Contactors Market Size 2024-2028

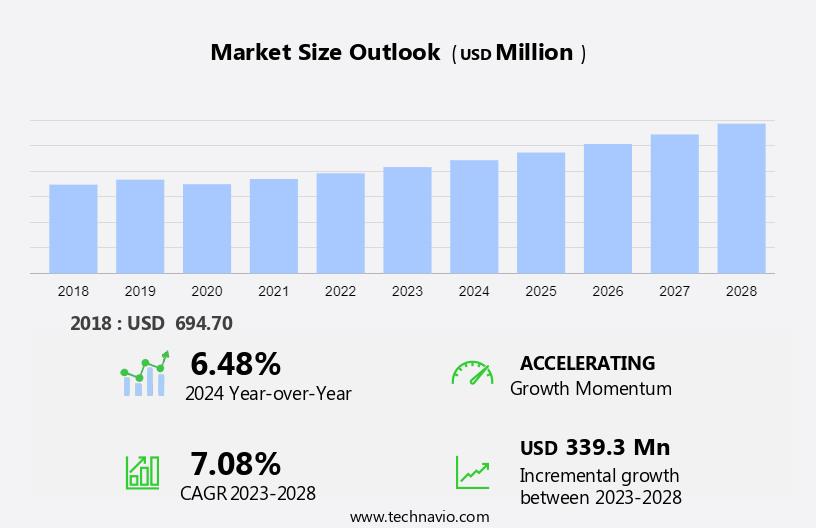

The contactors market size is forecast to increase by USD 339.3 million at a CAGR of 7.08% between 2023 and 2028. The market is experiencing significant growth, driven by the increasing demand for motor protection devices in various industries. This trend is fueled by the need for efficient and reliable power management systems. Exports of contactors and related components, such as gigabit fiber optics, solid state relays, cranes, magnet controllers, starters, mill auxiliary controllers, and solid state drives, contribute significantly to the global economy. Another emerging trend is the development of miniature and auxiliary contactors, which offer enhanced functionality and compact size, making them ideal for use in space-constrained applications. However, the market faces challenges due to the technical limitations of contactors, including their susceptibility to electrical arcing and the need for regular maintenance. Despite these challenges, the market is expected to continue growing, driven by advancements in technology and increasing demand for automation and energy efficiency.

Contactors are essential electrical switching devices that play a crucial role in various applications, including HVAC systems, electric vehicles (EVs) and hybrid electric vehicles (HEVs), renewable energy projects, and grid infrastructure. These electrical sources are connected to a load through contactors, which act as intermediaries, ensuring the safe and reliable transfer of electricity. In HVAC systems, contactors control the operation of compressors and fans. In the automotive industry, they are used in EVs and HEVs for battery management systems and other electrical functions. Renewable energy projects, such as solar energy, rely on contactors to connect the solar panels to the electrical grid.

Government bodies and automotive manufacturers are emphasizing safety and reliability in their projects, leading to an increased demand for high-quality contractors. The market for contactors is segmented into power contactors, DC contactors, and auxiliary contactors. Spring-loaded contactors are commonly used in residential and commercial settings, while industrial settings require heavy-duty contactors for larger loads. Data centers and industrial automation applications use DC contactors to manage power distribution. Safety and reliability are essential factors in the design and manufacturing of contactors. Electrical terminals and renewable energy sources are also important considerations in the market. The market is expected to grow significantly in the coming years due to the increasing demand for electricity and the shift towards renewable energy sources.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

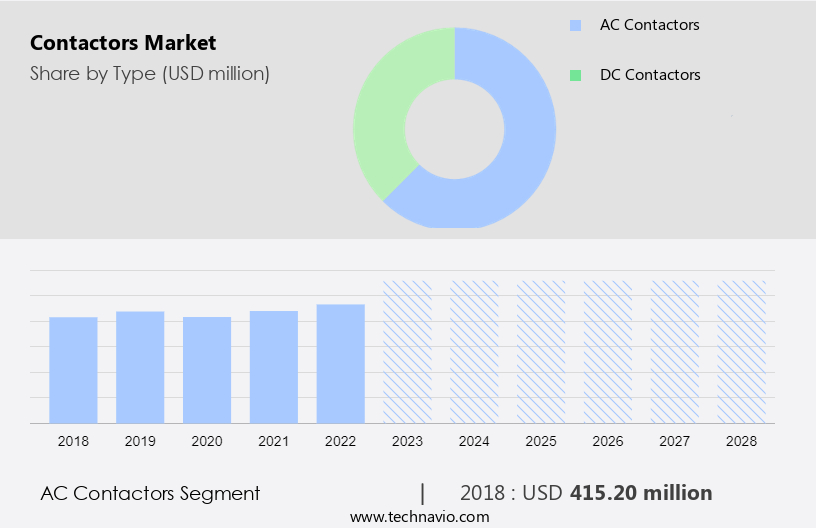

- AC contactors

- DC contactors

- End-user

- Residential

- Commercial

- Industrial

- Geography

- APAC

- China

- Europe

- Germany

- UK

- North America

- Canada

- US

- Middle East and Africa

- South America

- APAC

By Type Insights

The AC contactors segment is estimated to witness significant growth during the forecast period. In the realm of power distribution and control systems, AC contactors hold a pivotal position, particularly in industrial settings. These components are essential for managing electrical current flow in various applications, including HVAC systems, lighting, and motor control circuits. The expanding infrastructure of residential buildings, such as apartments and houses, necessitates the use of affordable residential units equipped with electrical distribution and power regulation systems, further fueling the demand for AC contactors. Moreover, commercial establishments like office buildings, shopping malls, hotels, hospitals, elevators, and escalators require sophisticated control systems, which in turn necessitate the use of advanced AC contactors for power switching and motor control.

The industrial sector's growth, driven by manufacturing plants, factories, warehouses, machinery, and manufacturing capabilities, also contributes significantly to the market's expansion. Additionally, AC contactors find extensive applications in specialized industries such as aerospace, automotive, and even space-based manufacturing, where precise torque control is essential. The rise of solid-state relays, starters, mill auxiliary controllers, and solid-state drives further expands the market's scope. Furthermore, the increasing demand for energy efficiency and automation solutions in various industries propels the adoption of AC contactors in data centers, DC contactors, cranes, steel mills, and magnet controllers. The growing popularity of electric vehicles (EVs) also presents a significant opportunity for AC contactors in the automotive sector.

Get a glance at the market share of various segments Request Free Sample

The AC contactors segment accounted for USD 415.20 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

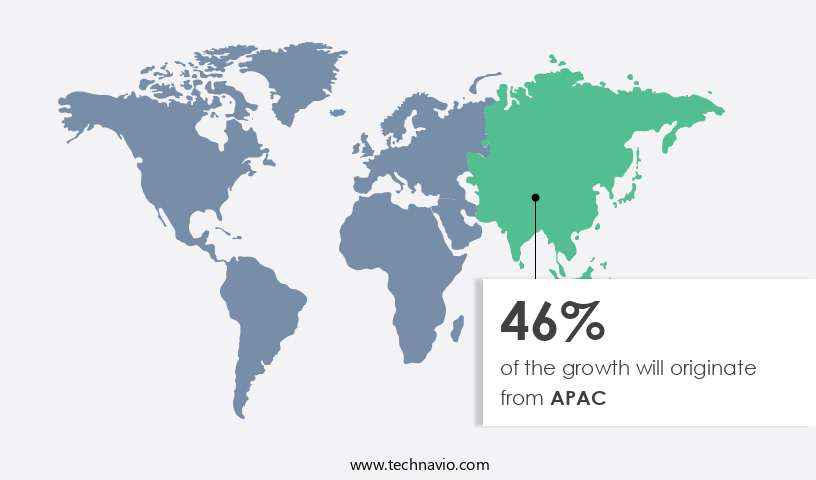

APAC is estimated to contribute 46% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

In industrial settings, contactors play a crucial role in power distribution and control systems. These components are essential for infrastructure expansion, managing motor control circuits in various applications such as lighting systems, HVAC systems, and electrical distribution in residential buildings, including apartments, houses, and affordable residential units. In commercial establishments, contactors are used in office buildings, shopping malls, hotels, hospitals, elevators, escalators, and security systems, ensuring reliable power regulation for household applications and heavy-duty machinery. Contactors are also integral to the manufacturing sector, powering manufacturing capabilities in industrial buildings, manufacturing plants, factories, warehouses, and machinery. Data centers and DC contactors are other major applications for contactors, ensuring efficient power management and reliability.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Growing demand for motor protection devices is the key driver of the market. In the realm of industrial automation, contactors play a crucial role in ensuring safety and reliability by managing the electrical power supply to industrial motors. The increasing adoption of drives and motor control systems in various industries, driven by the need for continuous device monitoring to prevent productivity losses, has led to a higher demand for contactors. These components help protect electrical motors from potential damage caused by high voltage and current fluctuations. In the context of renewable energy sources and grid infrastructure, contactors are essential for energy projects involving battery management systems, the Internet of Things, smart cities, transportation networks, power grids, and smart grids. Furthermore, contactors are vital for commercial vehicles, such as buses, trucks, and passenger cars, to ensure optimal performance and prevent costly faults in motors and transmission lines.

Market Trends

The emergence of miniature and auxiliary contactors is the upcoming trend in the market. Miniature contactors play a crucial role in industrial automation by enabling remote control and protection of electrical motors and loads. These compact components are particularly valuable in applications with limited space, such as those found in renewable energy sources, grid infrastructure, and energy projects. Miniature contactors are also essential in battery management systems, IoT applications, smart cities, transportation networks, power grids, and smart grids. Auxiliary contactors, a type of miniature contactor, serve to protect control circuits by acting as helpers to the main contactor. These mechanically operated switches ensure the safety and reliability of various systems, including those used in commercial vehicles like buses, trucks, and passenger cars.

Market Challenge

Technical limitations of contactors is a key challenge affecting the market growth. The market plays a significant role in industrial automation, particularly in ensuring safety and reliability in various applications. These components are integral to the functioning of electrical terminals in renewable energy sources, grid infrastructure, energy projects, battery management systems, and various types of transportation networks, including buses, trucks, and passenger cars. However, contactors face operational and technical challenges that can hinder their performance and longevity. Temperature is a critical factor that impacts the lifespan of contactors. For every 10 degree C increase in temperature, the insulation material's lifespan is reduced by half. Coil windings are another issue, as the small diameter of the wire makes it susceptible to chemical seepage.

Magnet systems are also prone to failure due to their complex nature. In the context of the growing adoption of smart cities, smart grids, power grids, energy management systems, and Internet of Things (IoT) technologies, the demand for contactors is increasing. Despite these opportunities, addressing the operational and technical challenges is essential to ensure the reliability and efficiency of contactors in various applications.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

ABB Ltd. - The company offers the ACS800, the ACS550, and the ACS380.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMETEK Inc.

- Danfoss AS

- Eaton Corp. Plc

- Furukawa Electric Co. Ltd.

- HIMEL Hong Kong LTD.

- Hubbell Inc.

- ISKRA elektro in sistemske resitve d.o.o

- Kohler Co.

- Kunshan GuoLi Electronic Technology Co. Ltd.

- Legrand SA

- LOVATO Electric Spa

- LS ELECTRIC Co. Ltd.

- Mitsubishi Electric Corp.

- Rockwell Automation Inc.

- Sassin International Electric Shanghai Co. Ltd.

- Schaltbau Holding AG

- Schneider Electric SE

- Siemens AG

- Zhejiang CHINT Electrics Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Contactors are essential electrical switching devices that play a crucial role in various industries, including HVAC systems, automobiles, aerospace and defense, and power generation. In the context of renewable energy, contactors are extensively used in solar energy projects, such as PV plants, to manage the flow of electricity from the PV strings to the power distribution network. The growing adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs) is fueling the demand for contactors in the automotive sector. Government bodies and automotive manufacturers are investing heavily in the development of zero-emission vehicles, leading to an increase in the production of EVs and HEVs.

Moreover, contactors are also used in various other applications, such as power transmission, medical diagnosis, wind power, energy management, building technologies, process industries, healthcare, financial services, and more. The electrical power circuit requires contactors to switch between the electrical source and the load, ensuring efficient power distribution. The market for contactors is segmented into AC and DC contractors, with AC contractors holding a larger market share due to their extensive use in various industries. Spring-loaded contractors and auxiliary contactors are other types of contactors that find applications in residential and commercial settings. The future of the market looks promising, with the increasing focus on energy efficiency and the growing adoption of renewable energy sources.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.08% |

|

Market growth 2024-2028 |

USD 339.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.48 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 46% |

|

Key countries |

China, US, Germany, UK, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ABB Ltd., AMETEK Inc., Danfoss AS, Eaton Corp. Plc, Furukawa Electric Co. Ltd., HIMEL Hong Kong LTD., Hubbell Inc., ISKRA elektro in sistemske resitve d.o.o, Kohler Co., Kunshan GuoLi Electronic Technology Co. Ltd., Legrand SA, LOVATO Electric Spa, LS ELECTRIC Co. Ltd., Mitsubishi Electric Corp., Rockwell Automation Inc., Sassin International Electric Shanghai Co. Ltd., Schaltbau Holding AG, Schneider Electric SE, Siemens AG, and Zhejiang CHINT Electrics Co. Ltd. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -