Automotive Transmission Fluid Market Size 2024-2028

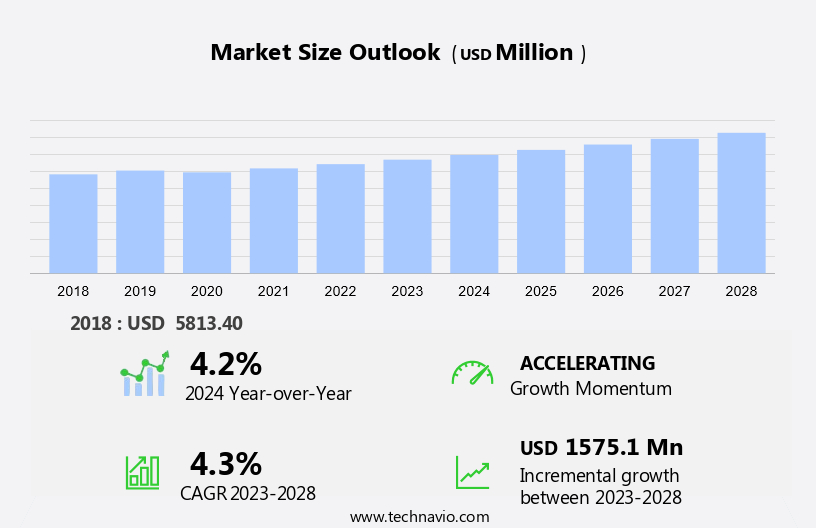

The automotive transmission fluid market size is forecast to increase by USD 1.58 billion at a CAGR of 4.3% between 2023 and 2028.

- The market is experiencing significant growth due to several key factors. Rising household income in the US is leading to increased disposable funds for consumers, allowing them to invest in personal vehicles. In addition, there is a growing focus on fuel efficiency and environmental sustainability, leading to the demand for biodegradable transmission fluids. The market is evolving with advancements in lubricant technology and fluid performance to meet the demands of passenger vehicle and electric vehicle adoption, autonomous driving, and smart mobility.

- Furthermore, product differentiation is also driving market growth, as OEMs seek to offer specialized transmission fluids for their vehicles to enhance performance and extend maintenance intervals. Furthermore, the shift towards electric power trains is creating opportunities for new types of transmission fluids to cater to the unique requirements of these vehicles. Overall, the market is poised for continued expansion, driven by these market trends and the evolving needs of the automotive industry.

What will be the Size of the Market During the Forecast Period?

- The market is experiencing significant growth due to advancements in transmission technology and the increasing demand for improved vehicle performance. Transmission fluids play a crucial role in ensuring the smooth operation of automotive drivetrains, enabling optimal engine efficiency and vehicle safety. The global automotive market is expanding, driven by factors such as urban transportation needs, increasing vehicle sales, and the future of mobility. As a result, the demand for high-performance transmission fluids is on the rise. Environmental concerns are also influencing the automotive industry, leading to the adoption of green technology and sustainable transportation solutions.

- Furthermore, transmission fluids with lower carbon emissions and better energy efficiency are becoming increasingly popular. Moreover, the integration of advanced technologies such as autonomous driving, connected car technology, and electric vehicle adoption is transforming the automotive landscape. These technologies require specialized transmission fluids that can handle the unique demands of electric drivetrains and autonomous systems. The automotive supply chain is also undergoing optimization, with a focus on logistics solutions and efficiency improvements. Transmission fluid manufacturers are adapting to these changes by offering just-in-time delivery and customized solutions for various vehicle applications. The automotive industry is subject to numerous regulations aimed at ensuring vehicle safety, environmental impact, and engine efficiency.

- Additionally, transmission fluid manufacturers must comply with these regulations while also meeting the evolving needs of the market. Vehicle maintenance is another critical factor driving the demand for automotive transmission fluids. Regular maintenance is essential for prolonging the life of transmission systems and ensuring optimal performance. In the heavy-duty vehicle sector, transmission fluids play a vital role in ensuring the longevity and productivity of construction equipment and agricultural machinery. The use of advanced lubricant technology in these applications is helping to reduce downtime and improve efficiency. The automotive innovation landscape is continually evolving, with a focus on lifecycle management, smart mobility, and autonomous vehicle technology.

- In conclusion, transmission fluids will continue to play a crucial role in enabling these advancements and ensuring the long-term sustainability of the automotive industry. In conclusion, the market is poised for growth, driven by advancements in transmission technology, the expanding global automotive market, and the integration of advanced technologies such as electric vehicles and autonomous driving. Transmission fluid manufacturers must adapt to these changes by offering specialized solutions that meet the unique demands of various vehicle applications while also complying with industry regulations and environmental standards.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Automatic transmission fluid

- Dual clutch transmission fluid

- Continuously variable transmission fluid

- Others

- Vehicle Type

- Passenger cars

- Commercial vehicles

- Geography

- APAC

- China

- India

- Japan

- South Korea

- North America

- Canada

- US

- Europe

- Germany

- France

- Italy

- South America

- Brazil

- Middle East and Africa

- APAC

By Type Insights

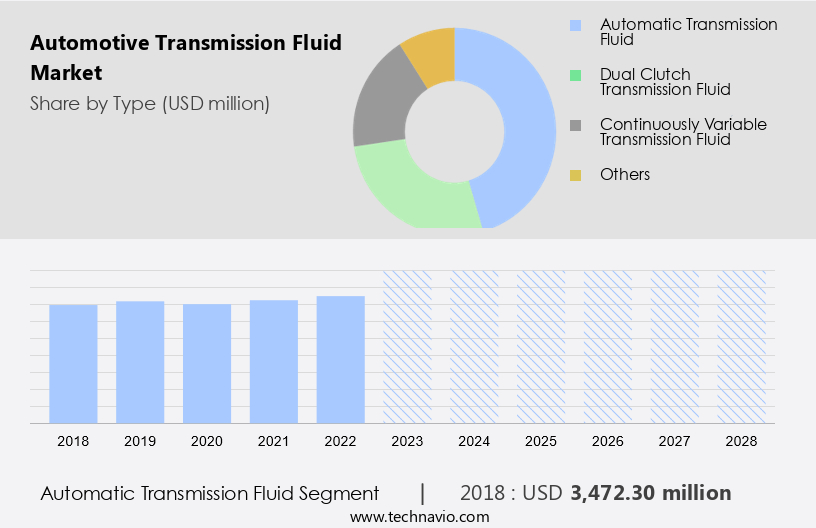

- The automatic transmission fluid segment is estimated to witness significant growth during the forecast period.

Automatic Transmission Fluid (ATF) plays a vital role in the United States market, enabling the smooth operation and protection of automatic transmissions in various transportation applications. Formulated to meet the unique demands of automatic transmissions, ATF offers several essential performance benefits. Heat resistance and thermal stability are crucial attributes of ATF, preventing the formation of deposits and sludge due to high-temperature operations. By maintaining cleanliness and preventing buildup, ATF ensures the transmission system's longevity and cost-efficiency. Moreover, collaborations between industry players and innovations in ATF formulations have led to the development of advanced transmission fluids for luxury vehicles and Internal Combustion Engines (ICE).

Furthermore, these advancements cater to the growing environmental concerns, as some ATF types offer reduced environmental impact. However, raw material price fluctuations and supply chain disruptions can impact the market's growth. Replacement of old transmission fluids with modern, more efficient alternatives is a significant trend in the aftermarket, driving demand for high-performance ATF. In conclusion, the United States market is witnessing significant growth, fueled by the need for cost-efficient, high-performance, and eco-friendly transmission fluids. By addressing the unique requirements of automatic transmissions, ATF plays a pivotal role in enhancing vehicle performance and ensuring a seamless driving experience.

Get a glance at the market report of share of various segments Request Free Sample

The automatic transmission fluid segment was valued at USD 3.47 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

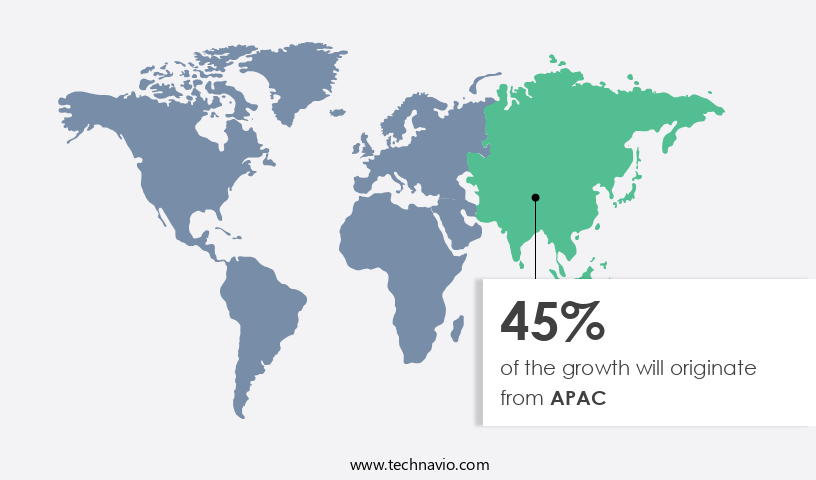

- APAC is estimated to contribute 45% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in the Asia Pacific region is witnessing substantial growth due to the expanding commercial vehicle sector and technological advancements in the transmission system. In India, for instance, the commercial vehicle industry experienced a notable increase in the second quarter of 2024, with over 234,000 trucks and buses sold, marking a 4.5% growth compared to the previous year. This growth is primarily driven by the strong replacement demand and ongoing infrastructure investments by the government, which are crucial for the transportation and logistics industries. The rise in commercial vehicle sales significantly influences the demand for premium transmission fluids.

Consequently, commercial vehicles, which are subjected to heavy loads and challenging operating conditions, necessitate dependable transmission fluids to ensure optimal performance and vehicle life. Earthmovers, agricultural utility vehicles, and other industrial applications also require high-quality transmission oil to maintain their efficiency and productivity. Technological advancements in the automotive segment, such as the growing adoption of electric vehicles (EVs), are also contributing to the market growth. These vehicles require specialized transmission fluids to ensure the smooth functioning of their complex transmission systems. As the automotive sector continues to evolve, the demand for advanced transmission fluids is expected to increase, offering significant opportunities for market participants.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Automotive Transmission Fluid Market?

Rising household income is the key driver of the market.

- The market is experiencing notable growth due to the increasing real household income in major economies. In the first quarter of 2024, household income per capita in OECD countries rose by 0.9%, a considerable improvement from the previous quarter's 0.3% increase. This trend is significant as it boosts consumer spending power, particularly in the automotive sector. All G7 economies reported a rise in real household income per capita during the pandemic period. Italy led the way with a substantial 3.4% increase, driven by higher employee compensation and social transfers, reversing the previous quarter's decline. Automotive transmission fluid plays a crucial role in maintaining the performance of engines and automatic transmissions by providing lubrication and preventing overheating.

- Furthermore, it also contains anti-wear agents that protect against hydraulic pressure loss and wear. As consumers invest in new vehicles, the demand for high-quality transmission fluids is increasing. Additionally, the growing popularity of hybrid vehicles and off-road vehicles is expanding the market's scope. Fuel economy is another factor driving the market's growth, as transmission fluids that improve fuel efficiency are in high demand. Manufacturers are developing advanced transmission fluids that cater to the unique requirements of different vehicle types, ensuring optimal performance and longevity. The supply chain for automotive transmission fluids is strong, with key players investing in research and development to meet the evolving needs of the market.

What are the market trends shaping the Automotive Transmission Fluid Market?

Product launches are the upcoming trend in the market.

- The market is experiencing notable growth due to the introduction of advanced transmission fluids. One such innovation is the recently launched Fluidsyn ATF/CVT by TotalEnergies Marketing Canada Inc. On November 11, 2024. This product is a game-changer in the fully synthetic transmission fluids category, engineered to optimize the functionality of both automatic transmission fluid (ATF) and continuously variable transmission (CVT) systems. Fluidsyn ATF/CVT is a high-performance fluid designed to meet the stringent demands of modern automotive transmissions. Its 100% synthetic formulation delivers superior performance and contributes to enhanced fuel efficiency, making it an ideal choice for consumers seeking to reduce their environmental footprint and save on fuel costs.

- Further, the automotive industry's focus on fuel efficiency and eco-friendliness is driving the demand for biodegradable transmission fluids. Moreover, product differentiation is a key strategy adopted by market players to cater to the diverse needs of consumers, including those in the tractor and specialized vehicle segments.

- Additionally, the increasing production of OEM vehicles and the growing popularity of electric power trains are expected to create new opportunities for the market. In conclusion, the market is poised for continued growth, driven by the launch of innovative products like Fluidsyn ATF/CVT and the evolving needs of consumers in the personal vehicle, tractor, and electric power train segments. Companies are investing in research and development to create specialized transmission fluids that cater to the unique requirements of various vehicle types and transmission systems. By focusing on product innovation and sustainability, market players can differentiate themselves and capture a larger market share.

What challenges does Automotive Transmission Fluid Market face during the growth?

Supply chain disruptions are key challenges affecting market growth.

- The market is currently experiencing disruptions in the supply chain due to geopolitical tensions and natural disasters. The ongoing conflict between Iran and Israel, which began in September 2024, has significantly affected crude oil prices. The Middle East, a crucial region for global oil production, has seen escalating tensions, leading investors to express concerns over potential supply interruptions. In October 2024, oil prices increased for the second consecutive week, with Brent crude oil futures decreasing slightly by 36 cents, or 0.4%, reflecting these concerns. Additionally, Hurricane Milton's impact on fuel demand in Florida, US, further exacerbated the situation. Extreme pressure agents, a critical component of transmission fluids for heavy-duty vehicles, are derived from crude oil.

- Consequently, any disruption in its supply can significantly impact the market. Logistics challenges and rising temperatures further complicate the situation, as transmission fluid's hydraulic system performance can degrade under extreme heat. Therefore, ensuring a reliable and efficient supply chain is crucial for the industry's growth.

Exclusive Customer Landscape

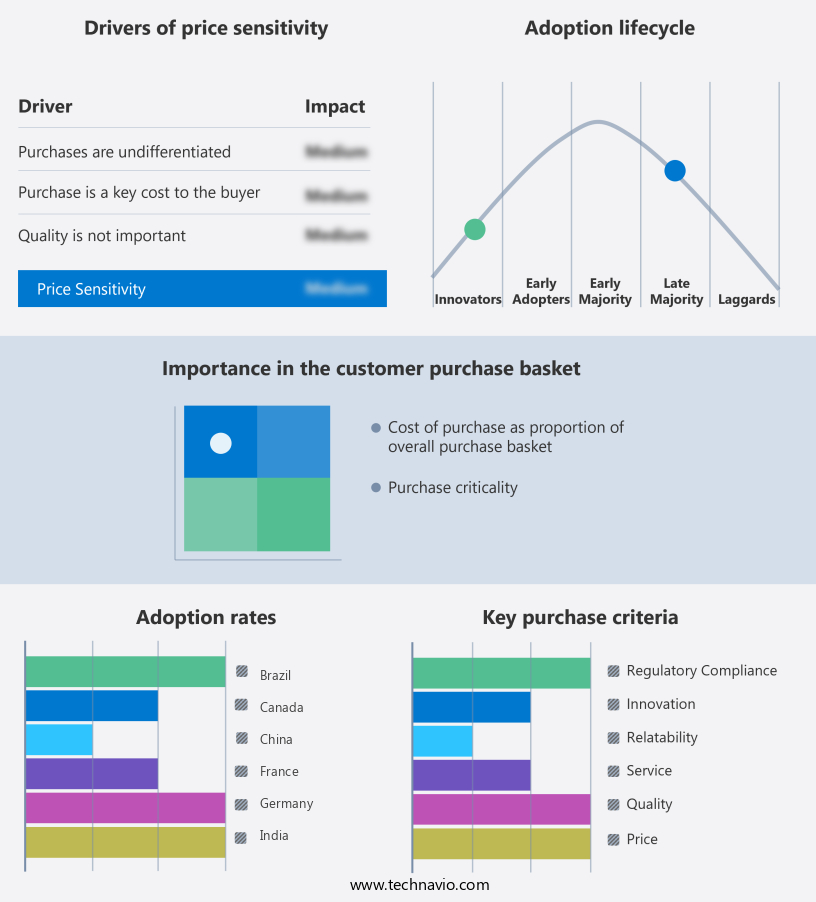

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMALIE OIL CO.

- BP Plc

- Castrol Ltd.

- Chevron Corp.

- Exxon Mobil Corp.

- FUCHS SE

- Gulf Oil International Ltd

- Idemitsu Kosan Co. Ltd.

- MOTUL SA

- Petro Canada Lubricants Inc

- PETRONAS Lubricants International

- Phillips 66

- PJSC LUKOIL

- Ravensberger Schmierstoffvertrieb GmbH

- Red Line Synthetic Oil

- Repsol SA

- Shell plc

- Sinopec Shanghai Petrochemical Co. Ltd.

- TotalEnergies SE

- Valvoline Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is a significant segment within the automotive sector, catering to the requirements of various vehicle types, including commercial vehicles and personal vehicles. Transmission fluid plays a crucial role in the transmission system, ensuring smooth operation by lubricating and cooling the components. It is essential for both manual and automatic transmissions, as well as in hydraulic systems, dual-clutch systems, and electric powertrains. Technological advancements have led to the development of specialized transmission fluids, such as those for high-performance sports cars, electric vehicles, and heavy-duty vehicles. These fluids offer enhanced performance, fuel economy, and temperature stability.

Moreover, they contain anti-wear agents, extreme pressure agents, and biodegradability features to extend transmission life and reduce environmental impact. The supply chain industry plays a vital role in the market, ensuring the timely delivery of raw materials and finished products to manufacturers, service centers, and end-users. However, factors like supply chain disruptions, raw material prices, and regulatory standards can impact the market's cost-efficiency and growth. Vehicle technologies, such as electrification and hybrid vehicles, are driving innovation in the transmission fluid market. For instance, automatic transmission fluids for electric vehicles require different properties than those for internal combustion engine vehicles. As vehicle connectivity and driver assistance systems enhance the driving experience, the market is witnessing increased demand for high-performance lubricants and fluid additives to optimize transmission fluid performance.

Additionally, the increasing focus on maintenance awareness and replacement of old transmission fluids is expected to boost market growth. In conclusion, the market is a dynamic and evolving industry that caters to the diverse needs of the automotive sector. It plays a crucial role in ensuring the longevity and performance of transmission systems, enabling seamless transportation and enhancing the driving experience for various vehicle types.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

215 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.3% |

|

Market growth 2024-2028 |

USD 1.58 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.2 |

|

Key countries |

US, China, Germany, Japan, India, Canada, France, South Korea, Italy, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -