Converted Flexible Packaging Market Size 2024-2028

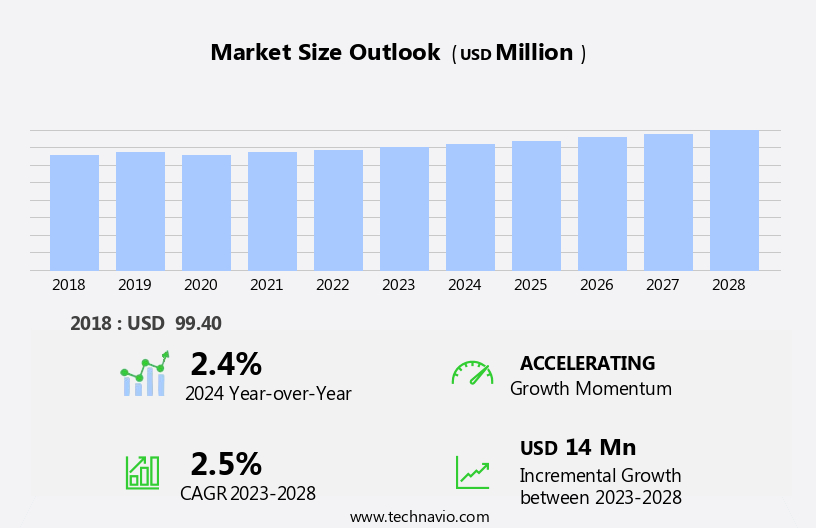

The converted flexible packaging market size is forecast to increase by USD 14 million at a CAGR of 2.5% between 2023 and 2028.

What will be the Size of the Converted Flexible Packaging Market During the Forecast Period?

How is this Converted Flexible Packaging Industry segmented and which is the largest segment?

The converted flexible packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Pouches

- Bags

- Others

- Geography

- APAC

- China

- Europe

- Germany

- UK

- North America

- Canada

- US

- South America

- Middle East and Africa

- APAC

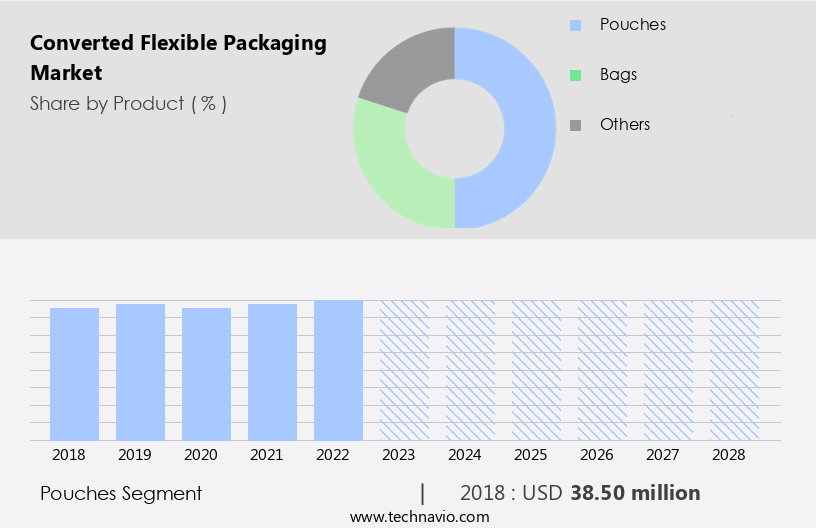

By Product Insights

The pouches segment is estimated to witness significant growth during the forecast period. Pouches are a popular packaging solution for various industries, including food and beverage, health and beauty, and consumer goods. Among the different types of pouches, stand-up pouches have gained significant traction due to their eye-catching shelf appeal and ease of use. These pouches offer multiple barrier layers, ensuring extended product shelf life and protection against moisture, dirt, and bacteria. Available in various sizes, stand-up pouches are suitable for packaging dry food, candies, confectioneries, agriculture products, and liquids. The convenience of stand-up pouches, which allow for an airtight closure and easy stacking, makes them a preferred choice over other types of pouch packaging.

High-barrier materials, such as polyesters, metallocene resins, and plastic, are commonly used In the production of stand-up pouches. Innovative packaging techniques, such as auto-venting films and zippered bags, are also being adopted to enhance the functionality and user-friendliness of these pouches. The market for converted flexible packaging, which includes pouches, bags, and sacks, is expected to grow due to increasing consumer demand for sustainable and convenient packaging solutions. Additionally, the rise in e-commerce sales and the growing popularity of perishable products, such as meat and seafood, are expected to drive the demand for high-barrier packaging materials.

Get a glance at the market report of various segments Request Free Sample

The Pouches segment was valued at USD 38.50 million in 2018 and showed a gradual increase during the forecast period.

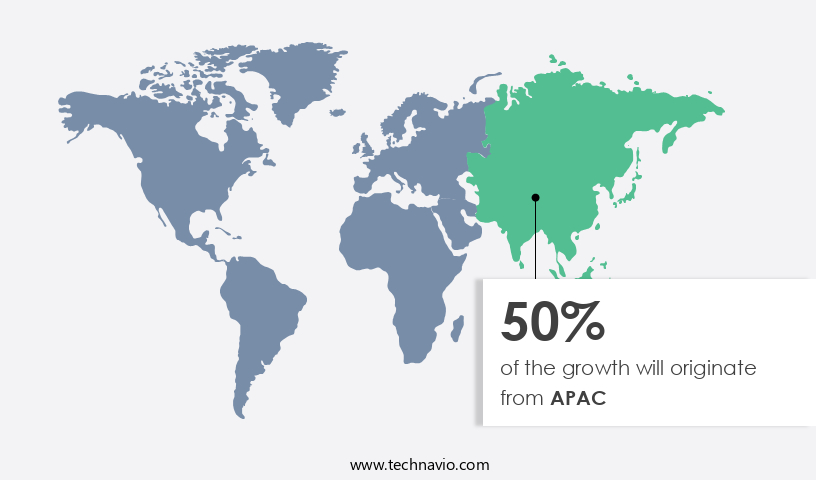

Regional Analysis

APAC is estimated to contribute 50% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in APAC is experiencing significant growth, driven by the expansion of key end-user industries, particularly e-commerce, FMCG, and personal care. Countries like China, India, and Japan are expected to be major revenue contributors due to their rapidly developing e-commerce sectors, with China's industry projected to grow by approximately 20% from 2018 to 2022. In the e-commerce sector, where product protection is crucial during transportation, multi-layered flexible packaging offers enhanced security. Innovative packaging solutions, such as high-barrier materials, auto-venting films, and biodegradable alternatives, cater to various market needs. Key industries, including food and beverage, health and beauty, pharmaceuticals, and consumer goods, rely on flexible packaging for its sustainability, user-friendliness, and extended shelf life.

Packaging materials, such as polyesters, plastics, adhesives, paperboard, aluminum foil, and bags and pouches, are integral to this market's growth.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Converted Flexible Packaging Industry?

- Shift from rigid packaging to converted flexible packaging is the key driver of the market.Flexible packaging is gaining popularity among end-users In the food and beverage, health and beauty, and consumer goods sectors due to its flexibility, durability, and lightweight nature. Converted flexible packaging, specifically, offers numerous benefits, including ease of use, portability, and extended shelf life. High-barrier packaging materials, such as metallocene resins and polyesters, are commonly used in this type of packaging to preserve the freshness and quality of perishable products like meat, seafood, baked goods, and dairy. Single-use packaging, such as zippered bags and pouches, is also increasingly popular for their convenience and user-friendly design. In the food and beverage industry, flexible packaging is used to protect against moisture, oxygen, and UV light, ensuring the preservation of aroma, taste, and texture.

In the healthcare and personal care sectors, flexible packaging is used for its ability to maintaIn the sterility and effectiveness of pharmaceuticals and cosmetics. E-commerce is another significant driver of the flexible packaging market, as it allows for easy shipping and handling of individually wrapped portions. High-performance materials, such as aluminum foil and recyclable insulation packaging, are also used in flexible packaging to enhance its functionality and sustainability. Innovative packaging techniques, such as auto-venting films, are being developed to further improve the convenience and shelf life of flexible packaging. Overall, the market for converted flexible packaging is expected to grow due to the increasing demand for sustainable packaging solutions and the need for longer shelf life for perishable products.

What are the market trends shaping the Converted Flexible Packaging market?

- Advanced recycling technologies and government initiatives to reduce packaging waste is the upcoming market trend.The market is gaining traction In the food industry due to its lightweight, convenient, and economical nature. Single-serve packaging, particularly in food and beverage, health and beauty, and consumer goods sectors, is driving the demand for high-barrier packaging materials such as polyethylene film, polyesters, and plastics. Innovative packaging techniques, like auto-venting films and zippered bags, are extending the shelf life of perishable products. However, the non-recyclability of flexible packaging is a significant challenge. To address this concern, packaging companies and raw material suppliers are introducing eco-friendly alternatives, such as biodegradable materials and recyclable insulation packaging. For instance, Graphic Packaging International offers recyclable paper-based packaging solutions, while ePac Flexible Packaging specializes in sustainable plastic packaging.

The seafood market, with its increasing demand, is also adopting converted flexible packaging for individually wrapped portions. The packaging industry is responding to consumer preferences for user-friendly and sustainable packaging solutions. Packaging materials, including paper, aluminum foil, and pouches and bags, are being developed with improved sustainability and functionality. Packaging technology advancements, such as the use of metallocene resins, are further enhancing the versatility of converted flexible packaging.

What challenges does the Converted Flexible Packaging Industry face during its growth?

- Stringent regulations on manufacture of converted flexible packaging is a key challenge affecting the industry growth.Converted flexible packaging plays a significant role in various industries, including food and beverage, health and beauty, and consumer goods. Innovative packaging solutions, such as high-barrier packaging materials, auto-venting films, and recyclable insulation packaging, are in high demand. Single-use packaging, like pouches, bags, and sacks made from polyesters, plastics, and paper, are popular choices due to their user-friendly design and extended shelf life. The food and beverage sector, which includes meat products and seafood, drives the demand for converted flexible packaging. Seafood consumption continues to rise, leading to an increase in packaged food consumption. In the health and beauty industry, individually wrapped portions of personal care products are gaining popularity.

Manufacturers must adhere to stringent regulations when producing converted flexible packaging. The US Environmental Protection Agency (EPA) has established the Organic Chemicals, Plastics, and Synthetic Fibers (OCPSF) Effluent Guidelines and Standards (40 CFR Part 414), which apply to the process of wastewater discharge after the manufacture of flexible packaging materials. Compliance with these regulations ensures the safety and sustainability of the packaging solutions. Packaging materials, such as polyethylene film, aluminum foil, and paper, are used to create bags, pouches, and other packaging types. Sustainable packaging, including biodegradable alternatives, is gaining traction as consumers become more environmentally conscious. Packaging technology advancements, such as metallocene resins and zippered bags, offer improved functionality and extended shelf life for perishable products.

Exclusive Customer Landscape

The converted flexible packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the converted flexible packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, converted flexible packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Amcor Plc - The market encompasses a diverse product range, with the company specializing in intricately engineered solutions for the dairy industry. Notably, its offerings for cheese feature the tiniest microperforations available, ensuring optimal product preservation and consumer convenience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- American Packaging Corp.

- Berry Global Inc.

- Bischof Klein SE and Co. KG

- Bryce Corp.

- Clondalkin Group Holdings BV

- Constantia Flexibles Group GmbH

- Coveris Management GmbH

- Graphic Packaging Holding Co.

- Huhtamaki Oyj

- Koehler Paper SE

- LLFlex

- Mondi Plc

- Printpack Inc.

- ProAmpac Holdings Inc.

- Sappi Ltd.

- Sealed Air Corp.

- Sonoco Products Co.

- Transcontinental Inc.

- Wipak Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a diverse range of applications across various industries, with food and beverage and health and beauty sectors being significant contributors. Innovative packaging solutions have gained prominence In these sectors to address the unique requirements of their products. Single-use packaging, particularly In the form of pouches and bags, has witnessed notable growth due to its convenience and extended shelf life. High-barrier packaging materials, such as polyesters and metallocene resins, have become increasingly popular for their ability to preserve the freshness and quality of perishable products. The rise of e-commerce has further fueled the demand for converted flexible packaging.

The need for user-friendly, protective, and attractive packaging is crucial for ensuring product safety and enhancing customer experience during transit. In the food and beverage industry, meat products and seafood have been major consumers of converted flexible packaging. The demand for individually wrapped portions and high-barrier materials is driven by the need to maintaIn the freshness and prevent contamination. The health and beauty sector also relies on converted flexible packaging for its lightweight, portable, and cost-effective nature. Biodegradable alternatives have gained traction as sustainable packaging solutions, addressing the growing concerns over plastic waste. Packaging materials used in converted flexible packaging include plastics, polyesters, adhesives, paperboard, and aluminum foil.

Each material type offers unique benefits, such as high-barrier properties, user-friendliness, and sustainability. The packaging solutions market for converted flexible packaging is dynamic, with ongoing research and development focused on improving shelf life, enhancing product protection, and reducing environmental impact. Innovative techniques, such as auto-venting films and recyclable insulation packaging, are gaining popularity. The pharmaceutical industry also utilizes converted flexible packaging for its sterile and tamper-evident properties. Pouches and bags offer the advantage of easy dosing and portability, making them suitable for various pharmaceutical applications. In conclusion, the market is a vibrant and evolving industry, catering to the diverse needs of various sectors, including food and beverage, health and beauty, and pharmaceuticals.

The focus on sustainable, user-friendly, and high-performance packaging solutions is driving innovation and growth in this market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

136 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.5% |

|

Market growth 2024-2028 |

USD 14 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.4 |

|

Key countries |

US, China, UK, Germany, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Converted Flexible Packaging Market Research and Growth Report?

- CAGR of the Converted Flexible Packaging industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the converted flexible packaging market growth of industry companies

We can help! Our analysts can customize this converted flexible packaging market research report to meet your requirements.

RIA -

RIA -