America focus on refining advanced driver assistance systems for vulnerable road user protection, driven by robust safety programs that emphasize nighttime AEB effectiveness and stringent pedestrian emergency braking standards.

In contrast, emerging economies are shaped by government mandates and cost sensitivity, particularly for AEB for commercial vehicles.

The pedestrian detection algorithm and cyclist detection system must be calibrated for unique regional traffic, such as the high density of two-wheelers in certain APAC nations, which challenges cyclist detection in urban environments.

The rollout of advanced features like junction turn assist varies significantly by region.

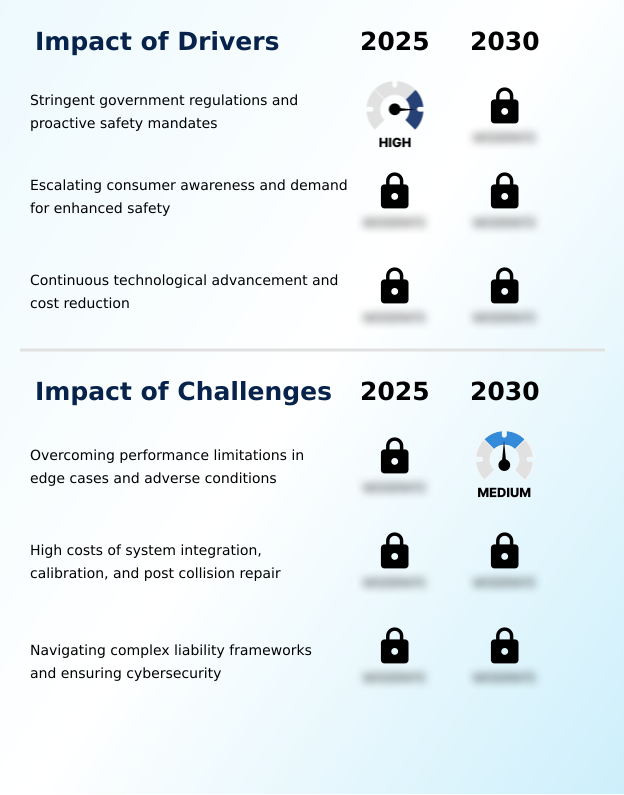

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic landscape of the automatic autonomous emergency braking market is increasingly defined by complex technical challenges and specialized use cases. A primary focus for developers is ensuring reliable aeb system performance in adverse weather conditions and developing robust aeb for complex edge cases.

- This is achieved through advanced sensor fusion algorithms for vulnerable road user detection and sophisticated ai models for predictive emergency braking intent. The impact of 4d imaging radar on aeb accuracy has been significant, though questions around radar versus lidar effectiveness in aeb systems persist.

- The industry is also grappling with the total cost of ownership for aeb systems, where challenges in aeb system post-collision repair are a major concern. Addressing cybersecurity vulnerabilities in connected aeb platforms and clarifying liability frameworks for autonomous braking failures are critical for market acceptance.

- Architecturally, the trend is toward aeb integration into centralized vehicle architectures and brake-by-wire integration for faster aeb response, which is vital for both high-speed aeb performance for highway scenarios and low-speed aeb effectiveness in stop-and-go traffic.

- New performance standards for aeb on heavy trucks are creating a distinct sub-market, while improving the real-world performance of pedestrian detection systems and aeb system validation for motorcycle detection remains a priority. This includes enhancing aeb functionality for intersection turning assist and reducing false positives in camera-based aeb, often through enhancing aeb with vehicle-to-everything data.

What are the key market drivers leading to the rise in the adoption of Automatic Autonomous Emergency Braking Industry?

- Stringent government regulations and proactive safety mandates, designed to reduce traffic fatalities, are key drivers propelling market expansion and technological adoption.

- Relentless technological innovation is a critical driver, with predictive AEB software transforming system capabilities. Modern advanced driver assistance systems depend on the performance and affordability of their underlying components.

- AI powered perception, in compliance with ISO 26262 functional safety standards, has revolutionized automotive perception software, allowing systems to move from reactive to predictive capability.

- Sensor fusion combines data from multiple sources, with some chipsets delivering a fourfold increase in angular resolution.

- This enables effective high-speed AEB managed by a centralized domain controller that orchestrates everything from sensor inputs to brake-by-wire systems for the 2028 model year and beyond, ensuring that the final AEB system calibration delivers optimal and safe performance.

What are the market trends shaping the Automatic Autonomous Emergency Braking Industry?

- The proliferation of sensor fusion and AI-powered perception represents a transformative market trend. This evolution enhances system capabilities by integrating multiple data streams for more reliable and nuanced environmental interpretation.

- The market is rapidly advancing beyond single-sensor systems toward a sophisticated sensor fusion architecture powered by AI. Where early systems had weaknesses, the current trend involves the collision avoidance technology integration of data from 8-megapixel cameras, 4D imaging radar, and solid-state LiDAR for a detailed environmental model. This approach enhances object classification accuracy and system confidence before braking.

- The use of specialized processors with a dedicated neural processing unit provides an efficient computational backbone. The evolution includes advancements like thermal imaging for AEB to improve performance and enabling over the air updates for AEB, which is critical for the continuous improvement of systems, particularly in AEB for electric vehicles where software-defined features are paramount.

What challenges does the Automatic Autonomous Emergency Braking Industry face during its growth?

- A key challenge restraining market growth involves overcoming system performance limitations, particularly in handling unpredictable edge cases and maintaining reliability in adverse environmental conditions.

- Performance variability in non-ideal conditions remains a primary challenge, as achieving full all-weather system capabilities is difficult. Edge case scenario handling is another significant hurdle, as systems may fail to react to unique situations, compromising reliability. This can lead to a need for AEB false positive reduction.

- The high cost of the sensor recalibration process post-collision significantly impacts ownership, with some data showing repair costs surging over 30%. Furthermore, ensuring robust cybersecurity for AEB systems through measures like end-to-end encryption is paramount as vehicles become more connected. These challenges affect both low-speed AEB in urban areas and reverse AEB functionality, requiring adherence to stringent regulatory test protocols.

Exclusive Technavio Analysis on Customer Landscape

The automatic autonomous emergency braking market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automatic autonomous emergency braking market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automatic Autonomous Emergency Braking Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automatic autonomous emergency braking market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AISIN Corp. - Analyzes offerings of radar and camera-based AEB systems designed for comprehensive collision mitigation, providing critical warnings and full emergency braking to protect vehicles, pedestrians, and cyclists.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN Corp.

- Analog Devices Inc.

- Aptiv Plc

- Autoliv Inc.

- Continental AG

- DENSO Corp.

- HELLA GmbH and Co. KGaA

- Hitachi Astemo Ltd.

- Hyundai Mobis Co. Ltd.

- Infineon Technologies AG

- Magna International Inc.

- Mobileye Technologies Ltd.

- NXP Semiconductors NV

- Robert Bosch GmbH

- Teledyne FLIR LLC

- Texas Instruments Inc.

- Valeo SA

- Veoneer Inc.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automatic autonomous emergency braking market

- In August, 2025, Aptiv Plc demonstrated a new predictive AEB software architecture at a major industry trade show, using a deep learning model to analyze pedestrian posture and gait to predict roadway entry.

- In April, 2025, Infineon Technologies AG announced the volume production of its next-generation automotive radar chipset, which offers a fourfold increase in angular resolution compared to its predecessor.

- In March, 2025, NXP Semiconductors NV officially launched its next-generation S32 family of automotive processors, featuring a dedicated neural processing unit to accelerate real-time sensor fusion and AI-based object recognition.

- In December, 2025, Magna International Inc. unveiled an innovative and highly integrated front fascia module for electric vehicles, which seamlessly incorporates an 8-megapixel camera, a solid-state LiDAR sensor, and an imaging radar.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automatic Autonomous Emergency Braking Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 315 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.5% |

| Market growth 2026-2030 | USD 66835.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 18.2% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automatic autonomous emergency braking market is defined by a complex interplay of technologies. A modern sensor fusion architecture is now standard, integrating radar based aeb, camera based aeb, and increasingly, lidar based aeb and ultrasonic based aeb for different scenarios. The goal is to enhance vulnerable road user protection through superior object classification accuracy.

- This requires sophisticated ai powered perception and predictive aeb software, managed by a centralized domain controller that also commands brake by wire systems. For automakers, the focus is on both high speed aeb for highways and low speed aeb for urban safety, including junction turn assist and reverse aeb functionality.

- However, achieving flawless all weather system capabilities and robust edge case scenario handling remains a challenge, with some systems demonstrating a fourfold increase in resolution to address this. The sensor recalibration process after minor incidents adds to ownership costs.

- Ensuring the performance of the pedestrian detection algorithm and cyclist detection system is critical for top safety ratings within the broader advanced driver assistance systems landscape.

What are the Key Data Covered in this Automatic Autonomous Emergency Braking Market Research and Growth Report?

-

What is the expected growth of the Automatic Autonomous Emergency Braking Market between 2026 and 2030?

-

USD 66.84 billion, at a CAGR of 18.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Lows speed AEB, and High speed AEB), Technology (Radar based AEB, Camera based AEB, LiDAR based AEB, Ultrasonic based AEB, and Others), Vehicle Type (Passenger cars, Commercial vehicles, and Others) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Stringent government regulations and proactive safety mandates, Overcoming performance limitations in edge cases and adverse conditions

-

-

Who are the major players in the Automatic Autonomous Emergency Braking Market?

-

AISIN Corp., Analog Devices Inc., Aptiv Plc, Autoliv Inc., Continental AG, DENSO Corp., HELLA GmbH and Co. KGaA, Hitachi Astemo Ltd., Hyundai Mobis Co. Ltd., Infineon Technologies AG, Magna International Inc., Mobileye Technologies Ltd., NXP Semiconductors NV, Robert Bosch GmbH, Teledyne FLIR LLC, Texas Instruments Inc., Valeo SA, Veoneer Inc. and ZF Friedrichshafen AG

-

Market Research Insights

- Market dynamics are shaped by the need for robust active safety system validation and precise AEB system calibration. The collision avoidance technology integration is advancing rapidly, with an ongoing AEB sensor technology comparison driving innovation in radar, camera, and LiDAR.

- Key areas of focus include improving nighttime AEB effectiveness and ensuring AEB for commercial vehicles meets stringent AEB regulatory test protocols. Pedestrian emergency braking standards and enhancing cyclist detection in urban environments are paramount.

- Firms are leveraging over the air updates for AEB to improve automotive perception software and achieve AEB false positive reduction, which is critical for AEB system reliability testing.

- With connectivity, vehicle to everything communication and thermal imaging for AEB are emerging as key enablers, while strong cybersecurity for AEB systems and adherence to ISO 26262 functional safety are non-negotiable, especially in AEB for electric vehicles where multi-sensor AEB redundancy is critical.

We can help! Our analysts can customize this automatic autonomous emergency braking market research report to meet your requirements.

RIA -

RIA -