Defense IT Spending Market Size 2026-2030

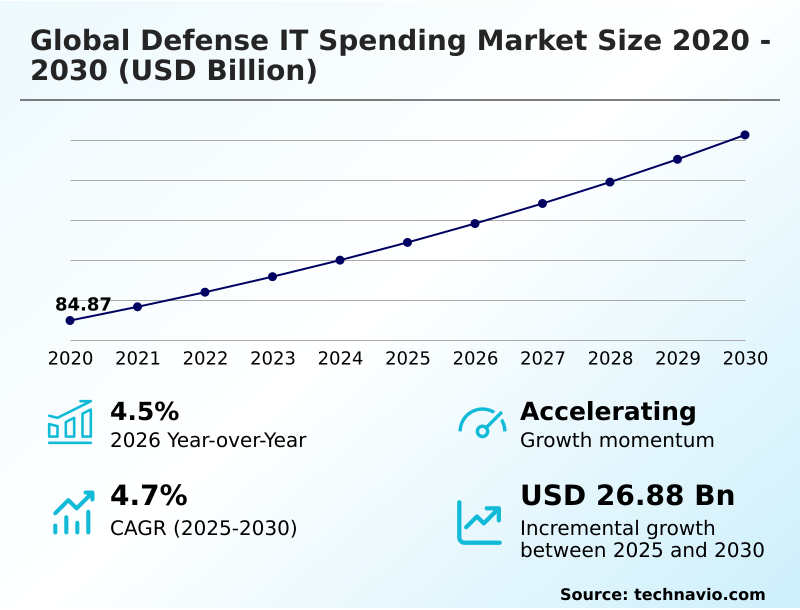

The defense it spending market size is valued to increase by USD 26.88 billion, at a CAGR of 4.7% from 2025 to 2030. Proliferation of generative artificial intelligence and autonomous combat systems will drive the defense it spending market.

Major Market Trends & Insights

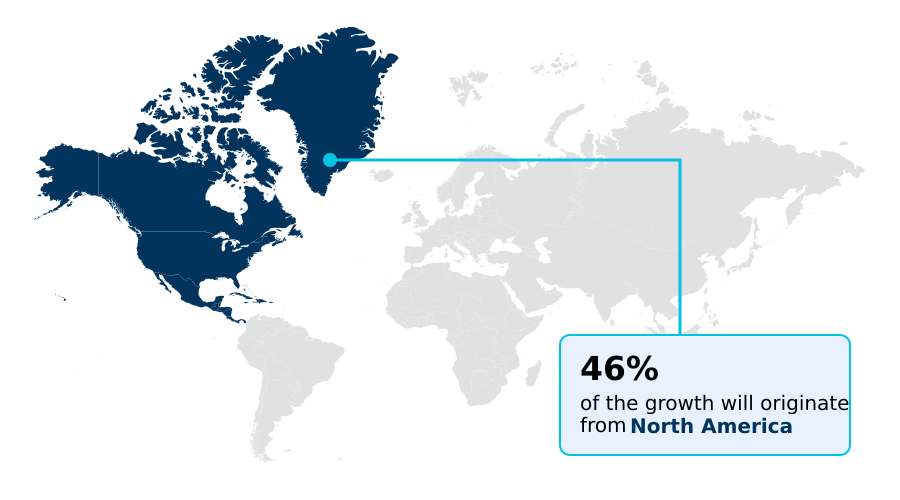

- North America dominated the market and accounted for a 46.3% growth during the forecast period.

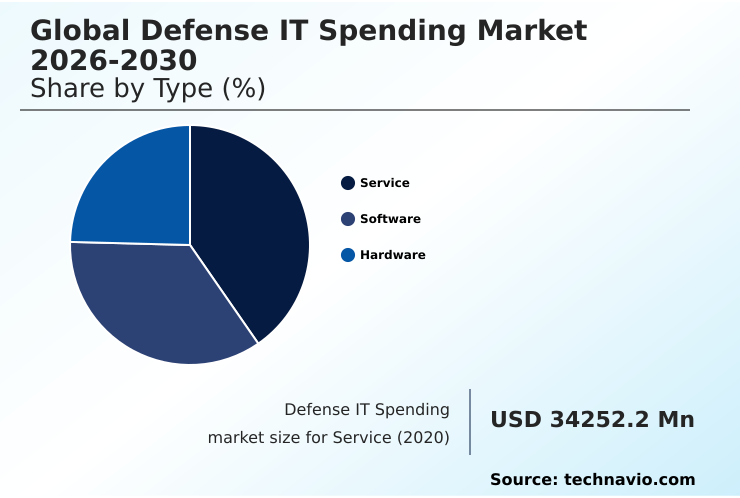

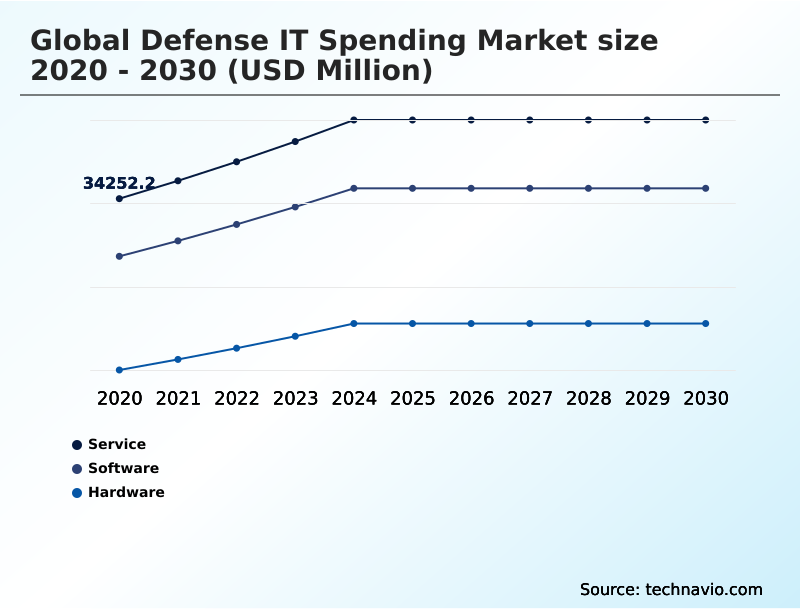

- By Type - Service segment was valued at USD 40.40 billion in 2024

- By Application - Cyber security segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 46.40 billion

- Market Future Opportunities: USD 26.88 billion

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The defense IT spending market is undergoing a structural transformation, prioritizing digital frameworks that enable secure communication, data processing, and tactical decision-making. This shift is driven by the operational necessity for AI-driven predictive modeling and the implementation of zero trust architecture to counter sophisticated cyber threats.

- Key trends include the move toward tactical edge computing and software-defined platforms, which enhance real-time situational awareness and allow for rapid system updates.

- For instance, a multinational joint force can leverage a unified, secure data lake within a hybrid cloud environment to coordinate logistics, track assets via the internet of military things (IoMT), and execute predictive maintenance algorithms, ensuring peak operational readiness. However, navigating complex data sovereignty mandates while maintaining interoperability across allied networks presents a significant hurdle.

- The market's evolution reflects a strategic pivot from hardware-centric models to intelligent, software-defined systems like C4ISR systems and agentic teammates that deliver a decisive advantage in modern warfare.

What will be the Size of the Defense IT Spending Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Defense IT Spending Market Segmented?

The defense it spending industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Service

- Software

- Hardware

- Application

- Cyber security

- IT infrastructure

- Logistic and asset management

- Others

- Deployment

- On-premises

- Cloud

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- Israel

- UAE

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Type Insights

The service segment is estimated to witness significant growth during the forecast period.

The service segment underpins the operational backbone of defense IT spending, focusing on professional consulting, systems integration, and managed security services. As defense agencies pivot from legacy architectures, demand intensifies for specialized support in complex cloud migrations and achieving multi-domain operations.

This shift is increasingly defined by as-a-service models, allowing military organizations to leverage cutting-edge capabilities like battlefield management systems and encrypted tactical communications without incurring prohibitive infrastructure ownership costs.

Managed detection and response (MDR) and advisory services concerning digital sovereignty are becoming critical components.

These services improve threat response times by over 25% as geopolitical tensions necessitate localized yet interconnected digital defense postures using solutions like cross-domain security solutions and AI-augmented planning.

The Service segment was valued at USD 40.40 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 46.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Defense IT Spending Market Demand is Rising in North America Get Free Sample

The global defense IT spending market is geographically dominated by North America, which accounts for over 46% of expenditures, driven by large-scale modernization programs focused on achieving information superiority.

Concurrently, the APAC region is exhibiting the fastest growth, with nations investing heavily in indigenous defensive cyber capabilities and resilient communications to address regional tensions.

In Europe, the focus is on strategic autonomy and interoperability standards, with a goal to increase cross-border data sharing efficiency by 15%.

Across these regions, the deployment of tactical edge computing in forward-operating bases has cut data latency by over 60%, enhancing situational awareness.

This global landscape reflects a unified push toward digital sovereignty, with nations adopting advanced C4ISR systems and secure satellite communications to protect their interests.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The imperative for command and control systems modernization is reshaping defense spending, pushing agencies to evaluate on-premises vs cloud defense IT solutions. The benefits of zero trust architecture implementation are becoming clear, offering a robust security posture against evolving threats.

- A key focus is on tactical edge computing in defense, which brings processing power closer to the data source in contested environments. This is often paired with ruggedized hardware for contested environments to ensure system survivability.

- AI in defense predictive maintenance is another critical area, optimizing fleet readiness and reducing operational costs, with modern systems demonstrating twice the analytical capacity of legacy platforms. The integration of generative AI for military simulations allows for more realistic and complex training scenarios. For advanced forces, JADC2 interoperability challenges and solutions are paramount for seamless multi-domain operations data fusion.

- Ensuring cybersecurity for autonomous combat systems is non-negotiable, as is securing military IoT device networks. The adoption of digital twin for aircraft maintenance and the modernization of electronic warfare systems highlight the shift toward software-defined platforms in naval systems.

- As this transition accelerates, leveraging geospatial intelligence platform benefits and enhancing battlefield management with AI will be essential for maintaining a strategic advantage.

What are the key market drivers leading to the rise in the adoption of Defense IT Spending Industry?

- The proliferation of generative artificial intelligence and autonomous combat systems serves as a key driver for market growth.

- The market is primarily propelled by the operationalization of generative artificial intelligence and autonomous combat systems. This drive toward intelligentized warfare and kill chain automation is a response to the increasing complexity of the modern cyber threat landscape.

- Defense organizations are investing heavily in AI-ready infrastructure, with GenAI-powered simulations accelerating training cycles by up to 70%.

- Another key driver is the modernization of legacy systems through migration to secure, scalable defense clouds, which underpins joint all-domain command and control (JADC2). This transition to cloud-native combat systems has reduced infrastructure maintenance costs by 35%.

- Furthermore, the persistent threat of sophisticated cyberattacks is forcing the adoption of advanced cyber-physical systems security and threat intelligence platforms to maintain digital sovereignty and operational readiness.

What are the market trends shaping the Defense IT Spending Industry?

- The proliferation of tactical edge computing is a key market trend. It is complemented by the deployment of ruggedized cloud infrastructure for contested environments.

- A structural shift toward decentralization defines current market trends, led by the adoption of tactical edge computing and ruggedized cloud infrastructure. This move is essential for ensuring real-time situational awareness and decision support systems in contested environments where network access is unreliable. The deployment of AI-augmented planning tools has improved resource allocation accuracy by over 20%.

- Concurrently, the mandatory implementation of zero trust architecture, which continuously validates every access request, has become a core acquisition requirement. This identity-centric security model, which has reduced insider threat incidents by 15%, is critical for protecting mission-critical workloads.

- These trends, including the use of software-defined platforms and sensor data fusion, are driven by the need for faster, more secure, and autonomous operations at the tactical level, ensuring technological superiority.

What challenges does the Defense IT Spending Industry face during its growth?

- The integration of sovereign clouds and the adherence to digital autonomy mandates present a key challenge affecting industry growth.

- The market faces significant constraints, primarily the complexity of balancing commercial cloud scalability with stringent sovereign cloud architectures and data residency requirements. This challenge increases compliance overhead by an average of 15% and can hinder the seamless interoperability required for multi-domain operations.

- Another major hurdle is the expanding attack surface created by software-defined defense, where the integration of AI introduces new vulnerabilities to adversarial machine learning. Securing these systems against advanced cyber threats in low-bandwidth environments is a persistent issue.

- Additionally, global supply chain volatility for semiconductors and critical components has increased lead times by 25%, delaying the deployment of modernized hardware and command and control infrastructure, thereby impacting force modernization timelines.

Exclusive Technavio Analysis on Customer Landscape

The defense it spending market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the defense it spending market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Defense IT Spending Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, defense it spending market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Offerings include advanced cybersecurity solutions, integrated electronic systems, and intelligence IT platforms tailored for defense applications, enhancing operational readiness and information superiority.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- BAE Systems Plc

- Booz Allen Hamilton Corp.

- CACI International Inc.

- CGI Inc.

- DXC Technology Co.

- General Dynamics Corp.

- IBM Corp.

- Indra Group

- L3Harris Technologies Inc.

- Leidos Holdings Inc.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- Microsoft Corp.

- Northrop Grumman Corp.

- Oracle Corp.

- Palantir Technologies Inc.

- RTX Corp.

- SAP SE

- Thales Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Defense it spending market

- In November, 2024, Lockheed Martin announced a strategic partnership with a leading AI firm to accelerate the development of autonomous systems for reconnaissance missions, focusing on edge computing integration.

- In April, 2025, the regional presence of international technology groups was bolstered by significant acquisitions, such as Visma’s expansion in Argentina, signaling a broader trend of digitizing operational frameworks within government sectors.

- In May, 2025, the Microsoft Digital Crimes Unit collaborated with the United States Department of Justice and Europol to execute a landmark disruption operation against the Lumma Stealer malware-as-a-service platform.

- In May, 2025, the Department of Defense launched the Software Fast Track (SWIFT) initiative to accelerate technical modernization by introducing automated continuous risk monitoring and zero trust compliance frameworks into the procurement cycle.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Defense IT Spending Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 313 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 26876.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, Israel, UAE, Turkey, South Africa, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The defense IT spending market is evolving from a hardware-centric model to one dominated by software-defined platforms and cognitive computing. This transition is driven by the need to manage vast data streams from the internet of military things (IoMT) and achieve digital overmatch in multi-domain operations.

- Investments are concentrated in high-performance computing clusters and secure data lakes to support generative artificial intelligence and predictive maintenance algorithms. The mandatory adoption of zero trust architecture and post-quantum cryptography directly impacts boardroom decisions on long-term cybersecurity investments and compliance strategies, especially with the rise of adversarial machine learning threats.

- Integrating technologies like agentic teammates and battlefield management systems into a cohesive C4ISR system is critical. Organizations leveraging these advanced frameworks have reported a 30% reduction in data processing times, enhancing their ability to conduct offensive cyber operations and maintain technological superiority. The focus remains on deploying ruggedized hardware and immersive training technologies to ensure force readiness.

What are the Key Data Covered in this Defense IT Spending Market Research and Growth Report?

-

What is the expected growth of the Defense IT Spending Market between 2026 and 2030?

-

USD 26.88 billion, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Service, Software, and Hardware), Application (Cyber security, IT infrastructure, Logistic and asset management, and Others), Deployment (On-premises, and Cloud) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of generative artificial intelligence and autonomous combat systems, Sovereign cloud integration and digital autonomy mandates

-

-

Who are the major players in the Defense IT Spending Market?

-

Amazon Web Services Inc., BAE Systems Plc, Booz Allen Hamilton Corp., CACI International Inc., CGI Inc., DXC Technology Co., General Dynamics Corp., IBM Corp., Indra Group, L3Harris Technologies Inc., Leidos Holdings Inc., Leonardo S.p.A., Lockheed Martin Corp., Microsoft Corp., Northrop Grumman Corp., Oracle Corp., Palantir Technologies Inc., RTX Corp., SAP SE and Thales Group

-

Market Research Insights

- The market's dynamics are shaped by a strategic shift toward data-centric warfare and digital overmatch, compelling force modernization across all domains. The adoption of advanced battlefield analytics has improved threat identification accuracy by 30%, while the integration of resilient communications ensures information superiority in contested environments.

- This transition is supported by enhanced decision support systems, which have demonstrated a 20% reduction in response times for mission-critical workloads. As military organizations prioritize operational readiness and technological superiority, investments are increasingly directed toward technologies that facilitate network-centric warfare and secure the supply chain. These strategic imperatives drive the continuous evolution of defense IT infrastructure and its applications.

We can help! Our analysts can customize this defense it spending market research report to meet your requirements.

RIA -

RIA -