Antibody Drug Conjugates Market Size 2026-2030

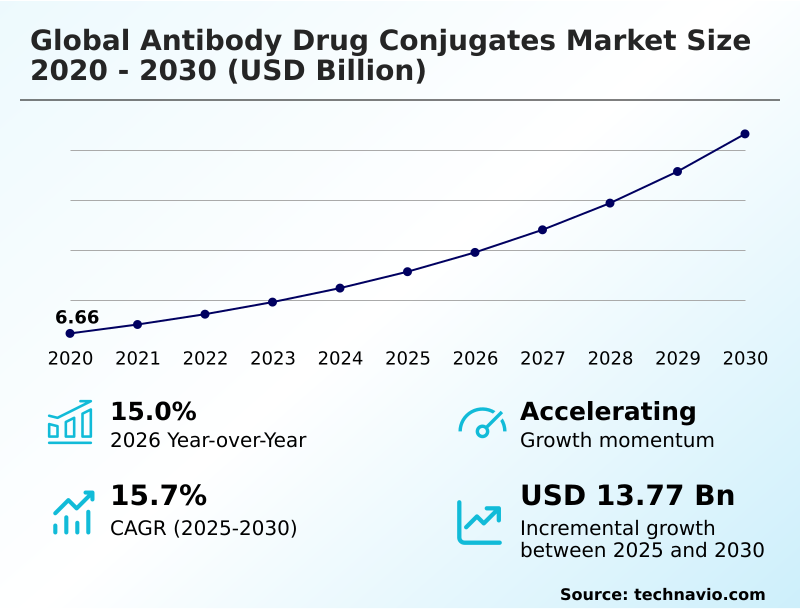

The antibody drug conjugates market size is valued to increase by USD 13.77 billion, at a CAGR of 15.7% from 2025 to 2030. Rising global incidence of cancer and paradigm shift toward precision oncology will drive the antibody drug conjugates market.

Major Market Trends & Insights

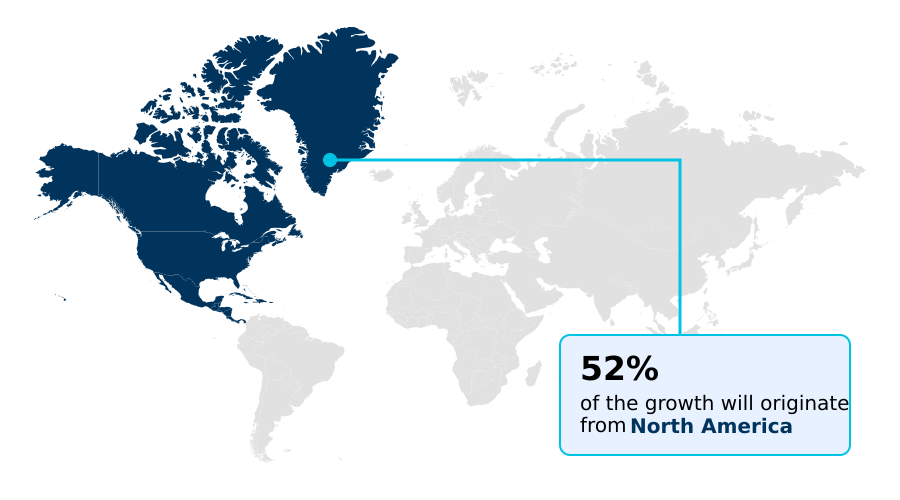

- North America dominated the market and accounted for a 52% growth during the forecast period.

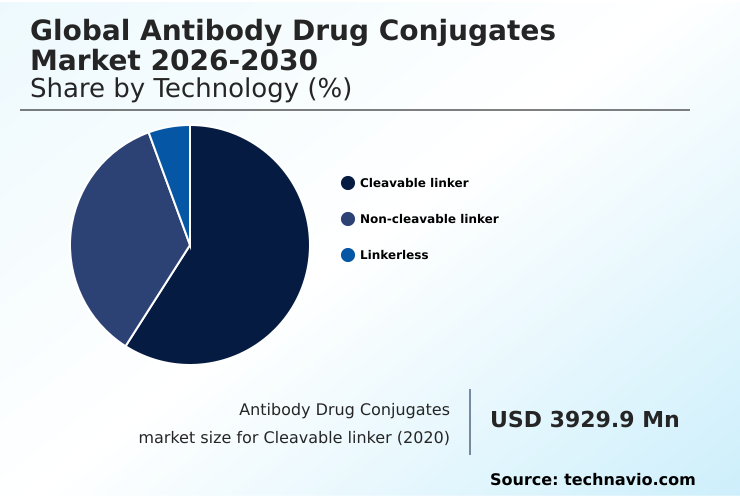

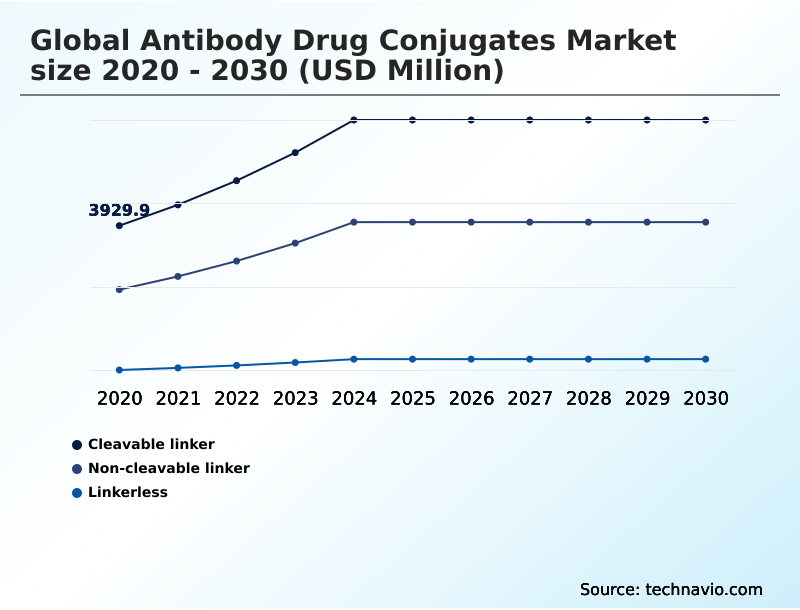

- By Technology - Cleavable linker segment was valued at USD 6.54 billion in 2024

- By Application - Breast cancer segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 19.95 billion

- Market Future Opportunities: USD 13.77 billion

- CAGR from 2025 to 2030 : 15.7%

Market Summary

- The antibody drug conjugates market is undergoing a significant transformation, driven by the pressing need for more effective and less toxic cancer treatments. This class of therapeutics represents a cornerstone of precision oncology, leveraging highly specific monoclonal antibodies to deliver potent cytotoxic payloads directly to tumor cells, thereby maximizing efficacy while minimizing collateral damage to healthy tissue.

- A key trend propelling the market is the expansion beyond traditional targets to a diverse array of novel antigens, enabling treatment for previously intractable cancers. For instance, a mid-sized biotechnology firm might leverage a contract development and manufacturing organization (CDMO) to navigate the complexities of cGMP manufacturing.

- This strategic outsourcing allows the firm to access specialized high-containment facilities required for handling high-potency APIs without incurring prohibitive capital expenditure. However, this reliance on external partners also highlights a central market challenge: a fragmented and constrained supply chain, which can introduce logistical risks and extend development timelines.

- As technology matures, the focus is shifting toward innovative linker-payload chemistries and combination therapies to overcome drug resistance and further improve patient outcomes.

What will be the Size of the Antibody Drug Conjugates Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Antibody Drug Conjugates Market Segmented?

The antibody drug conjugates industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Technology

- Cleavable linker

- Non-cleavable linker

- Linkerless

- Application

- Breast cancer

- Blood cancer

- Others

- Product type

- Trastuzumab emtansine

- Brentuximab vedotin

- Inotuzumab ozogamicin

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Technology Insights

The cleavable linker segment is estimated to witness significant growth during the forecast period.

The cleavable linker segment remains the cornerstone of the market, accounting for approximately 58% of therapeutic constructs. This dominance is due to a superior payload release mechanism engineered to exploit the unique tumor microenvironment.

Advanced linker chemistry enables the bystander effect, a critical feature for effective solid tumor treatment, especially in heterogeneous or refractory cancers.

The design allows the cytotoxic payload to diffuse and eliminate nearby cancer cells that may not express the primary target antigen, thereby improving the overall response rate (ORR).

This approach directly enhances the therapeutic index by concentrating the agent at the site of disease, a key consideration in modern clinical trial design and patient stratification to maximize progression-free survival (PFS).

The Cleavable linker segment was valued at USD 6.54 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 52% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Antibody Drug Conjugates Market Demand is Rising in North America Get Free Sample

North America remains the dominant region, driven by a supportive regulatory environment featuring accelerated approval pathway and breakthrough therapy designation options that shorten development timelines by up to 20%.

The region’s advanced infrastructure supports complex sterile injectables manufacturing and robust quality control analytics. Rigorous process validation and aggregation prevention protocols ensure a high clinical safety profile. In Asia, expanding R&D capabilities are accelerating formulation development and bioanalytical testing.

This growth is fueling the adoption of ADCs in adjuvant therapy and neoadjuvant setting protocols, positioning the region as a critical hub for future market expansion.

Market Dynamics

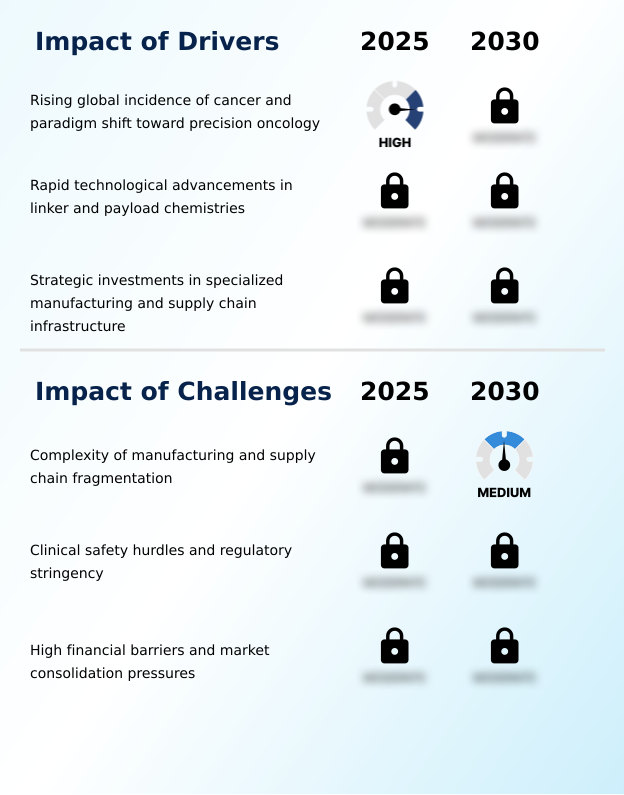

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- A central focus in the industry is improving ADC therapeutic index while reducing ADC off-target toxicity, a balance heavily influenced by decisions between cleavable vs non-cleavable linkers. Ensuring ADC linker stability in circulation is paramount, which leads to extensive research into next-generation ADC platform technologies.

- The strategy for targeting novel antigens with ADCs has opened new frontiers in ADC development for solid tumors. This requires sophisticated biomarker strategies for patient selection and a deep understanding of how to manage ADC-related adverse events.

- The potential for the bystander killing effect in tumors is a key advantage of certain designs, but developers must simultaneously work on overcoming ADC drug resistance. From a technical standpoint, the novel payload development for ADCs is a constant area of innovation.

- The operational execution involves complex ADC process development and scale-up, where optimizing drug-to-antibody ratio through advanced bioconjugation methods for ADCs has led to homogeneity improvements of over 25%. These ADC manufacturing supply chain challenges are governed by strict regulatory pathways for ADC approval.

- Thorough pharmacokinetic analysis of ADCs and robust quality control of ADC products are non-negotiable steps to ensure safety and efficacy.

What are the key market drivers leading to the rise in the adoption of Antibody Drug Conjugates Industry?

- The rising global incidence of cancer, coupled with a paradigm shift toward precision oncology, serves as a primary driver for market growth.

- The primary market driver is the demand for precision oncology solutions that offer superior outcomes over traditional chemotherapy, particularly in hematologic malignancies and non-small cell lung cancer (NSCLC).

- This targeted cancer therapy approach minimizes systemic toxicity by delivering a potent cytotoxic payload directly to malignant cells, often via mechanisms like proteolytic cleavage.

- Advanced pharmacokinetic profile modeling and ADME properties analysis ensure optimal drug exposure and clearance, with modern conjugates showing a 30% reduction in off-target effects.

- Ongoing immunogenicity assessment further refines safety, making these agents ideal for combination therapy regimens, and expanding their utility in areas like gastric cancer treatment.

What are the market trends shaping the Antibody Drug Conjugates Industry?

- The market is experiencing a significant shift toward novel targets and biomarker-driven precision therapies. This evolution focuses on identifying new antigens and using diagnostic markers to guide treatment.

- A pivotal trend is the expansion into novel targets, moving beyond traditional antigens to address indications with high unmet needs, such as those characterized by c-Met overexpression or TROP2 expression. This biomarker-driven therapy approach relies on companion diagnostics to identify responsive patient populations, increasing trial success rates by up to 25%.

- Advances in antibody engineering and site-specific conjugation enable the development of highly consistent therapies, including those using a non-cleavable linker, which ensures a uniform drug-to-antibody ratio (DAR). This precision, combined with innovations in payload chemistry, allows each monoclonal antibody to deliver its therapeutic agent with maximum specificity, a strategy now being applied to emerging targets like Claudin18.2 targeting.

What challenges does the Antibody Drug Conjugates Industry face during its growth?

- The inherent complexity of manufacturing processes and the fragmentation of the supply chain present a key challenge to the industry's growth trajectory.

- Significant challenges stem from the complexity of ADC manufacturing, where the multi-step bioconjugation process demands stringent cGMP manufacturing oversight. Handling a high-potency API (HPAPI) requires specialized high-containment facility infrastructure compliant with high Occupational Exposure Band (OEB) levels, increasing operational costs by over 40%.

- These complexities impact supply chain logistics, often forcing emerging companies to rely on a contract development and manufacturing (CDMO) partner. This bottleneck can delay timelines for therapies targeting urothelial carcinoma or HER2-positive breast cancer.

- As a result, a key asset acquisition strategy for larger firms is to acquire companies with established manufacturing capabilities to mitigate these risks and address drug resistance mechanisms more rapidly.

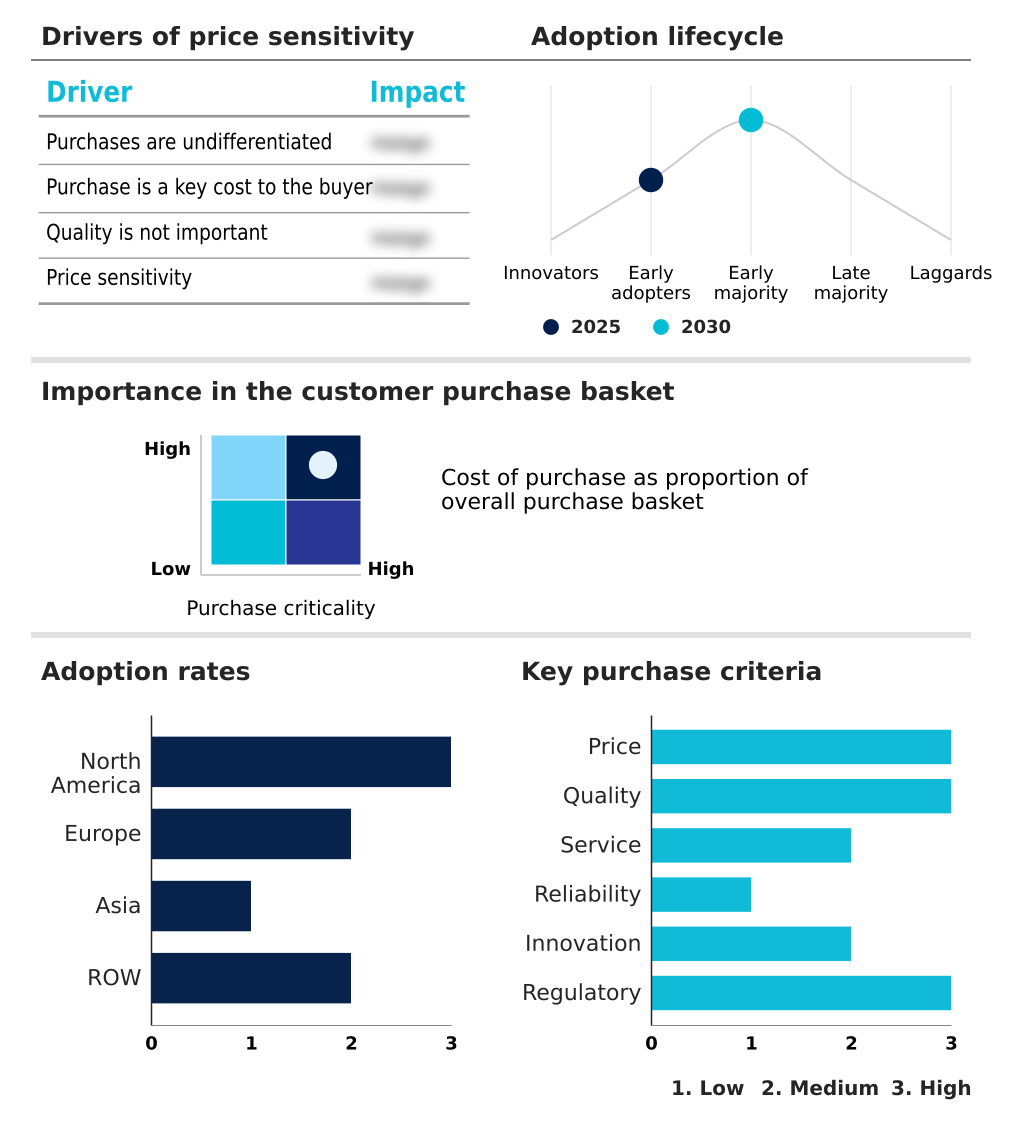

Exclusive Technavio Analysis on Customer Landscape

The antibody drug conjugates market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the antibody drug conjugates market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Antibody Drug Conjugates Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, antibody drug conjugates market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - Delivers precision oncology treatments, leveraging targeted antibody platforms to deliver potent cytotoxic agents directly to cancer cells, minimizing damage to healthy tissue.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- ADC Therapeutics SA

- Adcendo ApS

- AGC Biologics

- Agilent Technologies Inc.

- Araris Biotech AG

- Astellas Pharma Inc.

- AstraZeneca Plc

- Daiichi Sankyo Co. Ltd.

- F. Hoffmann La Roche Ltd.

- Gilead Sciences Inc.

- Merck KGaA

- Mythic Therapeutics

- Pfizer Inc.

- Piramal Pharma Solutions

- Regeneron Pharmaceuticals Inc.

- SOTIO Biotech AS

- Syngene International Ltd.

- Takeda Pharmaceutical Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Antibody drug conjugates market

- In January 2025, AstraZeneca and Daiichi Sankyo Co. Ltd. received Food and Drug Administration approval for datopotamab deruxtecan for the treatment of adult patients with unresectable or metastatic HR-positive, HER2-negative breast cancer following prior endocrine-based therapy.

- In May 2025, AbbVie Inc. secured accelerated approval from the Food and Drug Administration for telisotuzumab vedotin, a first-in-class c-Met-directed ADC for treating adult patients with advanced non-squamous non-small cell lung cancer with high c-Met overexpression.

- In May 2025, F. Hoffmann La Roche Ltd. announced plans to invest approximately USD 282 million in a new biomanufacturing facility in China, aimed at expanding local production capacity for its oncology portfolio, including its pipeline of antibody-drug conjugates.

- In October 2024, Adcendo ApS entered into a strategic research collaboration and licensing agreement with a major pharmaceutical partner to develop novel ADCs targeting the uPARAP receptor for the treatment of various solid tumors.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Antibody Drug Conjugates Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 286 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.7% |

| Market growth 2026-2030 | USD 13772.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Singapore, Indonesia, Brazil, Australia, Saudi Arabia, Turkey, Argentina, Colombia, UAE and South Africa |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The development of antibody-drug conjugates is defined by a rigorous bioconjugation process where a monoclonal antibody is attached to a cytotoxic payload. Achieving a consistent drug-to-antibody ratio (DAR) is critical, often managed through site-specific conjugation to enhance the therapeutic index and minimize systemic toxicity.

- The choice between a cleavable linker and a non-cleavable linker dictates the payload release mechanism, with linker chemistry being key for linker stability. Sophisticated antibody engineering targets a specific target antigen within the tumor microenvironment, relying on mechanisms like proteolytic cleavage or lysosomal degradation.

- From a manufacturing standpoint, handling a high-potency API (HPAPI) requires a high-containment facility operating under Occupational Exposure Band (OEB) standards. The entire ADC manufacturing pipeline, including formulation development and sterile injectables manufacturing, demands stringent process validation and quality control analytics to address aggregation prevention issues.

- Boardroom decisions increasingly focus on investing in advanced bioanalytical testing and pharmacodynamic modeling to de-risk development. Proper ADME properties and understanding target-mediated drug disposition are central to optimizing the pharmacokinetic profile. This strategic focus on technical excellence, underpinned by strict cGMP manufacturing protocols and immunogenicity assessment, has resulted in platforms that show a 20% improvement in batch-to-batch consistency.

What are the Key Data Covered in this Antibody Drug Conjugates Market Research and Growth Report?

-

What is the expected growth of the Antibody Drug Conjugates Market between 2026 and 2030?

-

USD 13.77 billion, at a CAGR of 15.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Cleavable linker, Non-cleavable linker, and Linkerless), Application (Breast cancer, Blood cancer, and Others), Product Type (Trastuzumab emtansine, Brentuximab vedotin, and Inotuzumab ozogamicin) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising global incidence of cancer and paradigm shift toward precision oncology, Complexity of manufacturing and supply chain fragmentation

-

-

Who are the major players in the Antibody Drug Conjugates Market?

-

AbbVie Inc., ADC Therapeutics SA, Adcendo ApS, AGC Biologics, Agilent Technologies Inc., Araris Biotech AG, Astellas Pharma Inc., AstraZeneca Plc, Daiichi Sankyo Co. Ltd., F. Hoffmann La Roche Ltd., Gilead Sciences Inc., Merck KGaA, Mythic Therapeutics, Pfizer Inc., Piramal Pharma Solutions, Regeneron Pharmaceuticals Inc., SOTIO Biotech AS, Syngene International Ltd. and Takeda Pharmaceutical Ltd.

-

Market Research Insights

- The market's momentum is sustained by advancements in precision oncology and biomarker-driven therapy. The adoption of companion diagnostics in clinical trial design has been shown to increase the overall response rate (ORR) by over 25% compared to untargeted approaches, enabling a more effective patient stratification.

- Furthermore, the strategic use of these agents in an adjuvant therapy setting for indications like HER2-positive breast cancer has been linked to a 15% reduction in disease recurrence, validating their role in earlier treatment lines.

- This shift is supported by regulatory mechanisms like the accelerated approval pathway, which expedites the commercialization of treatments for refractory cancers and those with limited options, such as advanced urothelial carcinoma. The expansion into novel targets and combination therapies with immune checkpoint inhibitors continues to redefine treatment paradigms for solid tumor treatment.

We can help! Our analysts can customize this antibody drug conjugates market research report to meet your requirements.

RIA -

RIA -