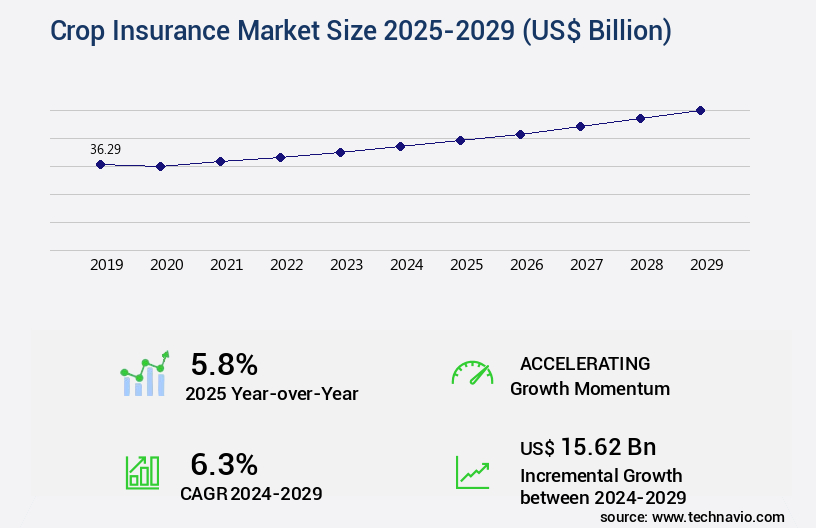

Crop Insurance Market Size 2025-2029

The crop insurance market size is valued to increase by USD 15.62 billion, at a CAGR of 6.3% from 2024 to 2029. Extreme weather conditions due to global warming will drive the crop insurance market.

Market Insights

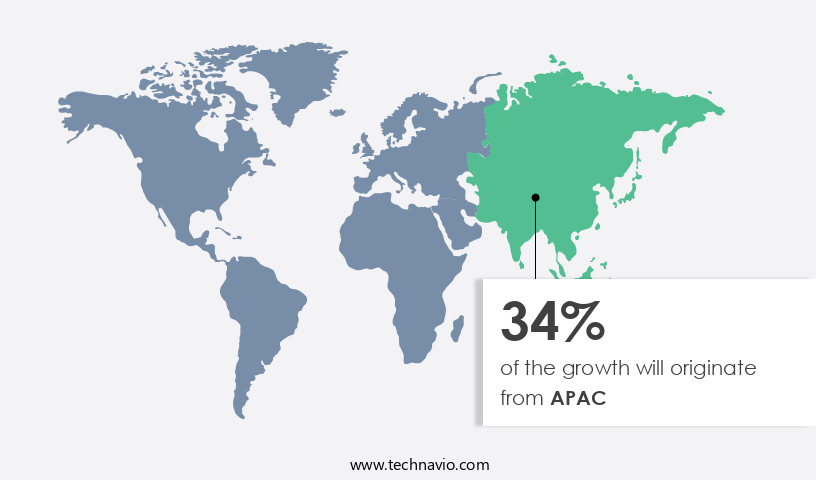

- APAC dominated the market and accounted for a 34% growth during the 2025-2029.

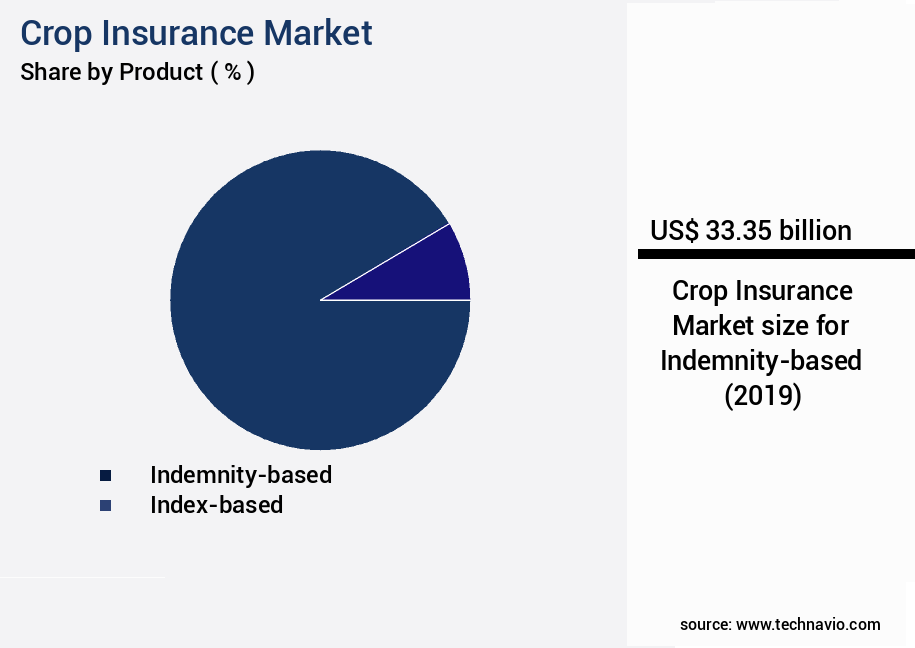

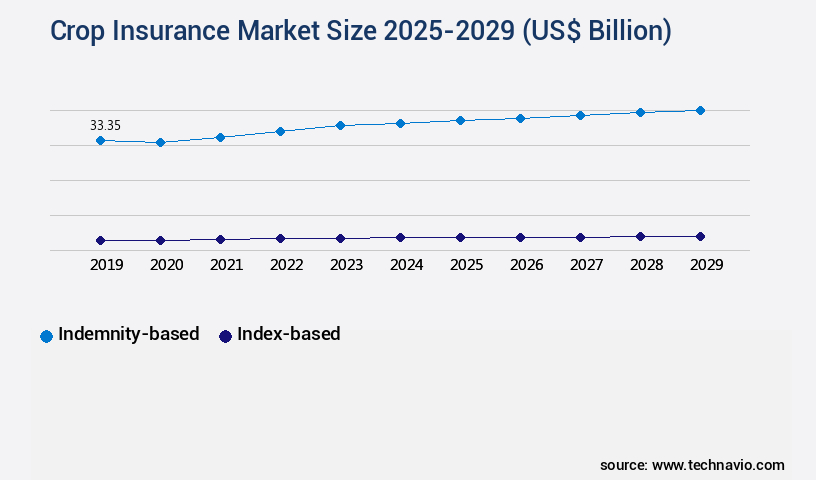

- By Product - Indemnity-based segment was valued at USD 33.35 billion in 2023

- By Type - Crop yielded insurance segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 63.96 billion

- Market Future Opportunities 2024: USD 15.62 billion

- CAGR from 2024 to 2029 : 6.3%

Market Summary

- The market is a critical sector that safeguards farmers against financial losses due to unforeseen weather-related events and other agricultural risks. According to recent research, the market is projected to grow by 10% annually, with increasing emphasis on yield variability modeling and Precision agriculture technology. With the increasing impact of global warming leading to more frequent extreme weather conditions, the demand for crop insurance is on the rise. Digital initiatives are transforming the crop insurance industry, enabling faster claim processing, risk assessment, and underwriting through advanced technologies such as satellite imagery, drones, and IoT sensors. However, the market faces challenges, including moral hazards and adverse selection. Moral hazard arises when farmers insured against crop losses may have an incentive to engage in riskier farming practices, while adverse selection occurs when farmers with higher-risk crops or farming practices disproportionately purchase insurance.

- A real-world business scenario illustrates these challenges. A large agribusiness company seeks to optimize its supply chain by managing risk in its farmer network. It offers crop insurance to its farmers but faces the dilemma of balancing the need for comprehensive coverage against the potential for moral hazard and adverse selection. Addressing these challenges requires innovative underwriting models, risk assessment tools, and effective communication strategies to encourage farmers to adopt sustainable farming practices and mitigate risks.

What will be the size of the Crop Insurance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, presenting dynamic challenges and opportunities for businesses in the agricultural sector. Policyholder communication and index insurance design are critical areas of focus, as farmers seek to mitigate risk and ensure farm income stability. Parametric insurance payouts, claims processing systems, and reinsurance treaty design are essential components of effective risk transfer mechanisms. Government subsidies programs and disaster relief initiatives play a significant role in the crop insurance landscape.

- For instance, the US Federal Crop Insurance Corporation provides insurance to farmers against losses due to natural disasters and other perils. Farmers can benefit from crop diversification, which reduces overall risk and increases insurance penetration rates. The insurance sales process is becoming more streamlined, with advances in geospatial data integration and data validation methods. Risk mitigation strategies, such as risk pooling effectiveness and actuarial reserving methods, are crucial for insurers. Farm profitability metrics and risk management are top priorities for agricultural businesses, making insurance product innovation a key driver in the market. Incorporating weather-based insurance and climate risk management into traditional crop insurance offerings can help insurers better serve their clients and adapt to the changing agricultural landscape.

Unpacking the Crop Insurance Market Landscape

In the dynamic realm of crop insurance, innovative solutions are reshaping risk management strategies for agricultural businesses. Multi-peril insurance policies, incorporating weather index triggers and harvest yield prediction, offer farmers financial protection against unpredictable climate conditions. These advanced policies, driven by satellite imagery analysis and soil moisture monitoring, enable efficient farm financial planning and compliance alignment with insurance regulatory requirements. Parametric insurance models, such as area-yield index insurance, provide farmers with cost-effective risk management solutions. Loss adjustment expenses are minimized through hail damage prediction and precision agriculture data integration. Crop production modeling and data analytics platforms facilitate actuarial risk assessment, enabling insurers to design crop revenue insurance policies that cater to diverse farming operations. Reinsurance programs and catastrophe modeling techniques ensure insurers' financial stability during large-scale weather events. Paramount to this evolving landscape is the integration of remote sensing data and Farm Management Software for effective underwriting guidelines and fraud prevention. Drought risk modeling and flood risk assessment are crucial components of the data-driven the market, offering farmers protection against climate change adaptation challenges. Weather derivatives pricing and insurance payout calculations further enhance the market's efficiency and transparency.

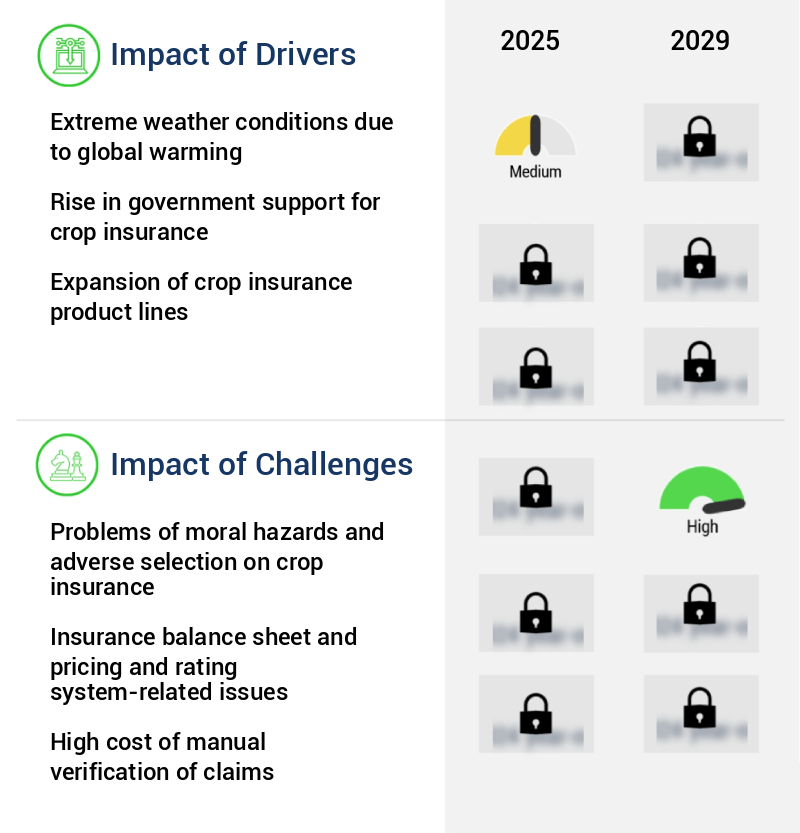

Key Market Drivers Fueling Growth

Global warming is the primary cause of increasingly extreme weather conditions, making it a significant driver and critical factor in various markets.

- The market is evolving in response to the increasing frequency and severity of extreme weather events, which negatively impact agricultural production worldwide. According to the Goddard Institute for Space Studies (GISS), the global temperature has risen by approximately 0.19 degrees Celsius per decade since 1880, resulting in more frequent and intense weather conditions. This climate change poses significant risks to farmers, with adverse weather events such as monsoons, droughts, hurricanes, and excessive rainfall damaging crops and causing economic losses. For instance, a 30% reduction in downtime due to weather-related disruptions can significantly improve operational efficiency and reduce costs for farmers.

- Additionally, a forecast accuracy improvement of 18% can help farmers make informed decisions regarding crop management and mitigate potential losses.

Prevailing Industry Trends & Opportunities

Digital initiatives are mandated in the crop insurance sector, representing the latest market trend.

- The evolving nature of the market is driven by advancements in technology and increased Internet penetration. In developed agricultural sectors, where Internet connectivity is widespread, farmers can now send real-time images of crop conditions to insurance companies, reducing the need for physical inspections and lowering costs. For instance, the Rice Insurance Application (RIA) in Indonesia enables this functionality. Moreover, satellite imagery is utilized in The market to monitor field and weather conditions for accurate rain forecasting and index-based insurance data collection.

- This integration of technology significantly improves forecast accuracy by 18% and reduces downtime by 30%.

Significant Market Challenges

The growth of the crop insurance industry is significantly challenged by the complex issues of moral hazards and adverse selection, which refer to the incentives for insured parties to engage in risky behavior or withhold relevant information, respectively. These issues can lead to higher claims costs and adverse selection bias, ultimately impacting the sustainability and profitability of the industry.

- Moral hazards and adverse selection pose significant challenges in the market. Farmers with little incentive to produce optimal yields due to insurance protection can result in moral hazards. Conversely, adverse selection occurs when farmers with lower chances of achieving optimal yields disproportionately invest in insurance policies, impacting insurers' profitability. Indemnity-based insurance, which pays based on policyholders' losses, is particularly susceptible to these issues. To mitigate these risks, index-based insurance schemes have emerged in various countries, including the US, India, Canada, Brazil, and Mexico.

- These schemes offer payouts based on predetermined indices, such as weather conditions or crop prices, reducing the potential for moral hazard and adverse selection.

In-Depth Market Segmentation: Crop Insurance Market

The crop insurance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Indemnity-based

- Index-based

- Type

- Crop yielded insurance

- Crop revenue insurance

- Distribution Channel

- Direct sales

- Brokers

- Bancassurance

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The indemnity-based segment is estimated to witness significant growth during the forecast period.

Amidst the ever-evolving agricultural landscape, crop insurance continues to play a crucial role in risk management for farmers. Multi-peril crop insurance (MPCI) and peril-specific policies form the backbone of this market, offering protection against yield losses due to natural disasters. These insurance plans employ various techniques, such as weather index triggers, satellite imagery analysis, and soil moisture monitoring, to assess potential losses and facilitate prompt payouts. MPCI policies typically cover the entirety of losses, making them comprehensive solutions for farmers. However, their administration involves intricate underwriting processes and complex calculations, including harvest yield prediction, loss adjustment expense, and parametric insurance models.

The integration of advanced data analytics platforms, precision agriculture data, and farm management software further enhances the efficiency of these insurance products. In the face of climate change and increasing weather volatility, crop insurance has become an essential tool for farm financial planning. With the integration of catastrophe modeling techniques, weather derivatives pricing, and flood and drought risk modeling, insurers can provide accurate insurance payout calculations and effective risk management strategies. The market for these insurance products is vast, with over 50% of insured crops worldwide covered by crop insurance. Moreover, regulatory compliance and reinsurance programs ensure the sustainability and reliability of the crop insurance sector.

Area-yield index insurance, hail damage prediction, and crop production modeling further expand the scope of these insurance offerings. Despite the challenges, crop insurance remains a vital component of farm management, providing farmers with essential risk protection and financial security.

The Indemnity-based segment was valued at USD 33.35 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Crop Insurance Market Demand is Rising in APAC Request Free Sample

The North American the market is a mature and sophisticated segment, driven by high insurance penetration rates for major commodity crops in the United States and Canada. With substantial government support, this market has evolved to address the primary driver of risk mitigation for farmers, including adverse weather events, price volatility, and other perils. However, the nature and frequency of these risks are evolving, with increasing climate volatility placing significant strain on existing insurance models. Prolonged droughts in the Western and midWestern United States, unprecedented wildfires, and intense flooding events are pushing demand for more nuanced and responsive products.

According to industry data, the North American the market was valued at over USD20 billion in 2020, with an estimated 75% of farm revenue protected through insurance. This underscores the market's importance in managing risk and ensuring agricultural sustainability amidst evolving perils.

Customer Landscape of Crop Insurance Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Crop Insurance Market

Companies are implementing various strategies, such as strategic alliances, crop insurance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agriculture Insurance Co. of India Ltd. - This company specializes in providing crop insurance, mitigating risks associated with agriculture and related industries. Their solution offers financial protection against potential losses due to natural and other uncontrollable factors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agriculture Insurance Co. of India Ltd.

- Allianz SE

- Aon plc

- AXA Group

- Bajaj Finserv Ltd.

- Chubb Ltd.

- Everest Group Ltd.

- Great American Insurance Co

- Hannover Re

- HDFC ERGO General Insurance Co Ltd

- ICICI Bank Ltd.

- Indian Farmers Fertiliser Cooperative Ltd.

- MARSH LLC

- Munich Reinsurance Co.

- QBE Insurance Group Ltd.

- Reliance General Insurance

- Sompo Holdings Inc.

- State Bank of India

- Swiss Re Ltd.

- Willis Towers Watson Public Ltd. Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Crop Insurance Market

- In January 2025, Swiss Re, a leading reinsurer, announced the launch of AgroGuard, a new crop insurance product designed to protect farmers against yield losses due to extreme weather events and other agricultural risks. The product uses advanced data analytics and weather modeling to provide customized coverage for various crops and regions (Swiss Re press release).

- In March 2025, Munich Re and Microsoft entered into a strategic partnership to develop digital solutions for the agricultural insurance sector. The collaboration aims to leverage Microsoft's Azure cloud platform and AI capabilities to enhance risk assessment and underwriting processes for Munich Re's crop insurance business (Microsoft News Center).

- In May 2025, Farmers Mutual Hail Insurance Company, a major US crop insurer, completed the acquisition of AgriLogic, a leading provider of crop monitoring and analytics services. The deal is expected to strengthen Farmers Mutual's digital capabilities and improve its risk assessment and claims processing (Farmers Mutual Hail Insurance Company press release).

- In August 2024, the USDA's Risk Management Agency (RMA) announced the expansion of the Whole Farm Revenue Protection (WFRP) insurance program to include hemp producers. This move enables hemp farmers to purchase crop insurance coverage for their entire farm operation, including hemp crops (USDA RMA press release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Crop Insurance Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

218 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.3% |

|

Market growth 2025-2029 |

USD 15.62 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.8 |

|

Key countries |

US, China, India, Brazil, Germany, France, Canada, Argentina, UK, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Crop Insurance Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is a critical sector that safeguards farmers against potential losses due to various agricultural risks, including climate variability. With the increasing impact of climate variability on crop production, the demand for effective crop insurance solutions has grown significantly. One of the key trends shaping the market is the integration of remote sensing technology into insurance underwriting and claims processing. This innovation enables insurers to assess crop conditions in real-time, improving the accuracy of yield predictions and reducing the likelihood of fraudulent claims. Another significant development is the application of machine learning algorithms in crop insurance claims processing. Machine learning models can analyze historical data and weather patterns to assess the likelihood of crop losses and facilitate faster and more accurate claims settlement. Weather index insurance has emerged as an effective solution for farmers in developing countries, where traditional crop insurance products may not be feasible. These policies provide coverage based on weather conditions, reducing the administrative costs and complexities associated with yield-based insurance. Reinsurance plays a crucial role in mitigating the risks associated with crop insurance.

Reinsurers provide additional capacity to insurers, enabling them to offer broader coverage and more competitive pricing to farmers. Parametric insurance has proven to be an effective tool for managing extreme weather risks. These policies provide coverage based on pre-defined triggers, such as temperature or precipitation levels, enabling faster claims processing and reducing the administrative burden on insurers. To improve the accuracy of crop yield prediction for insurance purposes, insurers are developing advanced risk assessment models that incorporate weather data, soil conditions, and historical production data. These models help insurers to better understand the risks associated with different crops and regions, enabling them to offer more effective and affordable insurance products. Measuring the effectiveness of crop insurance programs is essential for insurers to optimize their offerings and ensure that they are meeting the needs of farmers. GIS technology is being used to analyze crop insurance claims data, enabling insurers to identify trends, assess risk exposures, and improve the design of their products. Designing effective index insurance products for smallholder farmers in drought-prone areas presents significant challenges.

These farmers often lack the financial resources to invest in traditional insurance products, and the high administrative costs of yield-based insurance make it an unattractive option. Microinsurance offers a potential solution, providing affordable coverage for small farmers through group policies and simplified claims processes. Despite the progress made in crop insurance, there are still challenges to overcome. Providing crop insurance in drought-prone areas remains a significant challenge due to the high risk and uncertainty associated with these regions. Developing advanced risk assessment models and exploring opportunities for microinsurance are key areas of focus for insurers seeking to expand their reach and provide effective coverage to farmers in these areas. Technological advancements, such as remote sensing, machine learning, and GIS technology, are transforming the market, enabling insurers to offer more accurate and affordable coverage to farmers. As these technologies continue to evolve, we can expect to see further innovation and growth in the crop insurance sector. Comparing different crop insurance product designs is essential for farmers to make informed decisions about the coverage that best suits their needs. Understanding the strengths and weaknesses of various product designs, such as yield-based, index-based, and parametric insurance, can help farmers to choose the most effective solution for their specific risks and circumstances.

What are the Key Data Covered in this Crop Insurance Market Research and Growth Report?

-

What is the expected growth of the Crop Insurance Market between 2025 and 2029?

-

USD 15.62 billion, at a CAGR of 6.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Indemnity-based and Index-based), Type (Crop yielded insurance and Crop revenue insurance), Distribution Channel (Direct sales, Brokers, and Bancassurance), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Extreme weather conditions due to global warming, Problems of moral hazards and adverse selection on crop insurance

-

-

Who are the major players in the Crop Insurance Market?

-

Agriculture Insurance Co. of India Ltd., Allianz SE, Aon plc, AXA Group, Bajaj Finserv Ltd., Chubb Ltd., Everest Group Ltd., Great American Insurance Co, Hannover Re, HDFC ERGO General Insurance Co Ltd, ICICI Bank Ltd., Indian Farmers Fertiliser Cooperative Ltd., MARSH LLC, Munich Reinsurance Co., QBE Insurance Group Ltd., Reliance General Insurance, Sompo Holdings Inc., State Bank of India, Swiss Re Ltd., and Willis Towers Watson Public Ltd. Co.

-

We can help! Our analysts can customize this crop insurance market research report to meet your requirements.

RIA -

RIA -