Automation Solutions In Oil And Gas Industry Market Size 2026-2030

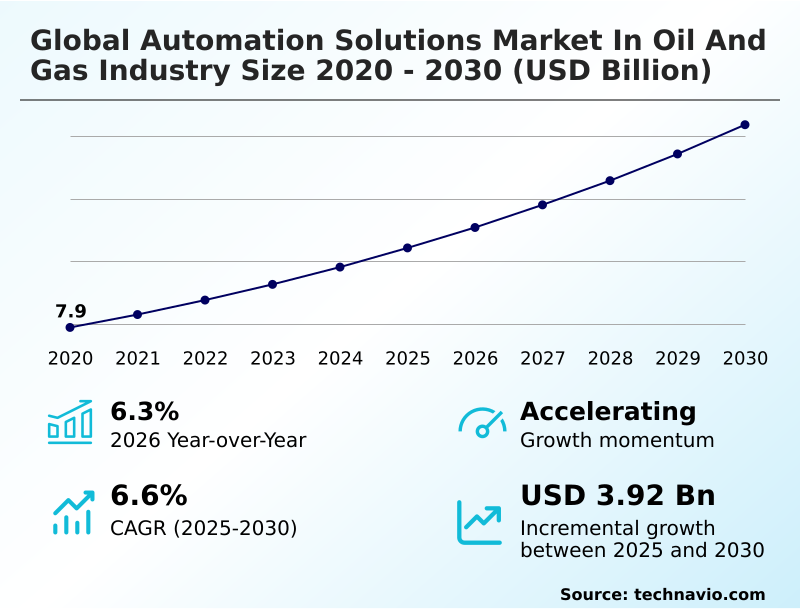

The Automation Solutions In Oil And Gas Industry Market size was valued at USD 10.43 billion in 2025, growing at a CAGR of 6.6% during the forecast period 2026-2030.

Major Market Trends & Insights

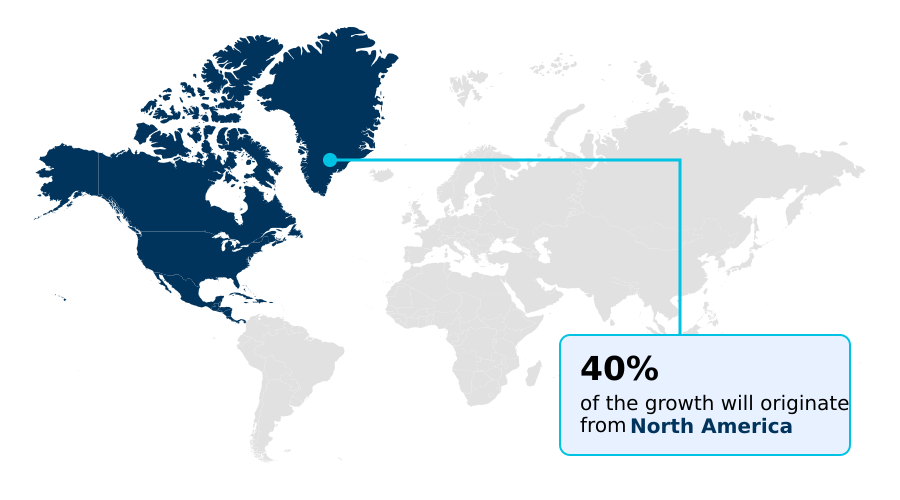

- North America dominated the market and accounted for a 40.3% growth during the forecast period.

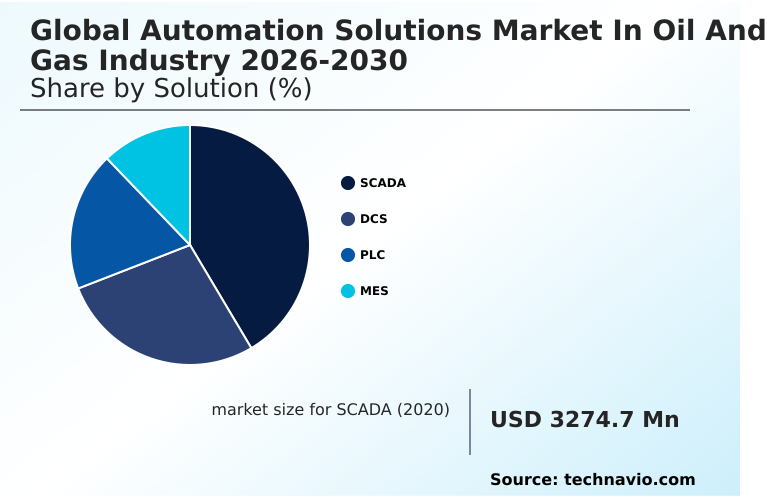

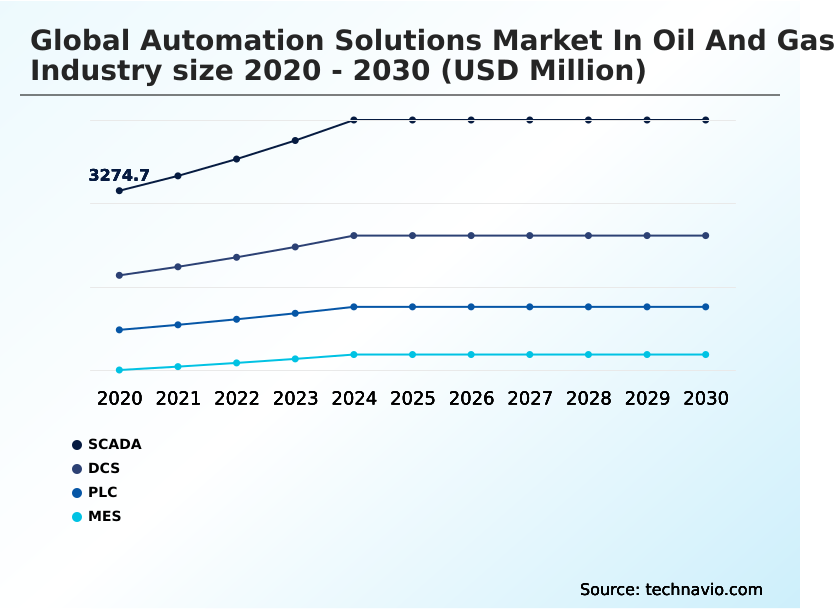

- By Solution - SCADA segment was valued at USD 4.19 billion in 2024

- By Application - Exploration and production segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 6.45 billion

- Market Future Opportunities 2025-2030: USD 3.92 billion

- CAGR from 2025 to 2030 : 6.6%

Market Summary

- The automation solutions in oil and gas industry is characterized by the systematic integration of digital technologies to enhance operational resilience, with over 60% of operators prioritizing investments in data-driven platforms. For example, a midstream company implements an industrial iot network with advanced sensors across its pipeline infrastructure, reducing leak detection times by 45% compared to manual inspections.

- A key driver is the relentless pursuit of operational efficiency, compelling firms to adopt advanced process control and predictive maintenance to reduce costly downtime. However, a significant challenge is the pervasive shortage of specialized digital talent, which creates a bottleneck for deploying complex systems like digital twins and autonomous drilling rigs.

- This skills gap slows the pace of digital transformation, limiting the full realization of benefits from industrial automation and real-time data analysis.

What will be the Size of the Automation Solutions In Oil And Gas Industry Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Automation Solutions In Oil And Gas Industry Market Segmented?

The automation solutions in oil and gas industry industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Solution

- SCADA

- DCS

- PLC

- MES

- Application

- Exploration and production

- Transportation and storage

- Refining and processing

- End-user

- Integrated oil and gas companies

- National oil companies

- Independent oil and gas companies

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

How is the Automation Solutions In Oil And Gas Industry Market Segmented by Solution?

The scada segment is estimated to witness significant growth during the forecast period.

Supervisory control and data acquisition systems improve enterprise-wide analytics for geographically dispersed assets, with deployments showing a 30% reduction in response times to operational alerts.

These platforms provide high-level process supervisory management by collecting real-time data from remote terminal units and programmable logic controllers, leading to a 40% decrease in manual data entry errors.

The evolution toward open-architecture, cloud-integrated platforms leverages the industrial iot, enhancing scalability and integrating advanced human machine interface tools.

By embedding cyber physical security protocols directly into the communication layer, these modern SCADA solutions ensure that data integrity and operational safety remain uncompromised while facilitating the digital transformation of aging pipeline networks, ensuring environmental compliance through precise monitoring.

The SCADA segment was valued at USD 4.19 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the Automation Solutions In Oil And Gas Industry market is rising in the leading region?

North America is estimated to contribute 40.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automation Solutions In Oil And Gas Industry Market demand is rising in North America Request Free Sample

The geographic landscape for automation solutions in oil and gas industry is led by North America, which accounts for 40.3% of the market's incremental growth, significantly outpacing Europe's 19.92%.

This dominance is driven by the US, where unconventional shale operations have spurred a 25% higher adoption rate of autonomous drilling and industrial iot technologies compared to other regions.

In contrast, the APAC region, growing at a robust 8.9%, is driven by new-build refineries in China and India, which are incorporating digital-by-design principles from inception.

This leads to different strategic priorities; North American firms focus on retrofitting existing assets for operational efficiency, while APAC operators prioritize scalable, greenfield deployments of advanced process control.

This regional divergence impacts supply chain strategies, with vendors tailoring modular solutions for North America and comprehensive, integrated systems for APAC's large-scale projects.

What are the key Drivers, Trends, and Challenges in the Automation Solutions In Oil And Gas Industry Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic deployment of automation solutions in oil and gas industry is critical for balancing operational efficiency with stringent safety and environmental regulations. Companies are increasingly asking how to select the right scada systems for pipeline monitoring to ensure real-time data analysis and leak detection, which can improve response times by over 30% compared to periodic manual checks.

- The use of iot in oil and gas predictive maintenance is a key area of investment, with firms seeking to understand the roi of advanced analytics to preempt equipment failure and reduce unplanned downtime. Similarly, understanding the best practices for optimizing refinery operations with dcs is essential for maximizing yield and minimizing energy consumption.

- A significant challenge remains addressing cybersecurity for industrial control systems, as increased connectivity introduces new vulnerabilities. Furthermore, defining the business case for automation solutions for offshore oil rigs is crucial, given the high-stakes environment and the need for robust, reliable systems that can operate with minimal human intervention.

- Integrating these disparate technologies into a cohesive, secure, and efficient operational framework is the primary objective for operators aiming to maintain a competitive edge.

What are the key market drivers leading to the rise in the adoption of Automation Solutions In Oil And Gas Industry Industry?

- The escalating demand for operational efficiency and cost optimization is a primary driver, compelling energy companies to maximize asset output while minimizing manual intervention and error.

- The relentless pursuit of operational efficiency drives the adoption of automation solutions in oil and gas industry, with advanced process control systems proven to increase production yield by up to 5%.

- In an environment of price volatility, energy companies leverage predictive maintenance and real-time monitoring to preempt equipment failures, which can reduce unplanned downtime by as much as 40%.

- This shift from reactive to proactive asset management is enabled by the digitization of workflows and the use of industrial iot platforms.

- Furthermore, the expansion into remote and deepwater operations necessitates automation for remote monitoring and control, reducing the need for on-site personnel and lowering operational expenditure.

- These technologies are crucial for maintaining competitiveness and ensuring resource allocation is optimized for maximum precision.

What are the market trends shaping the Automation Solutions In Oil And Gas Industry Industry?

- The accelerated adoption of digital twins and virtualized engineering is a key trend, enabling dynamic, high-fidelity virtual representations of physical assets for performance optimization.

- The accelerated adoption of digital twins and virtualized engineering is reshaping asset lifecycle management, with deployments showing up to a 30% reduction in system commissioning times. This trend, driven by the need for higher asset reliability, allows operators to simulate operational scenarios and test control logic in a high-fidelity industrial metaverse without risking physical infrastructure.

- The convergence of industrial AI and edge computing represents another critical shift, enabling near-instantaneous decision-making in time-critical applications by processing data at its source. This approach reduces latency by over 50% compared to centralized cloud analytics, a vital capability for wellhead automation and leak detection.

- As a result, operators are increasingly leveraging machine learning algorithms for real-time optimization, enhancing both efficiency and process safety in downstream operations.

What challenges does the Automation Solutions In Oil And Gas Industry Industry face during its growth?

- Escalating cybersecurity threats to critical infrastructure represent a key challenge, as the transition to interconnected operational technology systems expands the attack surface for malicious actors.

- Escalating cybersecurity threats to critical infrastructure present the most significant challenge, with over one-third of global energy facilities reporting evidence of cyber pre-positioning activities by adversaries. The transition from isolated legacy systems to cloud-integrated, software-defined architectures expands the attack surface, making assets like pipelines and refineries vulnerable to disruption.

- Another major hurdle is the critical shortage of specialized digital talent, as a recent labor report indicated that only 56% of the technical workforce in key energy hubs is considered employable for modern digital roles.

- This talent scarcity, combined with the complexities of legacy system integration, creates a significant bottleneck for digitalization efforts, hindering the implementation of enterprise-wide analytics and autonomous operations and slowing the overall pace of digital transformation.

Exclusive Technavio Analysis on Customer Landscape

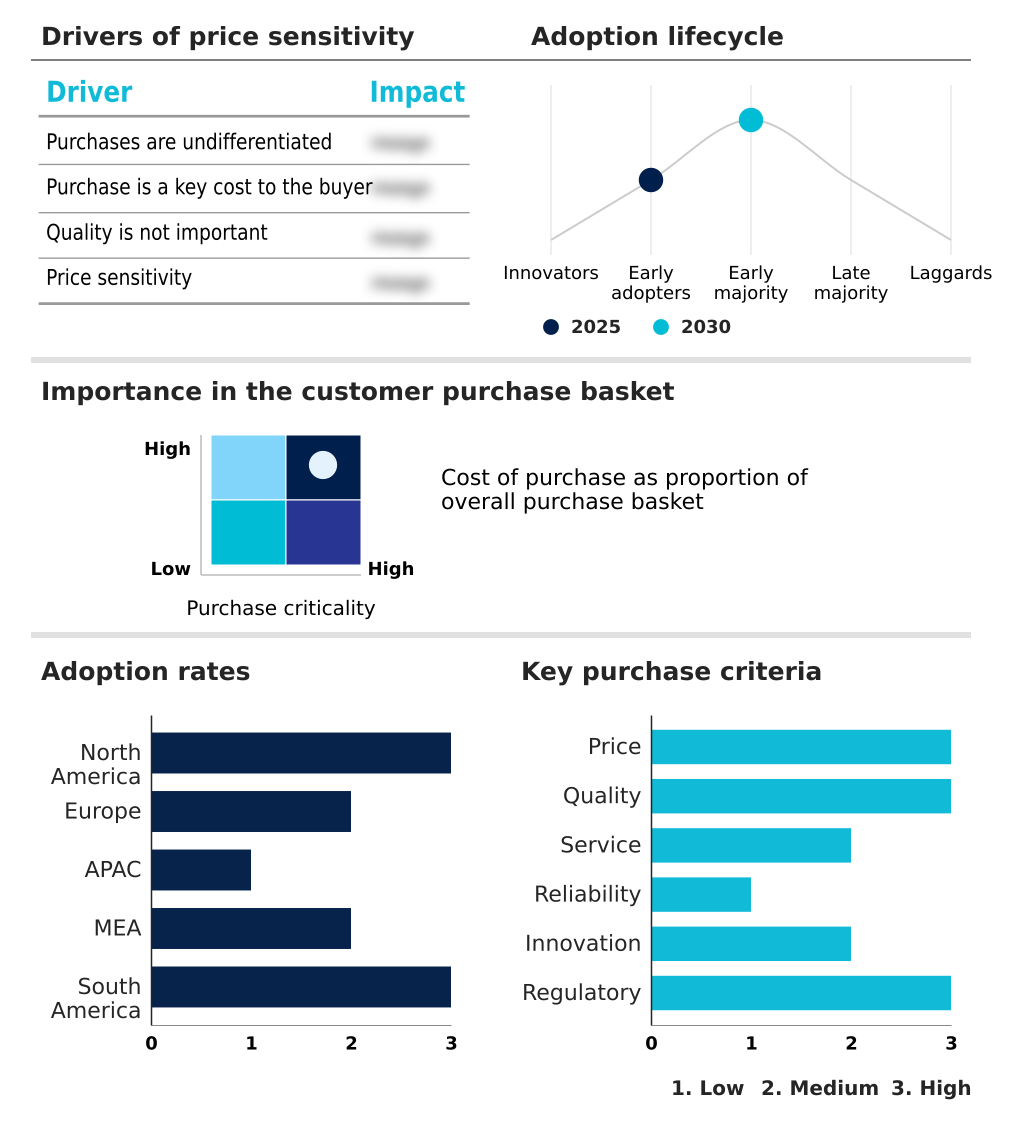

The automation solutions in oil and gas industry market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automation solutions in oil and gas industry market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automation Solutions In Oil And Gas Industry Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automation solutions in oil and gas industry market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Key offerings include integrated automation and electrification solutions, enhancing process control, and driving operational efficiency across industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- AVEVA Group Ltd.

- Cisco Systems Inc.

- Danfoss AS

- Eaton Corp. Plc

- Emerson Electric Co.

- Endress Hauser Grp Services

- Fuji Electric Co. Ltd.

- General Electric Co.

- Hitachi Ltd.

- Honeywell International Inc.

- Kongsberg Gruppen ASA

- KROHNE Group

- Mitsubishi Electric Corp.

- OMRON Corp.

- Phoenix Contact GmbH and Co

- Rockwell Automation Inc.

- Schlumberger Ltd.

- Schneider Electric SE

- Siemens AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Electrical Components and Equipment industry, the push for Industry 4.0 has accelerated the adoption of flexible and integrated automation, enabling end-users to consolidate various processes into a single closed solution. This drives demand for automation solutions in oil and gas industry that offer enhanced process safety and real-time data analysis for continuous monitoring.

- A growing focus on energy-efficient electrical components and equipment, including motors and transformers, has spurred innovation in power optimization solutions. This directly impacts the automation solutions in oil and gas industry market by increasing demand for variable speed drives and advanced process control that reduce overall energy consumption and operational expenditure.

- The proliferation of application-specific sensors for assessing process variables has expanded data collection for preventive and proactive maintenance. This development boosts the automation solutions in oil and gas industry market, where remote monitoring and industrial iot are critical for asset reliability in upstream data analysis and downstream operations.

- Increased investment in smart grid networking systems to manage energy consumption and improve load forecasting has created a need for robust data management. This trend supports the automation solutions in oil and gas industry market by fostering demand for interconnected systems that ensure grid stability and facilitate the integration of renewable energy sources.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automation Solutions In Oil And Gas Industry Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.6% |

| Market growth 2026-2030 | USD 3920.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, India, Japan, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ecosystem for automation solutions in oil and gas industry is a complex network where technology suppliers of semiconductors and sensors provide critical inputs to major automation vendors, whose platforms represent over 70% of new system deployments.

- These vendors, in turn, deliver integrated hardware and software such as distributed control systems and manufacturing execution systems to end-users, including integrated and national oil companies. A key dynamic is the interaction with regulatory bodies, which mandate standards for process safety and emissions control, directly influencing technology adoption.

- For instance, compliance with new emissions monitoring standards has driven a 20% year-over-year increase in demand for continuous emissions monitoring systems. Distribution channels are shifting from hardware-centric sales to subscription-based software and service models, reflecting the industry's move toward data-contextualization and enterprise-wide analytics.

What are the Key Data Covered in this Automation Solutions In Oil And Gas Industry Market Research and Growth Report?

-

What is the expected growth of the Automation Solutions In Oil And Gas Industry Market between 2026 and 2030?

-

The Automation Solutions In Oil And Gas Industry Market is expected to grow by USD 3.92 billion during 2026-2030, registering a CAGR of 6.6%. Year-over-year growth in 2026 is estimated at 6.3%%. This acceleration is shaped by escalating demand for operational efficiency and cost optimization, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Solution (SCADA, DCS, PLC, and MES), Application (Exploration and production, Transportation and storage, and Refining and processing), End-user (Integrated oil and gas companies, National oil companies, and Independent oil and gas companies) and Geography (North America, Europe, APAC, Middle East and Africa, South America). Among these, the SCADA segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, Middle East and Africa and South America. North America is estimated to contribute 40.3% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, India, Japan, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is escalating demand for operational efficiency and cost optimization, which is accelerating investment and industry demand. The main challenge is escalating cybersecurity threats to critical infrastructure , creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Automation Solutions In Oil And Gas Industry Market?

-

Key vendors include ABB Ltd., AVEVA Group Ltd., Cisco Systems Inc., Danfoss AS, Eaton Corp. Plc, Emerson Electric Co., Endress Hauser Grp Services, Fuji Electric Co. Ltd., General Electric Co., Hitachi Ltd., Honeywell International Inc., Kongsberg Gruppen ASA, KROHNE Group, Mitsubishi Electric Corp., OMRON Corp., Phoenix Contact GmbH and Co, Rockwell Automation Inc., Schlumberger Ltd., Schneider Electric SE and Siemens AG. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for automation solutions in oil and gas industry is intensely focused on software-defined ecosystems, with the top five vendors accounting for over 40% of the market. Key players are differentiating through the integration of AI and digital twin technologies to address complex operational demands.

- For instance, ABB launched its Automation Extended program, a strategic initiative designed to embed generative AI and edge-based analytics directly into existing industrial control systems. This move is mirrored by competitors like Emerson, which are also investing heavily in platforms that enable brownfield modernization without extensive capital expenditure.

- These developments directly respond to the industry's need for scalable and cyber-secure solutions that enhance asset performance management. The primary challenge remains the integration of these advanced systems with legacy infrastructure, which continues to slow enterprise-wide adoption.

We can help! Our analysts can customize this automation solutions in oil and gas industry market research report to meet your requirements.

RIA -

RIA -