Cardiology Electrodes Market Size 2025-2029

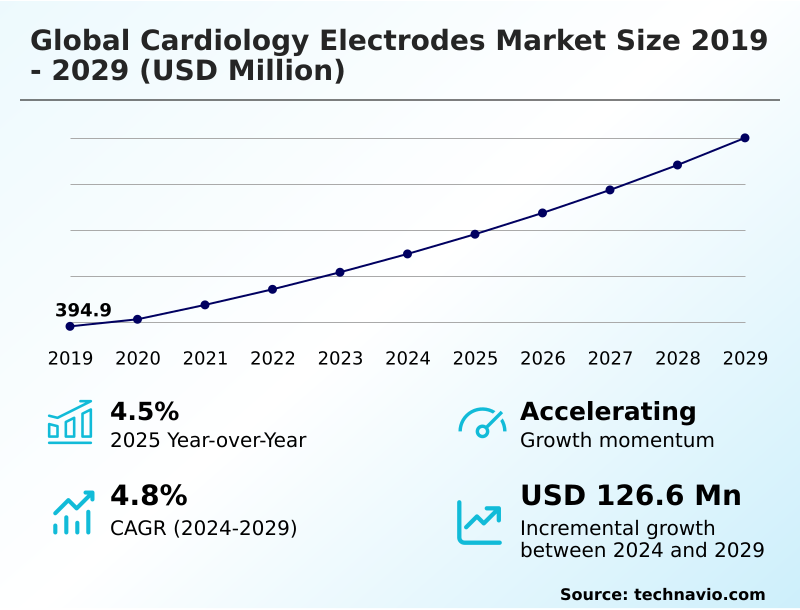

The cardiology electrodes market size is valued to increase by USD 126.6 million, at a CAGR of 4.8% from 2024 to 2029. Increasing prevalence of CVDs will drive the cardiology electrodes market.

Major Market Trends & Insights

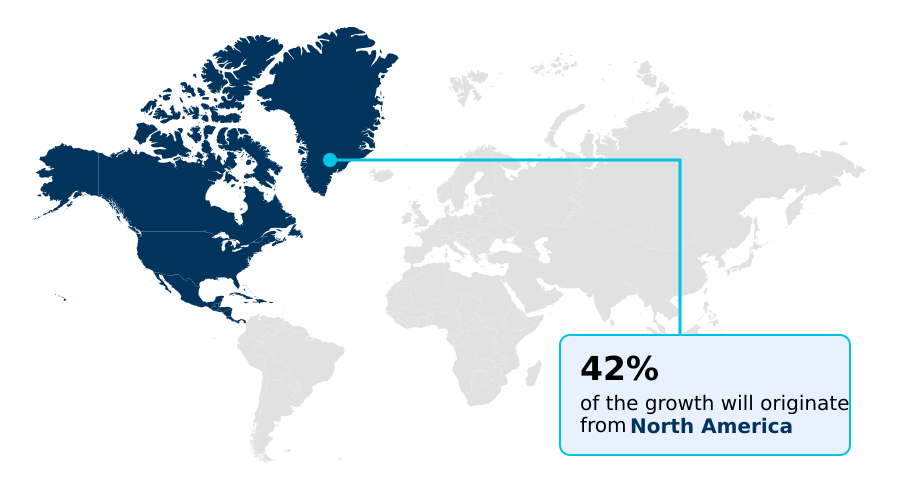

- North America dominated the market and accounted for a 41.9% growth during the forecast period.

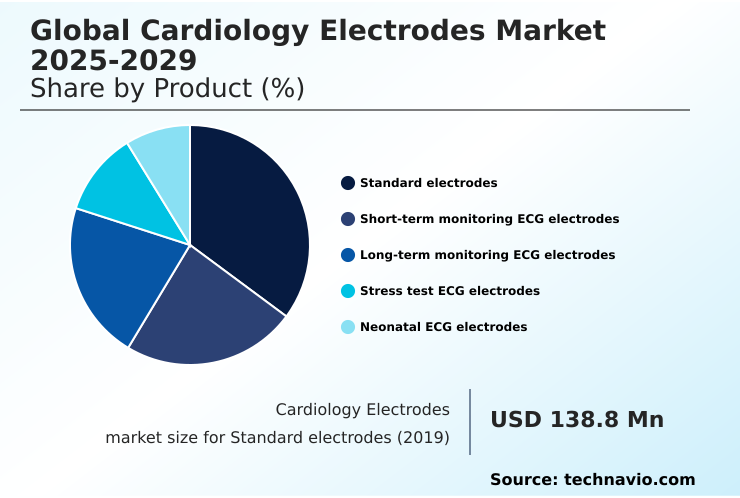

- By Product - Standard electrodes segment was valued at USD 160.4 million in 2023

- By End-user - Hospitals segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 205.6 million

- Market Future Opportunities: USD 126.6 million

- CAGR from 2024 to 2029 : 4.8%

Market Summary

- The cardiology electrodes market is integral to modern cardiac care, evolving beyond traditional diagnostics. A primary driver is the rising incidence of cardiovascular conditions, which elevates the demand for reliable monitoring in both clinical and remote settings. This has accelerated the industry-wide adoption of disposable ECG electrodes, which are critical for infection control and ensuring consistent performance.

- Technological advancements are a cornerstone of market development, with significant research directed toward creating innovative materials like conductive textiles and graphene-based films. These next-generation electrodes offer enhanced patient comfort and superior signal quality, which is crucial for long-term monitoring applications. For instance, a healthcare system can leverage wearable biosensors to continuously track at-risk cardiac patients post-discharge.

- This approach not only facilitates early detection of adverse events but also optimizes hospital resource allocation by reducing readmission rates, demonstrating the tangible link between advanced electrode technology and operational efficiency. The market is also navigating challenges related to material costs and the complexities of integrating new electrode technologies with existing diagnostic platforms.

What will be the Size of the Cardiology Electrodes Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cardiology Electrodes Market Segmented?

The cardiology electrodes industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

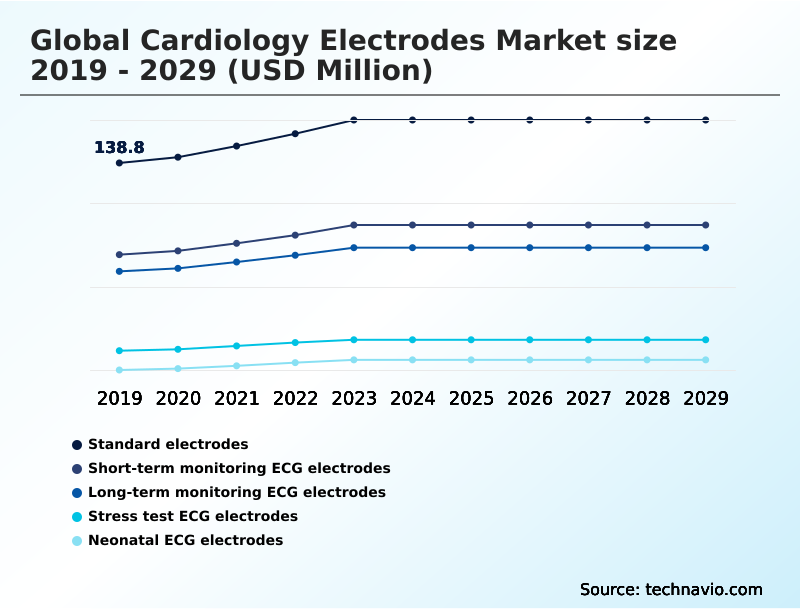

- Product

- Standard electrodes

- Short-term monitoring ECG electrodes

- Long-term monitoring ECG electrodes

- Stress test ECG electrodes

- Neonatal ECG electrodes

- End-user

- Hospitals

- ASCs

- Others

- Application

- Electrocardiography

- Monitoring

- Electroencephalography

- Cardiac resynchronization therapy

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Asia

- Rest of World (ROW)

- North America

By Product Insights

The standard electrodes segment is estimated to witness significant growth during the forecast period.

The standard electrodes segment constitutes the foundational component of the cardiology electrodes market, essential for routine diagnostic procedures in clinical settings. These products, designed for short-term use, are pivotal for conducting 12-lead resting ECGs.

Market dynamics are shaped by the high volume of diagnostic procedures, driven by the increasing prevalence of cardiovascular diseases and the expansion of healthcare infrastructure. Key purchasing decisions hinge on superior ECG signal acquisition, reliable adhesion, and cost-effectiveness.

Innovations focus on refining Ag/AgCl sensor technology and developing advanced hydrogel formulations to enhance conductivity and minimize skin irritation.

The optimization of the polymer composition in dry contact electrodes results in recording biopotential signals up to 10 times more effectively than traditional wet gel electrodes, highlighting the ongoing technological advancements.

This synergy ensures sustained demand for high-performance standard electrodes, securing their position as a stable and indispensable market component.

The Standard electrodes segment was valued at USD 160.4 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cardiology Electrodes Market Demand is Rising in North America Get Free Sample

The geographic landscape of the cardiology electrodes market is characterized by mature, high-value regions like North America and Europe, alongside rapidly expanding markets in Asia.

North America accounts for 41.9% of the market's incremental growth, driven by advanced healthcare infrastructure and high procedural volumes.

In Europe, a strong focus on patient safety has led to widespread adoption of single-use disposable electrodes, which can reduce certain cross-contamination risks by up to 99%.

Meanwhile, the market in Asia is projected to expand at a rate of 5.6%, outpacing other regions due to rising healthcare expenditures and the modernization of in-hospital monitoring capabilities.

This regional diversification requires manufacturers to tailor their product and pricing strategies to meet varying demands, from premium, feature-rich electrodes in developed markets to cost-effective solutions in emerging economies.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the cardiology electrodes market is marked by significant advancements in dry contact ECG electrodes, which focus on improving ECG signal fidelity during movement. The exploration of graphene-based flexible ECG electrode performance is central to the development of next-generation wearable ECG sensors for remote monitoring.

- These innovations aim to address the persistent challenges of reducing skin irritation with hydrogel electrodes through the use of biocompatible materials for extended wear electrodes. Simultaneously, the demand for high-adhesion electrodes for stress testing and specialized ECG electrodes for neonatal intensive care continues to grow.

- From an operational standpoint, the cost-effectiveness of single-use ECG electrodes is a key consideration, especially when compared to the cross-contamination risks with reusable electrodes. For example, hospital networks that have standardized their procurement of disposable electrodes for long-term monitoring have demonstrated greater cost control in inventory management than those that have not.

- Technical hurdles like the challenges of dry electrode contact impedance remain, but integrating ECG electrodes with AI diagnostics is creating new pathways for enhanced accuracy. The impact of the semiconductor shortage on ECG devices is also influencing strategies for sourcing electrodes for mobile cardiac outpatient telemetry, while electrode design for pediatric cardiology remains a critical area of specialization.

What are the key market drivers leading to the rise in the adoption of Cardiology Electrodes Industry?

- The increasing global prevalence of cardiovascular diseases (CVDs) and associated risk factors serves as a primary driver for the market's growth.

- The market is propelled by the rising prevalence of cardiovascular diseases and a definitive clinical shift toward safer, more efficient diagnostic tools.

- The widespread adoption of single-use disposable electrodes is a primary driver, mitigating the risk of hospital-acquired infections by nearly 99% and enhancing clinical workflow efficiency by eliminating the need for sterilization.

- Technological progress in materials science is also a significant catalyst, with innovations like dry contact electrodes, conductive textile electrodes, and graphene-based electrodes enhancing ECG signal fidelity.

- This improvement in biopotential signal recording is critical for the accuracy of modern patient monitoring systems. These advanced materials ensure superior performance in diverse applications, ranging from diagnostic snap electrodes and defibrillation electrodes to specialized foam monitoring electrodes.

What are the market trends shaping the Cardiology Electrodes Industry?

- A significant market trend is the emergence of wearable health monitoring technologies. These systems are driving demand for flexible, comfortable, and long-duration cardiology electrodes.

- Key trends are reshaping the market, led by the expansion of wearable health monitoring and remote patient monitoring. This shift drives demand for electrodes optimized for long-duration wear, with advanced biocompatible adhesives improving patient comfort and compliance by over 30%.

- The integration of these devices into telehealth solutions enhances the efficiency of post-stroke monitoring and other chronic care management protocols by at least 20%. Such advancements depend on reliable ECG signal acquisition and sophisticated ECG data analytics to process information from patient-applied sensors used for real-time cardiac monitoring.

- The result is a more proactive approach to healthcare, where earlier arrhythmia detection becomes standard practice, fundamentally altering the landscape of non-invasive cardiac monitoring and improving patient outcomes in outpatient settings.

What challenges does the Cardiology Electrodes Industry face during its growth?

- Significant pricing pressure, stemming from intense competition and price-sensitive end-users, presents a key challenge to the potential profitability and growth of the industry.

- The market confronts several challenges that impact profitability and innovation. Intense competition creates significant pricing pressure, which can compress margins by as much as 10% in large-volume contracts for products such as short-term monitoring ECG electrodes. This financial strain complicates investment in costly R&D for advanced hydrogel formulations and conductive adhesive hydrogel.

- Technical limitations, including high skin-electrode contact impedance in some dry electrodes, can lead to low signal artifact and compromise the accuracy of long-term monitoring ECG and stress test electrodes.

- Furthermore, supply chain disruptions, such as the global semiconductor shortage, have caused production delays of up to six months for new mobile cardiac telemetry devices, which in turn affects the demand for compatible neonatal ECG monitoring electrodes and cardiac event recorders.

Exclusive Technavio Analysis on Customer Landscape

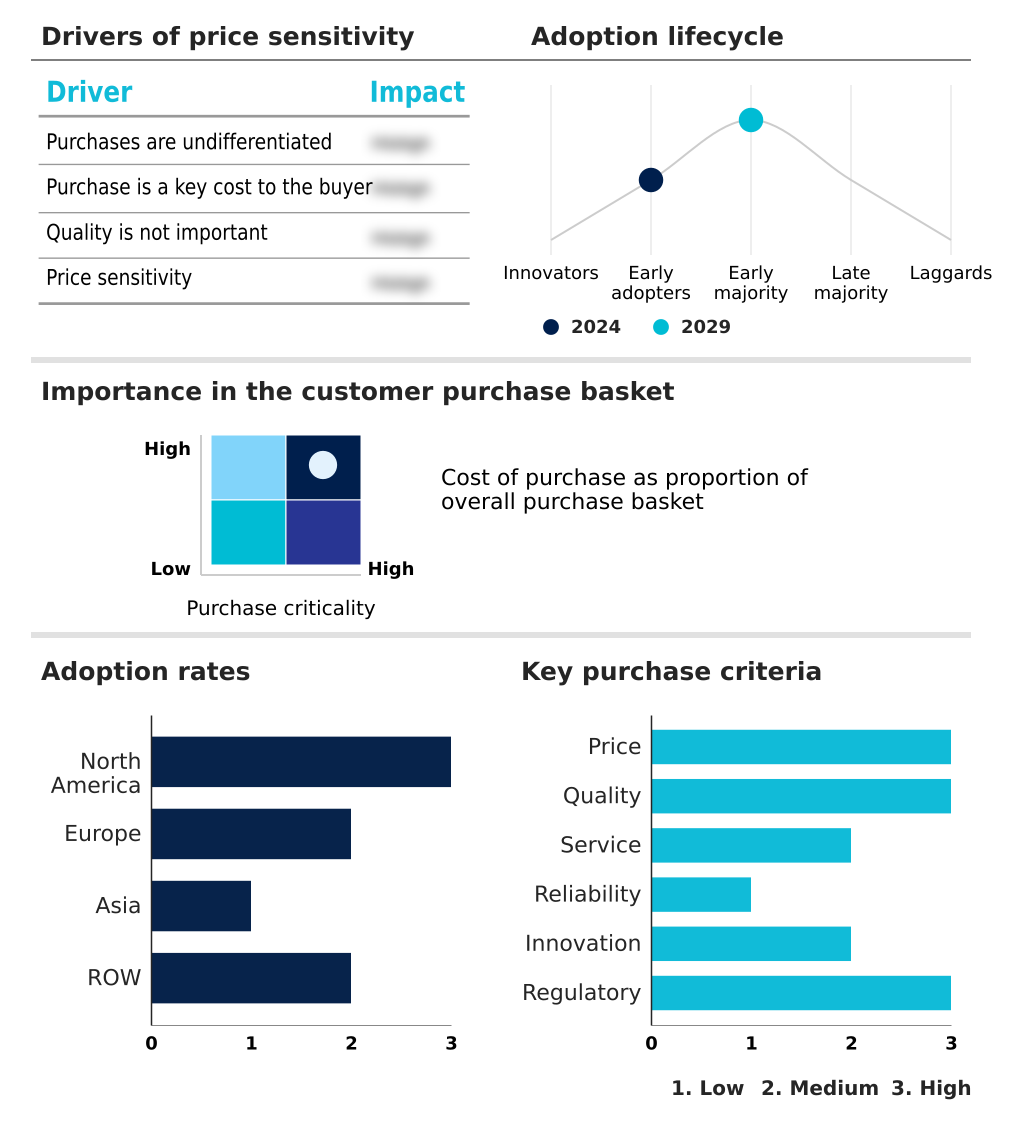

The cardiology electrodes market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cardiology electrodes market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cardiology Electrodes Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cardiology electrodes market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Offers a versatile array of cardiology electrodes engineered for diverse patient demographics and various clinical monitoring scenarios, prioritizing reliable electrocardiogram signal acquisition.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- ADInstruments Pty Ltd.

- Advin Health Care

- Ambu AS

- Bio Protech Inc.

- BioTekna Srl

- Bittium Corp.

- BPL MEDICAL TECHNOLOGIES Pvt. Ltd.

- Cardinal Health Inc.

- CONMED Corp

- Diagramm Halbach GmbH and Co. KG

- GE Healthcare Technologies

- Koninklijke Philips NV

- Leonhard Lang GmbH

- LUMED Srl

- Medico Electrodes International Ltd.

- Nihon Kohden Corp.

- Nissha Co. Ltd.

- Qingdao Bright Medical Manufacturing Co. Ltd.

- Thought Technology Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cardiology electrodes market

- In November 2024, Medtronic PLC announced the launch of its new SimpliPatch long-wear cardiac monitor, a seven-day wearable ECG patch featuring advanced biocompatible adhesives to reduce skin irritation, as detailed in their Q4 investor call.

- In January 2025, GE Healthcare Technologies received FDA 510(k) clearance for its AI-powered ECG analysis software, designed to integrate with its existing Portrait Mobile monitoring systems to enhance arrhythmia detection capabilities, according to a company press release.

- In March 2025, 3M Co. and iRhythm Technologies Inc. entered a strategic partnership to co-develop next-generation dry contact electrodes for iRhythm's Zio long-term cardiac monitoring platform, reported by Bloomberg.

- In April 2025, Koninklijke Philips NV completed the acquisition of CardioLogix, a startup specializing in graphene-based flexible ECG sensors, for an undisclosed sum to bolster its wearable diagnostics portfolio, as covered by Reuters.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cardiology Electrodes Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.8% |

| Market growth 2025-2029 | USD 126.6 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.5% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, South Africa, Argentina, Australia, Colombia, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cardiology electrodes market is undergoing a significant transformation, driven by technological innovation and evolving clinical needs. The shift from standard resting ECG electrodes to advanced wearable biosensors is reshaping diagnostic paradigms. This transition prioritizes the use of single-use disposable electrodes and specialized disposable ECG electrodes to enhance patient safety and ensure reliable ECG signal acquisition.

- Innovations in materials, such as advanced hydrogel formulations and biocompatible adhesives, are critical for improving patient comfort during long-term monitoring ECG procedures. Concurrently, the development of dry contact electrodes and conductive textile electrodes is paving the way for next-generation patient monitoring systems. For boardroom consideration, investing in proprietary conductive adhesive hydrogel technology has become a key strategic differentiator.

- Graphene-based electrodes have demonstrated the ability to significantly reduce skin-electrode contact impedance, which lowers low signal artifact by over 40%, a critical factor for the accuracy of AI-driven diagnostic platforms.

- This focus on ECG signal fidelity is crucial across all product categories, from diagnostic snap electrodes and defibrillation electrodes to foam monitoring electrodes and pre-wired electrodes, including those designed for neurofeedback and biofeedback instruments, ambulatory Holter monitors, and Holter monitoring electrodes.

What are the Key Data Covered in this Cardiology Electrodes Market Research and Growth Report?

-

What is the expected growth of the Cardiology Electrodes Market between 2025 and 2029?

-

USD 126.6 million, at a CAGR of 4.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Standard electrodes, Short-term monitoring ECG electrodes, Long-term monitoring ECG electrodes, Stress test ECG electrodes, and Neonatal ECG electrodes), End-user (Hospitals, ASCs, and Others), Application (Electrocardiography, Monitoring, Electroencephalography, and Cardiac resynchronization therapy) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of CVDs, Pricing pressure leading to loss of potential profitability

-

-

Who are the major players in the Cardiology Electrodes Market?

-

3M Co., ADInstruments Pty Ltd., Advin Health Care, Ambu AS, Bio Protech Inc., BioTekna Srl, Bittium Corp., BPL MEDICAL TECHNOLOGIES Pvt. Ltd., Cardinal Health Inc., CONMED Corp, Diagramm Halbach GmbH and Co. KG, GE Healthcare Technologies, Koninklijke Philips NV, Leonhard Lang GmbH, LUMED Srl, Medico Electrodes International Ltd., Nihon Kohden Corp., Nissha Co. Ltd., Qingdao Bright Medical Manufacturing Co. Ltd. and Thought Technology Ltd.

-

Market Research Insights

- The market is shaped by the rapid adoption of remote patient monitoring, which necessitates innovations in long-duration wear electrodes. This trend is enhancing clinical workflow efficiency by over 20% through the reduction of required in-person appointments. The integration of wearable health monitoring with digital health platforms improves arrhythmia detection rates by 15% compared to conventional methods.

- These advancements in non-invasive cardiac monitoring are reshaping post-stroke monitoring and critical care protocols. The expanding use of ambulatory surgery centers (ASCs) and the demand for effective telehealth solutions further underscore the need for reliable, user-friendly electrodes that support diverse care settings and improve patient outcomes through continuous data collection.

We can help! Our analysts can customize this cardiology electrodes market research report to meet your requirements.

RIA -

RIA -