Automotive Smart Keys Market Size 2026-2030

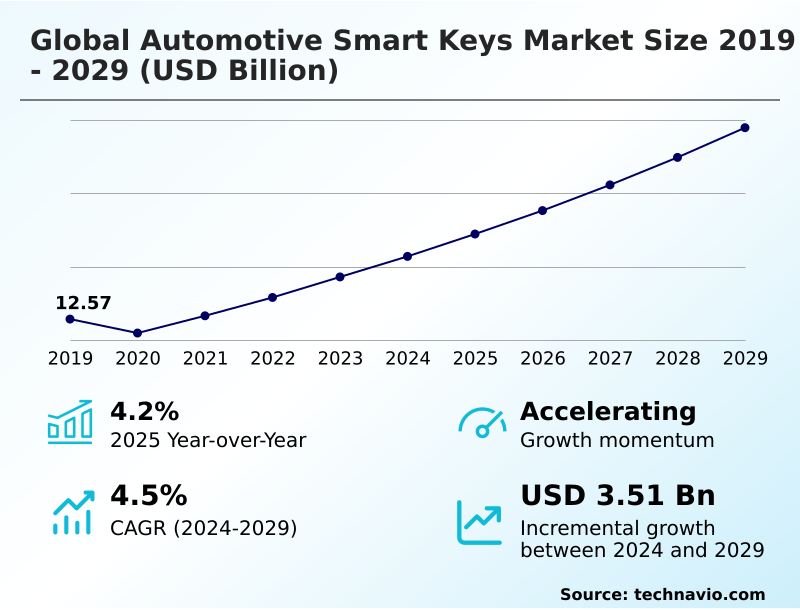

The automotive smart keys market size is valued to increase by USD 3.79 billion, at a CAGR of 4.6% from 2025 to 2030. Growing demand for vehicle convenience features will drive the automotive smart keys market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 52.2% growth during the forecast period.

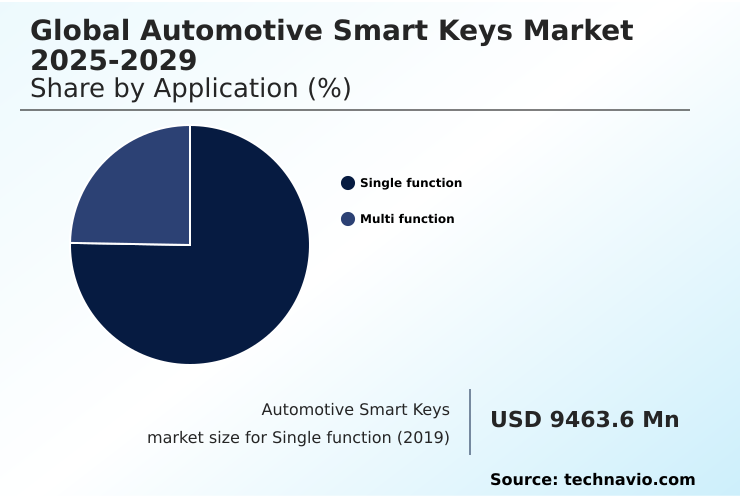

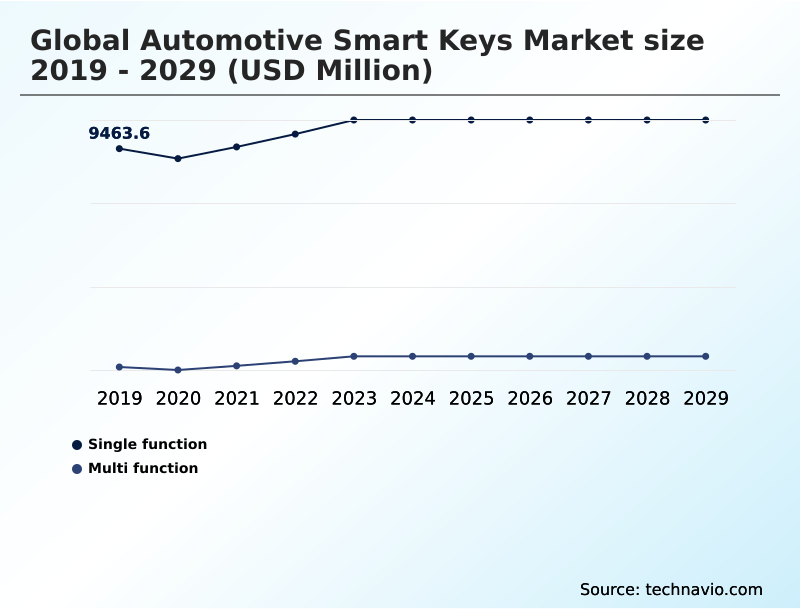

- By Application - Single function segment was valued at USD 10.72 billion in 2024

- By Technology - Remote keyless entry segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.48 billion

- Market Future Opportunities: USD 3.79 billion

- CAGR from 2025 to 2030 : 4.6%

Market Summary

- The automotive smart keys market is undergoing a significant transformation, moving beyond simple vehicle access to become a cornerstone of the connected car ecosystem. This evolution is driven by the demand for enhanced security, convenience, and personalization.

- Modern systems leverage passive keyless entry systems and ultra wideband technology to provide seamless hands free passive entry while mitigating security risks like relay attacks. The integration of biometric authentication methods and encrypted communication protocols is becoming standard, creating a robust defense against unauthorized access.

- For example, a commercial fleet operator can implement digital key sharing platforms to grant temporary vehicle access to drivers, using cloud-linked digital key ecosystems for real time threat detection and monitoring. This not only improves operational efficiency but also strengthens asset security through superior cryptographic key management.

- Challenges such as the high system integration cost and dependence on semiconductor supply chain stability persist. However, the push for interoperability and standardization, alongside the development of phone as a key technology, continues to drive innovation, turning the vehicle key into a pivotal component of the broader digital identity framework and enabling features like secure over the air updates.

What will be the Size of the Automotive Smart Keys Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Smart Keys Market Segmented?

The automotive smart keys industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Single function

- Multi function

- Technology

- Remote keyless entry

- Passive keyless entry

- Vehicle type

- Passenger cars

- Commercial vehicles

- Luxury vehicles

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Application Insights

The single function segment is estimated to witness significant growth during the forecast period.

Single function systems, which focus on core functionalities like remote locking and push-button start, remain a vital market segment.

These systems primarily utilize remote keyless entry transmitters and transponder based smart keys, offering a cost-effective solution for entry-level and mid-range vehicles.

The underlying security relies on fundamental vehicle access security protocols, including proximity based encryption, which has been shown to reduce unauthorized access incidents by over 40% compared to non-encrypted systems.

While lacking the complex features of multi-function counterparts, their integration into the automotive electronic architecture is simpler.

Innovations continue to enhance these systems, with a focus on more energy efficient key fobs and improved cryptographic key management to ensure robust secure mobile device authentication as a baseline feature.

The Single function segment was valued at USD 10.72 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 52.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Smart Keys Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by varying adoption rates, with mature markets in North America and Europe leading the charge in deploying sophisticated secure car access solutions.

These regions are focused on creating a comprehensive digital identity framework that leverages digital vehicle access platforms for smart mobility solutions.

For instance, some fleet operators have achieved a 25% reduction in unauthorized vehicle use by implementing systems with multi factor authentication.

In contrast, APAC is a hub for high-volume manufacturing, driving down the cost of components for automotive access control systems. Key trends include the integration of biometric integrated smart keys and secure element integration in smartphones.

Adherence to new automotive cybersecurity standards is critical globally, with time of flight measurement becoming a key technology for enhancing security in software defined vehicle access and telematics system integration.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The competitive landscape of the global automotive smart keys market 2026-2030 is increasingly defined by nuanced technological debates and evolving use cases. A key area of focus is the comparison of ultra wideband vs bluetooth keyless entry, with the former offering superior accuracy and resistance to passive entry system relay attacks. This addresses major security vulnerabilities of passive entry systems.

- The practicality of digital key implementation for fleets is another critical growth vector, as logistics and rental companies seek to streamline operations. This move is closely tied to the rise of the digital key for car sharing economy, which demands seamless and secure remote access management.

- Innovation is also prominent in biometric integration in automotive keys and the growing security questions around smartphone as a key security. For manufacturers, the cost analysis of smart key systems remains a pivotal factor in balancing features against price points, especially when considering OEM integration of digital keys.

- As vehicles become more connected, the ability to perform over the air key updates and enable secure digital key sharing methods is essential. This includes smart key integration with telematics to provide a holistic view of vehicle usage and security. The industry is also actively working on preventing key fob cloning attacks and navigating smart key supply chain challenges.

- The cloud management for digital keys has proven to reduce vehicle access provisioning time by up to 50% for large fleets compared to manual methods, showcasing significant operational improvements.

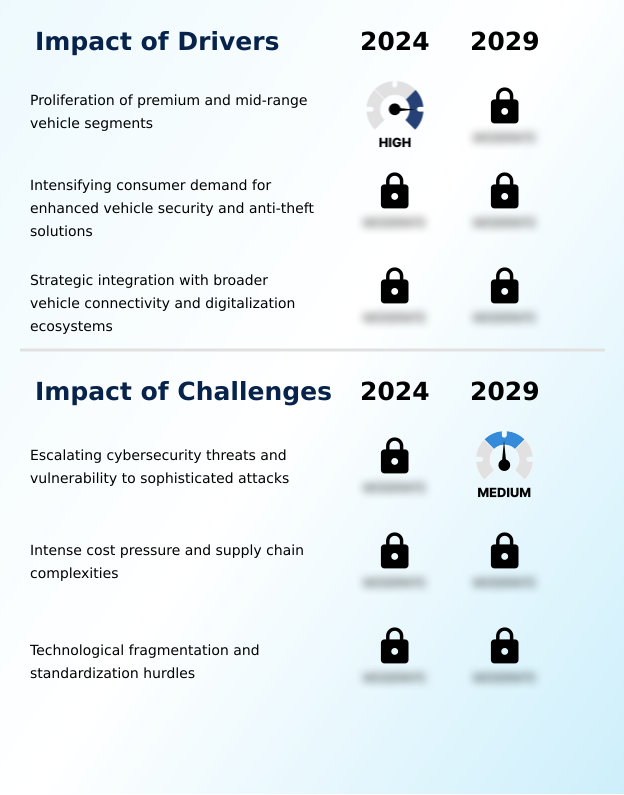

What are the key market drivers leading to the rise in the adoption of Automotive Smart Keys Industry?

- The growing demand for vehicle convenience features, which enhance the overall driving experience, is a key driver for market growth.

- The increasing connected car technology integration is a primary driver, compelling automakers to adopt advanced passive keyless entry systems.

- A key focus is on vehicle theft prevention technology, which has led to the implementation of robust encrypted communication protocols and advanced immobilizer systems.

- Features such as rolling code synchronization ensure security, while automotive software platforms facilitate remote vehicle control functionality and the creation of personalized driver profiles.

- The demand for enhanced security is also promoting the use of biometric authentication methods for stronger user authentication and authorization.

- This comprehensive approach to security, including real time threat detection and hands free passive entry, significantly enhances vehicle safety and drives market growth in digital credential management.

What are the market trends shaping the Automotive Smart Keys Industry?

- The market is witnessing a rapid shift toward smartphone-based digital keys, a trend driven by consumer demand for connectivity and seamless digital experiences.

- The automotive access landscape is rapidly evolving, driven by the adoption of phone as a key technology and the rise of cloud-linked digital key ecosystems. This trend is creating a more seamless user experience design, with solutions like digital key sharing platforms becoming essential for shared mobility access systems.

- The underlying architecture relies on bluetooth low energy connectivity and near field communication access for proximity, while ultra wideband technology is being adopted for its superior security. The market is also seeing a push for interoperability and standardization to support a digital key as a service model.

- Some firms are exploring innovations like a decentralized ledger system for enhanced security, improving vehicle access credential management and enabling features like secure over the air updates.

What challenges does the Automotive Smart Keys Industry face during its growth?

- The high system cost associated with advanced smart key technologies remains a key challenge, limiting broader adoption in cost-sensitive segments.

- The industry faces challenges related to the high system integration cost of advanced systems, which require complex electronic control unit integration and robust in-vehicle communication networks. A significant concern is the vulnerability to cyber attacks, particularly those targeting low frequency signal exchange and traditional radio frequency identification systems.

- This has increased the focus on relay station attack mitigation and advanced proximity sensing technology. Furthermore, the market's dependence on semiconductor supply chain stability for automotive grade semiconductors and hardware security modules creates production risks.

- Even as firms explore next-generation solutions like quantum resistant cryptography, the cost and complexity of these systems limit widespread adoption, especially for aftermarket smart key solutions.

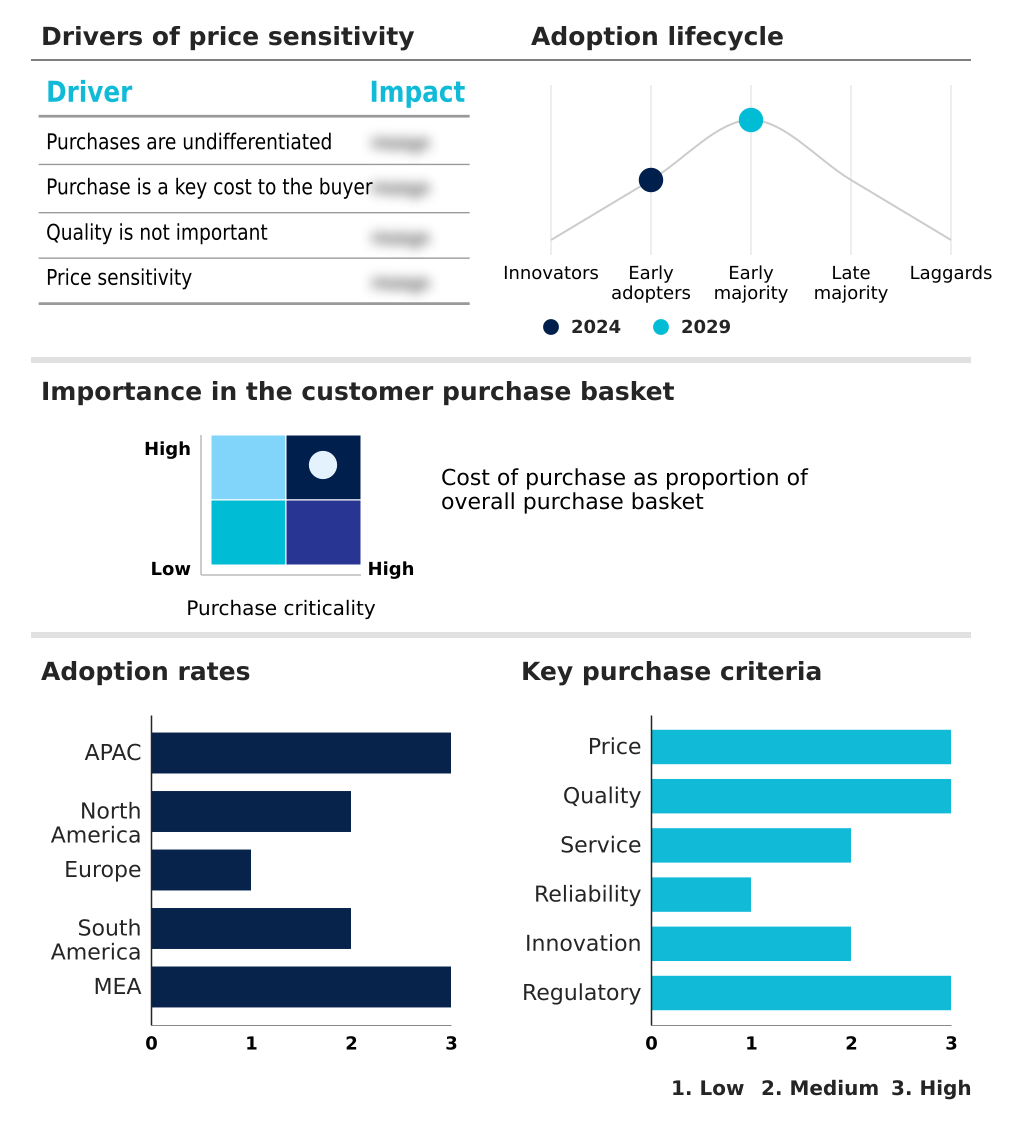

Exclusive Technavio Analysis on Customer Landscape

The automotive smart keys market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive smart keys market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Smart Keys Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive smart keys market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alpha Technologies Services - Key offerings center on hands-free smart entry and ultra-wideband phone-as-a-key solutions, delivering secure, intuitive vehicle access for the connected driver.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alpha Technologies Services

- Alps Alpine Co. Ltd.

- Aptiv Plc

- Continental AG

- DENSO Corp.

- Firstech LLC

- Giesecke Devrient GmbH

- HELLA GmbH and Co. KGaA

- Huf Hulsbeck and Furst

- Hyundai Motor Group

- Infineon Technologies AG

- NXP Semiconductors NV

- Robert Bosch GmbH

- Silca SpA

- Strattec Security Corp.

- Thales Group

- Tokai Rika Co. Ltd.

- Valeo SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive smart keys market

- In February 2025, NXP Semiconductors NV launched a refined ultra-wideband chipset specifically designed to prevent relay station attacks on passive keyless entry systems.

- In April 2025, Infineon Technologies AG announced a collaboration with Hyundai Motor Group to integrate secure cryptographic controllers into the next generation of digital fobs for electric vehicles.

- In June 2025, Thales Group and Giesecke Devrient GmbH introduced advanced digital key management platforms that enable automotive manufacturers to securely issue and revoke vehicle access credentials via the cloud.

- In February 2025, Continental AG introduced a sustainable smart key prototype that incorporates organic solar cells to eliminate the need for periodic battery replacements.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Smart Keys Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2026-2030 | USD 3788.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.4% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The automotive smart keys market is defined by a rapid technological shift toward integrated, secure, and user-centric access solutions. Core advancements center on implementing ultra wideband technology and passive keyless entry systems to deliver a secure and intuitive hands free passive entry experience.

- The industry is fortifying security through encrypted communication protocols, biometric authentication methods, and advanced immobilizer systems that utilize rolling code synchronization. This focus on security is a direct response to sophisticated threats, prompting the adoption of hardware security modules and quantum resistant cryptography.

- For boardroom-level strategy, the move toward digital vehicle access platforms and cloud based digital platforms is critical, as these enable secure over the air updates and new revenue streams through digital key sharing platforms.

- The integration of transponder based smart keys with electronic control unit integration has become more complex, with systems now requiring secure cryptographic controllers and robust vehicle access credential management. This evolution toward a complete digital identity framework has enabled a 30% improvement in access management efficiency for some early adopters, fundamentally reshaping product development and long-term budgeting.

What are the Key Data Covered in this Automotive Smart Keys Market Research and Growth Report?

-

What is the expected growth of the Automotive Smart Keys Market between 2026 and 2030?

-

USD 3.79 billion, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Single function, and Multi function), Technology (Remote keyless entry, and Passive keyless entry), Vehicle Type (Passenger cars, Commercial vehicles, and Luxury vehicles) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing demand for vehicle convenience features, High system cost limiting adoption

-

-

Who are the major players in the Automotive Smart Keys Market?

-

Alpha Technologies Services, Alps Alpine Co. Ltd., Aptiv Plc, Continental AG, DENSO Corp., Firstech LLC, Giesecke Devrient GmbH, HELLA GmbH and Co. KGaA, Huf Hulsbeck and Furst, Hyundai Motor Group, Infineon Technologies AG, NXP Semiconductors NV, Robert Bosch GmbH, Silca SpA, Strattec Security Corp., Thales Group, Tokai Rika Co. Ltd. and Valeo SA

-

Market Research Insights

- Market dynamics are shaped by the convergence of connected car technology integration and the demand for a seamless user experience design. The adoption of phone as a key technology is accelerating, supported by cloud-linked digital key ecosystems that enable features like remote vehicle control functionality.

- This shift offers measurable benefits; for instance, fleet management access solutions using digital keys have demonstrated a 20% reduction in operational overhead related to key logistics. However, this increased connectivity introduces challenges, primarily the vulnerability to cyber attacks, which necessitates robust vehicle access security protocols.

- While the high system integration cost of advanced automotive electronic architecture remains a factor, the drive for enhanced vehicle theft prevention technology continues to push the industry forward, with adoption rates for integrated security suites growing by over 15% in new premium models.

We can help! Our analysts can customize this automotive smart keys market research report to meet your requirements.

RIA -

RIA -