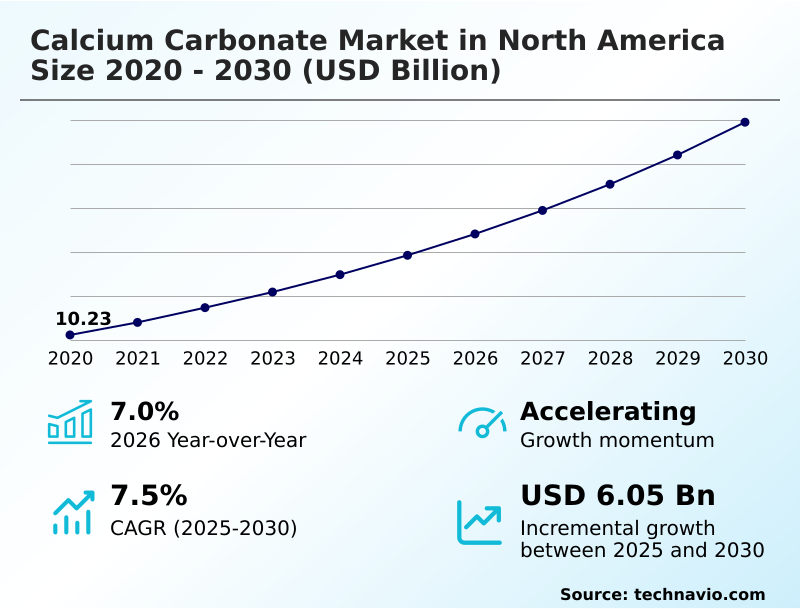

North America Calcium Carbonate Market Size 2026-2030

The north america calcium carbonate market size is valued to increase by USD 6.05 billion, at a CAGR of 7.5% from 2025 to 2030. Strategic integration of carbon capture and mineralization technologies will drive the north america calcium carbonate market.

Major Market Trends & Insights

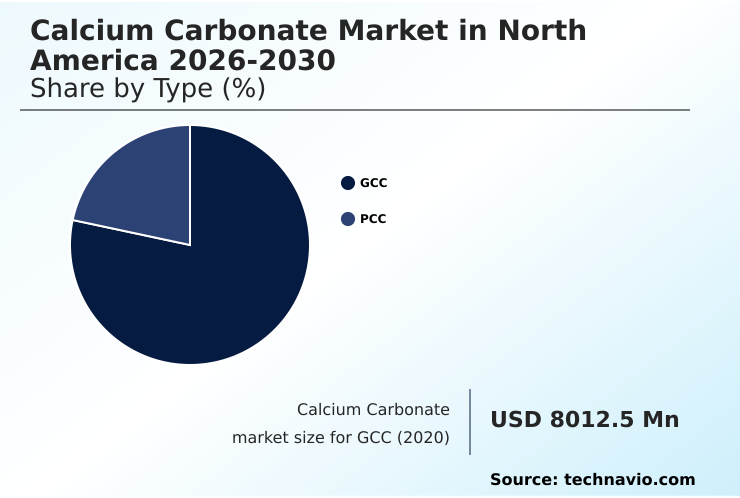

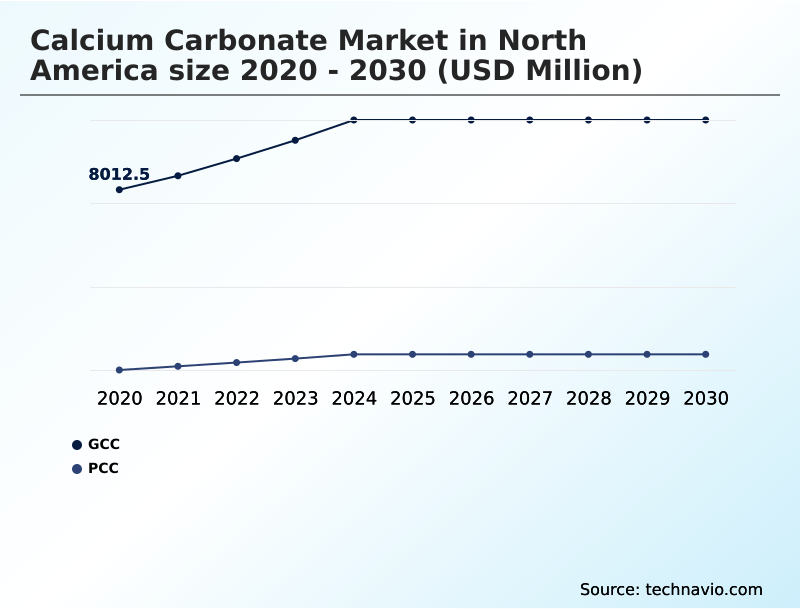

- By Type - GCC segment was valued at USD 10.25 billion in 2024

- By Application - Fillers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.67 billion

- Market Future Opportunities: USD 6.05 billion

- CAGR from 2025 to 2030 : 7.5%

Market Summary

- The calcium carbonate market in North America is characterized by a fundamental division between ground calcium carbonate (gcc), produced by mechanically processing limestone, and precipitated calcium carbonate (pcc), a synthetic product offering higher purity. As a critical functional filler, it enhances performance while reducing costs in sectors such as paper, plastics, and construction.

- A key dynamic is the push toward industrial decarbonization, which is reshaping production. For instance, a paper manufacturer might implement on-site satellite production of pcc, integrating it directly into its supply chain. This move not only reduces logistical costs and improves paper brightness but also provides a competitive advantage by aligning with corporate sustainability goals.

- While this shift requires significant capital investment, it addresses the dual pressures of market demand for high-performance materials and the growing imperative for environmentally responsible manufacturing. The market's evolution is thus defined by this balance between cost-effective bulk applications and the strategic adoption of advanced, sustainable production technologies.

What will be the Size of the North America Calcium Carbonate Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the North America Calcium Carbonate Market Segmented?

The north america calcium carbonate industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- GCC

- PCC

- Application

- Fillers

- Pigments

- Raw chemical materials

- pH balancing agents

- Dietary supplements

- End-user

- Construction

- Paper and pulp

- Plastics

- Paints and coatings

- Others

- Geography

- North America

- US

- Mexico

- Canada

- North America

By Type Insights

The gcc segment is estimated to witness significant growth during the forecast period.

The calcium carbonate market in North America is primarily segmented by product type, with ground calcium carbonate (GCC) representing the foundational category.

Produced via a mechanical grinding process, GCC is favored for its cost-effectiveness as a functional filler and for material extension in high-volume industries. Its application in flue gas desulfurization and as a soil amendment highlights its role in environmental compliance.

Demand is driven by the need for sustainable raw materials that support circular economy principles and resource efficiency.

As industries seek comprehensive mineral solutions, GCC's utility in water treatment applications and as a key component in pH adjustment systems continues to expand, solidifying its importance across construction, agriculture, and environmental sectors, where it improves material rigidity by up to 25%.

The GCC segment was valued at USD 10.25 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The application of precipitated calcium carbonate in paper production continues to evolve, with an emphasis on improving opacity in paper with mineral fillers. Simultaneously, the use of ground calcium carbonate for plastic composites is expanding, driven by the need for lightweighting automotive parts through advanced mineral fillers.

- A significant development is the focus on carbon neutral mineral fillers applications, stemming from innovations in using ccu for calcium carbonate synthesis. This sustainable sourcing of industrial minerals is reshaping the industry's approach to the calcium carbonate role in circular economy.

- In coatings, ultra-fine calcium carbonate in coatings enhances finish and durability, while surface-treated calcium carbonate for pvc improves processing and final product quality. The use of calcium carbonate for flue gas desulfurization and as a pH balancing agent in industrial minerals in water treatment processes highlights its environmental utility.

- The impact of mineralogy on gcc performance remains a key research area to optimize particle size for polymer reinforcement. High-purity pcc for pharmaceuticals and specialty mineral additives for food fortification demonstrate the material's versatility. In construction, limestone aggregates in construction materials and calcium carbonate in sealants and adhesives are foundational.

- Facilities adopting such integrated processes report operational uptimes more than 15% higher than those with traditional supply chains.

What are the key market drivers leading to the rise in the adoption of North America Calcium Carbonate Industry?

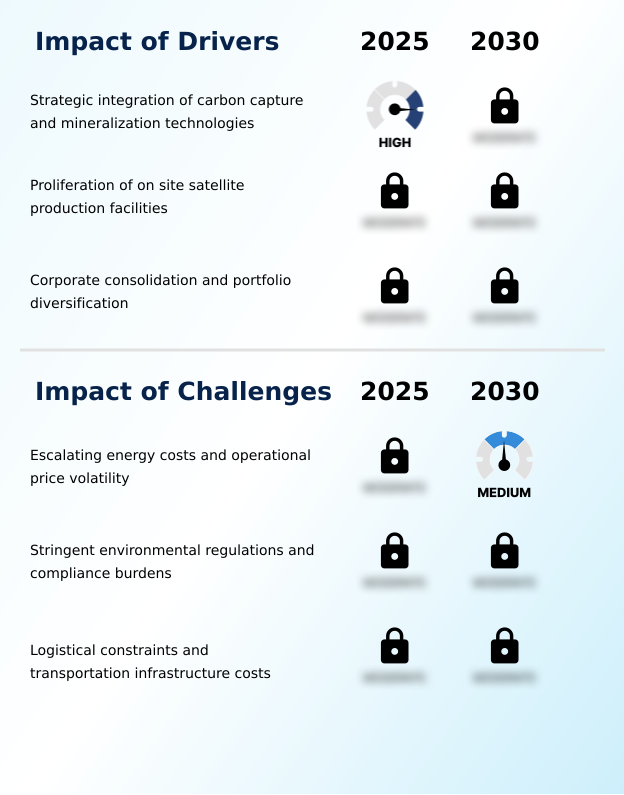

- The strategic integration of carbon capture and mineralization technologies stands as a key driver propelling market expansion.

- The adoption of green chemical manufacturing is a major driver, utilizing chemical carbonation of high-purity limestone to produce high-purity calcium carbonate.

- This creates carbon-neutral precipitated calcium carbonate, which serves as a high-performance industrial mineral and pigment extender, improving product weatherability and impact resistance.

- A significant push toward supply chain resilience is accelerating the adoption of a localized manufacturing approach, with on-site plants reducing mineral slurry transport costs by up to 90%. This strategy, coupled with investments in value-added processing, enhances regional capabilities.

- These integrated models not only lower operational expenses but also improve material consistency, with some facilities reporting a 10% reduction in production line defects.

What are the market trends shaping the North America Calcium Carbonate Industry?

- The strategic integration of carbon capture and mineralization technologies is emerging as a significant market trend. This shift is redefining production methods and sustainability standards within the industry.

- A primary trend is the shift toward mineral synthesis via carbon capture and utilization, creating carbon neutral minerals and advancing industrial decarbonization. This approach produces high-purity precipitated calcium carbonate, with innovations in particle engineering enhancing its performance and optical properties.

- The adoption of on-site satellite production, which improves operational agility and has been shown to reduce logistics-related emissions by 35%, reflects a move toward strategic resource management. This localization, coupled with advanced processing technologies, meets the rising demand for eco-friendly materials.

- As sustainable procurement becomes standard, these trends are reshaping supply chains, with digitally monitored systems increasing grade consistency by over 20%.

What challenges does the North America Calcium Carbonate Industry face during its growth?

- Escalating energy costs and operational price volatility present a key challenge affecting the industry's growth trajectory.

- A key challenge involves the high energy costs of the chemical precipitation process and mechanical grinding for producing materials used in polymer composites and for mechanical reinforcement. Volatile energy prices can cause production costs to fluctuate by 15-20%, pressuring margins. While specialized mineral reagents and nanotechnology offer technical differentiation, scaling these requires significant capital.

- The industry also faces the need to invest in low-emission technologies and emissions management to meet stricter regulations. Integrating carbon-negative fillers, excipients, and firming agents into products like joint compounds presents logistical hurdles, as transportation can add up to 30% to the final material cost, complicating supply chain economics.

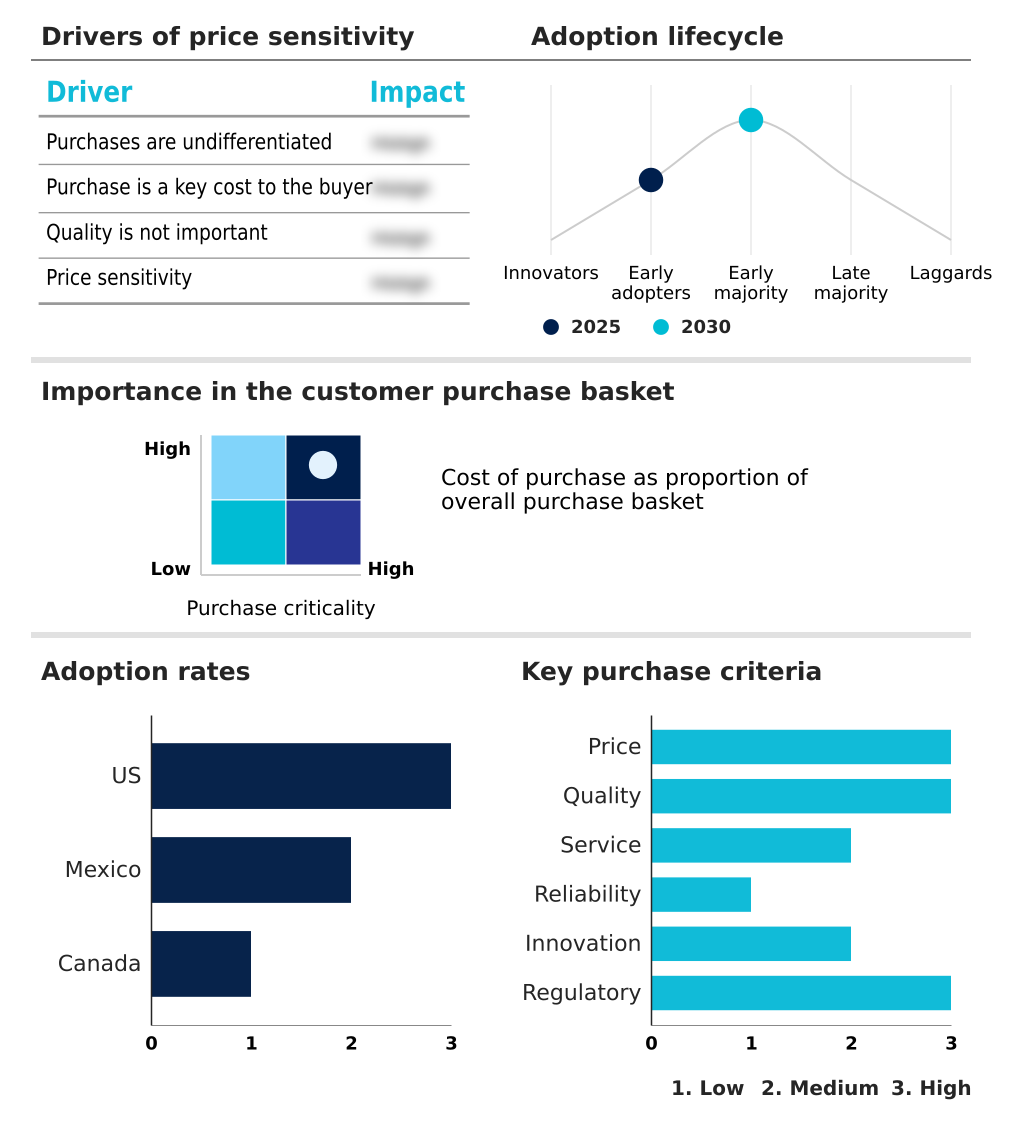

Exclusive Technavio Analysis on Customer Landscape

The north america calcium carbonate market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the north america calcium carbonate market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of North America Calcium Carbonate Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, north america calcium carbonate market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AGSCO Corp. - Offerings center on industrial minerals, primarily calcium carbonate-based fillers and pigments, engineered for diverse manufacturing and polymer applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGSCO Corp.

- Arkema Group

- Carmeuse SA

- Chemi Enterprises LLP

- Covia Holdings LLC

- GLC Minerals

- Graymont Ltd.

- Holcim Ltd.

- Imerys S.A.

- J M Huber Corp.

- Kishida Chemical Co. Ltd.

- Lhoist SA

- Mccarthy Bush Corp.

- Minerals Technologies Inc.

- Mississippi Lime Co.

- Omya International AG

- Pete Lien and Sons Inc.

- SCR Sibelco NV

- Solvay SA

- Tan Ky Mineral JSC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in North america calcium carbonate market

- In February 2025, Domtar, in a strategic collaboration with Omya AG, successfully established an on-site PCC plant at its Nekoosa mill in Wisconsin to ensure a reliable and cost-effective supply of essential raw materials.

- In February 2025, CarbonFree introduced EnduroCal, a zero-carbon precipitated calcium carbonate alternative designed to help manufacturers reduce Scope 3 emissions.

- In October 2024, Mississippi Lime Co. completed the acquisition of Burnett, Inc., a move that significantly expanded its mineral solutions platform and operational presence in the Southeast United States.

- In November 2024, CarbonFree initiated the commercial-scale operation of its SkyCycle technology at a major steel facility in Gary, Indiana, to mineralize flue gas emissions into carbon-neutral precipitated calcium carbonate.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled North America Calcium Carbonate Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 214 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.5% |

| Market growth 2026-2030 | USD 6046.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.0% |

| Key countries | US, Mexico and Canada |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The calcium carbonate market in North America is transitioning from a commodity-centric model to one emphasizing high-value, specialized materials. The proliferation of carbon capture and utilization is a critical factor, enabling the production of carbon-neutral minerals and advancing industrial decarbonization.

- This shift requires significant boardroom-level decisions regarding capital allocation: whether to invest in proprietary chemical precipitation process technology or acquire firms with existing capabilities in particle engineering and surface-treated grades. Innovations in mechanical grinding processes are yielding ultra-fine ground calcium carbonate with superior rheological properties, essential for advanced polymer composites.

- Producers are focusing on creating functional fillers and specialty mineral additives that offer enhanced mechanical reinforcement, thermal conductivity, and impact resistance. Investments in advanced grinding technology have yielded a 15% improvement in particle size consistency, enabling the development of sophisticated mineral solutions for applications ranging from pigment extenders to non-toxic excipients, demonstrating a clear move toward technical differentiation.

What are the Key Data Covered in this North America Calcium Carbonate Market Research and Growth Report?

-

What is the expected growth of the North America Calcium Carbonate Market between 2026 and 2030?

-

USD 6.05 billion, at a CAGR of 7.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (GCC, and PCC), Application (Fillers, Pigments, Raw chemical materials, pH balancing agents, and Dietary supplements), End-user (Construction, Paper and pulp, Plastics, Paints and coatings, and Others) and Geography (North America)

-

-

Which regions are analyzed in the report?

-

North America

-

-

What are the key growth drivers and market challenges?

-

Strategic integration of carbon capture and mineralization technologies, Escalating energy costs and operational price volatility

-

-

Who are the major players in the North America Calcium Carbonate Market?

-

AGSCO Corp., Arkema Group, Carmeuse SA, Chemi Enterprises LLP, Covia Holdings LLC, GLC Minerals, Graymont Ltd., Holcim Ltd., Imerys S.A., J M Huber Corp., Kishida Chemical Co. Ltd., Lhoist SA, Mccarthy Bush Corp., Minerals Technologies Inc., Mississippi Lime Co., Omya International AG, Pete Lien and Sons Inc., SCR Sibelco NV, Solvay SA and Tan Ky Mineral JSC

-

Market Research Insights

- Market dynamics are increasingly influenced by a strategic pivot toward supply chain optimization and decarbonization. The proliferation of on-site satellite production models, which can reduce material waste by over 10%, exemplifies a wider push for operational agility and supply chain resilience.

- This shift aligns with corporate consolidation trends, where acquisitions have enabled top players to increase regional service coverage by an average of 5%. Furthermore, investments in green chemical manufacturing and advanced processing technologies underscore a commitment to enhancing environmental credentials.

- These efforts are not just about compliance but are central to creating value-added processing capabilities that meet the demand for eco-friendly materials and support industrial reshoring initiatives.

We can help! Our analysts can customize this north america calcium carbonate market research report to meet your requirements.

RIA -

RIA -