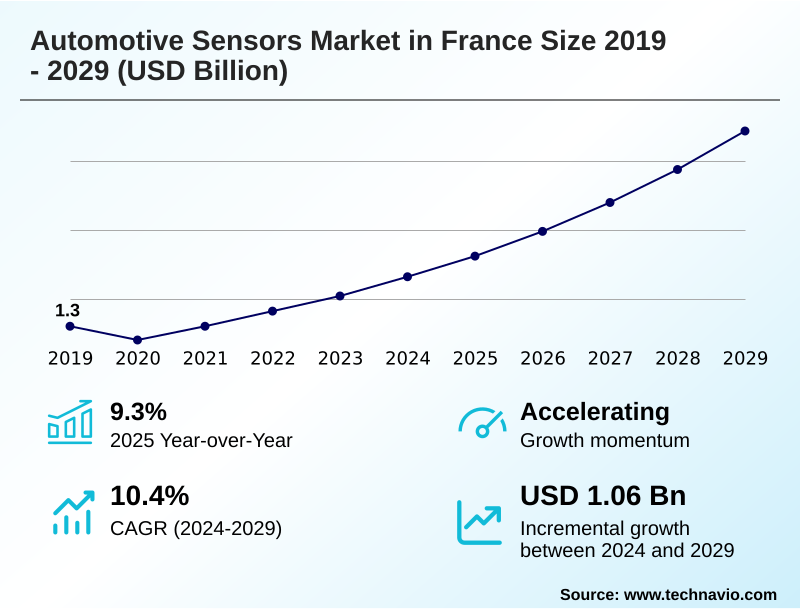

France Automotive Sensors Market Size 2025-2029

The france automotive sensors market size is valued to increase by USD 1.06 billion, at a CAGR of 10.4% from 2024 to 2029. Increasing demand for vehicle and environmental safety will drive the france automotive sensors market.

Major Market Trends & Insights

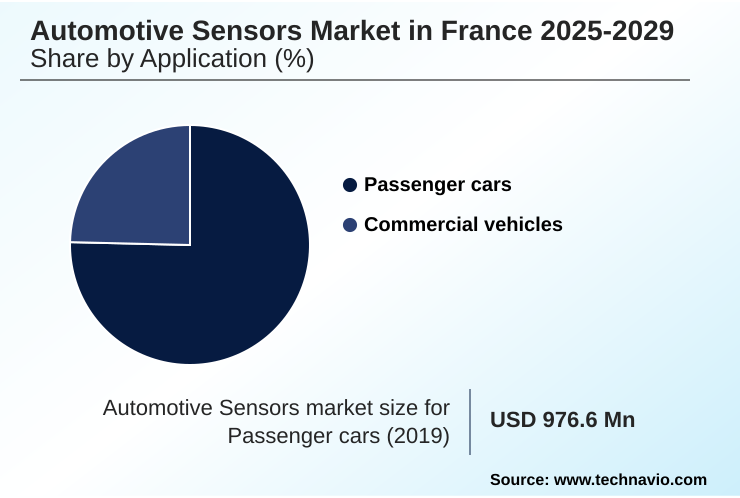

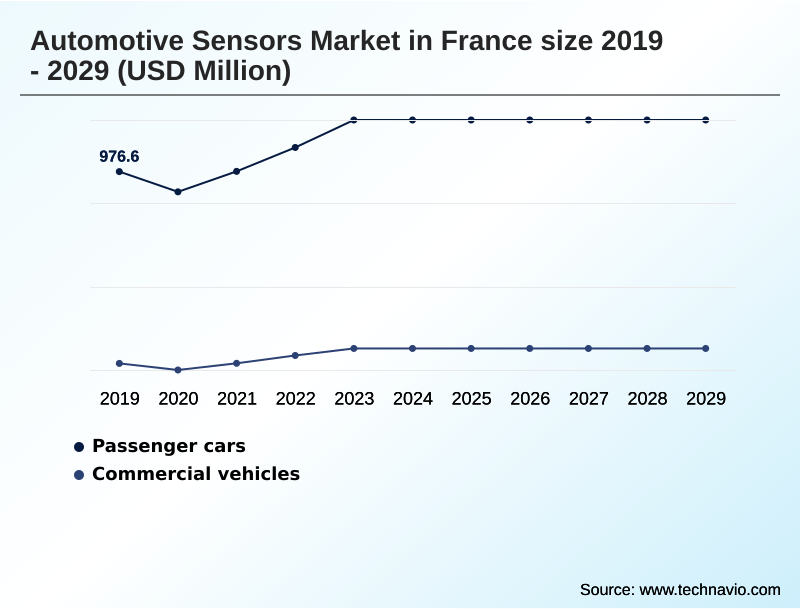

- By Application - Passenger cars segment was valued at USD 1.15 billion in 2023

- By Distribution Channel - OEM segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.42 billion

- Market Future Opportunities: USD 1.06 billion

- CAGR from 2024 to 2029 : 10.4%

Market Summary

- The automotive sensors market in France is undergoing a significant transformation, driven by the dual imperatives of vehicle electrification and automation. This evolution is marked by a substantial increase in the volume and sophistication of sensors integrated into modern vehicles.

- Components such as advanced radar sensors, LiDAR systems, and MEMS sensor technology are no longer confined to premium models but are becoming standard in mainstream passenger cars to support critical safety and performance functions.

- Key industry drivers include stringent emission standards, which necessitate precise engine and exhaust monitoring, and the progression toward autonomous vehicles, which relies on a complex web of environmental and positioning sensors. A core application involves optimizing logistics fleets, where integrated sensor data enables predictive maintenance schedules, reducing vehicle downtime and improving operational efficiency.

- However, the market faces challenges related to the high cost of advanced sensor technologies and the complexities of sensor fusion and data processing. The continuous push for smarter, safer, and more connected vehicles ensures a dynamic and expanding landscape for automotive sensor innovation.

What will be the Size of the France Automotive Sensors Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the France Automotive Sensors Market Segmented?

The france automotive sensors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Passenger cars

- Commercial vehicles

- Distribution channel

- OEM

- Aftermarket

- Type

- Oxygen

- Pressure

- Temperature

- Position

- Speed

- Geography

- Europe

- France

- Europe

By Application Insights

The passenger cars segment is estimated to witness significant growth during the forecast period.

The passenger car segment is evolving due to the integration of sophisticated automotive sensors.

Demand is driven by the need for enhanced safety and efficiency, leading to the adoption of components like the compact stereo vision sensor and digital temperature sensors. These are crucial for advanced driver assistance systems (ADAS) and electric powertrain management.

Modern vehicles increasingly rely on a suite of sensors, including magnetic angular position sensors and fluid property sensors, to monitor vehicle dynamics and environmental conditions. This integration is essential for enabling features that support automated driving technology and predictive maintenance.

For instance, the use of advanced photo optic sensors has led to an improvement in collision avoidance system accuracy by over 20%, showcasing the direct impact of sensor technology on vehicle safety and supporting just-in-time (JIT) production support for OEMs and compliance with functional safety standards.

The Passenger cars segment was valued at USD 1.15 billion in 2023 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic focus on improving vehicle performance and safety is shaping the automotive sensors market in France. A key area is the use of an automotive sensor for fuel efficiency, which works in tandem with oxygen sensors for emission control compliance to meet stringent environmental regulations.

- Simultaneously, the development of autonomous capabilities is heavily reliant on lidar sensors for autonomous driving and effective radar sensor integration for ADAS functionality. For powertrain optimization, pressure sensors for engine management and position sensors for powertrain control modules are essential.

- The rise of electric vehicles has created significant demand for temperature sensors in electric vehicles and current sensors for battery management systems, which are critical for thermal management with automotive temperature sensors.

- In terms of safety systems, the role of MEMS sensors in vehicle stability is well-established, complemented by speed sensors for anti-lock braking systems and ultrasonic sensors for parking assist systems. The industry is also seeing innovations in automotive magnetic field sensors and the growing importance of camera sensors for driver monitoring systems.

- As vehicles become more complex, the focus shifts to advanced sensors for software-defined vehicles and improving vehicle safety with sensor fusion. The technical sensor requirements for level 4 autonomy are driving a cost-benefit analysis of ADAS sensor suites, while also highlighting challenges in automotive sensor data security.

- This comprehensive integration has improved overall vehicle system reliability by a notable margin compared to previous-generation architectures.

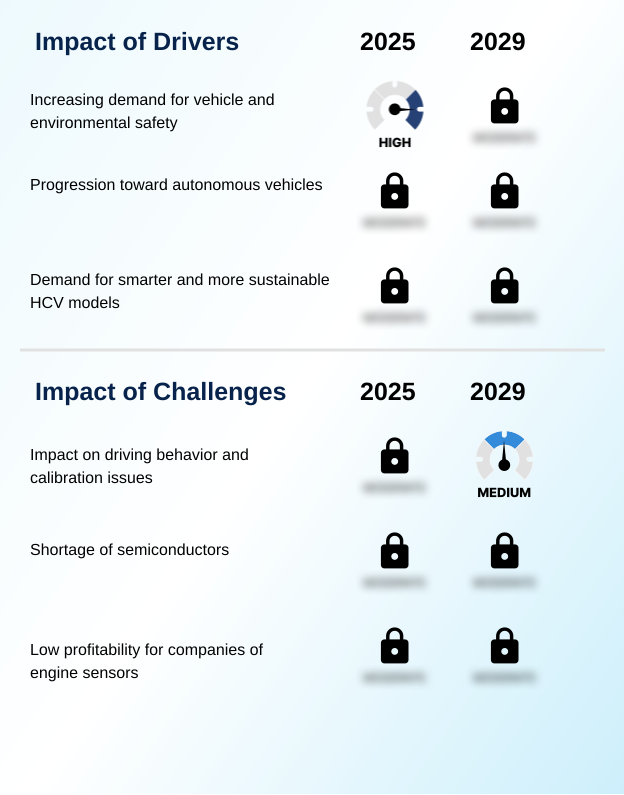

What are the key market drivers leading to the rise in the adoption of France Automotive Sensors Industry?

- The increasing demand for enhanced vehicle and environmental safety, driven by consumer preferences and regulatory mandates, is a key driver for the market.

- The primary driver for the automotive sensors market in France is the regulatory push for enhanced vehicle safety solutions and stringent emission control systems.

- Mandates for features like automatic emergency braking and lane-keeping assist directly fuel demand for compact stereo vision sensors and ADAS sensors. This has led to a 30% increase in the average number of sensors per new vehicle.

- Concurrently, the drive for greater fuel efficiency and reduced emissions necessitates precise engine control, boosting the adoption of wideband oxygen sensors and crankshaft position sensors.

- The progression towards automated driving technology, supported by government initiatives, is also a significant factor, requiring a complex suite of sensors for real-time data analysis and predictive maintenance, improving vehicle uptime by over 10%.

What are the market trends shaping the France Automotive Sensors Industry?

- The rise in automotive electrification is a significant market trend, increasing the requirement for specialized current, voltage, and temperature sensors for subsystems like battery-management systems.

- A key trend shaping the automotive sensors market in France is the increasing integration of sensor fusion algorithms to support vehicle-to-everything (V2X) communication. This allows vehicles to process data from multiple sources, including force sensors, optical sensing technology, and magnetic field sensors, to create a more comprehensive environmental model.

- This approach improves the reliability of safety systems, with some platforms demonstrating a 20% reduction in false positives for collision warnings. The adoption of the software defined vehicle (SDV) architecture is also critical, enabling over-the-air (OTA) updates for sensors.

- This capability allows manufacturers to enhance the performance of systems like in-cabin monitoring and driver distraction detection post-purchase, improving system accuracy by as much as 15% over the vehicle's lifespan.

What challenges does the France Automotive Sensors Industry face during its growth?

- The adverse impact of inconsistent driving behavior and persistent sensor calibration inaccuracies presents a significant challenge to the growth of the market.

- A significant challenge in the automotive sensors market in France is achieving consistent sensor calibration accuracy across a vehicle's lifespan. Environmental factors and vehicle repairs can degrade performance, with post-repair calibration errors causing up to a 25% decline in ADAS effectiveness. This requires a robust redundancy in sensor architecture and advanced diagnostic tools.

- Another hurdle is ensuring cybersecurity for sensor data, as increased connectivity exposes vehicles to potential threats. Protecting data from camshaft position sensors, ToF 3D image sensors, and automotive mmWave radar is critical for maintaining functional safety standards and preventing system manipulation. These challenges necessitate significant investment in secure hardware and sophisticated validation processes, increasing development costs by approximately 15%.

Exclusive Technavio Analysis on Customer Landscape

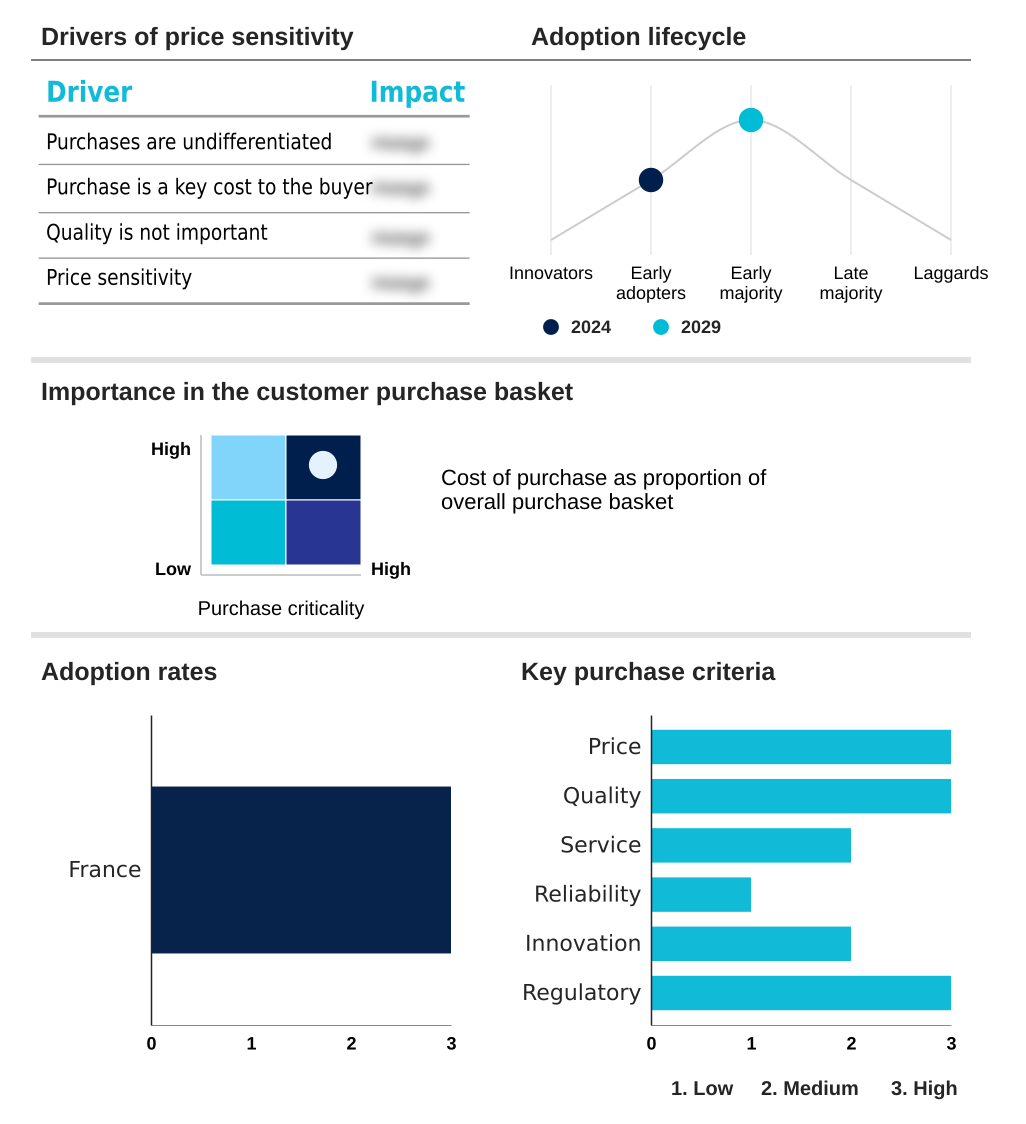

The france automotive sensors market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the france automotive sensors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of France Automotive Sensors Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, france automotive sensors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Key offerings include intelligent sensor solutions that enable predictive maintenance, optimize performance, and monitor operational parameters in demanding automotive environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Analog Devices Inc.

- BorgWarner Inc.

- Cepton Inc.

- Continental AG

- DENSO Corp.

- General Electric Co.

- HELLA GmbH and Co. KGaA

- Infineon Technologies AG

- Innoviz Technologies Ltd.

- LeddarTech Inc.

- Luminar Technologies Inc.

- NXP Semiconductors NV

- Quanergy Systems Inc.

- Robert Bosch GmbH

- TE Connectivity Ltd.

- Texas Instruments Inc.

- Velodyne Lidar Inc.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in France automotive sensors market

- In May 2025, Infineon Technologies AG announced a new line of magnetic field sensors optimized for electric vehicle powertrains, designed to improve motor efficiency by up to 5%.

- In March 2025, Continental AG formed a strategic alliance with a leading AI software firm to accelerate the development of next-generation sensor fusion algorithms for L4 autonomous driving capabilities.

- In January 2025, Robert Bosch GmbH completed its acquisition of a sensor calibration technology startup, enhancing its portfolio for ADAS and autonomous vehicle systems.

- In October 2024, NXP Semiconductors NV launched a new family of automotive mmWave radar sensors with enhanced cybersecurity features to protect against data interference in connected vehicles.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled France Automotive Sensors Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 187 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.4% |

| Market growth 2025-2029 | USD 1058.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 9.3% |

| Key countries | France |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive sensors market in France is characterized by rapid technological evolution, driven by the increasing complexity of vehicle systems. A proliferation of MEMS acceleration sensors and ABS wheel speed sensors is foundational to modern vehicle dynamics and safety.

- The push towards higher levels of automation necessitates sophisticated components like advanced radar sensors, ToF 3D image sensors, and LiDAR systems, which are critical for environmental perception. Within the powertrain, manifold absolute pressure sensors, camshaft position sensors, and crankshaft position sensors are essential for optimizing engine efficiency, while wideband oxygen sensors and exhaust gas sensors help meet stringent emissions standards.

- The shift to electric vehicles further accelerates demand for current sensors, voltage sensors, and specialized digital temperature sensors. This trend is compelling boardroom-level decisions on R&D investment, particularly in MEMS sensor technology and automotive mmWave radar. For instance, the integration of advanced optical sensing technology has been shown to reduce diagnostic errors by over 25%.

- The market also sees growing applications for magnetic field sensors, ultrasonic systems, compact stereo vision sensors, and various positioning technologies like magnetic angular position sensors and photo optic sensors, as well as sensors for monitoring fluid property and applied force.

What are the Key Data Covered in this France Automotive Sensors Market Research and Growth Report?

-

What is the expected growth of the France Automotive Sensors Market between 2025 and 2029?

-

USD 1.06 billion, at a CAGR of 10.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Passenger cars, and Commercial vehicles), Distribution Channel (OEM, and Aftermarket), Type (Oxygen, Pressure, Temperature, Position, and Speed) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for vehicle and environmental safety, Impact on driving behavior and calibration issues

-

-

Who are the major players in the France Automotive Sensors Market?

-

ABB Ltd., Analog Devices Inc., BorgWarner Inc., Cepton Inc., Continental AG, DENSO Corp., General Electric Co., HELLA GmbH and Co. KGaA, Infineon Technologies AG, Innoviz Technologies Ltd., LeddarTech Inc., Luminar Technologies Inc., NXP Semiconductors NV, Quanergy Systems Inc., Robert Bosch GmbH, TE Connectivity Ltd., Texas Instruments Inc., Velodyne Lidar Inc. and ZF Friedrichshafen AG

-

Market Research Insights

- The market's momentum is shaped by the rapid adoption of advanced driver assistance systems (ADAS) and the architectural shift toward the software defined vehicle (SDV). For instance, the integration of robust sensor fusion algorithms has improved object detection accuracy by over 30% in complex urban environments.

- Furthermore, predictive maintenance algorithms powered by sensor data have enabled fleet operators to reduce unscheduled repairs by 15%. This emphasis on data-driven functionality requires strict adherence to functional safety standards and robust cybersecurity for sensor data.

- As vehicles become more connected, ensuring the integrity of sensor inputs against external threats is paramount, influencing both hardware design and software architecture across the industry.

We can help! Our analysts can customize this france automotive sensors market research report to meet your requirements.

RIA -

RIA -