Automotive Advanced Driver Assistance System Market Size 2025-2029

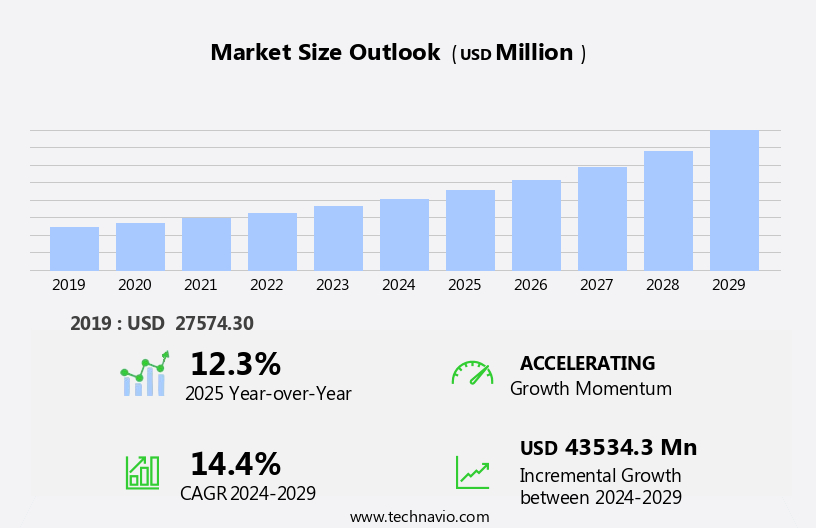

The automotive advanced driver assistance system (ADAS) market size is forecast to increase by USD 43.53 billion, at a CAGR of 14.4% between 2024 and 2029.

- The market is experiencing significant growth, driven primarily by the declining prices of sensors used in these systems. This affordability trend is enabling the mass adoption of ADAS technologies, making them increasingly accessible to a broader consumer base. Simultaneously, the development of Artificial Intelligence (AI) in ADAS solutions is revolutionizing the automotive industry, offering enhanced safety features and improved driving experiences. However, the market faces challenges that require strategic navigation. One such challenge is the high costs associated with servicing and maintaining these advanced systems.

- As technology advances, the complexity of ADAS increases, leading to higher repair and replacement costs. Companies must address this challenge by exploring cost-effective service models or developing more robust, durable components to reduce maintenance requirements. By capitalizing on the market's growth drivers while effectively managing challenges, organizations can seize opportunities and maintain a competitive edge in the evolving ADAS landscape. As the market continues to evolve, companies must navigate these challenges while capitalizing on the opportunities presented by declining sensor prices and the advancement of AI-enabled technologies.

What will be the Size of the Automotive Advanced Driver Assistance System (ADAS) Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, integrating various technologies to enhance vehicle safety and improve the driving experience. Edge computing plays a crucial role in real-time data processing, enabling applications such as lane departure warning, blind spot detection, and automated driving systems. Precision engineering and quality control ensure the reliability and accuracy of vehicle dynamics control, GPS navigation, and camera systems. Semiconductor technology advances fuel the development of high-definition mapping, adaptive cruise control, and machine learning algorithms. Functional safety and regulatory compliance are paramount, with certification standards and algorithm optimization ensuring passenger safety. Radar and lidar sensors, ultrasonic sensors, and traffic sign recognition contribute to data acquisition and real-time processing, enabling features like adaptive headlights and automatic emergency braking.

Vehicle-to-everything (V2X) communication and over-the-air updates facilitate continuous improvement and innovation. The market's unfolding patterns reflect the integration of various technologies, including deep learning models, camera systems, lane keeping assist, and driver monitoring systems. The evolving nature of the ADAS market underscores the importance of ongoing research and development in automotive technology.

How is this Automotive Advanced Driver Assistance System (ADAS) Industry segmented?

The automotive advanced driver assistance system (adas) industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Passenger cars

- Commercial vehicles

- Technology

- AEBS

- TPMS

- PAS

- Others

- Component

- Sensors

- Processor

- Software

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- Japan

- South Korea

- Rest of World (ROW)

- North America

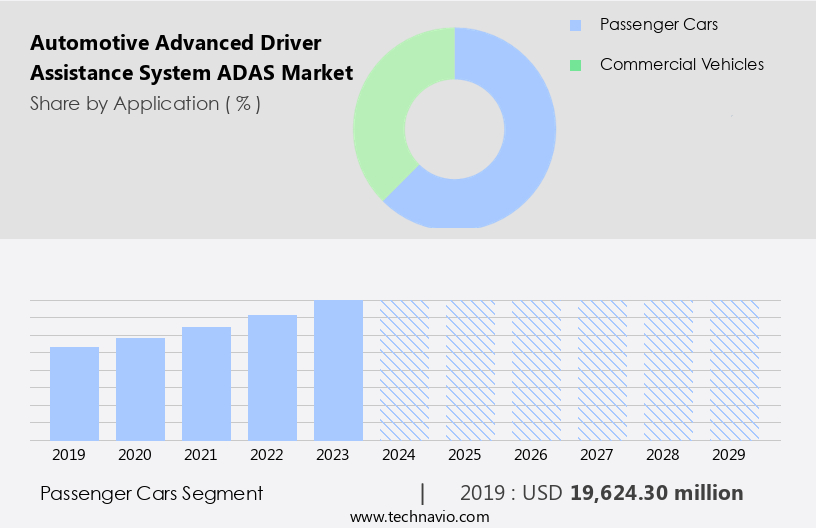

By Application Insights

The passenger cars segment is estimated to witness significant growth during the forecast period. The market is witnessing significant growth due to the increasing adoption of these technologies in passenger cars. Automotive Original Equipment Manufacturers (OEMs) are integrating ADAS features to enhance vehicle safety and differentiate their products in the competitive automotive industry. Developed regions, such as North America and Europe, lead the market, driven by stringent safety regulations, including the US's National Highway Traffic Safety Administration's (NHTSA) 5-Star Safety Ratings program, which highlights ADAS technologies like Automatic Emergency Braking Systems (AEBS), Forward Collision Warning Systems (FCWS), Lane Departure Warning Systems (LDWS), Tire Pressure Monitoring Systems (TPMS), and rear-view video systems. Advancements in technology, such as edge computing, precision engineering, automated driving systems, and sensor fusion, are enabling the development of sophisticated ADAS features like lane keeping assist, blind spot detection, adaptive cruise control, and parking assist.

Real-time data processing, using machine learning algorithms and deep learning models, is crucial for the effective functioning of these systems. Certification standards, such as ISO 26262 for functional safety and regulatory compliance, are essential for ensuring the safety and reliability of these systems. Semiconductor technology, including automotive-grade silicon, plays a crucial role in the development of ADAS components, such as radar sensors, lidar sensors, and camera systems. The integration of cloud computing and vehicle-to-everything (V2X) communication is paving the way for advanced features like over-the-air updates and real-time traffic sign recognition. Passenger safety is a primary concern, leading to the development of advanced driver monitoring systems, adaptive headlights, and night vision.

In summary, the automotive industry's shift towards advanced driver assistance systems is driven by safety regulations, competition, and technological advancements. The integration of various technologies, including edge computing, sensor fusion, and machine learning algorithms, is enabling the development of sophisticated features, ensuring passenger safety, and enhancing the driving experience. Hardware integration, system calibration, and sensor fusion are essential for seamless functionality.

The Passenger cars segment was valued at USD 19.62 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

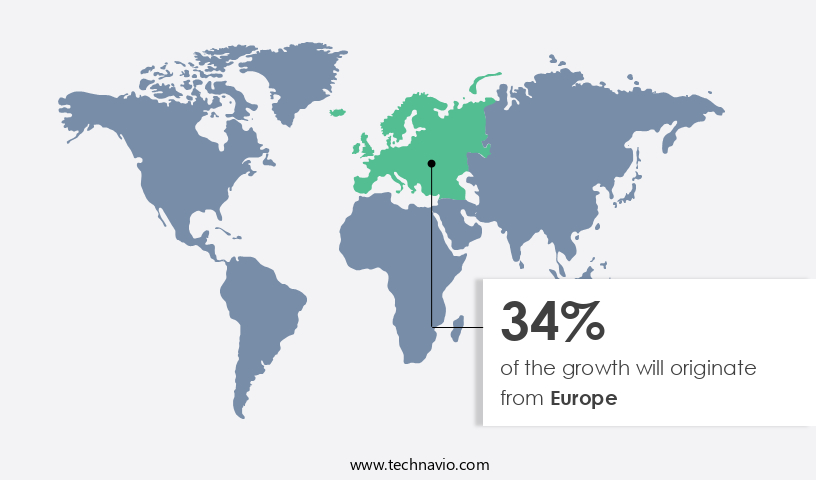

Europe is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The European automotive market is a significant contributor to the global Advanced Driver Assistance System (ADAS) industry, driven by the increasing demand for vehicular safety features in countries like Germany, France, Italy, Spain, and the UK. With major global automotive manufacturers and luxury brands, such as BMW, AUDI AG (AUDI), and Daimler, headquartered in Europe, the region is at the forefront of ADAS adoption. Strict vehicle safety norms enforced by the European Commission, mandating safety technologies in vehicles, further fuel market growth. The European automotive industry is highly competitive, with numerous leading Original Equipment Manufacturers (OEMs) vying for market share.

ADAS technologies, including lane departure warning, precision engineering, automated driving systems, quality control, vehicle dynamics control, GPS navigation, lidar sensors, data processing, real-time processing, radar sensors, blind spot detection, certification standards, deep learning models, testing and validation, vehicle-to-everything (v2x), adaptive headlights, automotive grade silicon, traffic sign recognition, driver monitoring system, algorithm optimization, cloud computing, automatic emergency braking, ultrasonic sensors, software development, high-definition mapping, semiconductor technology, forward collision warning, adaptive cruise control, machine learning algorithms, autonomous driving, functional safety, regulatory compliance, data acquisition, driver assistance features, parking assist, camera systems, lane keeping assist, hardware integration, system calibration, sensor fusion, passenger safety, image processing, embedded systems, over-the-air updates, and night vision, are increasingly being integrated into vehicles to enhance safety, comfort, and convenience.

Moreover, the European market is witnessing the adoption of advanced technologies like sensor fusion, which combines data from multiple sensors to provide more accurate and reliable information to the driver, and machine learning algorithms, which enable vehicles to learn from their environment and adapt to various driving conditions. Additionally, the integration of cloud computing and real-time data processing capabilities allows for over-the-air updates, ensuring that vehicles remain up-to-date with the latest safety features and functionalities. Regulatory compliance and functional safety are crucial aspects of the European automotive market, with stringent certification standards in place to ensure the safety and reliability of ADAS technologies.

Companies are investing in algorithm optimization and hardware integration to meet these standards while maintaining passenger safety and improving overall vehicle performance. The European automotive market is a major player in the global ADAS industry, driven by the demand for safety features, stringent safety regulations, and the presence of leading automotive OEMs. The integration of advanced technologies, such as sensor fusion, machine learning algorithms, cloud computing, and real-time data processing, is transforming the market and setting the stage for the future of autonomous driving.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Automotive Advanced Driver Assistance System (ADAS) Industry?

- The significant decrease in sensor prices serves as the primary catalyst for market growth. The market is experiencing significant growth due to the declining prices of essential technologies, such as sensors and displays. The reduction in costs is enabling automotive Original Equipment Manufacturers (OEMs) to offer cost-effective ADAS solutions to customers. For instance, the price of displays and infotainment systems has decreased significantly in the last decade due to their widespread adoption in consumer electronics and the automotive industry.

- Companies are focusing on improving the performance of these technologies through algorithm optimization and the integration of cloud computing to provide real-time data processing and analysis. Additionally, the development of certification standards is ensuring the safety and reliability of ADAS technologies, further boosting market growth. Similarly, the price of sensors like radars, cameras, and LiDAR is continuously declining, driven by their increasing application in the automotive sector. Moreover, certification standards, deep learning models, testing and validation, vehicle-to-everything (V2X) communication, adaptive headlights, driver monitoring systems, algorithm optimization, cloud computing, automatic emergency braking, and ultrasonic sensors are some of the key technologies driving the growth of the ADAS market.

What are the market trends shaping the Automotive Advanced Driver Assistance System (ADAS) Industry?

- The growing development of AI-enabled Advanced Driver-Assistance Systems (ADAS) represents a significant market trend in the automotive industry. This technological advancement aims to enhance vehicle safety and improve the overall driving experience. The automotive industry is witnessing significant advancements in driver assistance technology, with a focus on delivering personalized solutions in a connected environment. Artificial Intelligence (AI) is at the forefront of these innovations, as it strives to emulate human brain functions in Advanced Driver Assistance Systems (ADAS).

- Key features of ADAS include forward collision warning, adaptive cruise control, and parking assist. Functional safety and regulatory compliance are crucial considerations in the development of these systems. High-definition mapping and semiconductor technology are essential components that support the effective implementation of these features. The integration of AI in ADAS is a significant trend that is expected to drive the growth of the global market during the forecast period. AI-based ADAS solutions utilize machine learning algorithms to learn from experiences, enabling them to detect and recognize surroundings more effectively. This technology can identify multiple objects around the vehicle, reducing the risk of collisions. Moreover, AI-based ADAS consumes less power and expedites development time, making it an attractive option for prominent ADAS manufacturers.

What challenges does the Automotive Advanced Driver Assistance System (ADAS) Industry face during its growth?

- The escalating costs related to servicing and maintaining Advanced Driver-Assistance Systems (ADAS) represent a significant challenge to the industry's growth trajectory. The market is experiencing significant growth due to the increasing demand for enhanced passenger safety and convenience. Camera systems, such as lane keeping assist and night vision, are key components of ADAS, enabling features like automatic emergency braking and adaptive cruise control. Hardware integration and system calibration are essential for proper functioning, requiring advanced image processing capabilities and sensor fusion.

- To address these concerns, there is a growing emphasis on over-the-air updates and embedded systems to reduce repair costs and improve system reliability. However, the high cost of repair and maintenance for ADAS components poses a challenge to market expansion, particularly in emerging economies where price sensitivity is a major concern. In the US, for instance, the repair cost for radar sensors used in advanced emergency braking systems and adaptive cruise control exceeds USD900, while the cost for repairing rear radar sensors for blind spot detection and rear cross-traffic alert can reach approximately USD2,000.

Exclusive Customer Landscape

The automotive advanced driver assistance system (adas) market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive advanced driver assistance system (adas) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive advanced driver assistance system (adas) market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AISIN Corp. - THe comapny specilaies in Advanced Driver-Assistance Systems (ADAS) are integral to modern vehicles, enhancing safety and convenience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN Corp.

- Aptiv Plc

- Autoliv Inc.

- BorgWarner Inc.

- Continental AG

- DENSO Corp.

- Gentex Corp.

- Harman International Industries Inc.

- HELLA GmbH and Co. KGaA

- Hyundai Motor Co.

- Infineon Technologies AG

- Intel Corp.

- Magna International Inc.

- NXP Semiconductors NV

- Panasonic Holdings Corp.

- Renesas Electronics Corp.

- Robert Bosch GmbH

- Valeo SA

- Veoneer Inc.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Advanced Driver Assistance System (ADAS) Market

- In January 2024, Bosch and Magna announced a strategic collaboration to develop next-generation ADAS technologies, combining Bosch's software expertise with Magna's hardware capabilities (Bosch press release).

- In March 2024, Aptiv and Intel's Mobileye completed the acquisition of Panasonic's automotive safety and advanced driver assistance systems business, expanding Aptiv's ADAS portfolio (Intel press release).

- In April 2025, Tesla received regulatory approval for its Full Self-Driving (FSD) beta program in California, marking a significant step towards commercial deployment of advanced autonomous driving technology (California DMV press release).

- In May 2025, Continental and Veoneer signed a definitive agreement to merge their automotive technology businesses, creating a leading global ADAS supplier (Continental press release).

Research Analyst Overview

The market is experiencing significant growth, driven by the integration of advanced technologies such as actuator control, vehicle detection, pedestrian detection, and path planning. Cost optimization is a key focus for automakers, as they seek to balance the benefits of these systems with the challenges of sensor accuracy, reliability, and power consumption. Ethical considerations and legal liability are also emerging concerns, as ADAS systems increasingly rely on object recognition and decision-making capabilities. Integration challenges persist, as OEMs and suppliers work to ensure seamless HMI, UI, and UX experiences, while addressing issues of data security and privacy. As the market evolves, haptic feedback and trajectory prediction are expected to become increasingly important features, requiring further advancements in control algorithms and processing speed.

Supply chain management remains a critical factor, as the demand for sensors and other components continues to grow. Despite these challenges, consumer adoption of ADAS technologies is on the rise, driven by the promise of improved safety and convenience. The Automotive Advanced Driver Assistance System (ADAS) market is accelerating as the industry shifts toward safer, smarter driving experiences. At the core is enhanced decision making, powered by real-time data and intelligent algorithms to prevent accidents and optimize traffic flow. The integration of Human-Machine Interface (HMI) systems, refined User Experience (UX), and intuitive User Interface (UI) design ensures drivers can interact with technologies seamlessly and confidently. To maintain safety and performance, sensor reliability is criticalâensuring accurate detection under diverse conditions. As vehicles become more connected, privacy concerns are rising, prompting stringent data protection protocols.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Advanced Driver Assistance System (ADAS) Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

234 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.4% |

|

Market growth 2025-2029 |

USD 43.53 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

12.3 |

|

Key countries |

US, China, Germany, France, UK, Canada, Japan, South Korea, Italy, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Advanced Driver Assistance System (ADAS) Market Research and Growth Report?

- CAGR of the Automotive Advanced Driver Assistance System (ADAS) industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive advanced driver assistance system (ADAS) market growth of industry companies

We can help! Our analysts can customize this automotive advanced driver assistance system (ADAS) market research report to meet your requirements.

RIA -

RIA -