Chronic Kidney Disease (CKD) Drugs Market Size 2025-2029

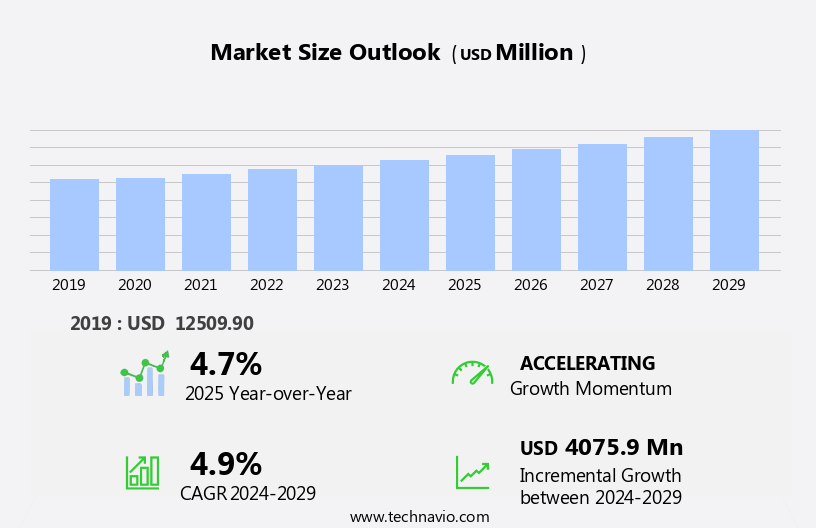

The chronic kidney disease (CKD) drugs market size is forecast to increase by USD 4.08 billion at a CAGR of 4.9% between 2024 and 2029.

- The market is experiencing significant growth due to the rising prevalence of CKD worldwide. This increasing burden of the disease is driving the demand for effective treatment options. The market is further driven by the growing number of drug approvals for CKD treatment, providing pharmaceutical companies with new opportunities to innovate and expand their offerings. Telehealth disparities and access to care remain challenges, with palliative care, support groups, and public awareness initiatives essential for improving patient quality of life. However, the high costs associated with CKD treatment pose a significant challenge for both patients and healthcare systems. This financial burden may limit access to care for some patients and create a need for more affordable treatment options.

- Additionally, collaboration with healthcare providers and payers can help to address the financial challenges and ensure broad patient access to CKD treatments. Overall, the CKD drugs market holds great potential for growth, but companies must navigate the financial obstacles to effectively meet the needs of patients and healthcare systems. Pharmaceutical companies seeking to capitalize on market opportunities must focus on developing cost-effective solutions while maintaining therapeutic efficacy. Precision medicine, early detection, and personalized treatment approaches are gaining traction, with genetic testing and disease management programs paving the way for more effective interventions.

What will be the Size of the Chronic Kidney Disease (CKD) Drugs Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market exhibits dynamic trends, with a focus on addressing various complications. Diabetic nephropathy and hypertensive nephropathy are major causes of CKD, driving demand for contrast agents to aid in diagnosis and imaging. Vitamin D supplements and phosphorus restriction are essential for managing renal tubular acidosis. Kidney recipients require erythropoiesis-stimulating agents and immunosuppressive therapy, while potential donors undergo sodium and potassium restriction.

- Nephrotoxic drugs and interstitial nephritis pose challenges, necessitating careful monitoring and management. Calcium and iron supplements are crucial for maintaining bone health and addressing anemia, respectively. Market players innovate to cater to diverse patient needs, incorporating dietary modifications and addressing nephrotoxicity. The rising popularity of herbal supplements and the development of monoclonal antibodies are contributing to treatment options.

How is this Chronic Kidney Disease (CKD) Drugs Industry segmented?

The chronic kidney disease (CKD) drugs industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Drug Class

- Erythropoietin stimulating agents

- Calcium channel blockers

- Phosphate binders

- ACE inhibitors

- Others

- Route Of Administration

- Oral

- Subcutaneous

- Intravenous

- Distribution Channel

- Offline

- Online

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Drug Class Insights

The erythropoietin stimulating agents segment is estimated to witness significant growth during the forecast period. In the complex landscape of Chronic Kidney Disease (CKD) treatment, erythropoietin stimulating agents (ESAs) play a pivotal role in managing anemia, a common complication arising from impaired kidney function. ESAs, such as epoetin alfa and darbepoetin alfa, mimic the function of endogenous erythropoietin, a hormone naturally produced by the kidneys to stimulate red blood cell production in the bone marrow. With CKD patients experiencing a diminished ability to produce erythropoietin, anemia ensues, leading to debilitating symptoms like fatigue and decreased oxygen-carrying capacity in the blood. ESAs address this issue by stimulating the bone marrow to produce more red blood cells, thereby improving hemoglobin levels and alleviating anemia-related symptoms.

Personalized medicine and precision medicine approaches are increasingly being employed to optimize ESAs' efficacy and safety, with genetic testing playing a crucial role in determining the most suitable treatment regimen for individual patients. Drug safety remains a significant concern, with vascular calcification and drug interactions being potential complications. Early detection and timely intervention are essential to mitigate disease progression and improve the quality of life for CKD patients. Access to care is a critical issue, with home dialysis and peritoneal dialysis gaining popularity as alternatives to traditional dialysis centers. Renal pathologists and kidney function tests are integral to diagnosing and monitoring CKD, while patient education and support groups are vital in promoting adherence to treatment plans and managing the emotional and psychological aspects of living with the disease.

Regulatory approval, cost-effectiveness analysis, and healthcare infrastructure are essential factors influencing the market dynamics of ESAs and other CKD treatments. Creatinine clearance, metabolic acidosis, and bone mineral density are key indicators of kidney function and disease progression. Renin inhibitors and mineralocorticoid receptor antagonists are among the emerging therapies targeting various aspects of CKD management. In the context of CKD treatment, ESAs represent a significant component of the market, with ongoing clinical trials and disease management programs focusing on improving patient outcomes, optimizing treatment strategies, and addressing the unique challenges posed by this complex condition.

_drugs_market_size_abstract_2024_v2.jpg)

The Erythropoietin-stimulating agents segment was valued at USD 4.16 billion in 2019 and showed a gradual increase during the forecast period.

The Chronic Kidney Disease (CKD) Drugs Market continues to grow, addressing critical needs in patient care. Effective fluid restriction plays a key role in managing kidney function, preventing excess fluid buildup. Similarly, sodium restriction is essential to control blood pressure and reduce strain on the kidneys. Patients with CKD often require calcium supplements to maintain bone health, as kidney disease impacts mineral balance. Advances in treatment also support both kidney donors and kidney recipients, ensuring successful transplant outcomes.

Regional Analysis

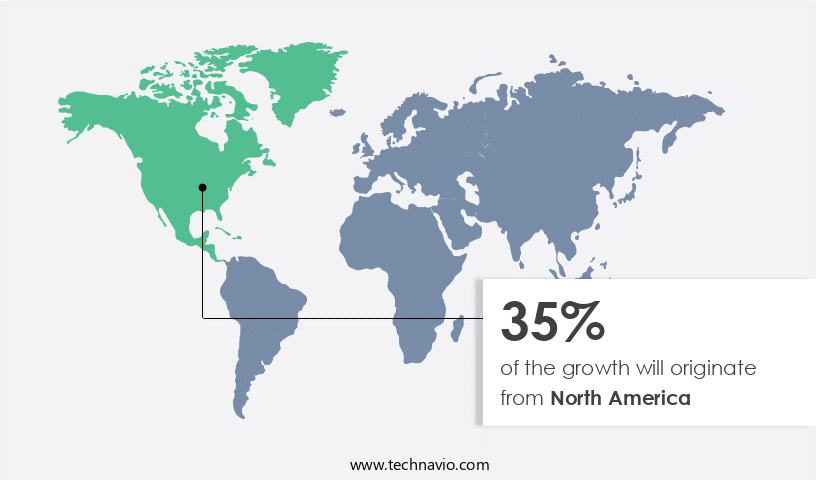

North America is estimated to contribute 35% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America continues to expand due to the region's high prevalence rate and advanced healthcare infrastructure. In 2024, North America accounted for the largest revenue share, with the US and Canada being the major contributors. The US alone had over 30 million adults living with CKD, with a significant number progressing to end-stage kidney disease (ESKD). In Canada, over 49,000 individuals lived with ESKD in 2023, with approximately 29,906 undergoing dialysis and 19,356 living with a functioning kidney transplant. Personalized medicine and precision telemedicine play a crucial role in CKD treatment, with genetic testing and kidney biopsy aiding in early detection and disease progression assessment.

Drug safety remains a top priority, with a focus on minimizing vascular calcification, electrolyte imbalance, and metabolic acidosis. Patient education is essential for improving patient adherence to treatment plans, particularly for home dialysis and peritoneal dialysis. Regulatory approval for new treatments, such as SGLT2 inhibitors and mineralocorticoid receptor antagonists, is driving market growth. The cost-effectiveness analysis of these treatments, along with disease management programs, is crucial for healthcare infrastructure and health economics. Renal pathologists and dialysis centers provide essential services for patients, with dialysis equipment and vascular access playing a significant role in treatment.

Pharmacokinetic studies and clinical trials are ongoing to develop new treatments and improve existing ones, while regulatory bodies ensure their safety and efficacy. The market also faces challenges such as drug interactions, kidney function tests, and end-of-life care. In summary, the CKD drugs market in North America is driven by the high prevalence rate, advanced healthcare infrastructure, and the presence of leading companies. Personalized medicine, drug safety, and patient education are key focus areas, with regulatory approval, cost-effectiveness, and healthcare infrastructure also playing significant roles. Challenges include health disparities, access to care, and the complexities of treating CKD.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Chronic Kidney Disease (CKD) Drugs market drivers leading to the rise in the adoption of Industry?

- The global rise in the prevalence of chronic kidney disease (CKD) serves as the primary driver for the market's growth. Chronic Kidney Disease (CKD) is a significant health concern worldwide, affecting approximately 8.5-9.5% of the adult population. Diabetes, hypertension, vascular disease, and glomerulonephritis are the primary causes of CKD. In developing countries, infections leading to glomerulonephritis and interstitial nephritis are the major contributors to the disease. CKD can lead to complications such as electrolyte imbalance, requiring patient education on diet and medication adherence.

- Bone mineral density may be affected due to kidney function loss, and regulatory approval is required for certain treatments. Ensuring patient adherence to treatment plans and regular check-ups is crucial for managing CKD effectively. In advanced stages, patients may undergo kidney biopsy for diagnosis and renal pathologist evaluation. Home dialysis, including hemodialysis and peritoneal dialysis, is an option for some patients, necessitating the use of dialysis equipment and vascular access.

What are the Chronic Kidney Disease (CKD) Drugs market trends shaping the Industry?

- The increasing approval of drugs for the treatment of chronic kidney disease (CKD) represents a significant market trend. This trend reflects the growing demand for effective solutions to manage CKD and improve patient outcomes. Chronic Kidney Disease (CKD) is a global health issue with significant unmet medical needs. Pharmaceutical companies are advancing research and development efforts, leading to the identification and approval of new drugs for CKD treatment. Regulatory agencies, including the FDA, are prioritizing the approval of drugs addressing CKD, given its impact on health disparities and the need for effective treatment options. For instance, Boehringer Ingelheim and Eli Lilly and Company's Jardiance (empagliflozin) tablets, under investigation as a potential treatment to reduce the risk of kidney disease progression and cardiovascular disease-related death in adults with CKD, recently had an sNDA accepted by the FDA in January 2023.

- Health economics, metabolic acidosis, and drug interactions are crucial factors influencing the CKD drugs market. Palliative care, support groups, kidney transplantation, and dialysis centers are essential aspects of CKD management. Pharmacokinetic studies are ongoing to optimize drug efficacy and minimize side effects. Renin inhibitors, among other drug classes, are gaining attention due to their potential benefits in managing CKD. Public awareness campaigns and education are vital in addressing the challenges associated with CKD, including its complications and available treatment options.

How does Chronic Kidney Disease (CKD) Drugs market face challenges during its growth?

- The escalating costs linked to the treatment of Chronic Kidney Disease (CKD) represent a significant challenge impeding the growth of the associated industry. Chronic Kidney Disease (CKD) is a significant healthcare challenge due to its long-term management requirements and high treatment costs. The market for CKD drugs faces substantial financial burdens as patients often need a combination of medications, dialysis, and, in severe cases, kidney transplants. The costs of managing CKD without renal replacement therapy (RRT) for patients in Stages I to II are estimated to be between USD 7,725 and USD 11,879. The expenses escalate substantially for dialysis and kidney transplant procedures, which amount to USD 124,271 and USD 87,538, respectively. Clinical trials and disease management programs play a crucial role in mitigating the progression of CKD.

- SGLT2 inhibitors and mineralocorticoid receptor antagonists are among the medications commonly used for CKD treatment. The cost-effectiveness analysis of these drugs is essential to ensure optimal patient care and healthcare infrastructure sustainability. Kidney function tests are an integral part of CKD diagnosis and monitoring. End-of-life care for CKD patients is another critical aspect of managing this disease. Dialysis solutions are a vital component of end-of-life care for patients with advanced CKD. The healthcare infrastructure must be robust to cater to the diverse needs of CKD patients, from disease management programs to dialysis facilities and kidney transplant centers.

Exclusive Customer Landscape

The chronic kidney disease (CKD) drugs market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the chronic kidney disease (CKD) drugs market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, chronic kidney disease (ckd) drugs market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - This company specializes in the development and commercialization of innovative treatments for chronic kidney disease.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AbbVie Inc.

- Akebia Therapeutics

- Amgen Inc.

- AstraZeneca Plc

- Bayer AG

- Biogen Inc.

- Boehringer Ingelheim International GmbH

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- Horizon Therapeutics Plc

- Johnson and Johnson Services Inc.

- Novartis AG

- OPKO Health Inc.

- Pfizer Inc.

- Rockwell Medical Inc.

- Sanofi SA

- Sun Pharmaceutical Industries Ltd.

- Takeda Pharmaceutical Co. Ltd.

- Zydus Lifesciences Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Chronic Kidney Disease (CKD) Drugs Market

- In January 2024, AstraZeneca and FibroGen announced the US Food and Drug Administration (FDA) approval of their collaborative product, roxadustat, for the treatment of anemia in adult patients with chronic kidney disease (CKD) not on dialysis. This approval marked a significant advancement in the CKD drugs market, as roxadustat is the first orally administered hypoxia-inducible factor prolyl hydroxylase inhibitor approved for this indication (AstraZeneca press release, 2024).

- In March 2024, Amgen and Fresenius Medical Care entered into a strategic partnership to co-develop and commercialize Amgen's investigational drug, evolocumab, for the treatment of cardiovascular disease in patients with CKD. This collaboration aimed to improve patient outcomes and address the high cardiovascular risk associated with CKD (Amgen press release, 2024).

- In May 2024, Fresenius Medical Care, a leading provider of dialysis services and products, acquired NxStage Medical, a pioneer in home hemodialysis, for approximately USD1.7 billion. This acquisition expanded Fresenius Medical Care's home dialysis offerings and strengthened its position in the CKD market (Fresenius Medical Care press release, 2024).

- In April 2025, the European Commission approved AstraZeneca's drug, faricimab, for the treatment of patients with neovascular (wet) age-related macular degeneration and diabetic macular edema. Although not directly related to CKD, faricimab is notable because it is also indicated for patients with CKD and diabetic nephropathy, expanding the therapeutic options for this patient population (AstraZeneca press release, 2025).

Research Analyst Overview

The chronic kidney disease (CKD) market continues to evolve, shaped by various dynamics and applications across diverse sectors. Metabolic acidosis, a common complication in CKD, necessitates ongoing research for effective treatment options. Health disparities persist, highlighting the need for targeted interventions and improved access to care. Renin inhibitors, a potential treatment for CKD, are under investigation for their role in disease progression. Health economics and cost-effectiveness analysis are crucial considerations in the development and implementation of CKD therapies. Palliative care and support groups play essential roles in enhancing the quality of life for patients. Drug interactions and electrolyte imbalances pose significant challenges, necessitating rigorous pharmacokinetic studies and patient education.

Kidney transplantation and dialysis centers remain key components of CKD care, with ongoing advancements in dialysis equipment and vascular access. Public awareness campaigns and disease management programs aim to facilitate early detection and improve patient adherence. Precision medicine and personalized approaches to care are gaining traction, with genetic testing and SGLT2 inhibitors offering promising avenues for treatment. Regulatory approval processes and healthcare infrastructure developments continue to shape the CKD market. Mineralocorticoid receptor antagonists and disease progression studies are among the ongoing research areas. The ongoing unfolding of market activities underscores the continuous need for innovation and adaptation in the CKD landscape. The high costs associated with CKD treatment necessitate a comprehensive understanding of the disease, its progression, and available treatment options. The role of clinical trials, disease management programs, cost-effectiveness analysis, kidney function tests, and end-of-life care in managing CKD is essential to ensure optimal patient outcomes and healthcare infrastructure sustainability.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Chronic Kidney Disease (CKD) Drugs Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

228 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.9% |

|

Market growth 2025-2029 |

USD 4.08 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.7 |

|

Key countries |

US, China, Germany, Canada, India, UK, France, Japan, Brazil, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Chronic Kidney Disease (CKD) Drugs Market Research and Growth Report?

- CAGR of the Chronic Kidney Disease (CKD) Drugs industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the chronic kidney disease (ckd) drugs market growth of industry companies

We can help! Our analysts can customize this chronic kidney disease (ckd) drugs market research report to meet your requirements.

RIA -

RIA -