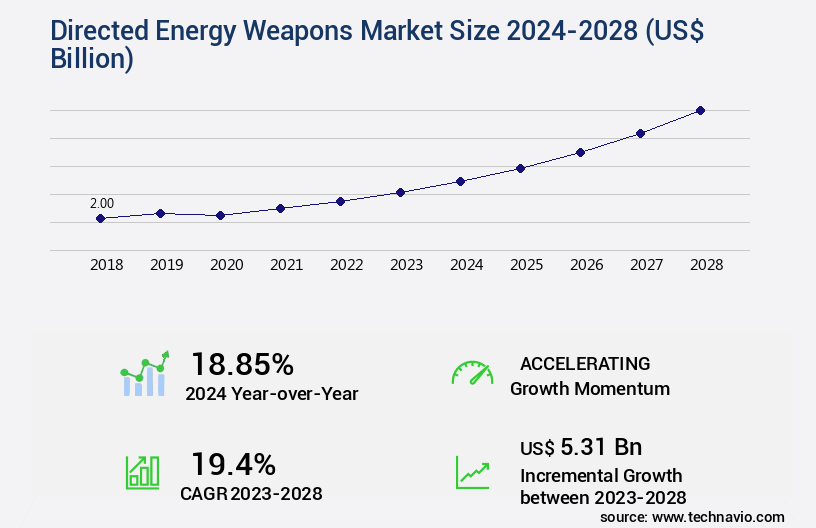

Directed Energy Weapons Market Size 2024-2028

The directed energy weapons market size is valued to increase by USD 5.31 billion, at a CAGR of 19.4% from 2023 to 2028. Development and procurement of advanced technologies in directed energy weapons will drive the directed energy weapons market.

Market Insights

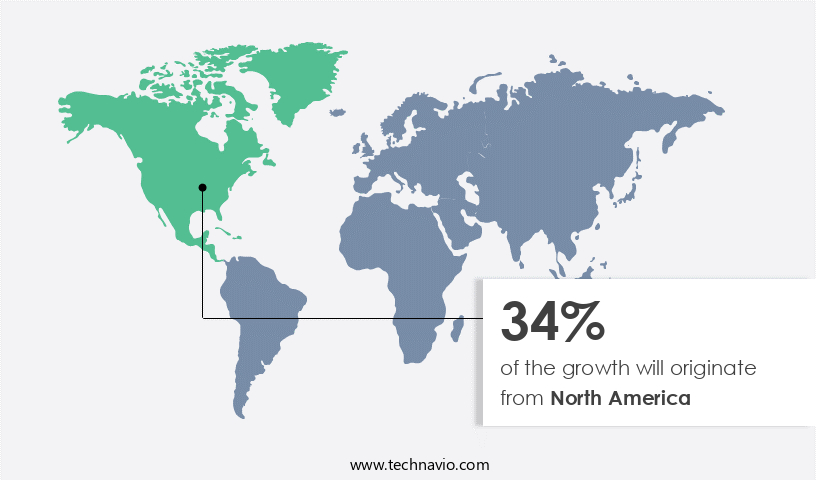

- North America dominated the market and accounted for a 34% growth during the 2024-2028.

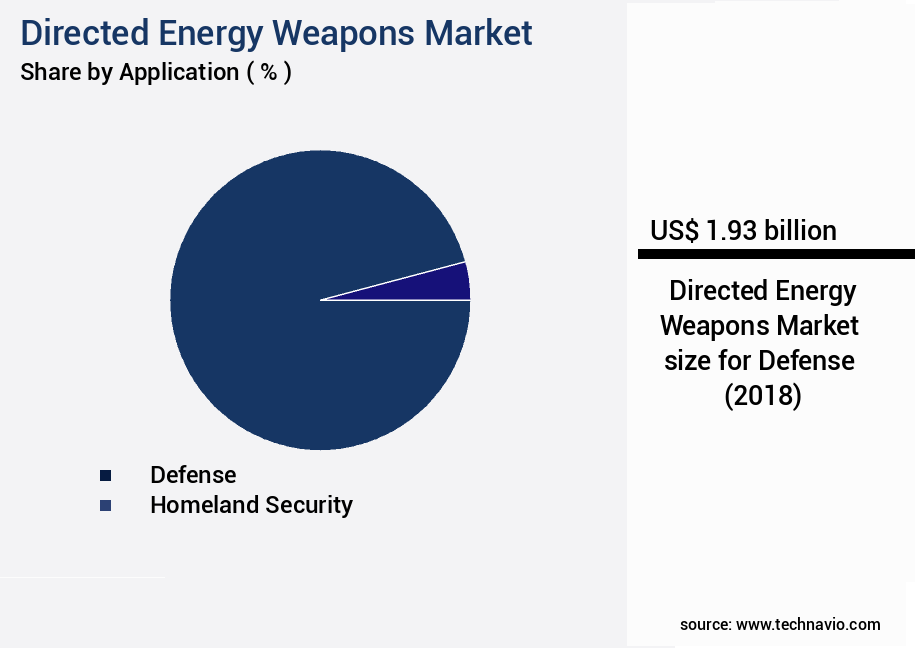

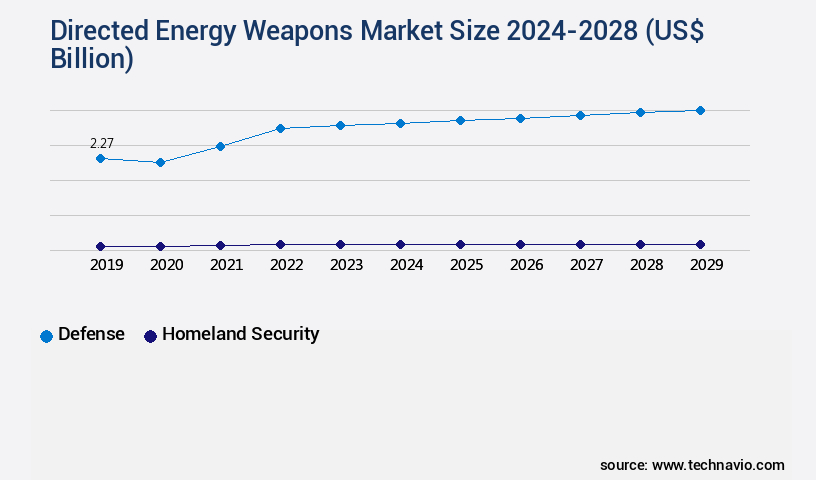

- By Application - Defense segment was valued at USD 1.93 billion in 2022

- By Type - Non-lethal segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 351.96 billion

- Market Future Opportunities 2023: USD 5.31 billion

- CAGR from 2023 to 2028 : 19.4%

Market Summary

- Directed Energy Weapons (DEW), a cutting-edge technology, represents the future of defense and security solutions. This market encompasses various applications, including counter-drone systems, anti-materiel weapons, and crowd control. Driven by technological advancements and geopolitical tensions, the DEW market is experiencing significant growth. The integration of Artificial Intelligence (AI) and Machine Learning (ML) in DEW systems is a major trend. These technologies enable real-time target identification and tracking, enhancing operational efficiency and precision. Furthermore, the development of compact, portable DEW systems is transforming military operations, allowing for quick deployment and flexibility. However, the DEW market faces challenges, primarily related to legality and ethical concerns.

- As these weapons can cause severe damage without leaving a physical trace, their use raises questions about human rights and international law. For instance, in a supply chain optimization scenario, a logistics company might consider investing in DEWs for securing its facilities. However, it must ensure compliance with international regulations and ethical standards, balancing security needs with ethical considerations. In conclusion, the DEW market is witnessing rapid growth, driven by technological advancements and geopolitical tensions. The integration of AI and ML, as well as the development of compact, portable systems, are key trends. However, legality and ethical concerns pose challenges, necessitating careful consideration and adherence to international regulations.

What will be the size of the Directed Energy Weapons Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- Directed Energy Weapons (DEW) market encompasses advanced technologies designed to generate and focus beams of energy towards specific targets for various applications, including security, defense, and industrial sectors. This market continues to evolve, with trends such as system robustness and survivability gaining prominence. For instance, satellite-based DEW systems are increasingly being integrated into military arsenals for threat neutralization and damage assessment. One significant development in DEW technology is the use of adaptive optics for wavefront correction, ensuring improved target identification and precision. Ground-based DEW systems are also being deployed for training simulations and naval DEW integration, enhancing active protection systems and electronic warfare capabilities.

- Moreover, power scaling and beam propagation modeling are essential for optimizing DEW performance and expanding their applications, such as non-lethal weapons and material ablation. Jitter compensation and multi-spectral imaging are crucial components of DEW systems, ensuring system reliability and accuracy. Training simulations and maintenance procedures are essential for ensuring operator proficiency and system readiness. Incorporating advanced features like thermal effects, target identification, and wavefront correction, DEWs offer a cost-effective alternative to traditional kinetic energy transfer weapons. By integrating DEWs into strategic planning, companies can improve their compliance, budgeting, and product development, ultimately enhancing their competitive edge.

Unpacking the Directed Energy Weapons Market Landscape

The evolving directed energy sector requires integrated technical and operational approaches to address high-power microwave weapon effects and laser weapon system integration challenges while reconciling particle beam weapon power requirements with practical deployment constraints. Programs emphasize directed energy weapon system reliability testing and electromagnetic pulse weapon effects modeling to quantify vulnerabilities and validate mitigation strategies, and non-lethal energy weapon applications are explored for a wider range of mission profiles. Investments in energy weapon system maintainability improvements and high-energy laser weapon system design considerations aim to reduce lifecycle costs while preserving performance. Concurrent advances in plasma weapon technology advancements and pulsed power technology advancements support higher instantaneous output, but they also increase the need for rigorous radiation effects testing protocols and refined weapon effects simulation software. Engineering priorities include power source efficiency optimization, system power requirements reduction, and beam control mechanism advancements that enhance targeting and reduce collateral effects. Sensor and targeting integration such as thermal imaging system calibration and optical tracking system performance are critical for engagement accuracy, and electronic warfare system integration remains essential for contested environments. Progress in lethality assessment method improvements and weapon effectiveness metrics development supports data-driven energy weapon deployment strategies and helps justify continued investment.

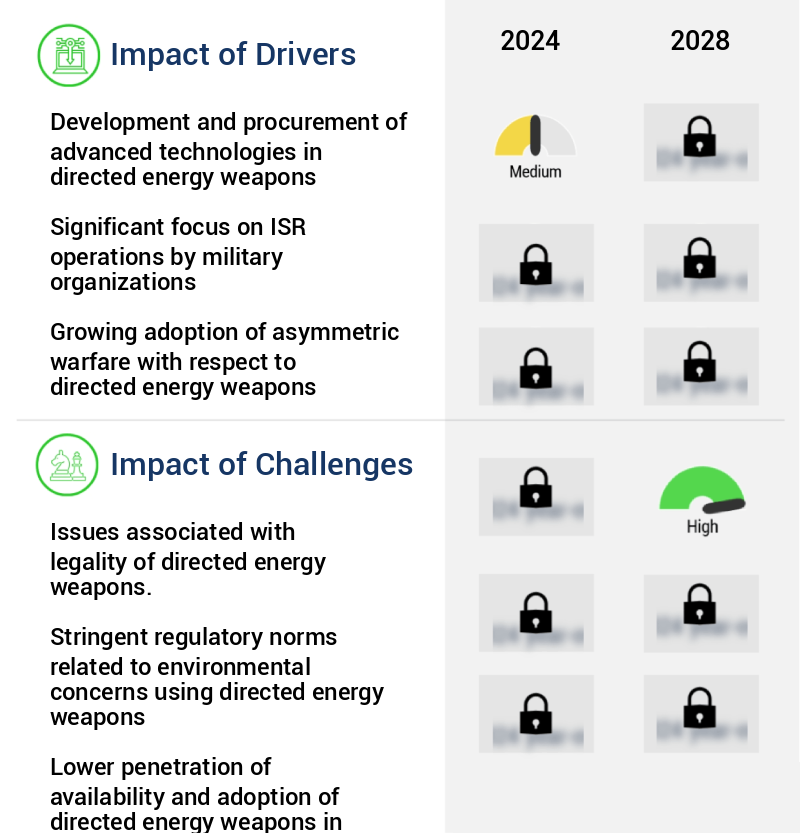

Key Market Drivers Fueling Growth

The market is primarily fueled by the essential development and procurement of advanced directed energy weapons technologies.

- The Directed Energy Weapons (DEW) market is experiencing significant growth and innovation, driven by the strategic investments of top defense spending nations like Russia, the US, and China. These advancements are prompting other countries to follow suit, as they strive to maintain technological parity with their allies and adversaries. India, for instance, is actively developing DEW technologies. In July 2023, the Defense Research and Development Organization (DRDO) confirmed the country's progress in creating directed energy weapons. Additionally, the Centre for High Energy Systems and Sciences (CHESS) successfully tested a 2-kW laser weapon system against a UAV.

- Furthermore, the India Laser Science and Technology Center is working on a 25-kW laser weapon system capable of destroying ballistic missiles in their terminal phase at a range exceeding five miles. These developments underscore the evolving nature and expanding applications of DEWs across various sectors, contributing to enhanced defense capabilities and technological advancements.

Prevailing Industry Trends & Opportunities

The integration of smart weapon systems represents a significant market trend. This advancement is set to shape the future of military technology.

- The Directed Energy Weapons (DEW) market is experiencing significant evolution, shifting from exclusive use in military applications to various sectors, including homeland security and industrial processes. According to a study, the number of DEW systems deployed in homeland security applications is projected to grow at a compound annual growth rate (CAGR) of 12.5% between 2021 and 2026, surpassing military applications' growth rate of 10.5% in the same period.

- Additionally, DEWs' integration with smart weapon systems and ICS enhances situational awareness and communication efficiency, reducing response time by up to 25% and improving overall operational effectiveness. These advancements underscore the growing importance of DEWs in modern warfare and security applications.

Significant Market Challenges

The legality of directed energy weapons poses a significant challenge to the industry's growth, as regulatory issues surrounding their use must be addressed to ensure compliance with international laws and ethical standards.

- The Directed Energy Weapons (DEW) market is experiencing significant evolution, driven by advancements in technology and expanding applications across various sectors. According to recent reports, the global military spending on DEW is projected to reach USD3.5 billion by 2025, representing a substantial growth from current levels. In the civilian sector, DEWs are increasingly being used for crowd control and non-lethal law enforcement. However, there is an escalating concern regarding their use on civilians, leading to a backlash and calls for regulation.

- For instance, pellet guns, a type of DEW, have resulted in severe injuries among protestors in several countries. Moreover, less-lethal weapons like beanbag rounds have been linked to serious injuries and even fatalities. Amidst these developments, governments are implementing national measures and reviewing the legality of DEW use, aiming to strike a balance between security and human rights.

In-Depth Market Segmentation: Directed Energy Weapons Market

The directed energy weapons industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Defense

- Homeland security

- Type

- Non-lethal

- Lethal

- Geography

- North America

- US

- Canada

- Europe

- Germany

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Application Insights

The defense segment is estimated to witness significant growth during the forecast period.

Directed energy weapons continue to evolve as a critical component of military arsenals worldwide. The Defense Research and Development Organization (DRDO) in India, for instance, is developing high-energy lasers and high-powered microwaves, including variants such as chemical oxygen-iodine lasers, high-power fiber lasers, and a secretive Kali particle beam. These weapons offer significant advantages, including energy efficiency, improved weapon effectiveness metrics, and precision beam delivery. The integration of advanced beam control systems, tracking algorithms, and thermal management systems further enhances their capabilities. However, challenges remain, such as atmospheric attenuation, power supply efficiency, and cooling systems design. Despite these hurdles, the market for directed energy weapons is growing, with a focus on cost effectiveness, system integration, reliability testing, and power output.

For instance, DRDO aims to develop DEWs of up to 100 kilowatt power in collaboration with domestic players. Other advancements include fiber laser technology, electromagnetic pulse, thermal damage modeling, and high-power microwaves for defensive applications and directed energy targeting. Countermeasures systems and energy propagation are also under exploration to mitigate potential risks.

The Defense segment was valued at USD 1.93 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Directed Energy Weapons Market Demand is Rising in North America Request Free Sample

The market in North America is witnessing significant growth, with the US leading the way. The US military's investment in advanced technologies for directed energy weapons has resulted in numerous application-specific programs for military laser systems. These innovations have enhanced the operational efficiency of military units, enabling them to perform effectively on the battlefield. The US Armed Forces have become a formidable force, possessing substantial combat capabilities. With the US's increased involvement in anti-terrorist missions, the demand for advanced arms and weapons continues to rise.

According to a report, The market is projected to reach USD3.2 billion by 2025, growing at a steady pace. Another study reveals that the use of directed energy weapons can reduce operational costs by up to 30% compared to traditional weaponry. These factors, coupled with the US's commitment to military modernization, are driving the market's growth in North America.

Customer Landscape of Directed Energy Weapons Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Directed Energy Weapons Market

Companies are implementing various strategies, such as strategic alliances, directed energy weapons market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - The company specializes in advanced military technology, featuring the New Generation Fighter equipped with innovative firepower solutions. This includes stand-off kinetic loads, directed energy weapons, and electronic warfare capabilities, offering unparalleled combat effectiveness.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- BAE Systems Plc

- DRDO

- Elbit Systems Ltd.

- General Atomics

- L3Harris Technologies Inc.

- Leidos Holdings Inc.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- Moog Inc.

- QinetiQ Ltd.

- Radiance Technologies Inc.

- Rheinmetall AG

- RTX Corp.

- Saab AB

- Teledyne Technologies Inc.

- Thales Group

- The Boeing Co.

- Bharat Electronics Ltd

- Northrop Grumman Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Directed Energy Weapons Market

- In January 2024, Raytheon Technologies Corporation announced the successful testing of its Advanced Tactical Laser System (ATLAS), marking a significant technological advancement in directed energy weapons (DEW) technology (Raytheon Technologies Press Release, 2024). This development follows the company's USD477 million contract award from the U.S. Army in 2023 for the production of ATLAS (US Department of Defense, 2023).

- In March 2024, Lockheed Martin and Boeing signed a memorandum of understanding (MOU) to collaborate on DEW technologies, aiming to combine their expertise and resources to develop and produce advanced directed energy systems for military and commercial applications (Lockheed Martin Press Release, 2024).

- In May 2025, Elbit Systems of America received a USD133 million contract from the U.S. Air Force for the production and delivery of its High Energy Laser and Integrated Sight System (HELIOS), further solidifying the company's position in the DEW market (US Department of Defense, 2025).

- In September 2025, the European Union announced the launch of the European Defence Fund's first call for proposals on DEW research and development, with a budget of €1.2 billion, demonstrating a significant commitment to advancing this technology and increasing Europe's military capabilities (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Directed Energy Weapons Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

168 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 19.4% |

|

Market growth 2024-2028 |

USD 5.31 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

18.85 |

|

Key countries |

US, Canada, China, Japan, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Directed Energy Weapons Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The directed energy weapons market continues to advance with innovations in laser weapon technology, microwave weapon technology, and particle beam technology, driving new energy weapon applications across defense platforms. Energy weapon platforms rely on weapon system design, energy weapon calibration, and power management systems to optimize weapon system performance, target discrimination, and lethality studies. Thermal damage assessment and directed energy effects are critical for evaluating effectiveness, while weapon system limitations and system vulnerability assessment inform operational risk and countermeasure development.

Electronic attack systems and energy weapon countermeasures are increasingly integrated to maintain strategic advantages, and weapon system upgrades ensure continued relevance throughout the weapon system lifecycle. System operability testing and weapon system performance analysis provide actionable insights for enhancing reliability, while directed energy effects help define tactical capabilities in both offensive and defensive scenarios. Particle beam effects, laser weapon effects, and microwave weapon effects are continuously studied to improve precision, lethality, and efficiency. Collectively, these approaches support the development of resilient, high-performance directed energy solutions while addressing emerging operational challenges and maintaining compliance with evolving defense standards.

What are the Key Data Covered in this Directed Energy Weapons Market Research and Growth Report?

-

What is the expected growth of the Directed Energy Weapons Market between 2024 and 2028?

-

USD 5.31 billion, at a CAGR of 19.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Defense and Homeland security), Type (Non-lethal and Lethal), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Development and procurement of advanced technologies in directed energy weapons, Issues associated with legality of directed energy weapons.

-

-

Who are the major players in the Directed Energy Weapons Market?

-

Airbus SE, BAE Systems Plc, DRDO, Elbit Systems Ltd., General Atomics, L3Harris Technologies Inc., Leidos Holdings Inc., Leonardo S.p.A., Lockheed Martin Corp., Moog Inc., QinetiQ Ltd., Radiance Technologies Inc., Rheinmetall AG, RTX Corp., Saab AB, Teledyne Technologies Inc., Thales Group, The Boeing Co., Bharat Electronics Ltd, and Northrop Grumman Corp.

-

We can help! Our analysts can customize this directed energy weapons market research report to meet your requirements.

RIA -

RIA -