Automotive Subscription Services Market Size 2026-2030

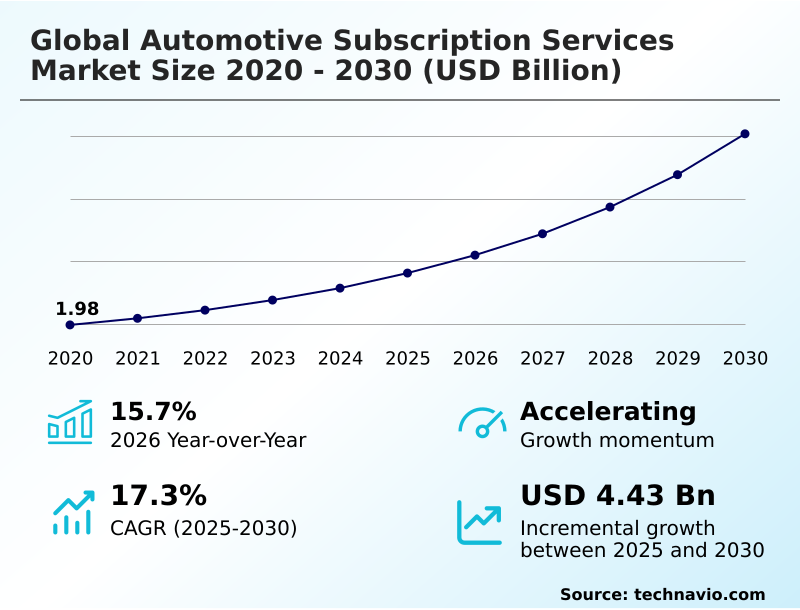

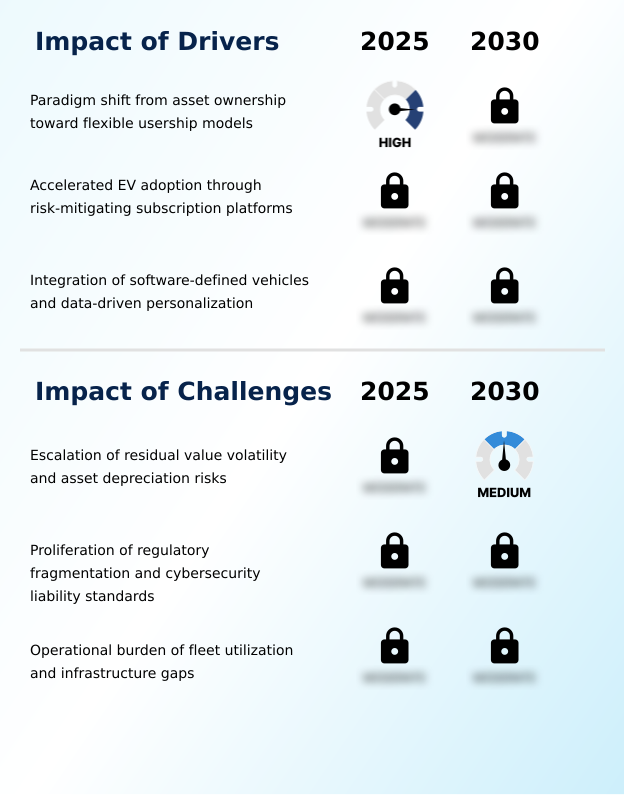

The automotive subscription services market size is valued to increase by USD 4.43 billion, at a CAGR of 17.3% from 2025 to 2030. Paradigm shift from asset ownership toward flexible usership models will drive the automotive subscription services market.

Major Market Trends & Insights

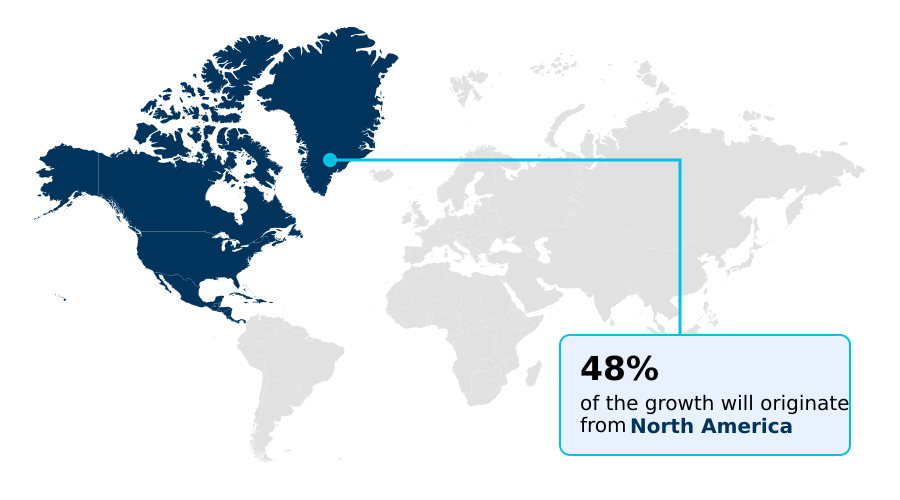

- North America dominated the market and accounted for a 48.3% growth during the forecast period.

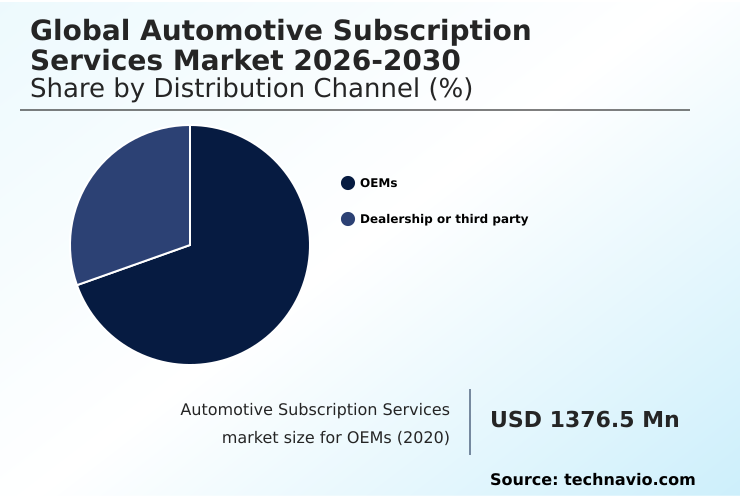

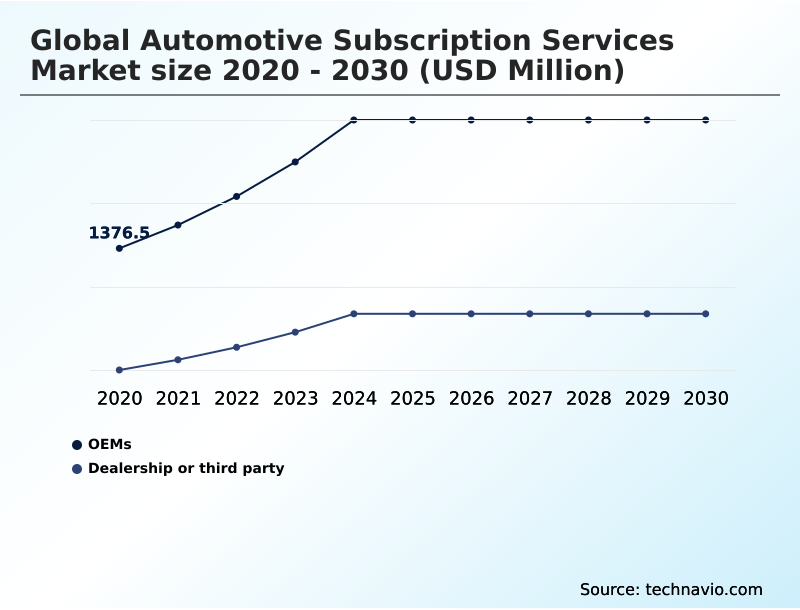

- By Distribution Channel - OEMs segment was valued at USD 2.19 billion in 2024

- By Type - Multi-brand subscriptions segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.08 billion

- Market Future Opportunities: USD 4.43 billion

- CAGR from 2025 to 2030 : 17.3%

Market Summary

- The automotive subscription services market represents a fundamental transformation in personal and corporate mobility, pivoting from traditional ownership to flexible, usage-based models. This evolution is driven by a consumer preference for convenience, where an all-inclusive monthly payment covers insurance, maintenance, and other associated costs, facilitated by seamless digital onboarding and app-based vehicle management.

- A key trend accelerating this shift is the rise of the software-defined vehicle, which allows for functions-on-demand and over-the-air updates, creating new recurring revenue streams.

- For instance, a logistics company can dynamically scale its delivery fleet for peak seasons using a corporate car subscription service, leveraging telematics data to optimize routes and monitor vehicle health, thereby enhancing operational efficiency without long-term capital expenditure.

- However, the industry grapples with significant challenges, including managing the residual value risk of rapidly advancing electric vehicle fleets and the operational complexity of maintaining high vehicle utilization rates across geographically dispersed user bases.

What will be the Size of the Automotive Subscription Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Automotive Subscription Services Market Segmented?

The automotive subscription services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- OEMs

- Dealership or third party

- Type

- Multi-brand subscriptions

- Single-brand subscriptions

- End-user

- Individual

- Business

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- South Korea

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The oems segment is estimated to witness significant growth during the forecast period.

The Original Equipment Manufacturers (OEMs) segment is foundational, representing a strategic shift from transactional sales to recurring service-oriented revenue streams. This channel enables direct-to-consumer models, allowing brands to cultivate customer lifetime value with younger, asset-light demographics.

By offering all-inclusive pricing and digital subscription tiers, OEMs lower entry barriers for premium and electric vehicles. These electric vehicle experience programs serve as a low-risk gateway for consumers.

This model's success is tied to a seamless digital onboarding process and the ability to manage vehicle lifecycle management effectively.

Data confirms this pivot, with some OEMs reporting a 24% increase in software-based revenue driven by commercial telematics data and fleet management software, transforming the car into a dynamic, software-defined vehicle.

The OEMs segment was valued at USD 2.19 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 48.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Subscription Services Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which captures nearly half the market's incremental growth, driven by consumer demand for on-demand transportation and asset-light mobility. This region benefits from a mature ecosystem of third-party providers offering vehicle swap services.

Conversely, the APAC region is the fastest-growing geography, with a projected growth rate almost 20% higher than Europe's, fueled by rapid urbanization and a digitally native consumer base.

This expansion is supported by marketplace-based car subscriptions and a strong interest in commercial vehicle subscriptions.

The adoption of advanced driver assistance systems and EV charging solutions is a key factor across all developed regions, with data-driven personalization becoming a competitive differentiator.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Understanding the automotive subscription services market growth requires a comprehensive look at its business model canvas. For entrepreneurs asking how to start a car subscription business, the initial focus must be on securing capital for fleet acquisition and developing software for managing vehicle subscriptions.

- A key decision involves choosing between an OEM-backed service and finding the best multi-brand automotive subscription, which often involves comparing OEM vs third-party car subscriptions. The rise of specialized niches, such as automotive subscription services for gig workers and automotive subscription services for startups, presents unique opportunities.

- Financial viability hinges on managing depreciation, leading many to seek residual value insurance for subscription fleets. Moreover, using telematics for subscription pricing models is becoming critical for profitability, while effective customer retention strategies for car subscriptions are essential for long-term success.

- Operators must also consider the tax implications of business car subscriptions and the complexities of integrating EV charging into subscription packages. The benefits of car subscription over leasing are clear, but providers offering an all-inclusive car subscription with no deposit face higher risk.

- Emerging trends include luxury car subscription with driver service and the logistical challenges of cross-border car subscription services, all while navigating data privacy in vehicle subscription apps and managing fleet maintenance for subscriptions. Addressing cybersecurity risks in connected car subscriptions remains a paramount concern for all stakeholders.

- Platforms that integrate telematics for subscription pricing models have demonstrated an ability to reduce unauthorized vehicle use by more than 15% compared to those with fixed-rate plans.

What are the key market drivers leading to the rise in the adoption of Automotive Subscription Services Industry?

- A key market driver is the fundamental paradigm shift from traditional asset ownership toward flexible, access-based usership models.

- A fundamental driver is the consumer shift toward flexible vehicle access, moving away from long-term financial commitments. This has spurred the growth of both OEM-led direct-to-consumer models and multi-brand vehicle access platforms.

- The all-inclusive monthly payment structure, bundling car subscription insurance and maintenance, simplifies budgeting for users.

- Subscription models also serve as a critical tool for fleet electrification, lowering EV adoption barriers; some providers report that over 25% of users who trial an EV via subscription subsequently purchase one.

- The adoption of app-based vehicle management and digital key access streamlines the user experience, boosting customer lifetime value and making on-demand transportation a practical reality for a wider audience.

What are the market trends shaping the Automotive Subscription Services Industry?

- A defining market trend is the integration of software-defined vehicle features. This shift is enabling the creation of digital subscription tiers for on-demand functionalities and services.

- The market is structurally realigning toward digital-first offerings, where the physical asset is secondary to the services it enables. A key trend is the growth of functions-on-demand, where capabilities like advanced infotainment content are unlocked via recurring billing. This user-centric mobility approach is enhanced by seamless digital onboarding processes.

- For instance, some providers have doubled their software-based revenue year-over-year by focusing on commercial telematics. This pivot to a subscription-based model is particularly effective for subscription fleet electrification, with some European markets seeing battery-electric vehicles, often introduced through subscriptions, achieve nearly 20% of new registrations. This strategy relies on effective vehicle lifecycle management and robust connected services to succeed.

What challenges does the Automotive Subscription Services Industry face during its growth?

- A primary challenge affecting industry growth is the escalating volatility of residual values and the associated risks of asset depreciation for fleet operators.

- The market faces significant operational and financial challenges. The primary issue is managing residual value risk, as the accelerated asset depreciation of early-model EVs can result in losses exceeding 40% of the initial value within two years.

- Another hurdle is the high cost associated with vehicle utilization; logistical expenses for cleaning and delivering vehicles can account for up to 15% of the monthly subscription fee, eroding margins. This is compounded by cybersecurity liability in software-defined vehicles and the complexity of remarketing used vehicle subscription fleets.

- These factors create economic friction, forcing providers to build significant risk premiums into their dynamic pricing models.

Exclusive Technavio Analysis on Customer Landscape

The automotive subscription services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive subscription services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Subscription Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive subscription services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Audi of America - Provides flexible, all-inclusive premium vehicle access through subscription models, bundling insurance and maintenance to streamline user mobility and reduce ownership costs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Audi of America

- Autonomy

- BMW of North America LLC

- Cadillac

- Cazoo Ltd.

- Dr. Ing. h.c. F. Porsche AG

- Electric Road

- Finn.auto

- FlexClub

- Ford Motor Co.

- Hyundai Motor Co.

- KIA CORP.

- Lexus

- Loopit

- Mercedes Benz USA LLC

- Renault SAS

- SIXT SE

- Stellantis NV

- Wagonex Ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive subscription services market

- In March, 2025, SIXT SE announced a record fiscal year for 2024, attributed to the successful global expansion of its SIXT Plus subscription platform and the rollout of its SIXT ONE digital ecosystem, which enhances fleet management across North America and Europe.

- In February, 2025, The European Union initiated new data frameworks to formalize protocols for sharing and commercializing connected vehicle data, creating significant compliance complexities for providers of cross-border subscription services.

- In October, 2024, Volvo Cars reaffirmed its long-term strategic commitment to its Care by Volvo platform, highlighting the integration of its newest fully electric models to accelerate EV adoption among urban professionals.

- In September, 2024, Stellantis NV initiated a strategic business reset to better align its vehicle fleet availability with shifting consumer demand for hybrids and advanced internal combustion engines within its subscription and sales channels.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Subscription Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 286 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 17.3% |

| Market growth 2026-2030 | USD 4430.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, South Korea, India, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is defined by the convergence of the software-defined vehicle and new business structures. Original equipment manufacturers and third-party providers are leveraging a SaaS platform approach to offer digital subscription tiers with all-inclusive pricing.

- This is enabled by connected car technologies that provide a constant stream of telematics data, which is crucial for predictive maintenance, data-driven personalization, and creating dynamic pricing models. The concept of functions-on-demand, delivered via over-the-air updates for infotainment content and advanced driver assistance systems, is central to this shift.

- This creates a system of recurring billing and fundamentally alters vehicle lifecycle management. While mobility-as-a-service and multi-modal mobility are expanding the service scope with concierge services and EV charging solutions, significant hurdles remain. Firms must manage asset depreciation and residual value through effective remarketing to maintain high vehicle utilization.

- Furthermore, the increasing reliance on connected services introduces significant cybersecurity liability, a boardroom-level concern. The deployment of over-the-air updates to millions of vehicles has demonstrated a significant increase in customer engagement, with feature adoption rates climbing by over 30% post-update.

- This move toward fleet electrification through electric vehicle experience programs, managed via white-label technology platform and app-based vehicle management with digital key access and seamless digital onboarding, is reshaping the industry.

What are the Key Data Covered in this Automotive Subscription Services Market Research and Growth Report?

-

What is the expected growth of the Automotive Subscription Services Market between 2026 and 2030?

-

USD 4.43 billion, at a CAGR of 17.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (OEMs, and Dealership or third party), Type (Multi-brand subscriptions, and Single-brand subscriptions), End-user (Individual, and Business) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Paradigm shift from asset ownership toward flexible usership models, Escalation of residual value volatility and asset depreciation risks

-

-

Who are the major players in the Automotive Subscription Services Market?

-

Audi of America, Autonomy, BMW of North America LLC, Cadillac, Cazoo Ltd., Dr. Ing. h.c. F. Porsche AG, Electric Road, Finn.auto, FlexClub, Ford Motor Co., Hyundai Motor Co., KIA CORP., Lexus, Loopit, Mercedes Benz USA LLC, Renault SAS, SIXT SE, Stellantis NV and Wagonex Ltd

-

Market Research Insights

- The market's dynamism is rooted in the shift toward user-centric mobility, where flexible vehicle access and all-inclusive monthly payments are standard. This subscription-based model appeals to consumers seeking alternatives to car subscription vs leasing, driven by a desire for no-commitment car access. The competitive environment is pushing providers to innovate with offerings like drive-to-buy financing and specialized corporate car subscriptions.

- This evolution is delivering tangible results; commercial operators using subscription fleet electrification report software-related revenue increases of over 20%. Furthermore, in certain mature markets, EV-focused car subscriptions now account for nearly one-fifth of new battery-electric vehicle registrations, demonstrating the model's effectiveness in lowering adoption barriers.

We can help! Our analysts can customize this automotive subscription services market research report to meet your requirements.

RIA -

RIA -