Data Center Storage Market Size 2025-2029

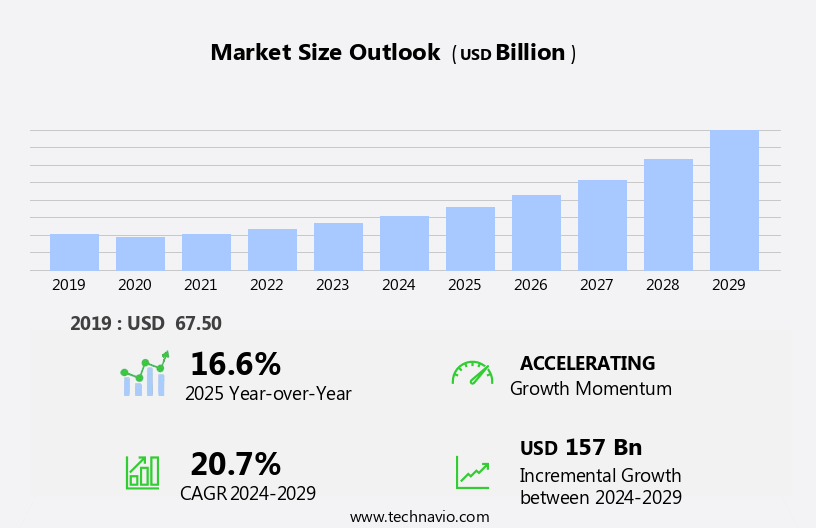

The data center storage market size is forecast to increase by USD 157 billion, at a CAGR of 20.7% between 2024 and 2029.

- The market is experiencing significant growth driven by the increasing volume, velocity, veracity, and variety (4Vs) of data. The proliferation of IoT-enabled devices is leading to an exponential increase in data generation, necessitating robust and scalable data center storage solutions. Furthermore, the trend towards data center consolidation is intensifying, as organizations seek to optimize their IT infrastructure and reduce costs. Additionally, advancements in technology, such as edge computing and the Internet of Things (IoT), are creating new opportunities for data center providers. However, this market landscape is not without challenges. Power consumption and cooling requirements for data centers continue to pose significant operational challenges, necessitating energy-efficient storage solutions. Additionally, data security and privacy concerns are becoming increasingly critical, with the risk of data breaches and cyber attacks growing in frequency and sophistication.

- Companies seeking to capitalize on the opportunities presented by the market must prioritize energy efficiency, data security, and scalability to meet the evolving demands of the digital economy. Navigating these challenges effectively will require strategic investments in innovative technologies and operational best practices. Data center storage solutions are increasingly being integrated with lawful interception to ensure secure and compliant data handling in response to regulatory requirements.

What will be the Size of the Data Center Storage Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

- The market is experiencing significant evolution, driven by the adoption of cloud native architectures and the integration of machine learning technologies. Performance monitoring and data lifecycle management have become essential for optimizing storage resources in this dynamic environment. Edge computing and edge storage are gaining traction, enabling real-time data processing and reducing latency. Data governance and security are paramount, with capacity monitoring, storage availability, and data privacy becoming increasingly important. AI and serverless computing are revolutionizing data analytics, while hybrid cloud solutions offer flexibility and cost savings.

- Data center optimization, storage consolidation, and migration are key strategies for managing the complexities of big data. Data sovereignty, data center virtualization, and storage maintenance are also critical aspects of the market, ensuring regulatory compliance, efficient resource utilization, and system reliability. Data loss prevention and storage automation are essential for mitigating risks and streamlining operations.

How is this Data Center Storage Industry segmented?

The data center storage industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- SAN system

- NAS system

- DAS system

- Component

- Hardware

- Software

- End-user

- IT and telecommunications

- BFSI

- Healthcare

- Retail

- Others

- Geography

- North America

- US

- Canada

- Europe

- Germany

- Italy

- The Netherlands

- UK

- APAC

- Australia

- China

- India

- Thailand

- Rest of World (ROW)

- North America

By Deployment Insights

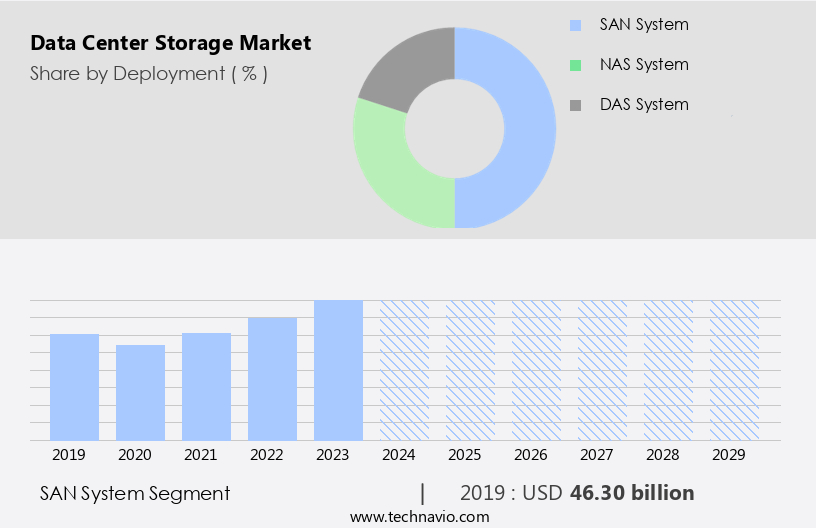

The SAN system segment is estimated to witness significant growth during the forecast period. In today's data-driven business landscape, data center storage solutions have become a critical investment for organizations. The need for data retention, security, and efficient management of large volumes of data has led to the adoption of advanced storage technologies. One such technology is Storage Area Networks (SAN), which offers centralized control and flexibility to share capacity between multiple hosts. SAN systems have gained popularity due to their cost-effective upgrades and independence from additional hardware storage. This trend has spurred technological advancements in SAN systems, resulting in the development of new storage solutions tailored to support the SAN protocol. Moreover, energy efficiency is a significant concern for data center operations, leading to the integration of cooling systems and power consumption optimization.

Data security remains a top priority, driving the adoption of data encryption and deduplication techniques. File storage, data archiving, and disaster recovery are essential components of a robust data center infrastructure. Tiered storage, object storage, and software-defined storage (SDS) are emerging trends, offering improved storage performance optimization and flexibility. Data center design and capacity planning are crucial aspects of any storage strategy. Disaster recovery and data replication are essential for business continuity. Data center management software and interconnects facilitate efficient management of storage resources. Compliance with data regulations and adherence to physical security measures are essential for maintaining data integrity. The integration of advanced technologies, such as SAN, SDS, and cloud storage, is transforming the landscape, offering improved performance, flexibility, and cost savings.

The SAN system segment was valued at USD 46.30 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

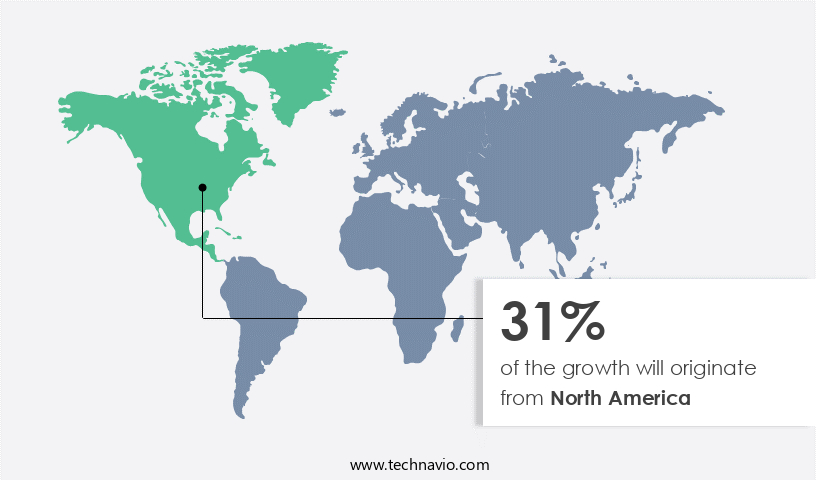

North America is estimated to contribute 31% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the dynamic market, various entities are shaping the industry's evolution. North America's dominance stems from the region's increasing number of data centers, driven by advanced technologies' adoption and well-established communication infrastructure. This growth is further fueled by investments in expanding existing data centers and establishing new ones. Data retention, a critical aspect of data center operations, is addressed through various solutions such as storage virtualization, data archiving, and tiered storage. Energy efficiency is another essential focus, with cooling systems, power consumption optimization, and green data centers playing significant roles. Data security is paramount, ensuring data encryption, deduplication, and physical security.

Storage hardware, including block storage, storage arrays, and flash memory, is essential for handling the vast amounts of data generated. Software-defined storage (SDS) and hyperconverged infrastructure (HCI) are disruptive technologies enhancing storage management and data center design. Data center management software, including storage interconnects and data center infrastructure management, optimizes performance and ensures compliance. Data replication and disaster recovery are crucial for business continuity, while data compression and data compression technologies improve storage capacity planning. Fibre channel and other storage interconnects facilitate seamless data transfer. Cloud storage and storage servers offer flexibility and scalability.

These entities include data retention, energy efficiency, data center operations, file storage, data security, storage virtualization, data archiving, storage controllers, data center design, storage capacity planning, disaster recovery, tiered storage, storage management software, object storage, cooling systems, data deduplication, data encryption, block storage, storage arrays, software-defined storage, storage hardware, flash memory, green data center, hyperconverged infrastructure, data replication, data center management, storage interconnects, data compliance, power consumption, storage performance optimization, fibre channel, data center infrastructure, data compression, physical security, and cloud storage.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Data Center Storage market drivers leading to the rise in the adoption of Industry?

- The integration and expansion of volume, velocity, veracity, and variety (4Vs) in data are essential drivers propelling market growth. The market is experiencing significant growth due to the increasing volume and velocity of data. With data now being generated on a massive scale, measuring it in units of zettabytes and yottabytes, and the demand for real-time access, the velocity of data generation and processing is accelerating. Initially, data analysis was performed through batch processing, but now it's essential to extract insights from data in real-time. Data center operations require efficient storage solutions to manage this vast amount of data while ensuring data security and retention. File storage, data archiving, and storage virtualization are crucial components of data center design.

- Energy efficiency is another critical factor as data centers consume a significant amount of power. Storage controllers play a vital role in managing data flow and optimizing storage utilization. Data security is a top priority, and advanced technologies like encryption, access control, and data masking are used to protect sensitive information. Data center design must consider these factors to ensure efficient, secure, and cost-effective storage solutions.

What are the Data Center Storage market trends shaping the Industry?

- The increasing prevalence of Internet of Things (IoT)-enabled devices represents a significant market trend. This development is driven by the growing demand for connectivity and automation across various industries. The proliferation of IoT-connected devices worldwide has led to a significant increase in data generation. This trend, coupled with the adoption of connected cars, homes, health, and smart cities, has resulted in an increase in data center network traffic. Consequently, enterprises are under pressure to manage and analyze this data effectively to derive valuable business insights. To address this need, they are investing in advanced storage systems and big data analytics solutions. Effective storage capacity planning is crucial in managing this data influx. Tiered storage solutions enable businesses to allocate storage resources efficiently based on data access frequency and importance.

- Storage management software facilitates the automation of storage resource allocation and optimization. Moreover, data security is a top priority for businesses. Data deduplication, data encryption, and block storage are essential features that ensure data security and integrity. Additionally, cooling systems help maintain optimal operating temperatures for data centers, reducing energy consumption and costs. Object storage, with its scalability and flexibility, is gaining popularity due to its ability to store vast amounts of unstructured data.

How does Data Center Storage market face challenges during its growth?

- The ongoing trend of data center consolidation poses a significant challenge to the industry's growth by necessitating increased efficiency, capacity, and cost savings. The market is experiencing a significant shift towards consolidation, driven by the adoption of advanced technologies and strategies. This trend is leading to the merger of multiple data centers into larger, more efficient ones, resulting in cost savings for service providers. Consolidation reduces the need for excessive storage hardware and decreases operational and maintenance expenses. Furthermore, it enhances security and control by centralizing data management. Software-defined storage (SDS) and hyperconverged infrastructure (HCI) are two emerging technologies contributing to this consolidation trend. SDS enables the separation of storage software from hardware, providing greater flexibility and efficiency. HCI integrates compute, storage, and networking resources into a single system, simplifying data center management.

- Another critical aspect of data center consolidation is the implementation of green initiatives. The use of flash memory and energy-efficient storage interconnects is becoming increasingly popular, as they help minimize energy consumption and reduce the carbon footprint of data centers. Data replication is also a crucial factor, ensuring business continuity and disaster recovery in the event of data loss. Consolidation, SDS, HCI, green initiatives, and data replication are some of the key drivers shaping the market's growth.

Exclusive Customer Landscape

The data center storage market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the data center storage market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, data center storage market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

DataDirect Networks Inc. - This company specializes in advanced storage solutions, engineered for artificial intelligence (AI), high-performance computing (HPC), and enterprise applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- DataDirect Networks Inc.

- Dell Technologies Inc.

- Equinix Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise Co.

- Hitachi Vantara LLC

- Huawei Technologies Co. Ltd.

- Inspur Group.

- International Business Machines Corp.

- Lenovo Group Ltd.

- NEC Corp.

- NetApp Inc.

- Nimbus Data Inc.

- Oracle Corp.

- Pure Storage Inc.

- Quanta Computer Inc.

- Vast Data

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Data Center Storage Market

- In February 2023, IBM announced the launch of its new AI-powered storage system, IBM Elastic Storage System (ESS) 3000, designed to optimize data access and reduce costs for enterprise clients. This innovation marks a significant advancement in data center storage, combining AI with flash storage to improve data efficiency and performance (IBM Press Release).

- In May 2024, Amazon Web Services (AWS) and Microsoft Azure entered into a strategic partnership to expand their cloud services interoperability, allowing customers to easily transfer data between their platforms. This collaboration is expected to boost competition in the market and provide more flexibility for businesses (Reuters).

- In October 2024, Dell Technologies completed its acquisition of data protection and disaster recovery solutions provider, Commvault, for approximately USD 1.8 billion. This move strengthens Dell's data management offerings and positions the company to better compete in the growing data protection market (Dell Technologies Press Release).

- In January 2025, Google Cloud Platform announced the availability of its new service, Anthos Filestore, a fully managed file storage service for stateful workloads in the cloud. Anthos Filestore is designed to simplify the management of file storage for businesses and integrates seamlessly with Kubernetes environments (Google Cloud Platform Blog).

Research Analyst Overview

The market continues to evolve, driven by the ever-increasing demand for data retention and efficient data center operations. Energy efficiency is a significant concern, leading to advancements in cooling systems and storage capacity planning. Disaster recovery solutions, such as tiered storage and storage management software, ensure business continuity. Object storage and data archiving offer scalability and cost savings, while data security measures like data encryption and data deduplication protect sensitive information. Storage virtualization and software-defined storage (SDS) enable agile and flexible storage infrastructure. Data center design incorporates storage controllers, storage arrays, and storage interconnects to optimize storage performance. Flash memory and green data centers are gaining popularity for their energy efficiency and high-speed data access.

Hyperconverged infrastructure (HCI) streamlines data center management, while power consumption remains a critical factor in data center operations. Data compliance regulations necessitate robust data security and compliance measures. Data replication ensures data availability and reduces risk. Cooling systems continue to evolve, with innovations in liquid cooling and free cooling. Data center infrastructure is increasingly adopting cloud storage and storage servers to meet the growing demand for data storage and processing power. Fibre channel and other storage interconnects facilitate seamless data transfer between storage devices and servers. In this dynamic market, storage solutions continue to adapt to meet the evolving needs of various sectors, including finance, healthcare, and manufacturing.

The ongoing unfolding of market activities and evolving patterns underscore the importance of staying informed and agile in the ever-changing data center storage landscape.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Data Center Storage Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

230 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.7% |

|

Market growth 2025-2029 |

USD 157 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

16.6 |

|

Key countries |

US, Germany, China, Canada, UK, The Netherlands, Italy, Thailand, India, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Data Center Storage Market Research and Growth Report?

- CAGR of the Data Center Storage industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the data center storage market growth of industry companies

We can help! Our analysts can customize this data center storage market research report to meet your requirements.

RIA -

RIA -