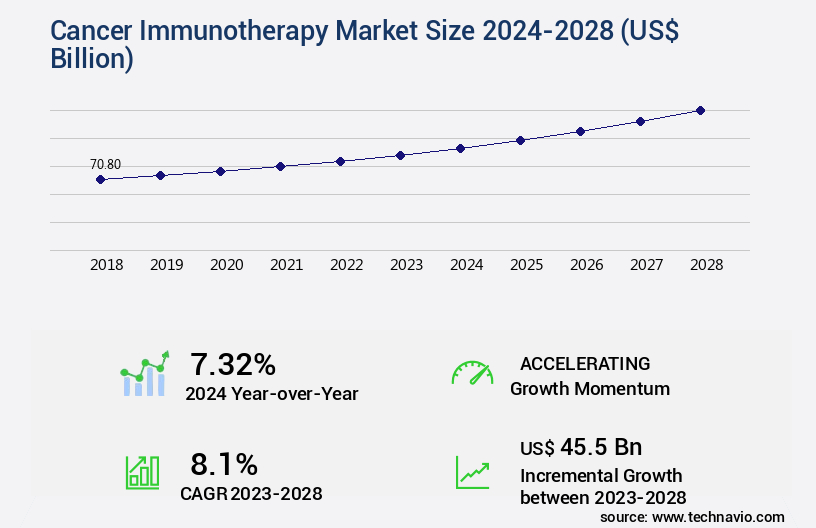

Cancer Immunotherapy Market Size 2024-2028

The cancer immunotherapy market size is valued to increase USD 45.5 billion, at a CAGR of 8.1% from 2023 to 2028. High prevalence of cancer will drive the cancer immunotherapy market.

Major Market Trends & Insights

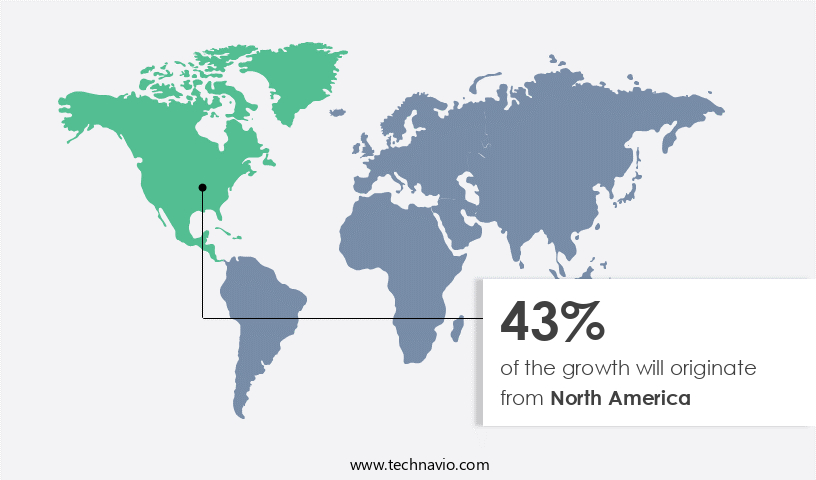

- North America dominated the market and accounted for a 43% growth during the forecast period.

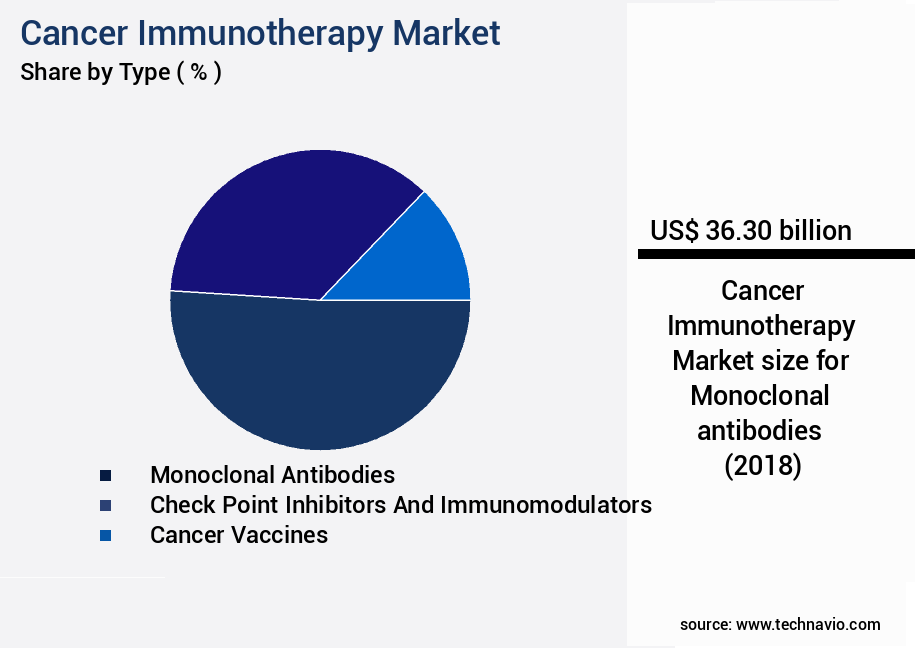

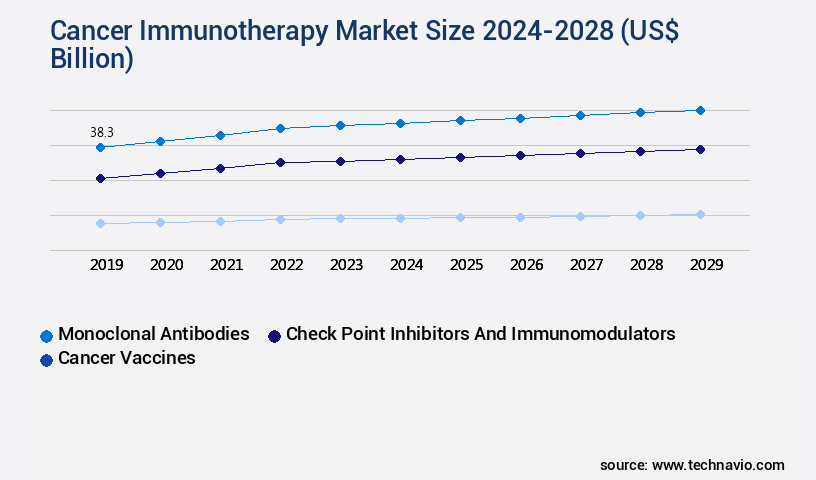

- By Type - Monoclonal antibodies segment was valued at USD 36.30 billion in 2022

- By Application - Lung cancer segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 99.29 billion

- Market Future Opportunities: USD 45.50 billion

- CAGR from 2023 to 2028 : 8.1%

Market Summary

- The market represents a significant and rapidly evolving sector in the healthcare industry. This market is characterized by the adoption of advanced core technologies, including immune checkpoint inhibitors, CAR-T cell therapy, and monoclonal antibodies, which are transforming cancer treatment. Applications span various types of cancer, with a high prevalence in lung, breast, and skin cancers. Service types or product categories include biopharmaceutical companies, research institutions, and hospitals. Regulations play a crucial role, with stringent policies ensuring safety and efficacy. For instance, the US Food and Drug Administration (FDA) has approved over 20 immunotherapies since 2011.

- Despite challenges, such as high costs and limited accessibility, opportunities abound, including the development of combination therapies and personalized medicine. According to a recent study, the global immunotherapy market is expected to reach a 30% market share in the oncology therapeutics market by 2027.

What will be the Size of the Cancer Immunotherapy Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cancer Immunotherapy Market Segmented ?

The cancer immunotherapy industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Monoclonal antibodies

- Check point inhibitors and immunomodulators

- Cancer vaccines

- Application

- Lung cancer

- Breast cancer

- Colorectal cancer

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- APAC

- China

- Rest of World (ROW)

- North America

By Type Insights

The monoclonal antibodies segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, driven by advancements in immune cell engineering and tumor microenvironment understanding. Personalized immunotherapies, such as adoptive cell transfer and cancer cell destruction, are revolutionizing treatment. Patient response prediction relies on immunomodulatory antibodies, immunogenicity assays, and treatment response biomarkers. Progression-free survival rates have improved with oncolytic viruses, t cell activation, and cytokine therapy. Monoclonal antibodies, targeting the major histocompatibility complex, are integral to immune system stimulation, with clinical trial outcomes showing promising overall survival rates. Novel approaches include antibody-drug conjugates, cancer vaccines, and combination therapies using chimeric antigen receptors, checkpoint blockade, neoantigen targeting, and dendritic cell vaccines.

Bispecific antibodies and tumor-associated antigens are also under investigation. Adverse event profiles are closely monitored to ensure safe and effective treatments. The market's continuous growth is a testament to the ongoing research and development in this field.

The Monoclonal antibodies segment was valued at USD 36.30 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cancer Immunotherapy Market Demand is Rising in North America Request Free Sample

North America's the market holds the largest global share, primarily due to substantial investments in the oncology sector in the US. The US dominates this regional market, contributing significantly to its revenue generation. The pharmaceutical industry's considerable investments, particularly in the oncology sector, and the presence of leading pharmaceutical companies in the region underpin the US's market dominance. In the US, cancer remains one of the most prevalent chronic diseases, with approximately 436 new cases reported per 100,000 population and about 156 deaths in the same year.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing robust growth, driven by the efficacy of checkpoint inhibitors in treating various types of cancer, particularly melanoma. Checkpoint inhibitors have revolutionized cancer treatment by enabling the immune system to recognize and attack cancer cells more effectively. However, challenges persist, such as car T-cell persistence and relapse, which necessitate continuous research and development. One promising area of research is oncolytic viruses, which selectively target cancer cells while maintaining safety. Dendritic cell vaccines are another approach, with manufacturing processes undergoing refinement to improve efficacy. Bispecific antibodies are being designed and developed to enhance immune response by binding to both cancer cells and T cells.

Engineering challenges in chimeric antigen receptors (CAR-T) are being addressed to improve their efficacy in cancer treatment. Immune response biomarkers play a crucial role in evaluating treatment progress, with research focusing on programmed cell death pathways in cancer and t cell exhaustion rejuvenation strategies. Antibody drug conjugates (ADCs) offer targeted cancer treatment, but their toxicity mechanisms need further investigation. Radioimmunotherapy dosimetry and targeting techniques are being refined to improve precision and reduce side effects. The impact of major histocompatibility complex polymorphism on immunotherapy response is an area of ongoing research. Tumor associated antigen identification methods and immune system stimulation approaches are being explored to enhance cancer cell destruction mechanisms in vitro.

Immune cell engineering using CRISPR technology holds great promise for personalized immunotherapy treatment selection. Neoantigen prediction algorithms and applications are revolutionizing cancer treatment, enabling more effective targeting of individual tumors. Clinical trial endpoints for evaluating immunotherapy are under constant review to ensure accurate measurement of treatment efficacy. Adoption rates of these advanced immunotherapies are significantly higher in developed regions compared to developing countries, highlighting the need for increased investment in research and development in emerging markets.

What are the key market drivers leading to the rise in the adoption of Cancer Immunotherapy Industry?

- The high prevalence of cancer significantly drives the market demand for diagnostic tools and treatment options.

- Cancer is a significant global health concern, with various risk factors contributing to its prevalence. These include unhealthy lifestyle choices, such as poor nutrition, physical inactivity, tobacco use, and excessive alcohol consumption. Exposure to ionizing radiations, chemical mutagens, infectious micro-organisms, and environmental pollutants are additional risk factors. The World Health Organization (WHO) reported an estimated 20 million new cancer cases and 9.7 million deaths in 2022.

- Lung cancer was the most common cancer, with approximately 12.4% of all new cases (2.5 million), followed by colon cancer with 9.6% (1.9 million) of new cases. The ongoing rise in cancer incidence underscores the need for continuous research and prevention efforts across various sectors.

What are the market trends shaping the Cancer Immunotherapy Industry?

- The adoption of diverse strategies is mandated for the growth of the market. This trend is upcoming and significant in the healthcare industry.

- In the dynamic and evolving the market, companies employ diverse strategies to expand their presence and drive innovation. Acquiring or licensing drug candidates and technologies from smaller biotech firms and academic institutions broadens a company's pipeline and fortifies its competitive edge. Mergers and acquisitions facilitate access to complementary capabilities, expertise, and intellectual property, fostering innovation and market expansion. Continuous optimization of existing products through lifecycle management strategies, such as new formulations, expanded indications, and combination therapies, extends product life cycles and sustains revenue growth.

- Furthermore, companies invest in capital and seek government support to develop and introduce advanced or upgraded devices. These strategies enable market participants to innovate, capture larger market shares, and ultimately enhance patient outcomes in The market.

What challenges does the Cancer Immunotherapy Industry face during its growth?

- The strict regulatory policies posing significant challenges are a key factor impeding industry growth.

- The market faces regulatory hurdles due to stringent regulations imposed by international regulatory bodies. In the US, the Food and Drug Administration (FDA) imposes restrictions on the marketing approval and manufacturing of biosimilars. The Biologics Price Competition and Innovation Act (BPCI Act) of 2009 established a licensure pathway for biological products that are proven to be biosimilar to an FDA-approved biological product. companies must submit comprehensive data to the FDA reviewer to obtain approval, including results from animal model studies, pharmacokinetic and pharmacodynamic properties, and safety profiles from human clinical trials.

- These requirements ensure the efficacy and safety of biosimilars in the market. Despite these challenges, the market continues to evolve, with ongoing research and development efforts in various sectors, such as adoptive cell therapy, monoclonal antibodies, and immune checkpoint inhibitors.

Exclusive Technavio Analysis on Customer Landscape

The cancer immunotherapy market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cancer immunotherapy market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cancer Immunotherapy Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cancer immunotherapy market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amgen Inc. - The company specializes in innovative cancer immunotherapy treatments, including Oncolytic Immunotherapy. Notable solutions include Amgen Oncology's offerings. These advanced therapies harness the power of the immune system to target and destroy cancer cells, contributing significantly to the ongoing fight against this disease.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amgen Inc.

- Amneal Pharmaceuticals Inc.

- AstraZeneca Plc

- Bayer AG

- Bristol Myers Squibb Co.

- Dendreon Pharmaceuticals LLC

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- Fresenius SE and Co. KGaA

- Gilead Sciences Inc.

- GlaxoSmithKline Plc

- Immunocore Holdings Plc

- Inovio Pharmaceuticals Inc.

- Johnson and Johnson Services Inc.

- Merck KGaA

- Novartis AG

- Pfizer Inc.

- Sanofi SA

- Seagen Inc.

- Takeda Pharmaceutical Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cancer Immunotherapy Market

- In January 2024, Merck KGaA and INSIGHT Therapeutics announced a strategic collaboration to develop and commercialize ADAPTIR, a novel T-cell engager for the treatment of solid tumors. This partnership combines Merck KGaA's expertise in oncology with INSIGHT Therapeutics' proprietary T-cell engager technology (Merck KGaA press release, 2024).

- In March 2024, Bristol Myers Squibb received FDA approval for Opdivo (nivolumab) in combination with Yervoy (ipilimumab) for the first-line treatment of advanced renal cell carcinoma. This approval expanded the indications for these immunotherapies, further solidifying their position in the market (FDA press release, 2024).

- In May 2024, Moderna Therapeutics announced the closing of a USD1.8 billion Series H financing round. The funds will be used to support the development and commercialization of its pipeline, including mRNA-based cancer immunotherapies (Moderna Therapeutics press release, 2024).

- In April 2025, AstraZeneca and Merck & Co. Entered into a global strategic collaboration to co-develop and co-commercialize potential new medicines from AstraZeneca's small molecule oncology portfolio. This partnership includes a focus on immunotherapies, further strengthening the commitment of these companies to the market (AstraZeneca press release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cancer Immunotherapy Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.1% |

|

Market growth 2024-2028 |

USD 45.5 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.32 |

|

Key countries |

US, Germany, China, France, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and evolving landscape of cancer treatment, immune cell engineering continues to reshape the tumor microenvironment. This innovative approach harnesses the power of the immune system to recognize and destroy cancer cells, leading to significant advancements in personalized immunotherapy. Adoptive cell transfer, a key component of immune cell engineering, enables the transfer of immune cells from a patient to enhance their ability to attack cancer cells. Tumor microenvironments are complex and intricate, necessitating the development of immunomodulatory antibodies to optimize patient response prediction. Immunogenicity assays play a crucial role in assessing the potential of cancer immunotherapies, ensuring effective immune system stimulation.

- Progression-free survival and overall survival rates have shown marked improvements with the use of oncolytic viruses, which selectively target and destroy cancer cells. T cell activation, cytokine therapy, and immune response modulation are other essential elements of immune cell engineering, each contributing to the complex interplay between the immune system and cancer cells. Major histocompatibility complex and treatment response biomarkers are essential tools in understanding the intricacies of these interactions. Immunotherapy continues to evolve, with the emergence of combination therapies, such as bispecific antibodies, antibody-drug conjugates, and chimeric antigen receptors. Checkpoint blockade, programmed cell death, and neoantigen targeting are among the latest innovations in cancer immunotherapy, offering promising avenues for future research.

- Dendritic cell vaccines and tumor-associated antigens are also gaining attention, as they hold the potential to stimulate a more robust immune response against cancer cells. Clinical trial outcomes continue to demonstrate the efficacy of these approaches, further fueling the ongoing exploration of immune cell engineering in cancer treatment. Despite the advancements, adverse event profiles remain an area of concern, necessitating continuous research and development to minimize risks and optimize patient safety. The future of cancer immunotherapy lies in the ongoing collaboration between scientific innovation and clinical application, with the ultimate goal of improving patient outcomes and ultimately, saving lives.

What are the Key Data Covered in this Cancer Immunotherapy Market Research and Growth Report?

-

What is the expected growth of the Cancer Immunotherapy Market between 2024 and 2028?

-

USD 45.5 billion, at a CAGR of 8.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Monoclonal antibodies, Check point inhibitors and immunomodulators, and Cancer vaccines), Application (Lung cancer, Breast cancer, Colorectal cancer, and Others), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

High prevalence of cancer, Presence of stringent regulatory policies

-

-

Who are the major players in the Cancer Immunotherapy Market?

-

Amgen Inc., Amneal Pharmaceuticals Inc., AstraZeneca Plc, Bayer AG, Bristol Myers Squibb Co., Dendreon Pharmaceuticals LLC, Eli Lilly and Co., F. Hoffmann La Roche Ltd., Fresenius SE and Co. KGaA, Gilead Sciences Inc., GlaxoSmithKline Plc, Immunocore Holdings Plc, Inovio Pharmaceuticals Inc., Johnson and Johnson Services Inc., Merck KGaA, Novartis AG, Pfizer Inc., Sanofi SA, Seagen Inc., and Takeda Pharmaceutical Co. Ltd.

-

Market Research Insights

- The market continues to evolve, driven by advancements in various areas such as toxicity monitoring, gene editing, and drug delivery systems. According to recent estimates, the global market for CTLA-4 inhibitors and PD-1 inhibitors is projected to reach USD150 billion by 2026, growing at a compound annual growth rate of 12%. This significant expansion can be attributed to the increasing adoption of combination regimens, which leverage the synergistic effects of multiple immunotherapies. For instance, lymphocyte infiltration and effector T cell activation have been shown to enhance the efficacy of PD-1 inhibitors. However, challenges remain, including regulatory T cell suppression, immune evasion mechanisms, and tumor heterogeneity.

- To address these, researchers are exploring innovative approaches such as apoptosis induction through cytokine signaling and viral vectors, as well as NK cell therapy and targeted therapy based on molecular profiling. Clinical trial design continues to evolve, with a focus on improving quality of life and addressing drug resistance through genetic alterations. Despite these advancements, the complex nature of cancer and the need for personalized treatment approaches underscore the ongoing need for research and innovation in the market.

We can help! Our analysts can customize this cancer immunotherapy market research report to meet your requirements.

RIA -

RIA -