Autonomous Yard Management Market Size 2026-2030

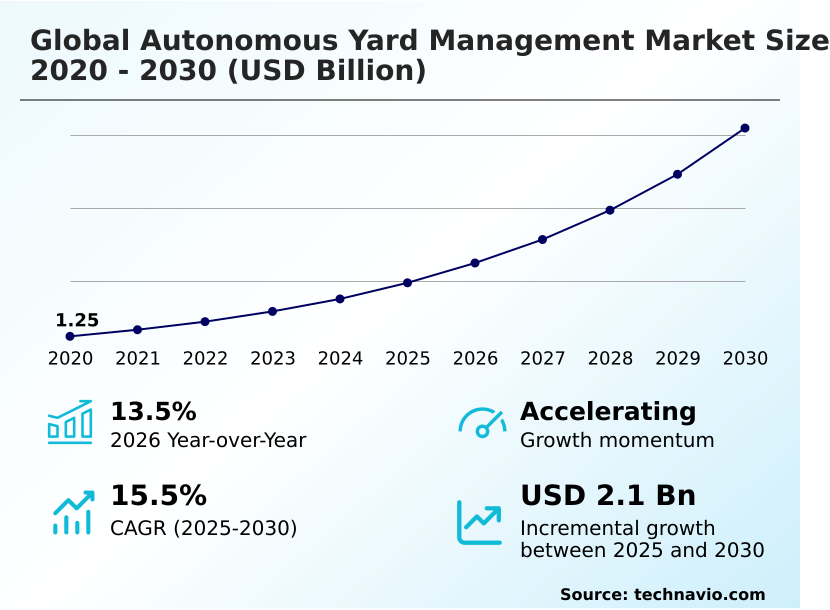

The autonomous yard management market size is valued to increase by USD 2.10 billion, at a CAGR of 15.5% from 2025 to 2030. Severe labor shortages and rising operational costs in logistics will drive the autonomous yard management market.

Major Market Trends & Insights

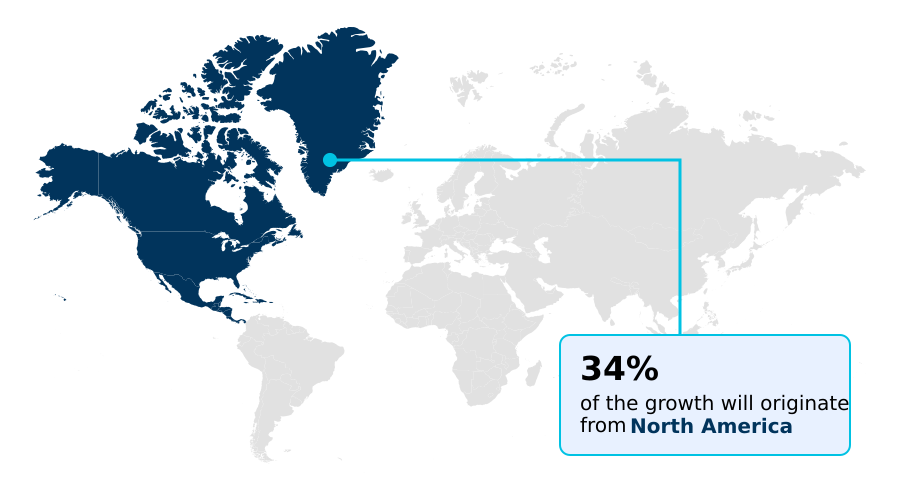

- North America dominated the market and accounted for a 33.7% growth during the forecast period.

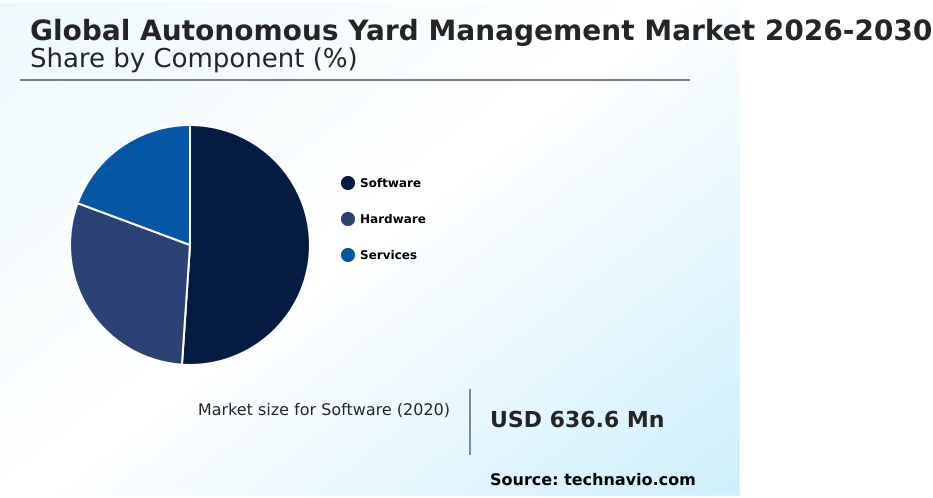

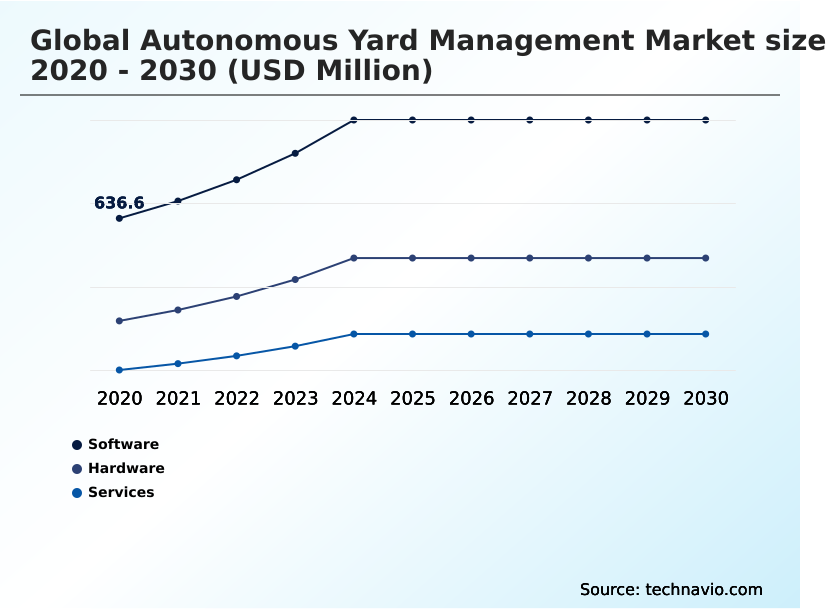

- By Component - Software segment was valued at USD 893.2 million in 2024

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.84 billion

- Market Future Opportunities: USD 2.10 billion

- CAGR from 2025 to 2030 : 15.5%

Market Summary

- The Autonomous Yard Management Market demonstrates an accelerated shift toward digitized and fully synchronized terminal operations. Enterprise distribution centers increasingly rely on self driving terminal tractors to combat severe skilled labor shortages and stabilize escalating overhead expenses. This transition from manual trailer spotting to automated workflows significantly improves supply chain transparency.

- Facilities implementing advanced sensor fusion and telemetry tracking report a 25% improvement in dock utilization rates compared to conventional manual operations. The primary driver of this market is the integration of machine learning algorithms, which enables real time spatial awareness and drastically reduces idle times across congested logistics hubs.

- Conversely, the market faces substantial challenges due to high initial capital integration costs. Deploying pervasive edge computing architecture and automated gate checkpoints requires massive upfront investments, which frequently deters small to medium-sized operators.

- However, as international ports and massive retail distribution networks demand faster cross docking velocity, the necessity for robust, automated route optimization supersedes initial financial barriers, forcing the industry to adapt rapidly to evolving operational frameworks.

What will be the Size of the Autonomous Yard Management Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Autonomous Yard Management Market Segmented?

The autonomous yard management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Hardware

- Services

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Application

- Logistics and distribution centers

- Ports and container terminals

- Manufacturing facilities

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Europe

- Germany

- UK

- France

- Italy

- The Netherlands

- Spain

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Turkey

- Israel

- South America

- Brazil

- Argentina

- Colombia

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software subsegment functions as the operational core of the Autonomous Yard Management market, dictating all automated movements within complex logistics hubs.

By utilizing predictive analytics, these digital twin technologies forecast potential bottlenecks and orchestrate automated guided vehicles without manual intervention. Facilities increasingly prioritize software as a service platform deployments because they enable rapid scalability and seamless legacy system integration.

This architectural transition directly reduces administrative overhead, allowing enterprises to optimize cross docking velocity. Implementing advanced computer vision within these software frameworks improves spatial awareness, resulting in a 15% reduction in trailer spotting errors.

Consequently, logistics providers experience highly synchronized operations, maximizing dock utilization rates while achieving idle time minimization across vast distribution networks.

The Software segment was valued at USD 893.2 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Autonomous Yard Management Market Demand is Rising in North America Get Free Sample

Regional disparities in the Autonomous Yard Management Market are primarily defined by varying technological infrastructure and localized labor dynamics.

North America exhibits a highly aggressive adoption curve, driven by massive e-commerce networks seeking supply chain transparency and automated route optimization to mitigate severe driver shortages.

In contrast, the market in Europe prioritizes regulatory compliance, focusing heavily on decarbonization mandates and localized particulate matter reduction.

European facilities integrating zero emission drivetrains and intelligent energy management systems experience a 30% reduction in environmental penalties compared to legacy operations.

Meanwhile, North American operators utilizing sophisticated computer vision and robotic trailer connections report a 25% increase in cross docking velocity.

Because North America possesses a more mature venture capital ecosystem supporting edge computing architecture, its implementation of multi site orchestration occurs 15% faster than in APAC regions, illustrating how localized strategic priorities dictate the pace of industrial automation framework integration.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The continuous maturation of the Autonomous Yard Management Market highlights a profound shift toward intelligent logistics infrastructure. Distribution centers face mounting pressure to accelerate throughput while controlling overhead costs, making traditional manual tracking highly inefficient. Integrating an automated dock scheduling process transforms these operations by establishing predictable, seamless inbound and outbound freight flows.

- Facility managers utilizing real time terminal tractor tracking report a 35% improvement in trailer retrieval speed compared to operations relying on radio communications. This enhanced supply chain visibility ensures that dock utilization remains optimal during peak shipping seasons. To further combat environmental concerns and fuel price volatility, operators are increasingly transitioning to electric self driving freight handlers.

- These specialized vehicles minimize operational downtime and align perfectly with corporate sustainability goals. Simultaneously, the deployment of cloud hosted yard operations software allows multi site enterprise shippers to manage complex geographic networks from centralized command centers, drastically reducing localized administrative burdens.

- By orchestrating robotic container moving solutions directly through these cloud platforms, maritime ports and inland hubs achieve highly synchronized asset transfers. This precise automation minimizes human error, decreases accident rates, and ensures strict adherence to occupational health guidelines.

- Ultimately, the intersection of advanced software architectures and automated physical hardware provides logistics providers with the necessary tools to navigate an increasingly volatile global trade environment, securing long-term operational resilience and superior financial performance.

What are the key market drivers leading to the rise in the adoption of Autonomous Yard Management Industry?

- Severe labor shortages combined with escalating operational costs in the logistics sector serve as the primary catalyst propelling rapid market expansion.

- Acute skilled labor shortages combined with the necessity for extreme supply chain transparency propel massive expansion within the Autonomous Yard Management Market.

- The chaotic nature of traditional logistics environments generates severe bottlenecks, forcing enterprises to adopt automated guided vehicles and self driving terminal tractors.

- Integrating high definition cameras and radar systems provides the machine intelligence perception necessary to operate heavy machinery safely without human intervention.

- This shift directly impacts operational efficiency, as facilities utilizing automated gate checkpoints experience a 40% reduction in vehicle check-in times. Furthermore, deploying precision collision avoidance systems decreases workplace accident rates by 35%, ensuring strict compliance with occupational health guidelines.

- Because businesses must process unprecedented freight volumes rapidly, the integration of these perception technologies guarantees continuous operations, lowering overall logistics overhead by 25%.

What are the market trends shaping the Autonomous Yard Management Industry?

- The integration of 5G infrastructure with edge computing networks represents a transformative trend fundamentally shaping the market landscape.

- The shift toward software as a service platform deployment marks a definitive trend redefining the Autonomous Yard Management Market. Logistics operators are abandoning rigid, capital-intensive architectures in favor of scalable cloud based orchestration. This transition occurs because cloud environments facilitate seamless multi site orchestration, allowing enterprise shippers to aggregate critical operational data across diverse geographic locations.

- By leveraging anonymized data aggregation, facility managers improve their automated route optimization, leading to a 20% increase in cross docking velocity compared to traditional localized servers. Furthermore, integrating digital twin technologies provides a virtual testing ground for terminal configurations, which reduces system deployment downtime by 30%. This agility empowers businesses to swiftly adapt to fluctuating supply chain demands.

- Ultimately, embracing subscription based deployment models removes substantial financial barriers, enabling a 25% faster integration of advanced telemetry tracking systems across expansive industrial distribution networks.

What challenges does the Autonomous Yard Management Industry face during its growth?

- Exorbitant initial capital expenditures and complex integration requirements pose substantial hurdles to widespread industry adoption.

- Severe regulatory ambiguity and prohibitive initial capital expenditures significantly constrain widespread adoption within the Autonomous Yard Management Market. Transitioning to an automated industrial automation framework requires a complete overhaul of existing infrastructure, including the installation of pervasive edge computing architecture and sophisticated light detection and ranging sensors.

- This massive financial barrier prevents mid-sized operators from modernizing, resulting in a 20% lower adoption rate compared to tier-one enterprise shippers. Furthermore, establishing flawless environmental perception in extreme weather conditions remains technologically difficult. When heavy rain or snow obstructs sensor fusion capabilities, system reliability degrades, leading to a 15% increase in operational downtime during adverse climates.

- Because occupational health compliance mandates require redundant safety mechanisms, organizations face exorbitant legacy system integration costs, delaying the implementation of highly efficient robotic trailer connections.

Exclusive Technavio Analysis on Customer Landscape

The autonomous yard management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the autonomous yard management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Autonomous Yard Management Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, autonomous yard management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Blue Yonder Group Inc. - The AI-powered software solution seamlessly integrates with existing facility infrastructure to accurately orchestrate and optimize self-driving dock operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Blue Yonder Group Inc.

- C3 Solutions

- Descartes Systems Group Inc.

- Easymile SAS

- FERNRIDE GmbH

- INFORM GmbH

- ISEE

- Kaleris

- Kalmar Corp.

- Manhattan Associates Inc.

- Oracle Corp.

- Orange EV

- Outrider

- project44

- SAP SE

- Trimble Inc.

- Venti Technology AI

- YardView

- Zebra Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Autonomous yard management market

- In the Air Freight and Logistics industry, the rapid deployment of private cellular networks across major transit hubs has enhanced ultra reliable low latency communication, directly impacting Autonomous Yard Management demand by enabling real time visibility for a 20% increase in cross docking velocity.

- Stringent decarbonization mandates from international environmental bodies have forced logistics providers to transition toward zero emission drivetrains, pulling demand for Autonomous Yard Management as terminal operators aim to lower localized particulate matter reduction by 30% through intelligent energy management systems.

- Widespread adoption of digital twin technologies for supply chain transparency has restructured legacy system integration frameworks, driving Autonomous Yard Management adoption by increasing dock utilization rates and supporting demurrage charge reduction by 25% at congested maritime ports.

- Severe occupational health compliance requirements regarding pedestrian proximity sensors have accelerated the shift toward automated guided vehicles, expanding the Autonomous Yard Management market as collision avoidance systems address blind spot elimination issues, reducing accident rates by 40% in high-traffic distribution centers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Autonomous Yard Management Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.5% |

| Market growth 2026-2030 | USD 2101.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.5% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, UAE, Saudi Arabia, South Africa, Turkey, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Autonomous Yard Management Market represents a critical evolution in industrial logistics, fundamentally redefining how distribution hubs orchestrate heavy freight movements. Supply chain leaders increasingly deploy self driving terminal tractors and automated guided vehicles to establish continuous, error-free operational workflows.

- This strategic transition heavily leverages sophisticated machine learning algorithms and sensor fusion to guarantee highly accurate environmental perception within dynamic, unpredictable lot spaces. Organizations implementing ultra reliable low latency communication networks achieve a 30% reduction in trailer processing time compared to manual operations. Such massive efficiency gains directly influence boardroom-level strategies regarding long-term budgeting and operational planning.

- The integration of light detection and ranging sensors alongside high definition cameras provides the spatial awareness necessary to safely navigate congested environments. Furthermore, relying on private cellular networks ensures that mission-critical data remains secure and immediately actionable. By leveraging edge computing architecture, facility executives eliminate communication delays, guaranteeing that collision avoidance systems function flawlessly.

- These precise technological integrations enable enterprises to maximize throughput, stabilize overhead costs, and maintain a competitive advantage in a demanding global economy.

What are the Key Data Covered in this Autonomous Yard Management Market Research and Growth Report?

-

What is the expected growth of the Autonomous Yard Management Market between 2026 and 2030?

-

USD 2.10 billion, at a CAGR of 15.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Hardware, and Services), Deployment (Cloud-based, On-premises, and Hybrid), Application (Logistics and distribution centers, Ports and container terminals, and Manufacturing facilities) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Severe labor shortages and rising operational costs in logistics, High initial capital expenditure and integration costs

-

-

Who are the major players in the Autonomous Yard Management Market?

-

Blue Yonder Group Inc., C3 Solutions, Descartes Systems Group Inc., Easymile SAS, FERNRIDE GmbH, INFORM GmbH, ISEE, Kaleris, Kalmar Corp., Manhattan Associates Inc., Oracle Corp., Orange EV, Outrider, project44, SAP SE, Trimble Inc., Venti Technology AI, YardView and Zebra Technologies Corp.

-

Market Research Insights

- The Autonomous Yard Management Market is rapidly evolving to address intense supply chain pressures through advanced technological integration. Implementing automated route optimization improves dock utilization rates by 22%, directly translating into substantial demurrage charge reduction for enterprise shippers. Furthermore, transitioning to subscription based deployment models provides necessary financial flexibility, lowering initial infrastructure costs by 35% compared to perpetual software licenses.

- This enhanced real time visibility enables facility managers to achieve a 20% increase in cross docking velocity, ensuring seamless inventory auditing without manual intervention. By prioritizing multi site orchestration, operators successfully align their complex logistics networks with rigorous operational efficiency benchmarks, fundamentally modernizing traditional freight handling capabilities.

We can help! Our analysts can customize this autonomous yard management market research report to meet your requirements.

RIA -

RIA -