Automotive Intelligent Rearview Mirror Market Size 2026-2030

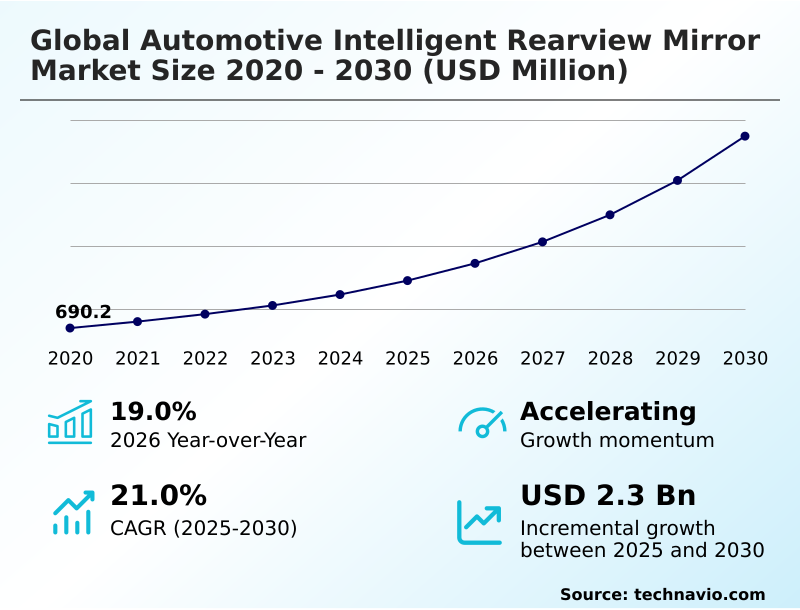

The automotive intelligent rearview mirror market size is valued to increase by USD 2.30 billion, at a CAGR of 21% from 2025 to 2030. Growing popularity of luxury vehicles will drive the automotive intelligent rearview mirror market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 33.8% growth during the forecast period.

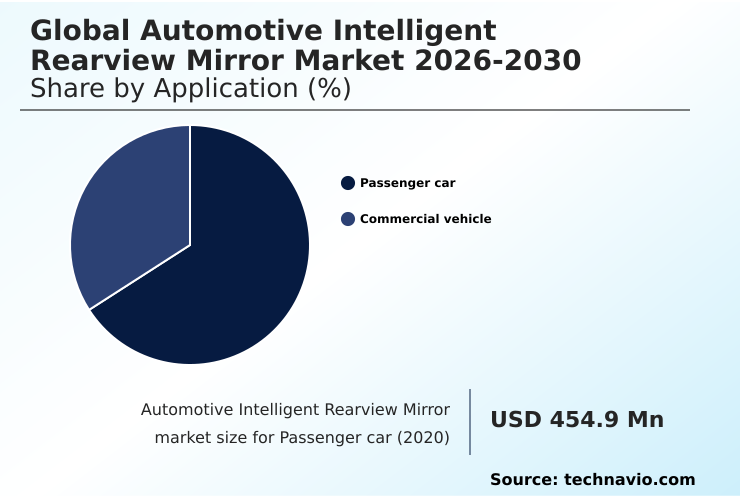

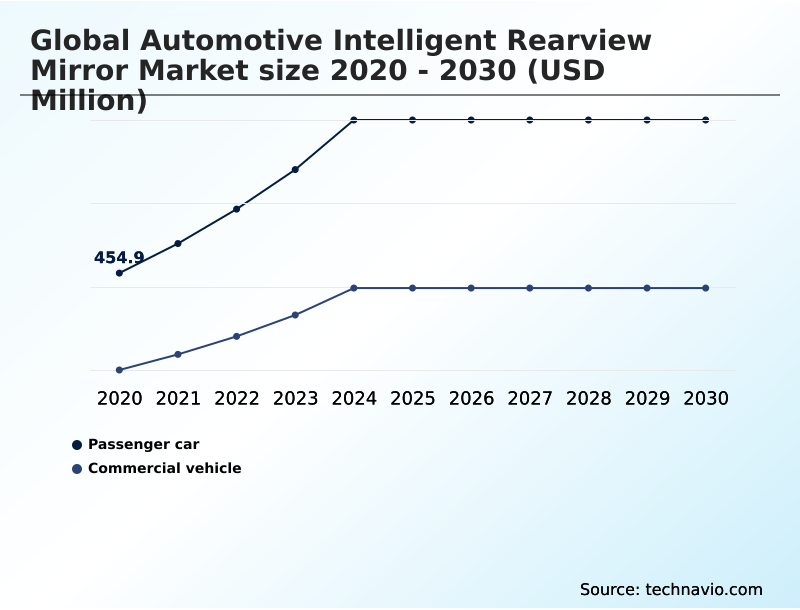

- By Application - Passenger car segment was valued at USD 801.9 million in 2024

- By Channel - OEM segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.05 billion

- Market Future Opportunities: USD 2.30 billion

- CAGR from 2025 to 2030 : 21%

Market Summary

- The automotive intelligent rearview mirror market is rapidly evolving from a simple reflective surface into a sophisticated hub for vehicle data and driver assistance. This transformation is propelled by the integration of advanced driver-assistance systems (ADAS), where the mirror housing becomes a prime location for sensor fusion, incorporating cameras and processors for features like blind-spot monitoring and lane departure warnings.

- The imperative for aerodynamic efficiency in electric vehicles is also a significant driver, with camera monitor systems replacing traditional side mirrors to extend range. For instance, some platforms now eliminate the rear window entirely, relying on a high-definition digital video feed to provide a panoramic view, a design choice that improves both aerodynamics and interior space.

- Concurrently, trends such as biometric authentication, over-the-air (OTA) updates, and augmented reality overlays are turning the mirror into a connected, updatable component of the software-defined vehicle. However, the industry grapples with challenges including complex global supply chains for electronic components and a fragmented regulatory landscape that requires costly, region-specific homologation processes.

What will be the Size of the Automotive Intelligent Rearview Mirror Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Intelligent Rearview Mirror Market Segmented?

The automotive intelligent rearview mirror industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Passenger car

- Commercial vehicle

- Channel

- OEM

- Aftermarket

- Powertrain type

- ICE

- Electric

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Application Insights

The passenger car segment is estimated to witness significant growth during the forecast period.

The passenger car segment is experiencing a significant design evolution, driven by the integration of intelligent vision systems that replace traditional optical glass.

This transition enables new vehicle architectures, such as designs without rear windows, which rely on a high-definition digital video feed for a complete panoramic view.

The adoption of a full display mirror within the digital cockpit is not just an aesthetic upgrade; it is a functional necessity that eliminates blind spots from pillars and cargo.

These camera-based monitoring systems are central to enhancing aerodynamic profiles, particularly in electric vehicles, where a reduction in drag coefficient of just 2.5% can extend operational range.

As high-definition displays become standard, the digital rear view is established as a primary source of situational awareness, fundamentally altering the human-machine interface for drivers.

The Passenger car segment was valued at USD 801.9 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

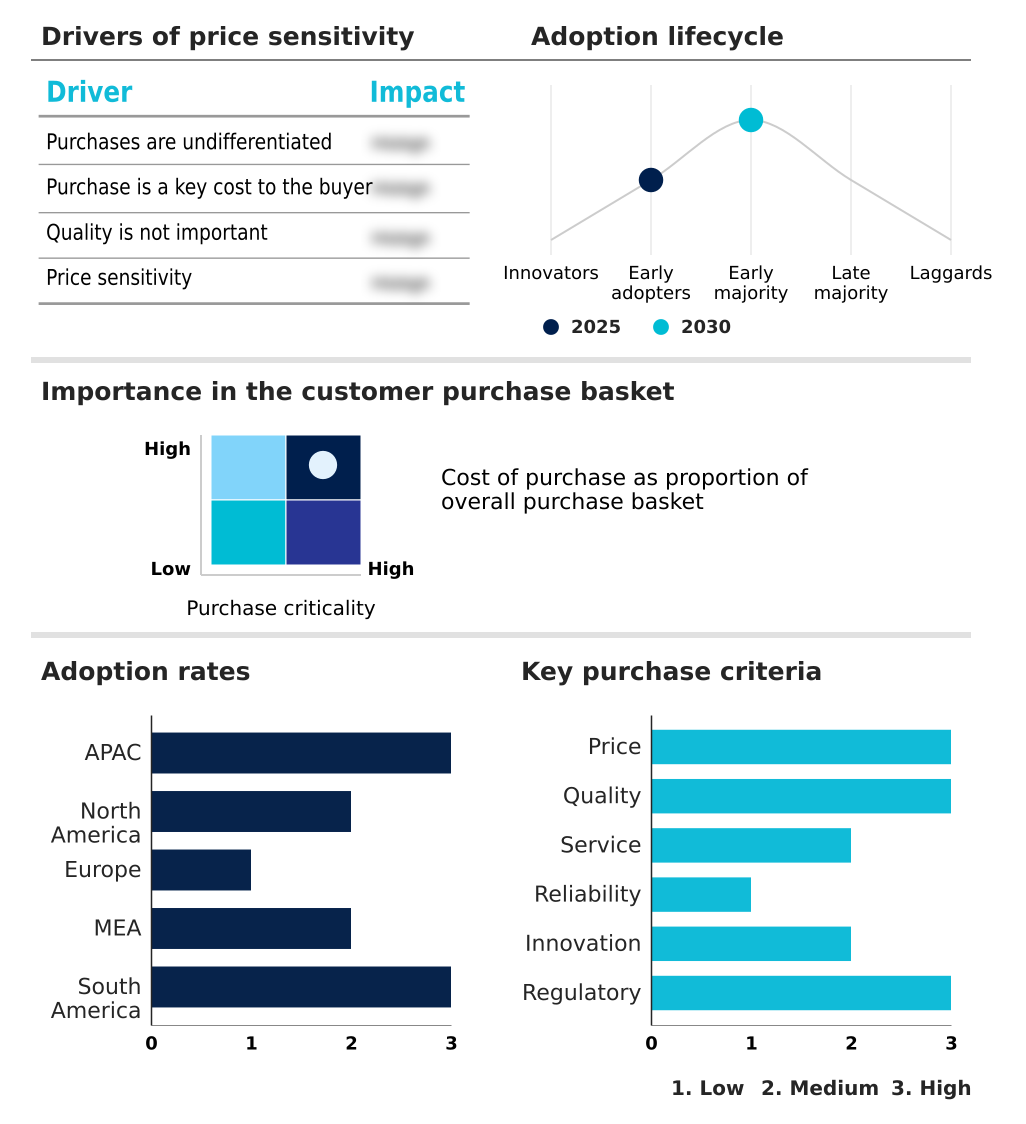

APAC is estimated to contribute 33.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Intelligent Rearview Mirror Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the market is characterized by distinct regional drivers and adoption rates.

APAC is the largest contributor to incremental growth, accounting for over 33% of the market expansion, fueled by high-tech consumer demand and a robust manufacturing ecosystem for advanced vision products.

In Europe, which is forecast to expand at a rate of 21.9%, strict regulatory mandates for driver state monitoring and ADAS-enabled smart vision are compelling the integration of in-cabin monitoring.

North America follows closely with a projected growth rate of 21.5%, where demand is driven by the utility of smart vision systems in large SUVs and commercial trucks.

The deployment of 5G connectivity is enabling the development of an intelligent transportation network, where connected mobility and camera-integrated digital rearview mirror systems share data to improve overall road safety across these key regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The application of intelligent rearview mirrors is diversifying to address specific operational needs and deliver measurable returns. For commercial vehicles, the adoption of camera monitor systems is a strategic decision rooted in efficiency.

- The debate over digital mirror vs traditional mirror is often settled by performance data; fleets utilizing camera-based systems report a nearly 3% improvement in fuel economy compared to those with traditional mirrors, directly impacting operational costs. For drivers of large SUVs, an intelligent rearview mirror for towing provides an unobstructed view, a critical safety benefit that optical mirrors cannot offer.

- In the aftermarket, smart mirror installation allows owners of older vehicles to access modern ADAS integration in rearview mirror functions. The benefits of camera monitor systems extend beyond fuel savings to include enhanced safety, a key consideration for intelligent mirror for fleet management.

- As driver monitoring system regulations become stricter, the inclusion of biometric authentication in vehicle mirrors is transitioning from a luxury feature to a compliance tool. The legal requirements for digital mirrors are solidifying, ensuring that systems replacing side mirrors with cameras provide fail-safe performance.

- This evolution is also driving innovation in the intelligent mirror human-machine interface design, with features like augmented reality mirror navigation becoming more common. OEMs and aftermarket suppliers must now weigh the different value propositions, as oem vs aftermarket intelligent mirrors offer distinct levels of vehicle integration.

- For instance, intelligent mirrors with 5g connectivity and cloud storage offer advanced data capabilities, while thermal imaging rearview mirror benefits provide unparalleled night vision. This is particularly relevant for the intelligent mirror for electric vehicles, where every component must contribute to both safety and efficiency.

- Finally, ensuring cybersecurity for connected car mirrors is a paramount challenge as these devices become more integrated.

What are the key market drivers leading to the rise in the adoption of Automotive Intelligent Rearview Mirror Industry?

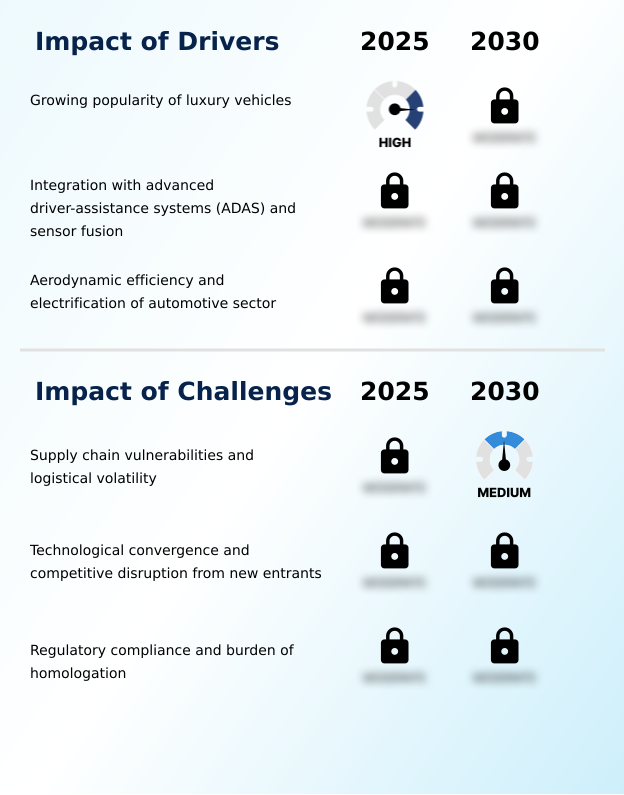

- The growing popularity of luxury vehicles, which increasingly feature advanced technologies, serves as a key driver for the market.

- Market growth is fundamentally driven by the mirror's evolving role as a centralized hub for the ADAS suite and the broader smart cockpit ecosystem.

- The integration of driver monitoring systems and advanced driver-assistance systems (ADAS) within a single unit streamlines vehicle architecture and enhances the human-machine interface (HMI).

- This sensor fusion creates a robust platform for vision assistance systems, which have been shown to reduce accident rates in equipped vehicles by up to 15%.

- The demand for a seamless smart mirror and driver vision solution is also propelled by the electrification trend, where replacing traditional mirrors with camera monitor systems can improve aerodynamic efficiency by 2-3%.

- This enhancement directly translates to extended battery range, a critical selling point in the competitive EV space.

What are the market trends shaping the Automotive Intelligent Rearview Mirror Industry?

- A key market trend is the integration of biometric authentication with driver monitoring systems. This convergence is reshaping in-cabin safety and personalization.

- Key market trends are centered on transforming the rearview mirror into a multi-functional, connected device. The integration of rear-vision technology with interior sensing capabilities is paramount, with new systems capable of processing biometric data up to 40% faster than previous generations. This enables seamless driver identification and personalization.

- Augmented reality overlays are moving beyond navigation to include active visual assistance, projecting real-time safety alerts directly onto the digital display. Furthermore, the connected cockpit concept is being realized through cloud connectivity and over-the-air (OTA) updates, allowing for new features and security patches to be deployed remotely.

- The adoption rate for mirrors with these integrated features is growing by more than 25% annually in premium vehicle segments, highlighting a clear consumer demand for a more interactive and secure in-vehicle experience.

What challenges does the Automotive Intelligent Rearview Mirror Industry face during its growth?

- Supply chain vulnerabilities and logistical volatility present a key challenge affecting industry growth.

- The market faces significant hurdles related to technological convergence and regulatory complexity. As camera-supported smart mirror systems become standard, manufacturers must navigate a fragmented global landscape of safety standards, which can increase compliance costs by as much as 30%. The transition to the software-defined vehicle (SDV) introduces challenges in ensuring robust cybersecurity solutions and reliable electromechanical redundancy.

- Supply chain volatility for high-performance components like digital display-based intelligent mirror panels remains a primary concern, with disruptions leading to production delays and increased costs.

- Furthermore, the need for adas-enabled smart vision and digital mirror replacement systems to offer flawless performance in all weather conditions requires significant R&D investment, particularly in areas like advanced hydrophobic coatings and thermal management for electronics.

Exclusive Technavio Analysis on Customer Landscape

The automotive intelligent rearview mirror market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive intelligent rearview mirror market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Intelligent Rearview Mirror Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive intelligent rearview mirror market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Continental AG - Offerings include advanced camera-integrated digital rearview mirror systems that enhance driver visibility and safety through innovative vision and sensor technologies.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Continental AG

- FLABEG Automotive Glass

- Ford Motor Co.

- Gentex Corp.

- KDC Auto Industry Co.

- Kocchi Technology Ltd.

- Magna International Inc.

- MEKRA Lang GmbH and Co. KG

- Murakami Corp.

- Nissan Motor Co. Ltd.

- Panasonic Holdings Corp.

- Pioneer Corp.

- Robert Bosch GmbH

- Samsung Electronics Co. Ltd.

- Shenzhen Jimi IoT Co. Ltd.

- SUBARU Corp.

- Valeo SA

- Varroc Engineering Ltd.

- VOXX International Corp.

- Xiaomi Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive intelligent rearview mirror market

- In August, 2024, Mazda Australia introduced a digital rearview mirror as a genuine accessory for its CX-90 and CX-60 models, targeting consumers who need unobstructed visibility while towing or carrying cargo.

- In September, 2024, Stoneridge Inc. showcased its latest MirrorEye Camera Monitor System at the IAA Transportation exhibition, releasing field test data showing a 2.5% fuel economy improvement for fleets using the system.

- In November, 2024, Qualcomm Technologies collaborated with a Tier 1 supplier to demonstrate a Snapdragon-powered smart mirror architecture featuring integrated 5G connectivity and a community safety mode for sharing road hazard data.

- In January, 2025, Gentex Corporation unveiled a new Full Display Mirror at CES, which integrated a comprehensive biometrics suite for driver identification and V2H connectivity for smart home control.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Intelligent Rearview Mirror Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21% |

| Market growth 2026-2030 | USD 2298.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.0% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, South Africa, UAE, Turkey, Egypt, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a profound technological shift, where the rearview mirror is being reimagined as a central node for the digital cockpit. This evolution is driven by the convergence of full display mirror technology with advanced driver-assistance systems (ADAS) and in-cabin monitoring capabilities.

- The integration of driver monitoring systems, including eye tracking and head position detection, is no longer a novelty but a critical component for meeting global safety regulations, directly influencing boardroom decisions on compliance and risk management.

- Systems now achieve sensor fusion by combining data from multiple inputs to provide unparalleled situational awareness, reducing blind spots by over 50% compared to traditional mirrors. Innovations such as biometric authentication through iris scanning and facial recognition are enabling enhanced vehicle security and personalization.

- The move toward the software-defined vehicle (SDV) is further accelerating this trend, with over-the-air (OTA) updates, cloud connectivity, and edge computing capabilities transforming static hardware into evolving platforms. Features like augmented reality overlays, 5g connectivity, and night vision enhancement are becoming key differentiators, while electrowetting technology and hydrophobic coatings address practical performance challenges.

What are the Key Data Covered in this Automotive Intelligent Rearview Mirror Market Research and Growth Report?

-

What is the expected growth of the Automotive Intelligent Rearview Mirror Market between 2026 and 2030?

-

USD 2.30 billion, at a CAGR of 21%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Passenger car, and Commercial vehicle), Channel (OEM, and Aftermarket), Powertrain Type (ICE, and Electric) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Growing popularity of luxury vehicles, Supply chain vulnerabilities and logistical volatility

-

-

Who are the major players in the Automotive Intelligent Rearview Mirror Market?

-

Continental AG, FLABEG Automotive Glass, Ford Motor Co., Gentex Corp., KDC Auto Industry Co., Kocchi Technology Ltd., Magna International Inc., MEKRA Lang GmbH and Co. KG, Murakami Corp., Nissan Motor Co. Ltd., Panasonic Holdings Corp., Pioneer Corp., Robert Bosch GmbH, Samsung Electronics Co. Ltd., Shenzhen Jimi IoT Co. Ltd., SUBARU Corp., Valeo SA, Varroc Engineering Ltd., VOXX International Corp. and Xiaomi Inc.

-

Market Research Insights

- The market's dynamism is rooted in the shift toward the connected cockpit, where intelligent vision systems are pivotal. Advanced rear-vision technology offers more than just a clearer view; it integrates interior sensing capabilities to enhance safety, with some systems reducing driver distraction events by up to 20%.

- The adoption of plug-and-play solutions in the aftermarket brings modern vision assistance systems to a wider range of vehicles, expanding market reach. This evolution is transforming the mirror into a secondary infotainment hub, with adoption rates in mid-tier vehicles increasing by over 15% in recent years.

- The focus on hands-free voice control and panoramic lens configurations in newer models underscores the consumer demand for both convenience and comprehensive situational awareness, redefining the role of the rearview display.

We can help! Our analysts can customize this automotive intelligent rearview mirror market research report to meet your requirements.

RIA -

RIA -