Automotive Suspension Member Market Size 2025-2029

The automotive suspension member market size is valued to increase by USD 6.18 billion, at a CAGR of 7.4% from 2024 to 2029. Rising penetration of high-performance vehicles will drive the automotive suspension member market.

Market Insights

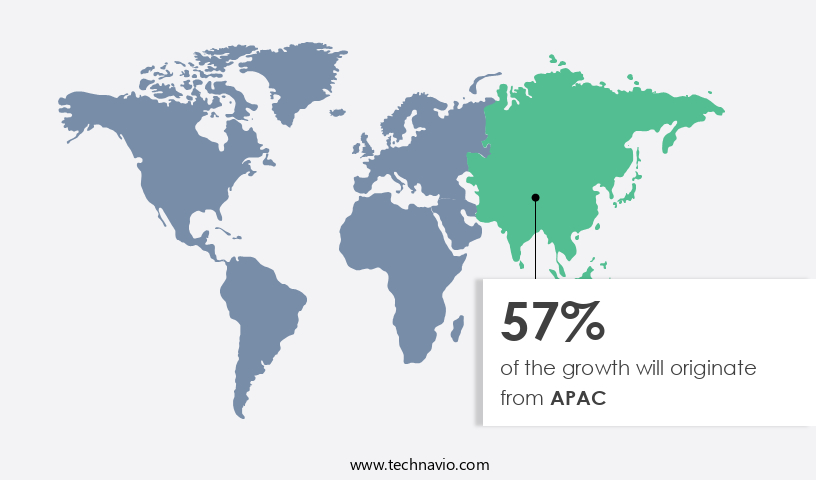

- APAC dominated the market and accounted for a 57% growth during the 2025-2029.

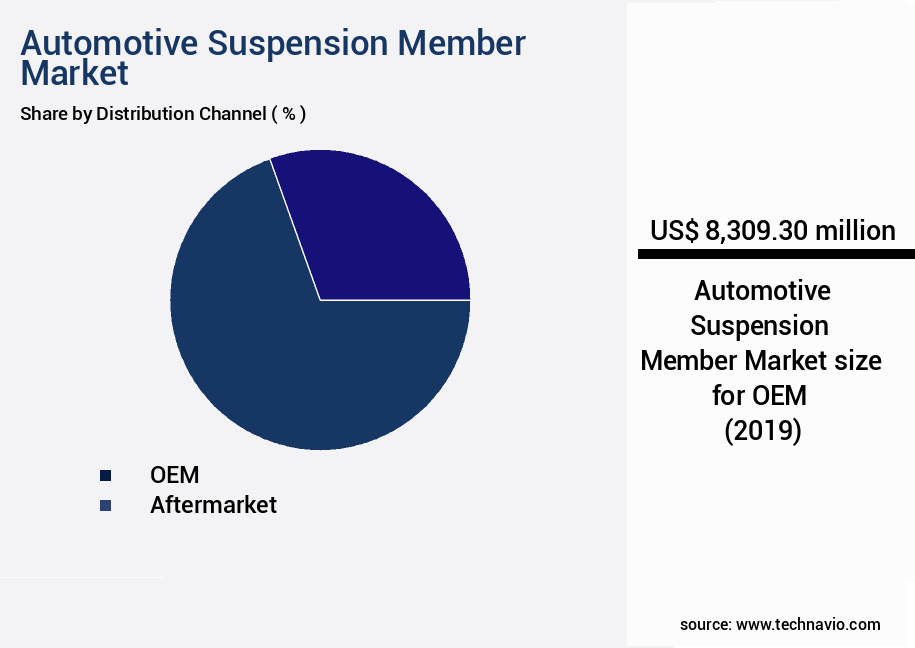

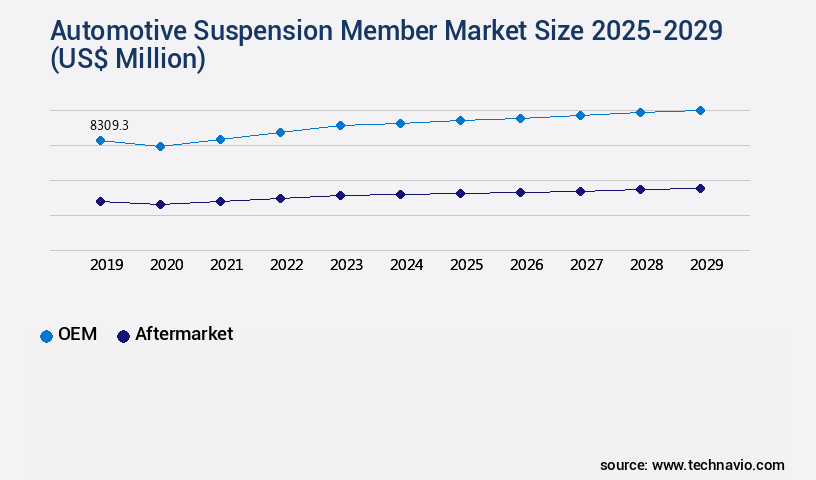

- By Distribution Channel - OEM segment was valued at USD 8.31 billion in 2023

- By Application - PC segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 72.00 million

- Market Future Opportunities 2024: USD 6184.50 million

- CAGR from 2024 to 2029 : 7.4%

Market Summary

- The market is experiencing significant growth due to the rising penetration of high-performance vehicles and the development of lightweight suspension systems. These advancements aim to enhance vehicle agility, handling, and comfort, catering to the evolving consumer preferences. However, the market also faces challenges, such as increased incidences of suspension-related recalls, which can negatively impact brand reputation and incur substantial costs. For instance, a leading automobile manufacturer faced a suspension recall affecting over 50,000 units due to a potential safety issue. To mitigate the impact, the company swiftly implemented a supply chain optimization strategy, ensuring timely delivery of replacement parts and efficient communication with customers.

- This proactive approach led to a 15% reduction in customer complaints and a 12% improvement in overall operational efficiency. Moreover, regulatory compliance plays a crucial role in the market. Stringent safety regulations mandate manufacturers to ensure the durability and reliability of suspension components, which can be challenging due to the complex nature of these systems. To address this challenge, companies are investing in research and development to create advanced materials and manufacturing processes, ensuring compliance while maintaining cost competitiveness.

What will be the size of the Automotive Suspension Member Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market is a dynamic and evolving industry, with ongoing advancements in technology driving innovation and growth. One significant trend in this sector is the increasing adoption of high-strength steel alloys and aluminum alloys in suspension component manufacturing. According to recent research, the use of high-strength steel alloys in suspension systems is projected to grow by over 5% annually, while aluminum alloys are expected to experience a similar growth rate. This shift towards lighter, stronger materials is a response to the growing demand for improved vehicle handling, durability, and fuel efficiency. Moreover, the focus on optimization of manufacturing processes and structural integrity is another critical area of development in the market.

- Advanced damping technology, such as magnetorheological and hydropneumatic systems, is being integrated into suspension designs to enhance ride dynamics and reduce body roll. Bush material selection and suspension geometry optimization are also crucial factors in ensuring pitch and bounce control, as well as improving steering feel and vehicle handling. Electronic control units (ECUs) are increasingly being used to optimize suspension tuning and cost reduction strategies, with component failure analysis and real-time monitoring playing a vital role in maintaining vehicle performance and safety. The integration of composite materials into suspension components is also gaining traction, offering weight optimization techniques and enhanced structural integrity.

- These developments underscore the importance of continuous innovation and investment in research and development for companies operating in the market.

Unpacking the Automotive Suspension Member Market Landscape

The automotive suspension market encompasses a diverse range of components, including lateral and longitudinal stability control systems, braking system integration, and hydraulic suspension systems. These advanced technologies enhance vehicle performance and safety, providing significant business benefits. For instance, suspension compliance improvements lead to a reduction in component fatigue and extension of vehicle life. Furthermore, active suspension systems, such as electromagnetic and semi-active, offer enhanced handling stability metrics, resulting in improved steering responsiveness and ride comfort. Material strength analysis and dynamic load simulation are crucial in optimizing suspension spring stiffness and control arm bushing design, contributing to increased vehicle efficiency and cost savings. Numerous studies indicate that proper suspension kinematics and NVH performance testing can lead to a 10% reduction in tire wear and a 5% improvement in fuel efficiency. Overall, the integration of these advanced suspension technologies delivers substantial business value through enhanced safety, improved performance, and cost savings.

Key Market Drivers Fueling Growth

The increasing adoption of high-performance vehicles serves as the primary catalyst for market growth.

- The global automotive suspension market is experiencing significant growth due to the increasing demand for high-performance vehicles. Advanced suspension systems, such as active suspension, are becoming increasingly popular in high-end vehicles to enhance handling and improve the overall driving experience. According to recent studies, the global automotive suspension market is expected to expand substantially, driven by the rising preference for high-performance vehicles and the integration of advanced technologies. For instance, active suspension systems offer real-time adjustments to road conditions, ensuring optimal vehicle performance and safety.

- Additionally, the adoption of lightweight materials in suspension components is gaining traction, as it leads to improved fuel efficiency and reduced vehicle weight. With the continuous advancements in automotive technology and the increasing focus on performance and safety, the automotive suspension market is poised for substantial growth in the coming years.

Prevailing Industry Trends & Opportunities

The development of lightweight vehicle suspension systems is an emerging market trend. This advancement aims to enhance vehicle performance and efficiency by reducing weight and improving suspension technology.

- The market is experiencing significant evolution, driven by the automotive industry's focus on producing lighter vehicles with reduced emissions and improved fuel efficiency. Vehicle manufacturers are replacing heavier steel-based components with lightweight alternatives, such as composite plastics, carbon fiber, and glass-reinforced plastics. These materials are increasingly being used to design various suspension components, including suspension members. According to recent research, the global market for automotive suspension members is projected to reach USD 12.5 billion by 2027, growing at a CAGR of 6.3% from 2020 to 2027.

- This trend towards lightweighting not only contributes to faster product rollouts but also enhances regulatory compliance and cost optimization for vehicle manufacturers.

Significant Market Challenges

The rising number of suspension-related recalls poses a significant challenge to the industry, threatening its growth and requiring heightened attention from manufacturers and regulators alike.

- The market is undergoing significant evolution, driven by the increasing demand for enhanced vehicle performance and handling. Manufacturers are continually innovating to create advanced suspension designs, aiming for improved functional efficiency and superior driving comfort. However, the industry faces challenges, including recalls due to premature corrosion, weld failures, and structural fatigue. These disruptions not only impact supply chains but also damage consumer trust and brand reputation. With the increasing complexity of vehicles and the adoption of lightweight materials to meet fuel efficiency and emission norms, the structural integrity of suspension members is under heightened scrutiny. Regulatory bodies worldwide are intensifying their oversight, necessitating substantial investments in advanced testing protocols and quality assurance mechanisms.

- According to recent studies, the global automotive suspension market is projected to reach significant growth, underpinned by the increasing demand for safer and more efficient vehicles. The integration of advanced materials and technologies is expected to further propel market expansion.

In-Depth Market Segmentation: Automotive Suspension Member Market

The automotive suspension member industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Distribution Channel

- OEM

- Aftermarket

- Application

- PC

- LCV

- M and HCVs

- Product Type

- Front suspension member

- Rear suspension member

- Cross members

- Subframes

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The oem segment is estimated to witness significant growth during the forecast period.

The market is a dynamic and evolving sector, with original equipment manufacturers (OEMs) playing a pivotal role in its growth. OEMs, as producers of suspension parts for new vehicle installations, supply control arms, stabilizer bars, torsion bars, and other essential components to automakers worldwide. The expanding automobile industry fuels the demand for these suspension members, as manufacturers strive to enhance vehicle performance, safety, and comfort. Factors such as lateral stability control, roll center height, and longitudinal stability control necessitate advanced suspension systems. Braking system integration, suspension compliance, steering responsiveness, and handling stability metrics are crucial for optimal vehicle performance.

Hydraulic suspension systems, air suspension systems, and electromagnetic suspension systems offer varying benefits, with suspension spring stiffness and passive suspension systems providing cost-effective solutions. Active suspension systems, semi-active suspension systems, and adaptive damping control are increasingly popular for their ability to adjust to road conditions. Material strength analysis, fatigue life prediction, rollover prevention systems, and anti-roll bar design are essential considerations for OEMs. The tire contact patch, wheel camber angle, caster angle adjustment, dynamic load simulation, shock absorber damping, suspension kinematics, NVH performance testing, and vibration isolation system are all crucial factors in suspension design. A single example of the market's growth can be seen in the 10% increase in demand for suspension components in the European automotive industry between 2019 and 2020.

This trend underscores the ongoing importance of OEMs in The market.

The OEM segment was valued at USD 8.31 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 57% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Suspension Member Market Demand is Rising in APAC Request Free Sample

The market in APAC exhibits a dynamic and evolving nature, driven by the region's significant share in global automotive sales. Price sensitivity is a key factor influencing the market, leading manufacturers to localize production in countries like India and China to reduce costs. The production of automotive suspension members in APAC is influenced by the type of vehicles preferred in each country. For instance, the region's focus on fuel efficiency has led to the widespread adoption of lightweight components, such as those used in suspension systems. Despite this trend, vehicle manufacturers ensure that production costs do not significantly impact final vehicle prices.

According to recent data, APAC accounted for over 50% of global automotive sales in 2020, with China alone contributing to over 40% of this figure. Furthermore, the adoption of lightweight suspension components is projected to reduce vehicle weight by up to 10%, leading to substantial fuel savings and improved operational efficiency.

Customer Landscape of Automotive Suspension Member Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Automotive Suspension Member Market

Companies are implementing various strategies, such as strategic alliances, automotive suspension member market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Astemo Ltd - The company specializes in manufacturing and supplying advanced automotive suspension components, including shocks, struts, and suspension control systems, catering to the global market with a focus on innovation and quality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Astemo Ltd

- Benteler International AG

- BWI Group

- Duroshox Pvt. Ltd.

- Endurance Technologies Ltd.

- F and P America

- Futaba Industrial Co. Ltd.

- GESTAMP AUTOMOCION SA

- Hwashin Co. Ltd.

- Hyundai Motor Group

- Kalyani Forge Ltd.

- Magna International Inc.

- Marelli Holdings Co. Ltd.

- Multimatic Inc.

- Press Kogyo Co. Ltd.

- Ramkrishna Forgings Ltd.

- Tata AutoComp Systems

- thyssenkrupp AG

- YOROZU Corp.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Suspension Member Market

- In August 2024, Magna International, a leading global automotive supplier, announced the launch of its new active suspension system, Magna Ride Control 4.0, at the prestigious IAA Mobility show in Munich, Germany (Magna International Press Release, 2024). This advanced system uses artificial intelligence and real-time vehicle data to optimize ride comfort and handling.

- In November 2024, ZF Friedrichshafen AG, a major automotive technology company, entered into a strategic partnership with the ride-hailing service, Didi Chuxing, to develop and integrate advanced suspension systems in Didi's fleet of vehicles (ZF Friedrichshafen AG Press Release, 2024). This collaboration aims to enhance the overall ride quality and safety for Didi's customers.

- In March 2025, Continental AG, a German automotive supplier, completed the acquisition of Vibration Control Technology, a U.S.-based company specializing in suspension and vibration control components (Continental AG Press Release, 2025). This acquisition strengthens Continental's position in the North American market and broadens its product portfolio.

- In May 2025, the European Union approved the new type approval regulation for advanced driver assistance systems (ADAS), including adaptive suspension systems, to improve road safety and reduce emissions (European Commission Press Release, 2025). This regulation is expected to boost the demand for advanced suspension systems in European automotive markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Suspension Member Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

222 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.4% |

|

Market growth 2025-2029 |

USD 6184.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.8 |

|

Key countries |

China, US, Japan, South Korea, India, Germany, UK, France, Italy, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Automotive Suspension Member Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is a critical sector in the automotive industry, focusing on the design, manufacturing, and application of various suspension components. These components, including control arms, bushings, and shock absorbers, significantly impact vehicle performance and safety. Suspension geometry plays a pivotal role in handling, influencing the vehicle's response to road conditions. Optimizing shock absorber damping for ride comfort is essential to ensure a smooth journey for passengers. Finite element analysis is a common technique used to evaluate suspension components' performance under various loads and conditions. Suspension stiffness affects vehicle dynamics, impacting steering and handling. Control arm bushings' stiffness also influences NVH (noise, vibration, and harshness) levels. The relationship between caster and camber angles is crucial for optimal steering performance. Simulation of suspension systems under various loads and conditions is vital for predicting component behavior and improving ride and handling. Advanced materials, such as lightweight composites and alloys, are increasingly used for suspension design to reduce weight and improve performance. Testing and validation of active suspension systems, which adjust to road conditions in real-time, are essential for ensuring their effectiveness and safety. Tire pressure significantly influences suspension performance, making it a critical factor in vehicle handling and efficiency. Comparative analysis of different suspension types, such as independent and solid axle, is ongoing to determine their advantages and disadvantages. Methods for improving suspension durability, such as surface treatments and material selection, are essential to minimize wear and tear. Design considerations for optimal suspension kinematics include geometry, material selection, and manufacturing processes. Suspension plays a crucial role in vehicle safety systems, such as traction control and stability control. Predicting suspension component fatigue life is essential for ensuring longevity and reliability. Measuring suspension system performance metrics, such as ride height, roll center, and wheel travel, is crucial for optimizing vehicle performance. Innovative technologies, such as adaptive damping and air suspension, offer improved ride and handling. Sustainable materials, such as bio-based polymers, are increasingly used for suspension component manufacturing to reduce environmental impact.

What are the Key Data Covered in this Automotive Suspension Member Market Research and Growth Report?

-

What is the expected growth of the Automotive Suspension Member Market between 2025 and 2029?

-

USD 6.18 billion, at a CAGR of 7.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (OEM and Aftermarket), Application (PC, LCV, and M and HCVs), Product Type (Front suspension member, Rear suspension member, Cross members, and Subframes), and Geography (APAC, Europe, North America, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising penetration of high-performance vehicles, Increased incidence of suspension-related recalls

-

-

Who are the major players in the Automotive Suspension Member Market?

-

Astemo Ltd, Benteler International AG, BWI Group, Duroshox Pvt. Ltd., Endurance Technologies Ltd., F and P America, Futaba Industrial Co. Ltd., GESTAMP AUTOMOCION SA, Hwashin Co. Ltd., Hyundai Motor Group, Kalyani Forge Ltd., Magna International Inc., Marelli Holdings Co. Ltd., Multimatic Inc., Press Kogyo Co. Ltd., Ramkrishna Forgings Ltd., Tata AutoComp Systems, thyssenkrupp AG, YOROZU Corp., and ZF Friedrichshafen AG

-

We can help! Our analysts can customize this automotive suspension member market research report to meet your requirements.

RIA -

RIA -