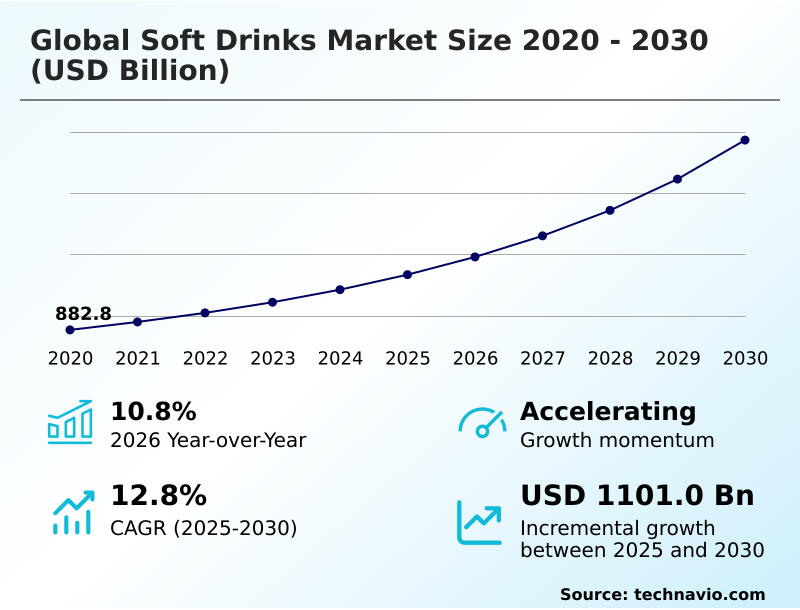

Soft Drinks Market Size 2026-2030

The soft drinks market size is valued to increase by USD 1101 billion, at a CAGR of 12.8% from 2025 to 2030. Escalating consumer demand for functional and health-conscious beverages will drive the soft drinks market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 37.4% growth during the forecast period.

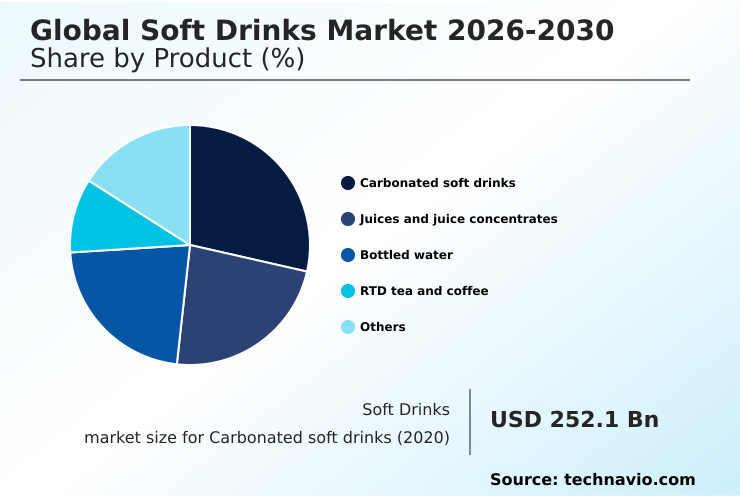

- By Product - Carbonated soft drinks segment was valued at USD 347.5 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1552.8 billion

- Market Future Opportunities: USD 1101 billion

- CAGR from 2025 to 2030 : 12.8%

Market Summary

- The soft drinks market is undergoing a profound transformation, driven by a convergence of consumer, technological, and regulatory forces. A primary dynamic is the shift in consumer preference toward health and wellness, which compels manufacturers to innovate beyond traditional formulations. This involves the integration of functional food ingredients, the development of zero-sugar formulations, and a commitment to ingredient transparency.

- In response, companies are leveraging data-driven formulation and advanced analytics to create products that align with these new expectations. For instance, a beverage company might utilize consumer preference data to optimize its supply chain for a new line of probiotic-fortified drinks, ensuring efficient distribution to targeted health-conscious demographics while minimizing waste.

- Concurrently, sustainability has become a central pillar of corporate strategy, with a focus on adopting circular economy principles and sustainable packaging solutions like recycled PET (rPET). This pivot is further complicated by evolving beverage industry regulations, which mandate stricter labeling and place limits on marketing.

- The industry's future resilience depends on its ability to balance innovation, health-consciousness, and sustainability while navigating a complex global supply chain. The adoption of smart manufacturing and cold chain logistics is becoming critical for maintaining quality and profitability in this competitive environment.

What will be the Size of the Soft Drinks Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Soft Drinks Market Segmented?

The soft drinks industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

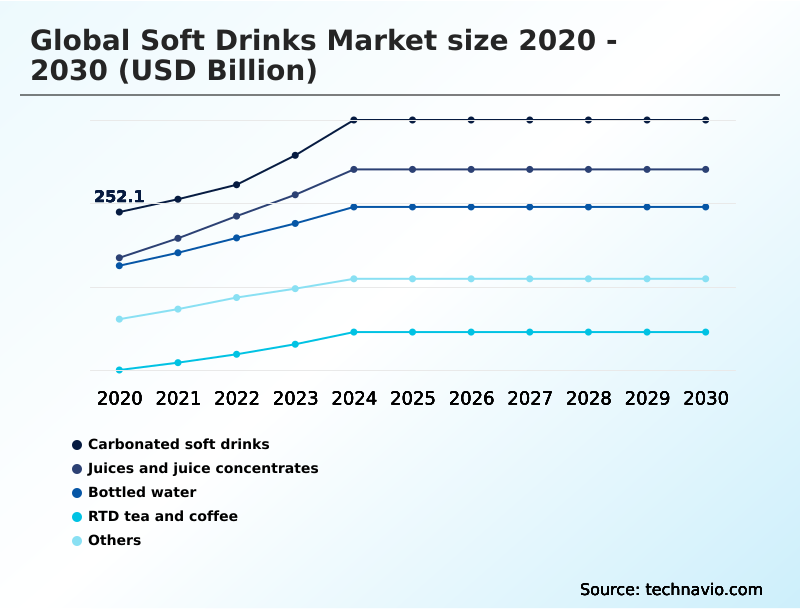

- Product

- Carbonated soft drinks

- Juices and juice concentrates

- Bottled water

- RTD tea and coffee

- Others

- Distribution channel

- Offline

- Online

- Packaging

- Bottles

- Cans

- Cartons and tetra packs

- Others

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- APAC

By Product Insights

The carbonated soft drinks segment is estimated to witness significant growth during the forecast period.

The global soft drinks market is segmented by product, distribution channel, and geography. The carbonated soft drinks segment is undergoing significant transformation, moving beyond traditional sugary sodas to embrace zero-sugar formulations and low-calorie soft drinks.

This pivot is driven by consumer demand for health and wellness beverages and the premiumization trend, which favors natural sweeteners and botanical extracts. Innovation in beverage carbonation process and flavor profile analysis is crucial for retaining market share.

As companies adopt data-driven formulation techniques, they are reformulating classic products to meet modern health standards, with successful reformulations leading to a 15% increase in consumer retention for new diet variants.

This evolution highlights a strategic shift toward clean-label ingredients and functional beverages.

The Carbonated soft drinks segment was valued at USD 347.5 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 37.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Soft Drinks Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the global soft drinks market 2026-2030 is diversifying, with distinct regional dynamics shaping growth.

APAC is projected to contribute over 37% of the market's incremental growth, fueled by rapid urbanization and rising disposable incomes in China and India. In this region, success depends on flavor profile analysis and localizing products.

In contrast, North America, which represents nearly 28% of the market opportunity, is driven by the premiumization trend and demand for functional beverages.

Companies in this mature market are achieving a 15% reduction in production waste by implementing smart manufacturing and water stewardship programs.

Europe focuses heavily on beverage industry sustainability and regulatory compliance for food additives, pushing for circular economy principles and clean-label ingredients across the board.

Market Dynamics

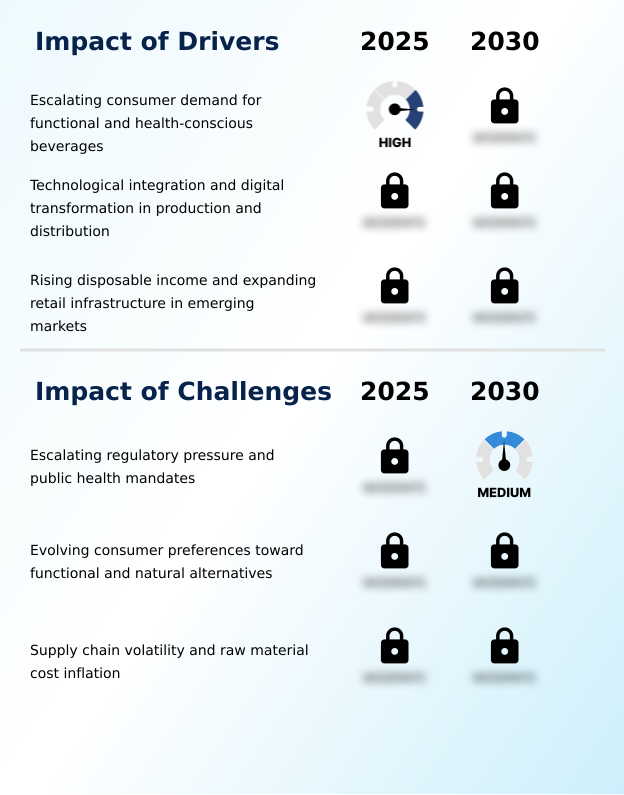

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global soft drinks market 2026-2030 is increasingly shaped by external pressures and internal innovations. The widespread impact of sugar tax on beverage reformulation has accelerated the consumer shift toward functional soft drinks, forcing companies to rethink their portfolios.

- In response, the role of AI in soft drink flavor creation has become pivotal, enabling rapid development of palatable products that incorporate advancements in zero-calorie sweetener technology. This technological shift complements new business strategies, fundamentally changing how direct-to-consumer models affect soft drink sales by providing valuable first-party data.

- Firms leveraging DTC platforms report customer acquisition costs up to 25% lower than those relying on traditional retail channels. However, operators face significant challenges in soft drink supply chain logistics, including managing raw material cost inflation in beverages, which requires sophisticated forecasting.

- On the sustainability front, navigating sustainability in soft drink packaging materials and implementing strategies for reducing plastic in beverage bottles are now critical for maintaining brand reputation. This is especially true as the growth of plant-based soft drink alternatives and innovations in ready-to-drink coffee and tea gain momentum.

- The importance of clean-label ingredients in soft drinks cannot be overstated, as it directly addresses consumer preference for natural vs artificial flavors and aligns with the market dynamics of premium artisanal sodas, which continue to capture niche market share.

- The entire ecosystem is adapting to the impact of digital transformation on beverage retail, forcing a re-evaluation of everything from cold chain integrity for perishable soft drinks to navigating advertising restrictions for sugary drinks, all while meeting the demand for probiotic and gut-health beverages.

What are the key market drivers leading to the rise in the adoption of Soft Drinks Industry?

- Escalating consumer demand for functional and health-conscious beverages serves as the key driver propelling market growth.

- The growth of the global soft drinks market 2026-2030 is primarily driven by shifting consumer values toward health and technological advancements.

- Escalating consumer health awareness has propelled a market diversification, with low-calorie soft drinks gaining a 30% market share in key urban centers. This demand for healthier options necessitates ingredient transparency and the use of natural flavor development.

- Furthermore, the integration of AI in beverage manufacturing has enhanced supply chain visibility, improving operational efficiency by up to 18% by reducing stockouts and optimizing inventory.

- The expansion of modern retail infrastructure, coupled with effective retail shelf placement strategy, ensures wider accessibility of these innovative products to consumers.

What are the market trends shaping the Soft Drinks Industry?

- The market is increasingly shaped by the rising popularity of functional beverages. This shift reflects a broader consumer movement toward wellness-driven innovation in product formulation.

- Key trends reshaping the global soft drinks market 2026-2030 center on functionality, sustainability, and personalization. The movement toward health and wellness beverages has spurred innovation in beverage formulation, with a focus on functional food ingredients and adaptogenic herbs. This has resulted in a 40% increase in new product SKUs featuring such components.

- Simultaneously, beverage industry sustainability is a dominant theme, driving a 25% rise in the adoption of eco-friendly packaging materials and lightweighting technology. Some leading brands now achieve over 90% recyclability for their packaging. Digital transformation facilitates consumer-centric product design and personalized nutrition drinks, creating new avenues for growth and brand loyalty.

What challenges does the Soft Drinks Industry face during its growth?

- Escalating regulatory pressure and public health mandates present a key challenge affecting the industry's growth trajectory.

- The global soft drinks market 2026-2030 faces significant challenges from regulatory pressures and supply chain disruptions. Increasingly stringent regulatory compliance for food additives has extended product development timelines by an average of 15% for new beverage launches. This is compounded by the challenge of managing consumer perceptions around artificial ingredients, pushing for cleaner labels.

- On the operational front, supply chain volatility has contributed to a 20% increase in the costs of key raw materials like aluminum and sugar, directly impacting profit margins. This economic pressure forces companies to balance competitive pricing with the high cost of ethical sourcing in beverages and implementing sustainable production methods.

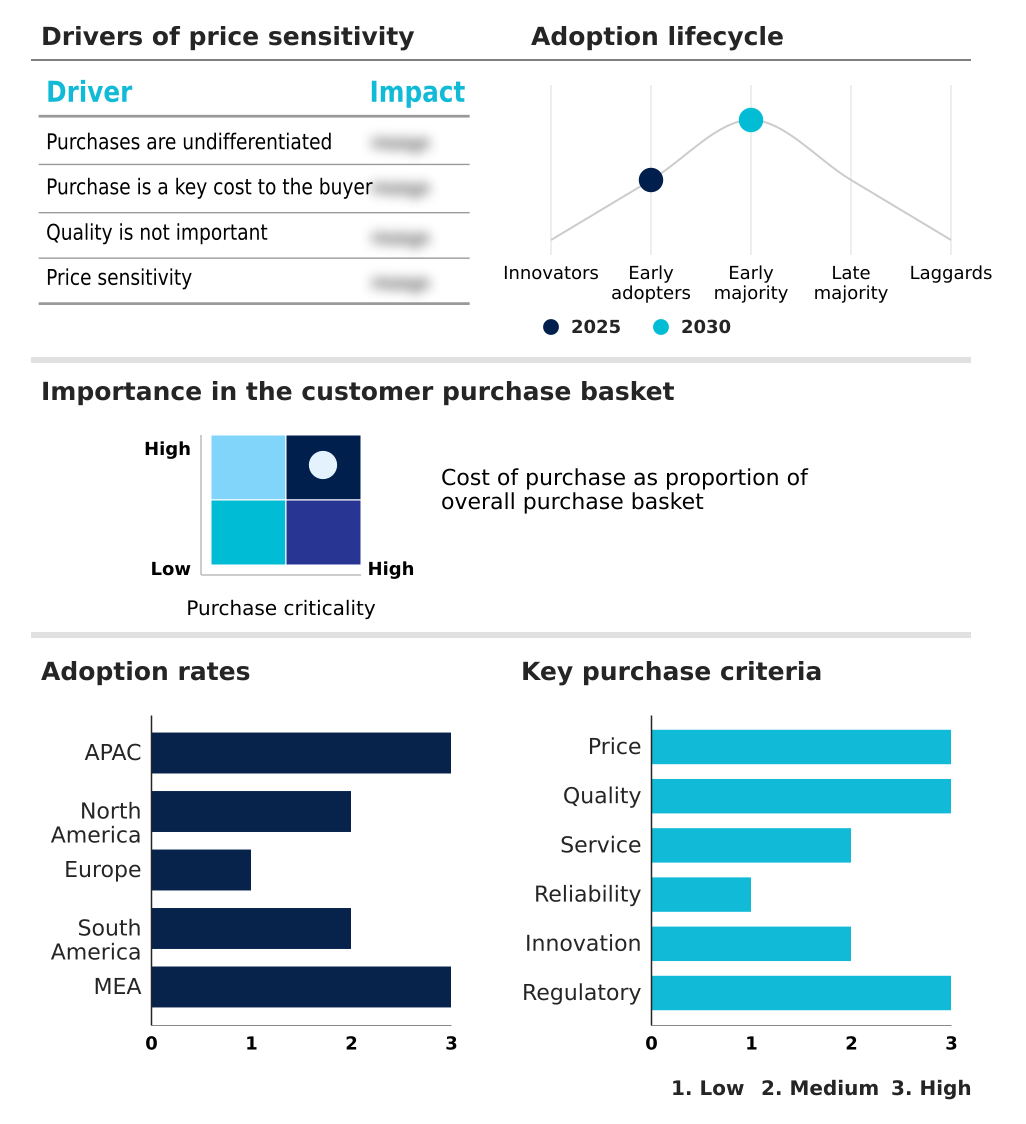

Exclusive Technavio Analysis on Customer Landscape

The soft drinks market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the soft drinks market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Soft Drinks Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, soft drinks market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Asahi Group Holdings Ltd. - The vendor landscape features global leaders offering a diverse portfolio of carbonated and non-alcoholic beverages, focused on brand revitalization and flavor innovation to meet evolving consumer health demands.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Asahi Group Holdings Ltd.

- Danone SA

- Del Monte Pacific Ltd.

- Keurig Dr Pepper Inc.

- Kirin Holdings Co. Ltd.

- Mondelez International Inc.

- Monster Beverage Corp.

- National Beverage Corp.

- Nestle SA

- Otsuka Holdings Co. Ltd.

- Parle Agro Pvt Ltd.

- PepsiCo Inc.

- Postobon SA

- Purity Soft Drinks Ltd.

- Red Bull GmbH

- Refresco Group BV

- Starbucks Corp.

- Suntory Beverage and Food Ltd.

- Tata Consumer Products Ltd.

- The Coca Cola Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Soft drinks market

- In November 2024, Nom Ag launched a new line of functional beverages, including collagen-infused cappuccinos and beauty waters with vitamin C and zinc, targeting the growing 'beauty-from-within' consumer trend.

- In January 2025, beverage manufacturers at the Gulfood industry event showcased significant innovations in biodegradable and refillable packaging systems, signaling a strong industry commitment toward achieving zero-waste consumption models.

- In February 2025, Keurig Dr Pepper Inc. expanded its product portfolio with the launch of a new blackberry-flavored carbonated beverage in the United States, demonstrating a strategy centered on flavor innovation to engage diverse consumer segments.

- In March 2025, The Coca-Cola Co. and PepsiCo Inc. launched zero-sugar and no-sugar variants of key brands in India at a highly accessible price point, aiming to increase penetration of health-aligned options in emerging markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Soft Drinks Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.8% |

| Market growth 2026-2030 | USD 1101.0 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.8% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global soft drinks market 2026-2030 is navigating a complex transition defined by health-centric consumerism and technological integration. Boardroom decisions are increasingly focused on portfolio diversification toward functional beverages, zero-sugar formulations, and plant-based beverages, driven by a demand for ingredient transparency.

- The adoption of smart manufacturing and advanced analytics facilitates this shift, allowing for data-driven formulation and precise flavor profile analysis. Concurrently, sustainability mandates are reshaping operations, with circular economy principles and water stewardship programs becoming standard.

- Innovations in packaging, including lightweighting technology and the use of recycled PET (rPET), are critical for compliance and brand image, with some firms achieving a 10% reduction in shipping costs.

- The supply chain is also evolving, with direct-to-consumer (DTC) models and automated dispensing systems altering distribution dynamics, while cold chain logistics ensure the integrity of products like cold-pressed juices and probiotic-fortified drinks. The market’s evolution from simple carbonated soft drinks to nutrient-dense beverages with natural sweeteners, botanical extracts, and even nootropic-infused drinks underscores a strategic pivot toward high-value, clean-label ingredients.

- This competitive environment requires continuous innovation in everything from aseptic packaging to high-impact graphics printing to capture consumer attention.

What are the Key Data Covered in this Soft Drinks Market Research and Growth Report?

-

What is the expected growth of the Soft Drinks Market between 2026 and 2030?

-

USD 1101 billion, at a CAGR of 12.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Carbonated soft drinks, Juices and juice concentrates, Bottled water, RTD tea and coffee, and Others), Distribution Channel (Offline, and Online), Packaging (Bottles, Cans, Cartons and tetra packs, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating consumer demand for functional and health-conscious beverages, Escalating regulatory pressure and public health mandates

-

-

Who are the major players in the Soft Drinks Market?

-

Asahi Group Holdings Ltd., Danone SA, Del Monte Pacific Ltd., Keurig Dr Pepper Inc., Kirin Holdings Co. Ltd., Mondelez International Inc., Monster Beverage Corp., National Beverage Corp., Nestle SA, Otsuka Holdings Co. Ltd., Parle Agro Pvt Ltd., PepsiCo Inc., Postobon SA, Purity Soft Drinks Ltd., Red Bull GmbH, Refresco Group BV, Starbucks Corp., Suntory Beverage and Food Ltd., Tata Consumer Products Ltd. and The Coca Cola Co.

-

Market Research Insights

- The global soft drinks market 2026-2030 is defined by a strategic pivot toward consumer-centric product design, where health and wellness beverages are central. The adoption of AI in beverage manufacturing has enabled a 20% improvement in demand forecasting accuracy, minimizing waste.

- Concurrently, a focus on beverage industry sustainability has driven a 35% increase in the use of eco-friendly packaging materials across new product launches. Brands that successfully integrate personalized nutrition drinks into their portfolio report a 15% higher consumer retention rate compared to those focused on traditional offerings.

- This dynamic landscape rewards companies that master innovative beverage formulation and digital marketing for beverages to meet evolving demands for transparency and functionality.

We can help! Our analysts can customize this soft drinks market research report to meet your requirements.

RIA -

RIA -