Caps And Closures Market Size 2024-2028

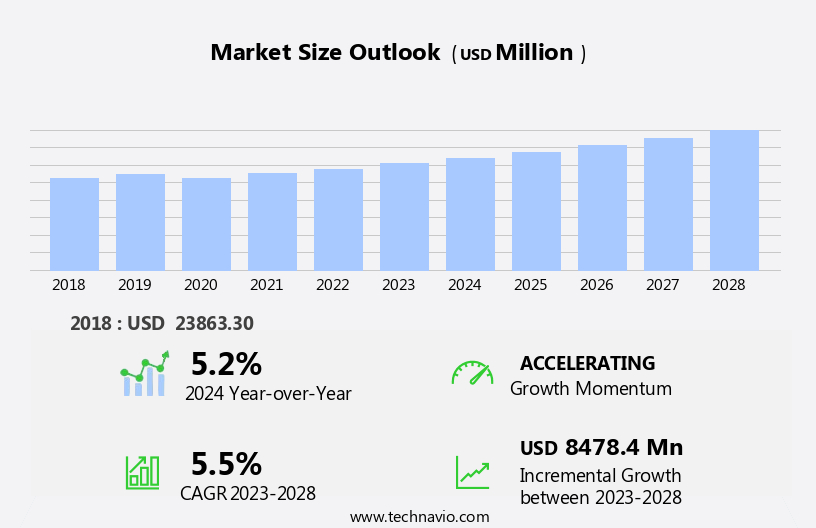

The caps and closures market size is forecast to increase by USD 8.48 billion, at a CAGR of 5.5% between 2023 and 2028.

- The market is witnessing significant growth, driven primarily by the increasing demand from the pharmaceutical industry. This sector's expansion is attributed to the rising production of pharmaceuticals and the subsequent requirement for secure and effective packaging solutions. Another key trend influencing the market is the continuous launch of new products catering to various applications, such as food and beverages, cosmetics, and healthcare. However, the market faces challenges due to the volatile raw material prices of caps and closures. The prices of raw materials like PVC, PE, and PP fluctuate significantly, leading to price instability for caps and closure manufacturers.

- This volatility can impact the profitability of companies in the market, necessitating effective supply chain management strategies and price negotiations with raw material suppliers. Additionally, the growing preference for sustainable packaging solutions is influencing the market. Companies are focusing on developing eco-friendly alternatives to traditional caps and closures made from plastic materials. Biodegradable caps and closures derived from renewable resources, such as sugarcane and cornstarch, are gaining popularity due to their reduced environmental impact. In conclusion, the market is experiencing robust growth, driven by the pharmaceutical industry's increasing demand and new product launches. However, the market is challenged by the volatile raw material prices and the growing preference for sustainable packaging solutions.

- Companies seeking to capitalize on market opportunities and navigate challenges effectively must focus on supply chain management strategies, price negotiations, and the development of eco-friendly alternatives.

What will be the Size of the Caps And Closures Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

- The market continues to evolve, driven by advancements in technology and shifting consumer preferences. Hermetically sealed containers with pilfer-proof closures ensure product preservation and security, making them a popular choice in various sectors. Flip-top closures offer convenience, while leak detection technology ensures safety and reliability. Sustainable packaging closures, such as those made from renewable materials, are gaining traction as companies prioritize eco-friendliness. Heat sealing equipment and closure torque control systems streamline the manufacturing process, improving efficiency and reducing costs. Container sterilization and closure integrity testing are crucial steps in ensuring product safety and quality. Metal container closures and automated capping systems are staples in industries like food and beverage, while pharmaceutical capping requires specialized equipment and material compatibility testing.

- The closure manufacturing process incorporates various technologies, including pressure sensitive adhesive, screw cap closures, and induction sealing processes. Child resistant closures and tamper evident seals prioritize consumer safety, while closure liner materials and bottle closure design cater to aesthetic and functional considerations. Single-use closures and modified atmosphere packaging extend product shelf life, while rotary capping machines and high-speed capping systems increase production capacity. Spout pouch closures and plastic bottle closures cater to the growing demand for convenience and portability. Aerosol can dispensing and flexible packaging closures expand market reach, with septic closure systems ensuring product purity. Closure quality control remains a priority, with continuous motion cappers and jar sealing mechanisms ensuring consistent results.

- The market's continuous dynamism underscores the importance of staying informed and adaptable.

How is this Caps And Closures Industry segmented?

The caps and closures industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

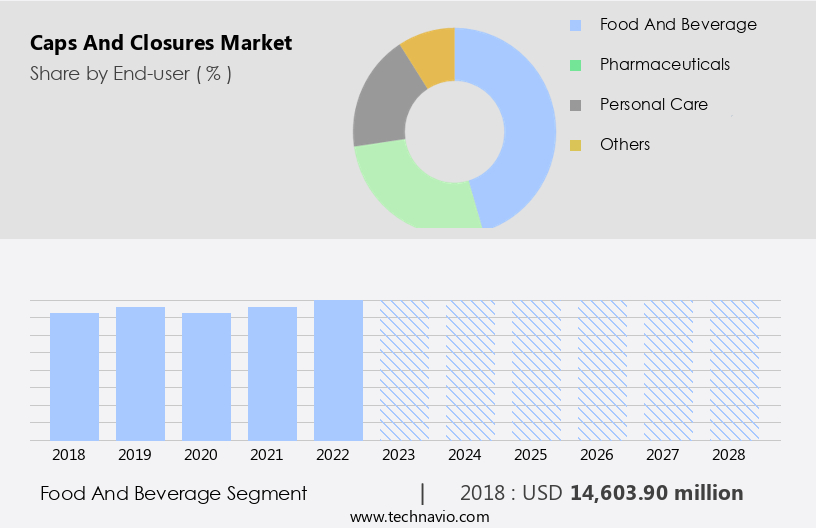

- End-user

- Food and beverage

- Pharmaceuticals

- Personal care

- Others

- Geography

- North America

- US

- Europe

- Germany

- Russia

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

The food and beverage segment is estimated to witness significant growth during the forecast period.

In the dynamic packaging market, various closure solutions cater to diverse industry requirements. The demand for pilfer-proof closures and hermetically sealed containers is significant in the food and beverage sector, particularly for carbonated soft drinks, packaged water, and juices, due to their preservative properties. Flip-top closures and leak detection technology are popular choices for consumer convenience and product safety in the liquid packaged foods and non-carbonated beverages segments. Sustainable packaging closures, such as those made from renewable materials, are gaining traction due to increasing consumer awareness and regulations. Heat sealing equipment and closure torque control ensure proper container sterilization and closure integrity testing, respectively, during the manufacturing process.

Metal container closures and automated capping systems are essential for the pharmaceutical industry, where pressure sensitive adhesive, screw cap closures, and induction sealing processes are commonly used. Child resistant closures and material compatibility testing are crucial for safety and regulatory compliance. Closure liner materials, bottle closure design, and single-use closures are continuously evolving to meet consumer preferences and convenience. Modified atmosphere packaging, rotary capping machines, container sealing systems, high-speed capping machines, spout pouch closures, plastic bottle closures, and pharmaceutical capping are integral components of the market. Tamper evident seals ensure product security in various applications, including aerosol can dispensing and flexible packaging closures.

The packaging industry's ongoing innovation and the growing demand for advanced closure solutions are key market drivers.

The Food and beverage segment was valued at USD 14.6 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

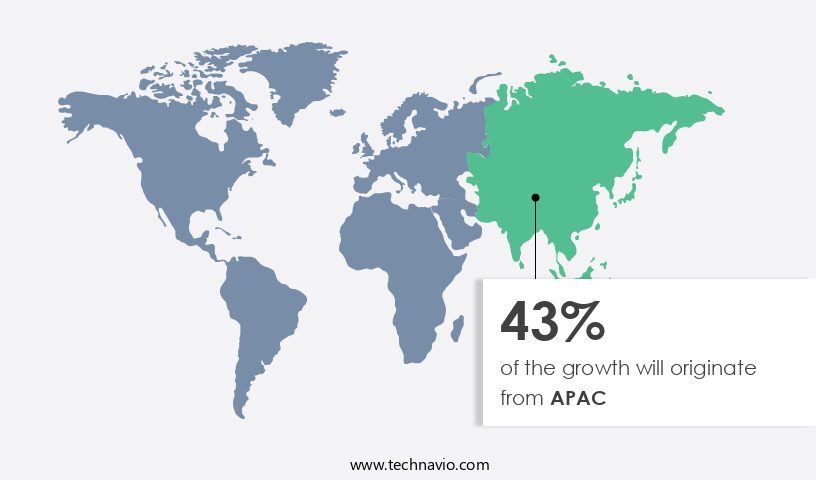

APAC is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the past decade, manufacturing activities in Asia Pacific countries, including India, China, Japan, Singapore, and Australia, have experienced significant growth. This expansion is driven by changing lifestyles and urbanization, leading consumers to prefer packaged and fresh food and beverages. In response, food product manufacturers are adopting innovative packaging solutions that offer enhanced aesthetic appeal and convenience. Furthermore, emerging economies such as Japan, India, and China have witnessed a surge in their food and beverage processing industries due to population lifestyle shifts.

The trend toward on-the-go food and beverage products has also fueled the demand for packaged food items. This shift in consumer preferences is transforming the food and beverage industry landscape, with a focus on creating immersive and harmonious packaging designs that resonate with consumers.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a diverse range of products designed to seal and protect containers, ensuring the preservation of their contents. From screw caps for food and beverage containers to snap-on closures for cosmetics and pharmaceuticals, this market caters to various industries and applications. One notable trend in the market is the focus on sustainability, with biodegradable and recyclable options gaining popularity. Another key area is the integration of advanced technologies, such as child-resistant closures and RFID tagging, to enhance functionality and security. Furthermore, the demand for tamper-evident caps and closures is increasing, particularly in the food and beverage sector, to maintain product safety and integrity. Additionally, the use of caps and closures in the growing e-commerce industry is driving innovation, with solutions that facilitate easy opening and resealing for online orders. Overall, the market is a dynamic and evolving sector, offering numerous opportunities for growth and innovation.

What are the key market drivers leading to the rise in the adoption of Caps And Closures Industry?

- The pharmaceutical industry's growing requirement for caps and closures serves as the primary market driver.

ai_test_driver_explanation_gai.multili

What are the market trends shaping the Caps And Closures Industry?

- The trend in the market is toward new product launches. As a professional, I am well-informed about this developing industry trend.

- companies in the market continue to innovate and introduce new products to cater to the evolving needs of consumers and industries. For instance, Berry Global, a leading player, recently collaborated with The Coca-Cola Company to provide a tethered closure for its carbonated soft drinks in PET bottles. This lightweight closure ensures bottle integrity and remains attached to the bottle. In another development, Berry Global launched a new lightweight plastic food closure that minimizes material usage without compromising performance and consumer convenience. Moreover, the importance of closure integrity testing has gained significant attention in the market. This testing ensures the proper sealing and functionality of closures, which is crucial for preserving the contents and maintaining food safety.

- Closure manufacturers invest in advanced technologies, such as automated capping systems and induction sealing processes, to ensure high-quality closure production and meet the stringent requirements of various industries. Material compatibility testing is another essential aspect of the market. Closure liner materials, such as pressure-sensitive adhesives and screw cap closures, must be compatible with the container materials to ensure a secure seal and prevent contamination. companies focus on research and development to create materials that offer superior compatibility and performance. Child-resistant closures are gaining popularity due to increasing regulations and consumer demand for safer packaging solutions. These closures prevent accidental ingestion of harmful contents, particularly in the pharmaceutical and food industries.

- Closure manufacturers invest in designing and producing child-resistant closures that meet the specific requirements of various applications.

What challenges does the Caps And Closures Industry face during its growth?

- The volatile pricing of raw materials for caps and closures poses a significant challenge to the industry's growth trajectory.

- The market is influenced by the volatility of global crude oil prices, which significantly impact the production cost of plastic, a primary material used in the manufacturing of caps and closures. Fluctuations in oil prices, such as those caused by geopolitical tensions like the Russian invasion of Ukraine, can lead to increased costs for raw materials like polyethylene and propylene. These price fluctuations can hinder the growth of the caps and closures industry. Closure integrity testing is essential to ensure product safety and consumer trust. Metal container closures, such as tin caps and aluminum screw caps, are widely used due to their durability and resistance to external factors.

- Automated capping systems are increasingly adopted for their efficiency and cost savings. Pressure sensitive adhesive (PSA) closures, including screw caps and snap-on lids, are popular for their ease of use and versatility. The induction sealing process is commonly used for PSA closures to ensure airtight seals. Child-resistant closures are crucial in various industries, including pharmaceuticals and food and beverage, to ensure safety. Material compatibility testing is vital to ensure the suitability of closure liners for various applications. Closure liner materials, such as polyethylene, polypropylene, and polyvinyl chloride, must be carefully selected based on the product's contents and intended use.

- Ensuring compatibility between the closure liner and the container's contents is crucial to maintain product quality and safety.

Exclusive Customer Landscape

The caps and closures market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the caps and closures market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, caps and closures market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ALCOPACK Group - The company specializes in providing diverse caps and closure solutions, including STELVIN aluminum screwcaps, capsules, and plastic variants, catering to various industry demands. These offerings ensure optimal product preservation and consumer convenience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ALCOPACK Group

- Amcor Plc

- AptarGroup Inc.

- BERICAP Holding GmbH

- Berry Global Inc.

- Blackhawk Molding Co. Inc.

- Caps and Closures Pty Ltd.

- Coral Products Plc

- Crown Holdings Inc.

- Guala Closures SpA

- HERTI JSC

- Oricon Enterprises Ltd.

- Pact Group Holdings Ltd.

- Pelliconi and C SpA

- Phoenix Closures Inc.

- Plastic Closures Ltd.

- Premier Vinyl Solutions Ltd.

- Reynolds Group Ltd.

- Silgan Holdings Inc.

- United States Plastic Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Caps And Closures Market

- In January 2024, Amcor, a global packaging company, announced the launch of its new PET bottle closure system, named 'Unibloc RC,' designed to reduce plastic waste by using mono-materials. This innovation addresses the growing market demand for sustainable packaging solutions (Amcor Press Release, 2024).

- In March 2024, Bericap, a leading international manufacturer of plastic closures, entered into a strategic partnership with Schmalbach-Lubeca, a German machinery manufacturer. This collaboration aimed to develop innovative, high-performance closures for the beverage industry, leveraging Bericap's expertise in closure design and Schmalbach-Lubeca's machinery capabilities (Bericap Press Release, 2024).

- In May 2024, Closure Systems International (CSI), a global leader in closure solutions, completed the acquisition of Capsulex, a U.S.-based provider of high-performance PET closures. This acquisition expanded CSI's product portfolio and strengthened its presence in the North American market (CSI Press Release, 2024).

- In February 2025, the European Union (EU) approved the use of polylactide (PLA) as a material for food contact applications, including caps and closures. This approval opened new opportunities for biodegradable caps and closures in the European market, addressing the growing demand for eco-friendly packaging solutions (European Commission Press Release, 2025).

Research Analyst Overview

The market continues to evolve, driven by advancements in packaging design optimization, child resistant technology, active packaging solutions, and aseptic packaging techniques. Leakage detection methods and container closure integrity are paramount in ensuring product safety and freshness, while modified atmosphere packaging and septic closure validation maintain product quality. Cap liner selection, sterile filling systems, and food grade closures are essential in various industries, including pharmaceuticals and cosmetics. Closure material science, packaging line efficiency, and quality control metrics are crucial in maintaining industrial container closures' performance. Sustainable packaging materials, high barrier packaging, and smart packaging technology are gaining traction, as businesses strive for waste reduction and improved supply chain traceability.

Packaging automation and circular economy packaging are further shaping the market, offering cost-effective and eco-friendly solutions. Closure performance testing remains a critical aspect of the market, ensuring consumer safety and regulatory compliance. The ongoing unfolding of market activities and evolving patterns reflect the dynamic nature of the caps and closures industry. From tamper evident labels and pharmaceutical packaging to smart technology and industrial applications, the market's continuous growth and innovation are shaping the future of packaging solutions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Caps And Closures Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

137 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.5% |

|

Market growth 2024-2028 |

USD 8478.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.2 |

|

Key countries |

US, China, Germany, Russia, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Caps And Closures Market Research and Growth Report?

- CAGR of the Caps And Closures industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the caps and closures market growth of industry companies

We can help! Our analysts can customize this caps and closures market research report to meet your requirements.

RIA -

RIA -