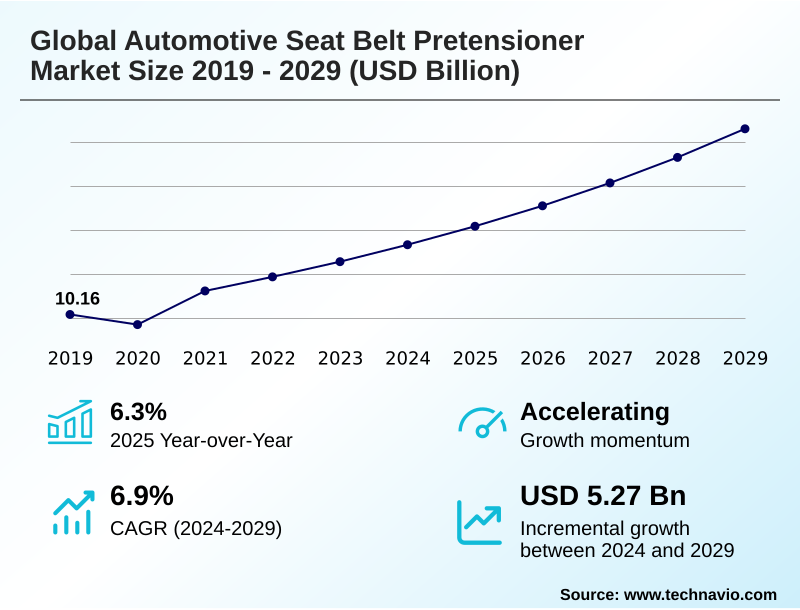

Automotive Seat Belt Pretensioner Market Size 2025-2029

The automotive seat belt pretensioner market size is valued to increase by USD 5.27 billion, at a CAGR of 6.9% from 2024 to 2029. Increasing demand for SUVs will drive the automotive seat belt pretensioner market.

Major Market Trends & Insights

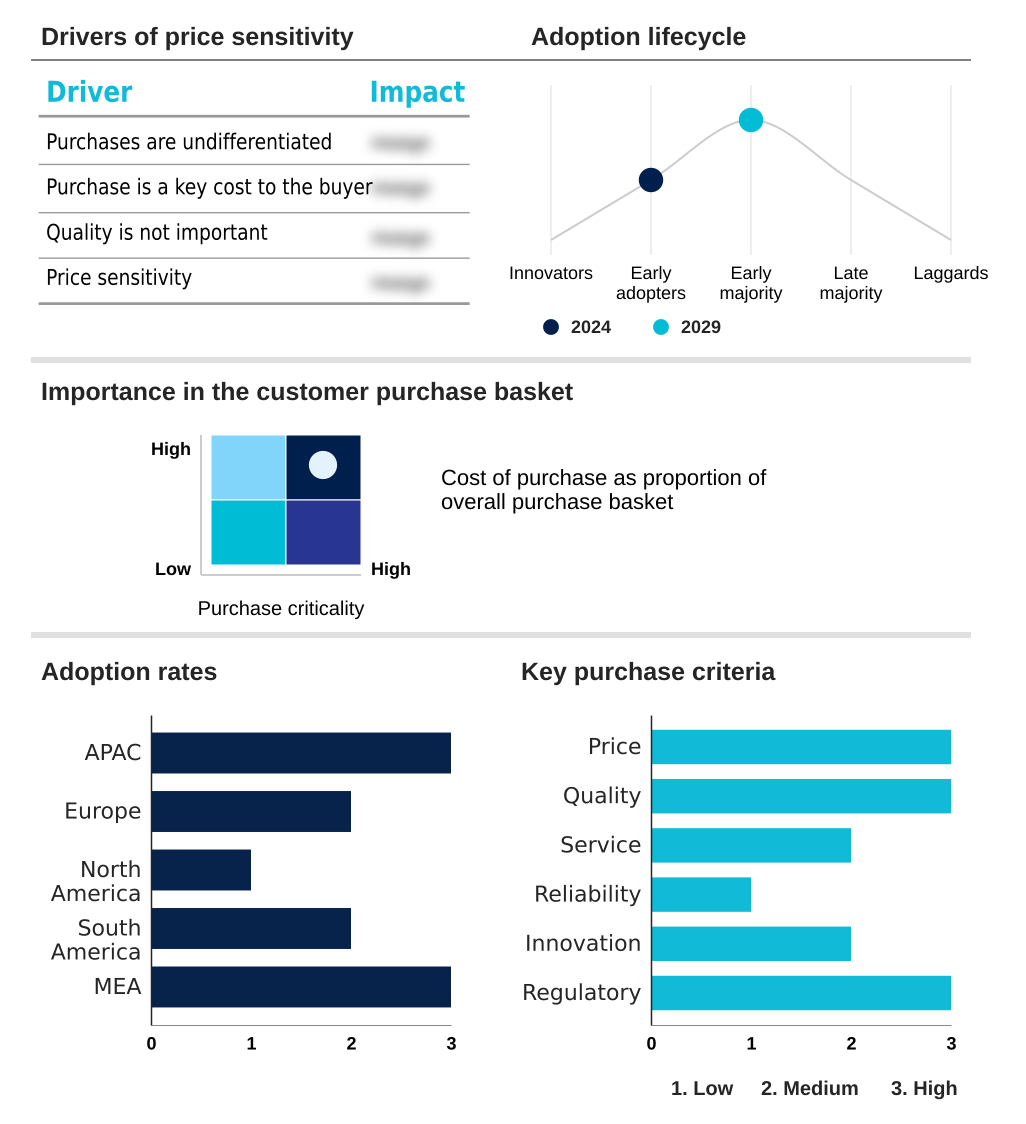

- APAC dominated the market and accounted for a 51.8% growth during the forecast period.

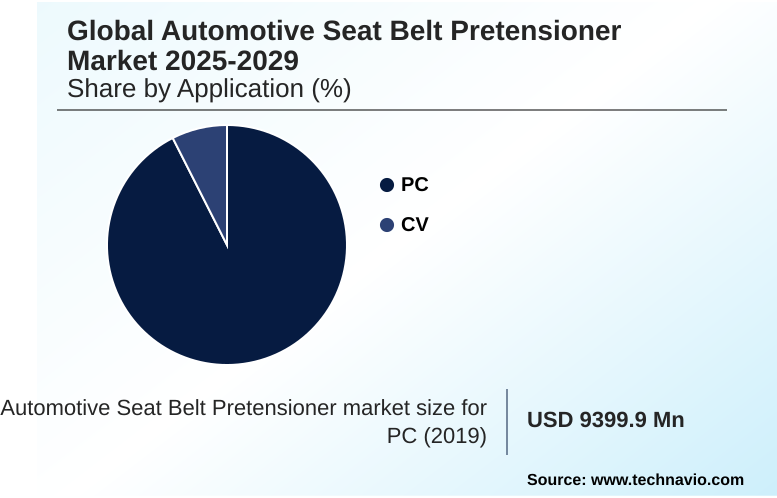

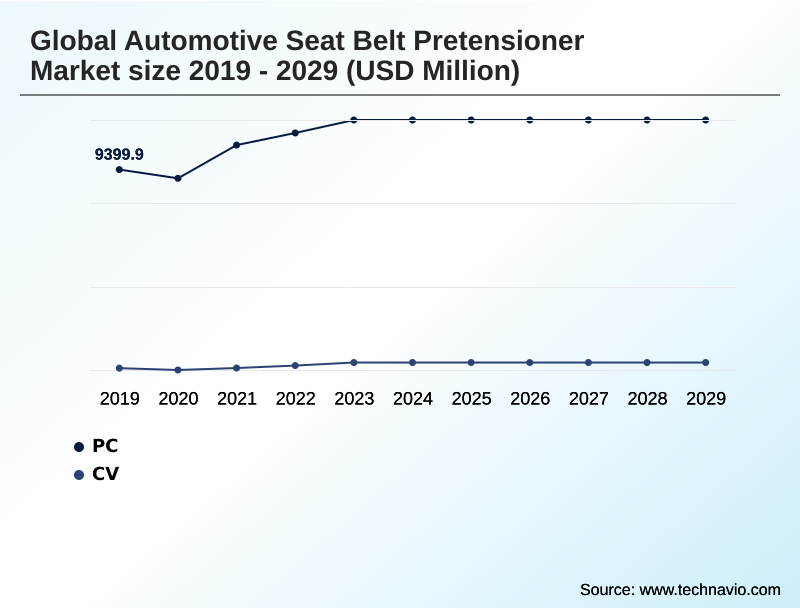

- By Application - PC segment was valued at USD 11.56 billion in 2023

- By Type - OEM segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 8.44 billion

- Market Future Opportunities: USD 5.27 billion

- CAGR from 2024 to 2029 : 6.9%

Market Summary

- The automotive seat belt pretensioner market is integral to enhancing vehicle safety, driven by stringent government regulations and rising consumer demand for robust occupant protection. These systems, a critical component of a vehicle's passive safety system, function by removing slack from the seat belt during a collision, securing the occupant firmly.

- Growth is propelled by the increasing production of passenger vehicles, especially SUVs, and the expanding integration of these safety features beyond luxury models into mid-range and economy cars. A key industry trend is the technological advancement toward more sophisticated systems, including the integration of crash sensors with the electronic control unit (ECU).

- For instance, a fleet management company optimizing its vehicle procurement strategy would prioritize models with advanced occupant restraint systems that meet the latest New Car Assessment Program (NCAP) standards. This not only ensures driver safety but also lowers insurance premiums and reduces liability, demonstrating a clear operational benefit.

- However, the market faces challenges from consumer perceptions of discomfort and cost pressures in manufacturing, which temper the pace of adoption in some segments.

What will be the Size of the Automotive Seat Belt Pretensioner Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Seat Belt Pretensioner Market Segmented?

The automotive seat belt pretensioner industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- PC

- CV

- Type

- OEM

- Aftermarket

- Technology

- Retractor pretensioner

- Buckle pretensioner

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Application Insights

The pc segment is estimated to witness significant growth during the forecast period.

Market segmentation is primarily defined by application, with passenger cars (PCs) representing the dominant share.

The PC segment, which accounted for over 91% of the market in 2024, is driven by stringent automotive safety regulations and high consumer expectations for safety.

The integration of a pyrotechnic pretensioner, particularly the retractor pretensioner type, is standard in new vehicles.

These systems are a core part of a vehicle's active safety system, relying on a crash sensor and seat belt sensor to analyze vehicle crash dynamics and occupant kinematics in real-time.

A pyrotechnic gas generator provides the rapid force needed for activation. This focus on advanced technology underscores the industry’s commitment to exceeding baseline safety requirements in the high-volume PC segment.

The PC segment was valued at USD 11.56 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 51.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Seat Belt Pretensioner Market Demand is Rising in APAC Get Free Sample

The geographic landscape is led by APAC, which is set to contribute over 51% of the market's incremental growth. This dominance is fueled by rising vehicle safety standards and local manufacturing strength.

In contrast, North America and Europe are mature markets focused on technological evolution, such as the adoption of energy-efficient pretensioner designs over older mechanical pretensioner systems.

The restraint control module in these regions features advanced sensor integration for precise crash severity detection and links to sophisticated occupant classification systems.

There is also a growing focus on adaptive seat belt systems that use occupant position detection and inputs from the accident data recorder to tailor restraint characteristics, improving safety outcomes by up to 10% in certain offset collisions.

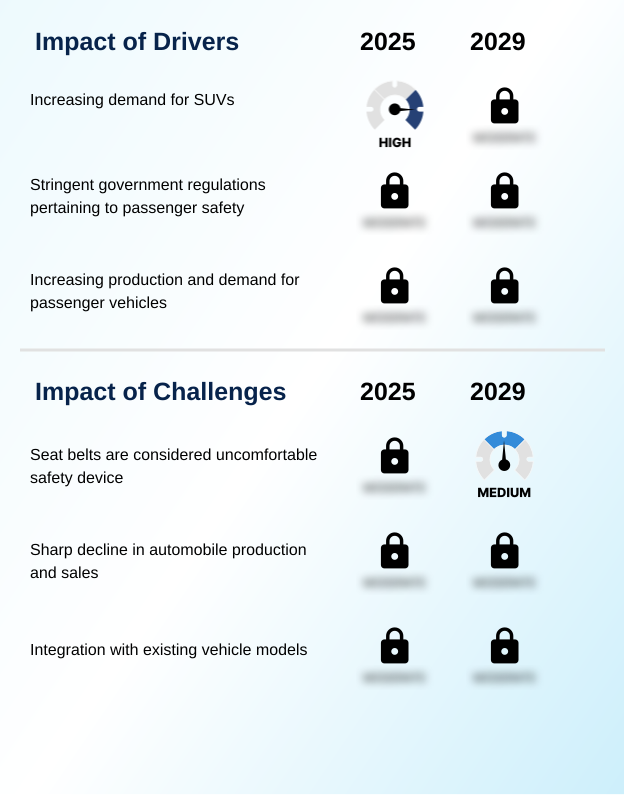

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the automotive safety sector require a deep understanding of component-level performance and system integration. A key debate involves the merits of pyrotechnic vs mechanical seat belt pretensioner designs, with pyrotechnic options offering faster response times.

- The successful retractor pretensioner integration with airbag systems is critical for synchronized occupant protection, a factor that is rigorously evaluated in crash simulations. Similarly, buckle pretensioner effectiveness in rollover collisions is a specialized area of R&D, as these events present unique kinematic challenges. Looking ahead, the design of an active safety system for autonomous vehicle occupants is a major focus.

- The impact of load limiters on occupant injury metrics is continuously studied to refine restraint forces. A crucial operational metric is seat belt pretensioner performance in low-speed impacts, where preventing nuisance deployments is key. Businesses conduct a thorough cost-benefit analysis of dual-stage pretensioners, weighing enhanced safety against higher unit costs.

- Furthermore, the challenges in retrofitting pretensioners in older vehicles limit aftermarket scope. Supply chain planning must account for strict regulatory compliance for seat belt pretensioner systems and OEM requirements for pretensioner cycle testing. The use of lightweight material adoption in pretensioner design supports fuel efficiency goals, while simulation of pretensioner deployment in crash tests accelerates development.

- The role of pretensioners in integrated safety systems and robust pretensioner malfunction diagnosis and fault codes are vital.

- The maintenance and replacement cycles for pyrotechnic units, human body modeling for pretensioner system optimization, integration of pretensioners with active seat bolsters, thermal management of pyrotechnic gas generators, and adaptive force limiting in seat belt systems represent the frontiers of personalized occupant safety.

What are the key market drivers leading to the rise in the adoption of Automotive Seat Belt Pretensioner Industry?

- A key driver fueling market growth is the increasing global demand for sports utility vehicles (SUVs), which frequently incorporate advanced safety systems.

- Market growth is strongly driven by regulatory mandates and the increasing complexity of vehicle safety architecture.

- The integration of a buckle pretensioner as part of a comprehensive passive safety system is becoming standard, offering enhanced frontal collision protection and side-impact protection. Innovations in lightweight materials are enabling the production of more efficient components without compromising strength.

- The electronic control unit (ECU) orchestrates these systems, often including a load limiter to manage belt forces. A key enabler is improved seat assembly integration, which simplifies manufacturing and improves system reliability.

- Automakers' focus on holistic safety design, where every component works in unison, propels demand and continuous R&D investment in these critical systems.

What are the market trends shaping the Automotive Seat Belt Pretensioner Industry?

- The market is witnessing a notable trend toward the increased adoption of advanced safety features in low-cost, compact cars and commercial vehicles.

- A significant trend is the democratization of advanced safety features, extending beyond luxury vehicles. The complete occupant restraint system, including durable seat belt webbing, is now a key factor in achieving high New Car Assessment Program (NCAP) ratings, driving adoption in economy models.

- This push for enhanced collision mitigation has resulted in a 95% installation rate for seat belt reminder (SBR) systems in new models in developed regions. Furthermore, advanced restraint technologies like active seat belt technology are gaining traction. This involves smart sensor integration for adaptive performance, ensuring vehicle safety compliance while improving user comfort.

- The industry is moving toward systems that not only react to crashes but also anticipate and adapt to occupant behavior.

What challenges does the Automotive Seat Belt Pretensioner Industry face during its growth?

- A key challenge impacting industry growth is the consumer perception of seat belts as uncomfortable, which can hinder consistent use.

- A primary challenge involves the cost and complexity of integrating pretensioners with other advanced systems. The link between the seat belt retractor mechanism and Advanced Driver-Assistance Systems (ADAS), for instance, requires sophisticated software to prevent false activations from a pyrotechnic initiator. Ensuring robust occupant protection across diverse crash scenarios on new modular vehicle platforms adds to engineering costs.

- While OEM safety specifications are stringent, the market for certified aftermarket pretensioner kits remains niche, creating maintenance challenges. The reliability of the pyrotechnic safety device over a vehicle's lifespan is another concern, as replacement costs can sometimes exceed 3-5% of a vehicle's residual value.

Exclusive Technavio Analysis on Customer Landscape

The automotive seat belt pretensioner market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive seat belt pretensioner market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Seat Belt Pretensioner Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive seat belt pretensioner market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AmSafe Inc. - Offerings include advanced dual-stage pretensioners that provide modulated protection by adjusting seat belt tension according to collision severity, ensuring optimal restraint.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AmSafe Inc.

- Ashimori Industry Co. Ltd.

- Autoliv Inc.

- DENSO Corp.

- Guangzhou Fuxin Auto Parts Co. Ltd.

- Hyundai Motor Group

- Illinois Tool Works Inc.

- Iron Force Industrial Co. Ltd.

- Joyson Safety Systems Aschaffenburg GmbH

- Robert Bosch GmbH

- Special Devices Inc.

- Tokai Rika Co. Ltd.

- Wenzhou Far Europe Auto Parts Co. Ltd.

- Wenzhou Far Europe Automobile Safety System Co. Ltd.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive seat belt pretensioner market

- In September 2024, SafeRide Systems announced a strategic partnership with AutoIntelli Inc. to integrate its new energy-efficient pretensioner systems with next-generation ADAS platforms, aiming to enhance predictive safety activation in autonomous vehicles.

- In November 2024, Autoliv Inc. completed the acquisition of a smaller tech firm, PyroTech Innovations, for $150 million to bolster its R&D in pyrotechnic gas generator technology and compact pretensioner designs.

- In March 2025, Joyson Safety Systems launched its 'Smart-Tension' active seat belt technology, a new product featuring sensor integration for adaptive force limiting based on occupant size and position.

- In May 2025, Robert Bosch GmbH received ECE R16 approval for its new modular buckle pretensioner, designed for simplified integration into electric vehicle platforms across European markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Seat Belt Pretensioner Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 278 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.9% |

| Market growth 2025-2029 | USD 5272.0 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 6.3% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, France, UK, The Netherlands, Italy, Spain, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive seat belt pretensioner market is defined by a sophisticated interplay of technologies designed for superior occupant protection. Core to this is the occupant restraint system, which relies on a seat belt retractor mechanism and a restraint control module.

- Activation is triggered by a crash sensor that prompts a pyrotechnic initiator; this ignites a pyrotechnic gas generator within either a retractor pretensioner or a buckle pretensioner. These pyrotechnic pretensioner designs are increasingly favored over older mechanical pretensioner systems.

- The integration of the electronic control unit (ECU) is crucial for collision mitigation, enabling coordination with the vehicle's passive safety system and active safety system. Innovations focus on energy-efficient pretensioner models and advanced sensor integration for improved crash severity detection. A key boardroom consideration is adherence to evolving vehicle safety standards and achieving high New Car Assessment Program (NCAP) ratings.

- This involves sophisticated occupant classification systems and the integration of a load limiter with seat belt webbing. Such enhancements, often linked with Advanced Driver-Assistance Systems (ADAS), have led to a demonstrated 15% reduction in certain injury metrics in certified crash tests.

What are the Key Data Covered in this Automotive Seat Belt Pretensioner Market Research and Growth Report?

-

What is the expected growth of the Automotive Seat Belt Pretensioner Market between 2025 and 2029?

-

USD 5.27 billion, at a CAGR of 6.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (PC, CV), Type (OEM, Aftermarket), Technology (Retractor pretensioner, Buckle pretensioner) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for SUVs, Seat belts are considered uncomfortable safety device

-

-

Who are the major players in the Automotive Seat Belt Pretensioner Market?

-

AmSafe Inc., Ashimori Industry Co. Ltd., Autoliv Inc., DENSO Corp., Guangzhou Fuxin Auto Parts Co. Ltd., Hyundai Motor Group, Illinois Tool Works Inc., Iron Force Industrial Co. Ltd., Joyson Safety Systems Aschaffenburg GmbH, Robert Bosch GmbH, Special Devices Inc., Tokai Rika Co. Ltd., Wenzhou Far Europe Auto Parts Co. Ltd., Wenzhou Far Europe Automobile Safety System Co. Ltd. and ZF Friedrichshafen AG

-

Market Research Insights

- The market's dynamics are heavily influenced by stringent automotive safety regulations and a focus on vehicle safety compliance. Innovations in advanced restraint technologies are paramount, with a move toward smart sensor integration and active seat belt technology. Manufacturers are leveraging lightweight materials and modular vehicle platforms to facilitate seat assembly integration while meeting OEM safety specifications.

- Understanding vehicle crash dynamics and occupant kinematics is essential for developing effective frontal collision protection and side-impact protection. A critical component is the seat belt sensor, which works with systems for occupant position detection. While pyrotechnic safety devices are standard, there's growing interest in adaptive seat belt systems.

- The seat belt reminder (SBR) is now a baseline feature, with a notable 90% adoption rate in new vehicles in developed regions. For the aftermarket, the availability of certified aftermarket pretensioner kits is growing, though their use is less than 10% compared to OEM installations, impacting maintenance strategies. The accident data recorder provides crucial post-crash information.

We can help! Our analysts can customize this automotive seat belt pretensioner market research report to meet your requirements.

RIA -

RIA -