Beer Market Size 2026-2030

The beer market size is valued to increase by USD 292.9 billion, at a CAGR of 5.9% from 2025 to 2030. Intensification of premiumization trend and craft segment maturation will drive the beer market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 36.8% growth during the forecast period.

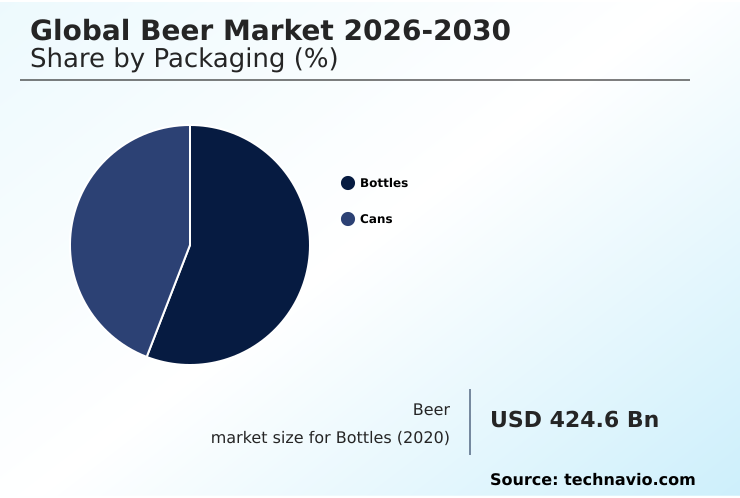

- By Packaging - Bottles segment was valued at USD 460.8 billion in 2024

- By Distribution Channel - On-trade segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 419.7 billion

- Market Future Opportunities: USD 292.9 billion

- CAGR from 2025 to 2030 : 5.9%

Market Summary

- The beer market is undergoing a significant transformation, driven by evolving consumer preferences and technological advancements. The premiumization trend continues to be a major force, with both macro breweries and an increasing number of craft breweries focusing on high-quality ingredients, including specialty malts and exotic hop varieties, to create premium lager and diverse ale styles.

- This shift toward quality over quantity is steering the brewing industry toward greater innovation. A parallel driver is the rising demand for healthier options, which has propelled the growth of low-abv beer and non-alcoholic beer. Advanced dealcoholization process technologies are critical, allowing producers to create flavorful alternatives that meet consumer wellness goals.

- For instance, a common business scenario involves optimizing the beer distribution network through supply chain verticalization and brewing process automation.

- By integrating predictive analytics, a company can better forecast demand, streamline cold-chain logistics, and reduce transport costs by over 15%, ensuring both operational resilience and profit margin optimization in a competitive landscape defined by both on-trade distribution and expanding e-commerce beverage sales.

What will be the Size of the Beer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Beer Market Segmented?

The beer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Packaging

- Bottles

- Cans

- Distribution channel

- On-trade

- Off-trade

- Product type

- Lager

- Ale

- Stouts

- Others

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Mexico

- Canada

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- Turkey

- UAE

- Rest of World (ROW)

- APAC

By Packaging Insights

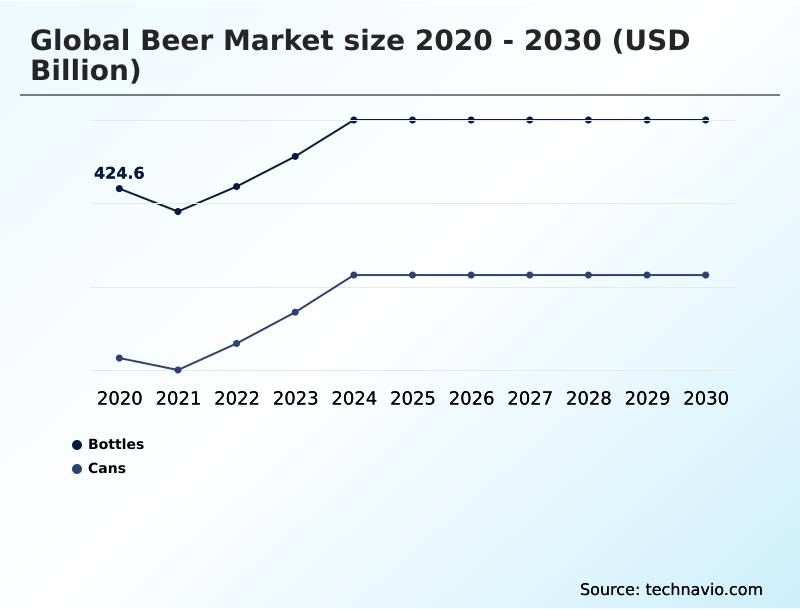

The bottles segment is estimated to witness significant growth during the forecast period.

The bottles segment is a cornerstone of the beer market, intrinsically linked to the premiumization trend and the heritage of artisanal brewing. Glass is preferred for its superior ability in organoleptic properties preservation, protecting premium lager from oxygen and moisture.

The segment is evolving through the adoption of lightweighting technologies and increased use of post-consumer recycled cullet, driven by circular economy initiatives.

These advancements enhance sustainability and can reduce shipping weights by over 10%, optimizing logistics without compromising the durable packaging solutions consumers associate with high-end products.

As brewers focus on differentiation, the tactile and branding potential of glass remains critical for market positioning, especially for heritage and craft offerings.

The Bottles segment was valued at USD 460.8 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 36.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Beer Market Demand is Rising in APAC Get Free Sample

The beer market's growth is predominantly led by the APAC region, which is set to contribute over 36% of the market's incremental growth, outpacing North America and Europe.

In this region, rising disposable incomes are fueling a shift from economy-tier products to premium offerings, driving value. Innovation is centered on local tastes, with a surge in flavored beer and unique styles that resonate with regional palates.

This contrasts with Europe, where traditional lager brewing and stylistic heritage remain central, though demand for wheat beer is also strong. Effective beer distribution is key, with a focus on off-trade retail optimization through e-commerce and modern retail formats.

Concurrently, a revitalized on-trade channel strategy is crucial for brand-building and capturing high-margin sales in urban centers across all major regions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Analyzing the future of the global beer market reveals complex dynamics. The impact of premiumization on beer market is profound, shifting value away from volume and forcing innovation. A key aspect is the growth of non-alcoholic beer category, driven by health and wellness trends in beer. This necessitates technological advancements in beer production, particularly in flavor preservation.

- Strategic decisions increasingly involve supply chain verticalization in brewing to counter rising ingredient costs and ensure stability, a more pressing concern for many firms than typical commodity price swings of 5-10%. The role of craft breweries in market evolution remains pivotal, as they often pioneer new styles and direct-to-consumer beer sales models.

- However, the regulatory impact on beer marketing, including restrictions on digital advertising, presents a significant hurdle. Understanding on-trade vs off-trade channel dynamics is crucial as consumer purchasing habits evolve. There is also rising beer market competition from substitutes like seltzers and spirits.

- The lager renaissance and market impact show a return to classic, high-quality styles, aligning with consumer preference for premium lagers. For new entrants, developing effective strategies for craft beer market entry requires navigating these trends, from AI applications in brewing industry to sustainability trends in beer packaging.

- Ultimately, success depends on addressing the challenges of shifting consumer demographics and understanding regional beer market growth drivers.

What are the key market drivers leading to the rise in the adoption of Beer Industry?

- The intensification of the premiumization trend, coupled with the maturation of the craft segment, serves as a key driver for market growth.

- The sustained consumer shift toward the premiumization trend is a primary market driver, fueled by craft segment maturation and a demand for unique flavor profiles from specialty malts and exotic hop varieties.

- This allows for higher margins, offsetting raw material cost fluctuations. Concurrently, the rapid expansion of non-alcoholic variants and low-abv beer, driven by health consciousness, is reshaping the industry.

- Advancements in the dealcoholization process preserve taste while meeting wellness demands, expanding the consumer base by over 15% in certain demographics. To enhance operational resilience, firms are pursuing strategic supply chain verticalization.

- For example, one major player’s reacquisition of a 49.9% stake in its container plants ensures cost efficiency and insulates operations from external market shocks, providing a foundation for sustainable growth.

What are the market trends shaping the Beer Industry?

- A strategic pivot toward premiumization and a renaissance in the lager category are defining the market's upcoming trajectory.

- The beer market is rebalancing around a lager renaissance, where consumers prioritize quality over novelty. This trend, a core part of beer premiumization, sees macro-breweries and craft breweries alike focusing on well-executed classic styles.

- Simultaneously, the brewing industry is seeing radical integration of agentic AI adoption, where predictive analytics optimize everything from recipe formulation in ale brewing to production schedules, improving forecast accuracy by over 18%. Packaging is also evolving, with aluminum cans gaining favor for their ability in photodegradation prevention.

- This is coupled with the rise of sophisticated direct-to-consumer logistics, enabling smaller producers to bypass traditional retail channels and reach a wider audience, which is a significant shift in the competitive landscape.

What challenges does the Beer Industry face during its growth?

- Shifting consumer demographics and the rise of temperance present a key challenge to industry growth.

- The beer market faces pressure from shifting consumer demographics, as younger cohorts consume less alcohol, challenging both macro breweries and microbreweries. This trend forces investment in non-alcoholic alternatives to avoid permanent volume loss. Profit margin optimization becomes difficult amid persistent supply chain fragility, with volatile aluminum and glass costs compressing earnings.

- A recent regional regulatory shift, for instance, created a shortfall of 130 million can units, highlighting the need for supply chain fragility mitigation. Furthermore, an intensifying regulatory environment, including the implementation of minimum unit pricing (MUP) and the threat of increased excise tax compliance burdens, restricts marketing and erodes the effectiveness of price-based promotions.

- These factors create high barriers to entry and diminish the viability of traditional marketing channels.

Exclusive Technavio Analysis on Customer Landscape

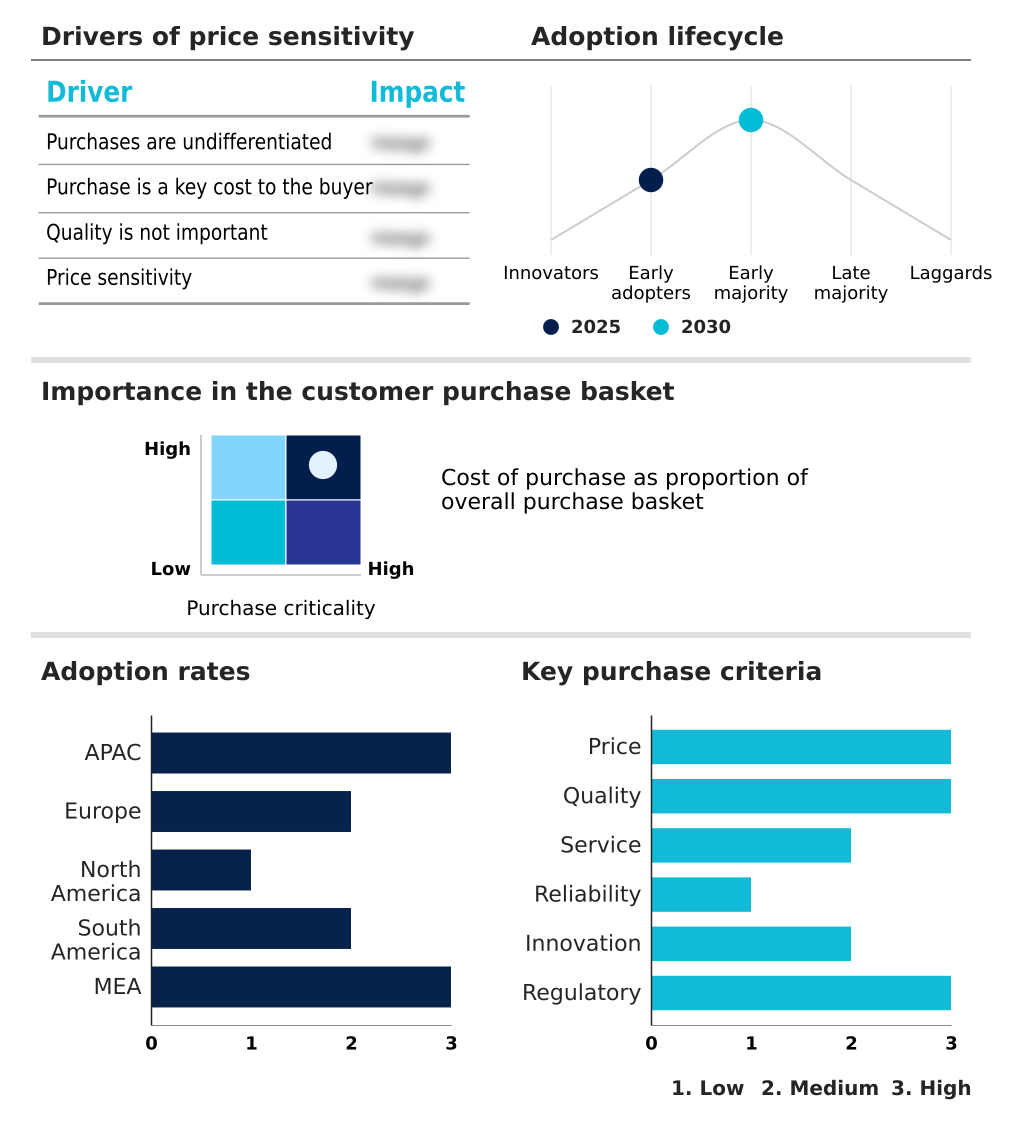

The beer market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the beer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Beer Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, beer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AleSmith Brewing Co. - This entity is recognized for its award-winning, handcrafted ales, which are distinguished by their bold flavor profiles and commitment to artisanal quality.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AleSmith Brewing Co.

- Anheuser Busch InBev SA NV

- Asahi Group Holdings Ltd.

- BrewDog Plc

- Carlsberg Breweries AS

- Cloudwater Brew Co.

- Diageo PLC

- Duvel Moortgat NV

- East 9th Brewing Co.

- Forbidden Root

- Heineken NV

- Kirin Holdings Co. Ltd.

- Mikkeller APS

- Mission Brewery

- Molson Coors Beverage Co.

- Saranac Brewery

- Sierra Nevada Brewing Co.

- Sprecher

- Swinkels Family Brewers

- The Boston Beer Co. Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Beer market

- In April 2025, The Bureau of Indian Standards implemented mandatory Quality Control Orders in India, creating a severe supply squeeze and a shortfall of approximately 130 million 500-milliliter cans during the peak summer consumption period.

- In April 2025, The Brewers Association reported that the total number of breweries in the United States increased to nine thousand nine hundred twenty-two, indicating a persistent trend toward market diversification.

- In March 2025, GE Aerospace announced a substantial $1 billion investment to modernize its manufacturing facilities, a development highlighting cross-industry advancements in high-precision manufacturing and material efficiency that influence the standards of the modern glass bottling industry.

- In January 2025, United Breweries Limited introduced two new Kingfisher flavored beers, Lemon Masala and Mango Berry Twist, in India to appeal to the evolving tastes of younger consumers and diversify its product portfolio.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Beer Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.9% |

| Market growth 2026-2030 | USD 292.9 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.7% |

| Key countries | China, India, Japan, Australia, South Korea, Indonesia, Germany, UK, France, Russia, Italy, Spain, US, Mexico, Canada, Brazil, Argentina, Colombia, South Africa, Turkey, Egypt, Nigeria and UAE |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The beer market's evolution is shaped by the consumer-driven premiumization trend and craft segment maturation. Boardroom decisions now hinge on excise tax compliance and navigating regulations like minimum unit pricing. The lager renaissance is met with agentic AI adoption, where digital brewing techniques and fermentation monitoring are standard.

- Predictive maintenance algorithms and computer vision for quality control are boosting efficiency, with defect detection now exceeding 99% accuracy. Supply chain fragility mitigation is driving supply chain verticalization and the use of digital tracking systems. Core processes like the dealcoholization technology and top-fermented process are refined for non-alcoholic variants and artisanal ales.

- Brewers focus on organoleptic properties preservation through technologies that enable photodegradation prevention. Sustainability is key, with circular economy initiatives, use of post-consumer recycled cullet, and carbon capture technologies. Lightweighting technologies and water-efficient brewing technologies aid cost efficiency in brewing. The focus is on operational resilience, profit margin optimization, and managing alcohol by volume while ensuring caloric content transparency.

- This is all enabled by direct-to-consumer logistics, advanced on-trade channel strategy, and off-trade retail optimization to deliver ready-to-drink formulation and other products.

What are the Key Data Covered in this Beer Market Research and Growth Report?

-

What is the expected growth of the Beer Market between 2026 and 2030?

-

USD 292.9 billion, at a CAGR of 5.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Packaging (Bottles, and Cans), Distribution Channel (On-trade, and Off-trade), Product Type (Lager, Ale, Stouts, and Others) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Intensification of premiumization trend and craft segment maturation, Shifting consumer demographics and rise of temperance

-

-

Who are the major players in the Beer Market?

-

AleSmith Brewing Co., Anheuser Busch InBev SA NV, Asahi Group Holdings Ltd., BrewDog Plc, Carlsberg Breweries AS, Cloudwater Brew Co., Diageo PLC, Duvel Moortgat NV, East 9th Brewing Co., Forbidden Root, Heineken NV, Kirin Holdings Co. Ltd., Mikkeller APS, Mission Brewery, Molson Coors Beverage Co., Saranac Brewery, Sierra Nevada Brewing Co., Sprecher, Swinkels Family Brewers and The Boston Beer Co. Inc.

-

Market Research Insights

- The global beer market is defined by key dynamics, from artisanal brewing and craft beer production to the dominance of macro breweries. The brewing industry is seeing a push for beer premiumization in premium lager, while also expanding into low-abv beer and non-alcoholic beer using an advanced dealcoholization process.

- Innovation in lager brewing, ale brewing, and stout brewing now includes specialty malts and exotic hop varieties. The beer market ecosystem includes microbreweries and craft breweries leveraging direct-to-consumer beer sales and e-commerce beverage sales, challenging traditional on-trade distribution and off-trade distribution models. Brewing process automation and fermentation cycle optimization improve efficiency, with some systems reducing process deviations by 25%.

- Strategic supply chain verticalization is being adopted for better control over beer distribution, while demand for flavored beer, wheat beer, and malt beverage grows, all requiring durable packaging solutions.

We can help! Our analysts can customize this beer market research report to meet your requirements.

RIA -

RIA -