Fiber Laser Market Size 2026-2030

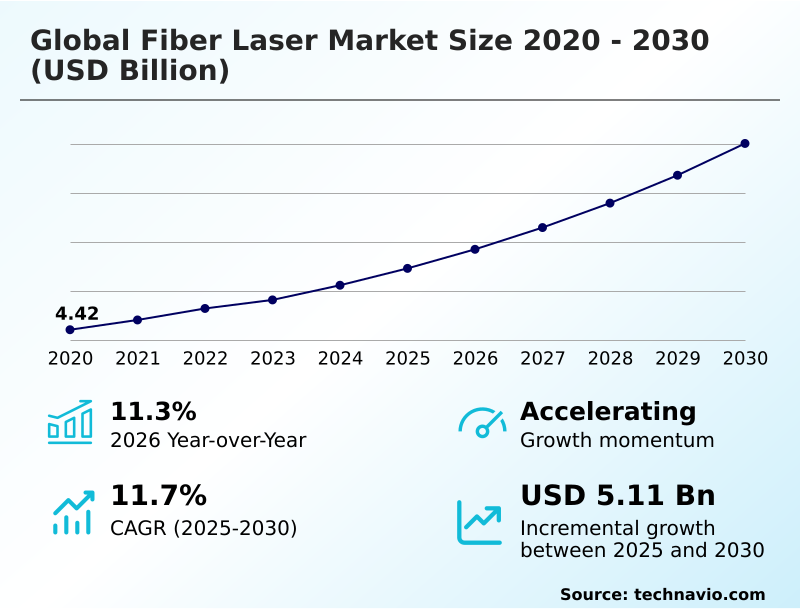

The fiber laser market size is valued to increase by USD 5.11 billion, at a CAGR of 11.7% from 2025 to 2030. Expanding automotive electrification and precision manufacturing will drive the fiber laser market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 31% growth during the forecast period.

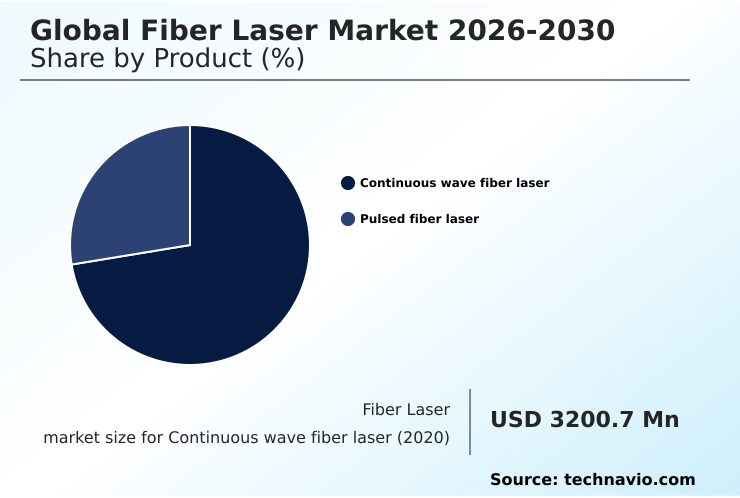

- By Product - Continuous wave fiber laser segment was valued at USD 4.47 billion in 2024

- By Application - Material processing segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 7.62 billion

- Market Future Opportunities: USD 5.11 billion

- CAGR from 2025 to 2030 : 11.7%

Market Summary

- The fiber laser market is foundational to the evolution of advanced manufacturing, driven by the need for higher precision and efficiency in industrial processes. This technology, utilizing mediums like ytterbium-doped fiber or an erbium-doped gain medium within specialty optical fibers, enables superior material processing.

- A key trend is the adoption of pulsed fiber laser systems, including femtosecond pulse laser technology for delicate tasks in semiconductor manufacturing and medical device fabrication. Simultaneously, the integration of smart manufacturing solutions is transforming operations. For instance, an aerospace components manufacturer can now employ digital twin technology to model a laser processing workflow in real-time.

- This allows for the application of predictive maintenance algorithms to anticipate equipment needs, minimizing downtime and ensuring the consistent quality of critical parts without the high costs associated with unexpected failures. The high capital investment, however, tempers adoption rates among smaller enterprises.

What will be the Size of the Fiber Laser Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Fiber Laser Market Segmented?

The fiber laser industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

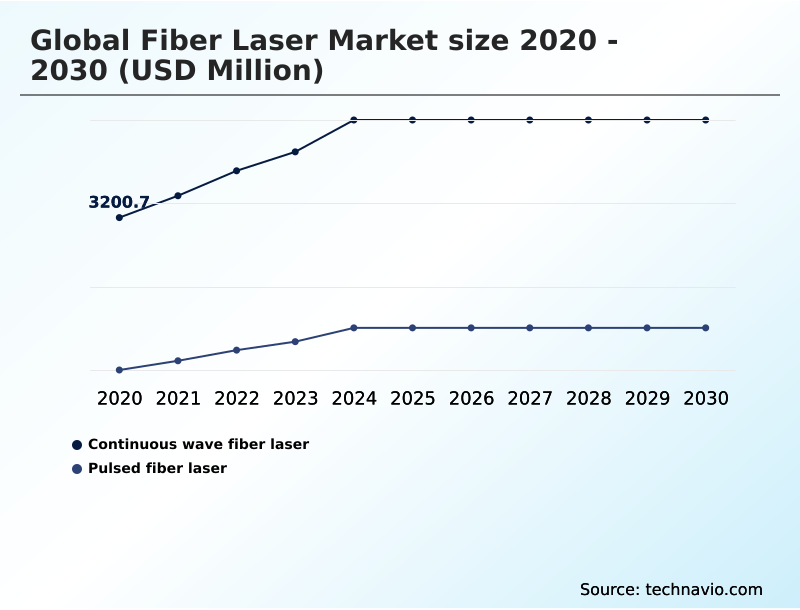

- Continuous wave fiber laser

- Pulsed fiber laser

- Application

- Material processing

- Advanced applications

- Healthcare

- Others

- Type

- Infrared

- Ultrafast

- Ultraviolet

- Visible

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Product Insights

The continuous wave fiber laser segment is estimated to witness significant growth during the forecast period.

The market is significantly defined by the continuous wave fiber laser segment, which is integral to modern industrial automation systems.

These systems provide a constant energy output, making them indispensable for heavy-duty tasks like high-speed metal cutting and the precision welding required in battery manufacturing.

The core architecture, featuring a robust laser resonator and high-power pump diodes feeding an active optical fiber cladding, ensures high reliability and minimal maintenance.

Advancements in beam shaping technology and the integration of features like on-the-fly welding and deep weld quality sensing are enhancing the capabilities of these multi-kilowatt systems.

As a result, this type of laser source achieves up to 40% higher wall-plug efficiency than legacy systems, solidifying its role in mass production environments.

The Continuous wave fiber laser segment was valued at USD 4.47 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 31% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Fiber Laser Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the fiber laser market is diverse, with regional specializations driving innovation.

APAC, contributing over 31% of the market's incremental growth, leads in high-volume manufacturing, employing infrared fiber laser systems for applications like photovoltaic cell scribing and flexible display production.

North America, with an 11.3% year-over-year expansion rate, is a hub for R&D, focusing on advanced applications such as remote sensing technology and medical systems using holmium-doped fiber lasers for optical coherence tomography.

Europe excels in precision engineering, integrating robotic arm integration and advanced beam delivery components.

Innovations in non-linear crystals and chirped pulse amplification for specialized thulium-doped fiber laser systems are prominent in European and North American research centers, enabling advanced non-contact processing techniques.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The Global Fiber Laser Market 2026-2030 continues its expansion, driven by the clear advantages of the technology over legacy systems. When evaluating the benefits of fiber laser vs co2 laser, users consistently point to superior energy efficiency and lower maintenance, addressing the high cost of ownership for industrial fiber lasers.

- The use of a high power fiber laser for metal cutting, particularly an infrared fiber laser for steel processing, has become an industry standard for speed and precision. In advanced applications, fiber laser welding for automotive battery manufacturing is critical, with green fiber laser for copper welding solving key challenges in joining dissimilar, highly reflective metals.

- The precision of ultrafast fiber laser for medical device fabrication is unmatched, enabling complex micro-structures. Furthermore, the role of fiber lasers in industry 4.0 is expanding through fiber laser integration with robotic automation, with some automated lines achieving a 40% reduction in cycle times compared to manual processes.

- Advancements in high-brightness fiber lasers and femtosecond lasers for cold ablation techniques are opening new possibilities in aerospace engineering and semiconductor lithography. However, challenges in fiber laser system maintenance and adhering to safety standards for kilowatt-class laser systems require ongoing focus.

- This has led to the development of digital twin modeling for laser processing and predictive maintenance for fiber laser systems, which promise to improve wall-plug efficiency in fiber lasers and streamline operations.

What are the key market drivers leading to the rise in the adoption of Fiber Laser Industry?

- The expansion of automotive electrification, coupled with the rising demand for precision manufacturing across multiple sectors, serves as a key driver for market growth.

- Market growth is propelled by several key drivers. The global shift toward Industry 4.0 is a primary catalyst, demanding automated cutting cells and smart factories where fiber lasers are a cornerstone laser source.

- This trend has resulted in a 30% reduction in production errors in some automated facilities. The automotive industry's transition to electric vehicles fuels demand for on-the-fly welding and laser-based cleaning of battery components.

- In parallel, continuous photonic innovation is expanding capabilities into new domains, from ultraviolet fiber laser systems for laser-based lithography in electronics to kilowatt-class directed energy systems for laser defense solutions.

- Furthermore, the rise of additive manufacturing and 3D printing workflows, which rely on precise laser control, is opening new avenues for complex component fabrication across aerospace and healthcare, where fiber lasers are also used in advanced flow cytometry.

What are the market trends shaping the Fiber Laser Industry?

- A key market trend is the proliferation of ultra-high-power fiber lasers within heavy industry. This shift is driven by intensifying demands for greater processing speeds and enhanced material capabilities.

- Key market trends are pushing the boundaries of laser-integrated machinery and performance. The proliferation of ultra-high-power systems with a high-brightness beam is enabling faster processing, with some achieving a 20% increase in cutting speed on thick metals.

- Simultaneously, advancements in ultrafast picosecond laser systems are revolutionizing micro-machining and surface engraving through cold ablation processing, which reduces the heat-affected zone by over 90%. This is critical for delicate electronics and medical devices. Innovations in rare earth dopants are also leading to more efficient blue fiber laser and green fiber laser sources for processing reflective metals.

- Furthermore, the integration of AI with optical sub-systems is enabling smart functionalities like laser annealing optimization and even novel applications like automated laser-based weeding, driving gains in wall-plug efficiency.

What challenges does the Fiber Laser Industry face during its growth?

- The high initial capital expenditure and total cost of ownership for advanced systems present a key challenge affecting widespread industry adoption and growth.

- Despite strong growth drivers, the fiber laser market faces notable challenges. The high initial capital expenditure for advanced laser processing systems, often 2-3 times that of conventional equipment, remains a significant barrier for small and medium-sized enterprises. This financial hurdle is compounded by the rapid pace of technological obsolescence.

- Furthermore, there is a pronounced scarcity of skilled technicians capable of operating and maintaining these complex systems, which incorporate sensitive components like fiber bragg grating sensors. This skills gap can lead to extended operational downtime, with facilities reporting up to 15% of potential production hours lost to maintenance delays.

- Navigating the complex and varied web of international safety regulations and compliance standards also adds significant operational overhead and can slow market entry for new products.

Exclusive Technavio Analysis on Customer Landscape

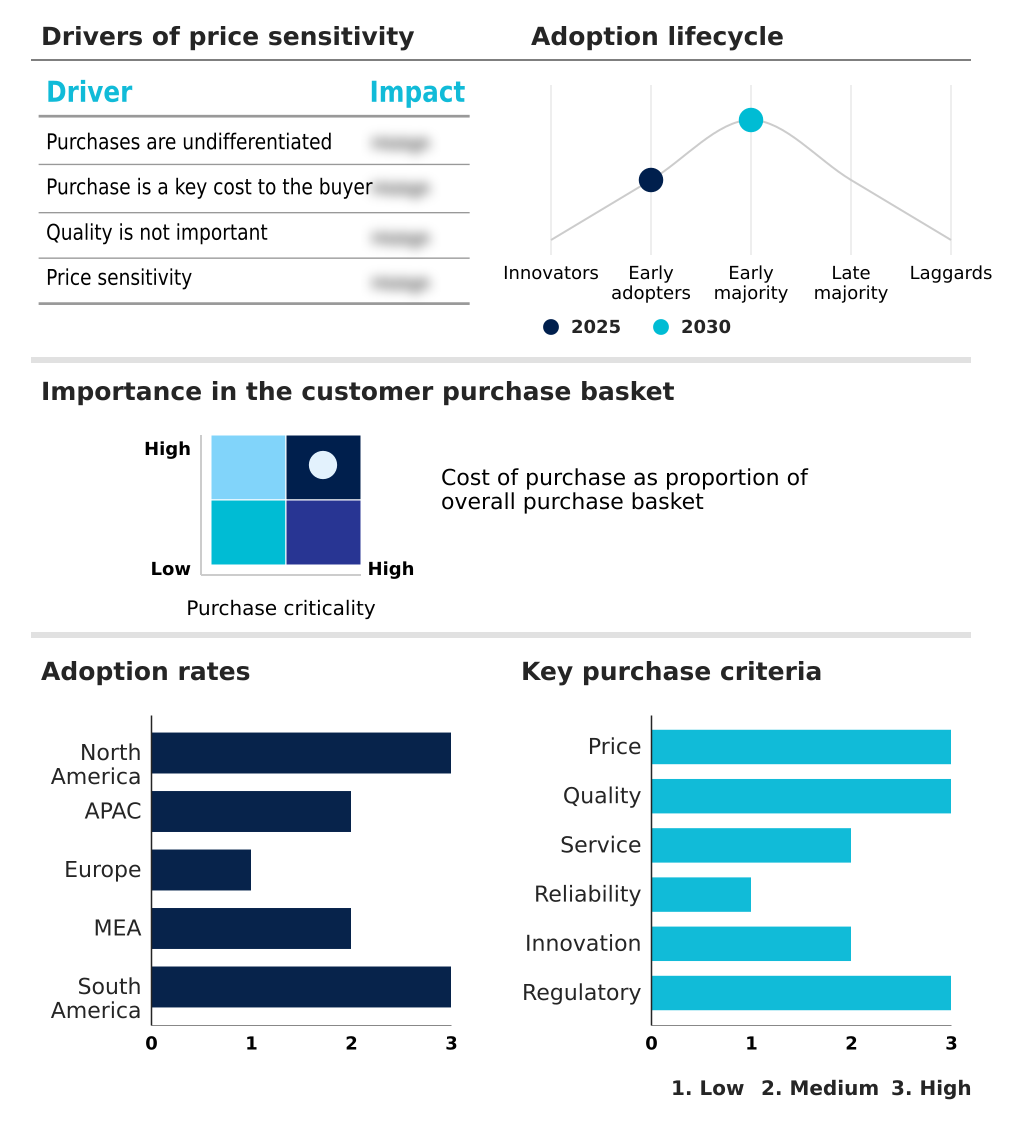

The fiber laser market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the fiber laser market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Fiber Laser Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, fiber laser market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AMADA WELD TECH - Precision fiber laser systems for welding, marking, and micromachining address critical needs within the global manufacturing sector, enhancing operational accuracy and throughput.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMADA WELD TECH

- Bodor Laser

- Bystronic Laser AG

- Calmar Laser Inc.

- Coherent Corp.

- CY Laser Srl

- Fujikura Co. Ltd.

- Hans Laser Technology Co. Ltd.

- HGLaser Engineering Co. Ltd.

- IPG Photonics Corp.

- Jenoptik AG

- Lead Lasers

- Lumentum Holdings Inc.

- Maxphotonics

- Mitsubishi Electric Corp.

- MKS Instruments Inc.

- nLIGHT Inc.

- TOPTICA Photonics AG

- TRUMPF SE Co. KG

- Wuhan Raycus Fiber Laser Tech Co Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fiber laser market

- In March 2025, TRUMPF SE Co. KG announced a new series of picosecond laser systems designed to enhance micro-machining precision for the semiconductor and medical device fabrication sectors.

- In January 2025, Coherent Corp. finalized its acquisition of a German-based specialty optical fiber manufacturer, furthering its vertical integration strategy for next-generation laser sources.

- In November 2024, IPG Photonics Corp. announced a strategic partnership with a leading robotics firm to develop fully integrated, automated cutting cells for the automotive industry.

- In September 2024, nLIGHT Inc. received a major government contract to develop kilowatt-class directed energy systems for advanced laser defense solutions, leveraging its high-brightness beam technology.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fiber Laser Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.7% |

| Market growth 2026-2030 | USD 5108.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 11.3% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Fiber Laser Market is evolving from a niche technology to a cornerstone of advanced industrial production, driven by its superior performance characteristics. The core technology, based on mediums like ytterbium-doped fiber, erbium-doped gain medium, and thulium-doped fiber laser sources, is constantly refined through innovations in high-power pump diodes and specialty optical fibers.

- Boardroom decisions increasingly center on the strategic adoption of these systems, weighing the high initial CAPEX against long-term operational gains. The integration of predictive maintenance algorithms and digital twin technology into laser-integrated machinery allows for a 30% reduction in unplanned downtime.

- This shift is particularly evident with the adoption of pulsed fiber laser technologies, including femtosecond pulse laser and picosecond laser systems, which enable cold ablation processing for delicate materials. Advanced features such as on-the-fly welding, deep weld quality sensing, and sophisticated beam shaping technology, are becoming standard.

- From laser-based lithography and optical coherence tomography to additive manufacturing workflows, the technology’s versatility is reshaping industries.

What are the Key Data Covered in this Fiber Laser Market Research and Growth Report?

-

What is the expected growth of the Fiber Laser Market between 2026 and 2030?

-

USD 5.11 billion, at a CAGR of 11.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Continuous wave fiber laser, and Pulsed fiber laser), Application (Material processing, Advanced applications, Healthcare, and Others), Type ( Infrared, Ultrafast, Ultraviolet, and Visible) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Expanding automotive electrification and precision manufacturing, High initial capital expenditure and cost of ownership

-

-

Who are the major players in the Fiber Laser Market?

-

AMADA WELD TECH, Bodor Laser, Bystronic Laser AG, Calmar Laser Inc., Coherent Corp., CY Laser Srl, Fujikura Co. Ltd., Hans Laser Technology Co. Ltd., HGLaser Engineering Co. Ltd., IPG Photonics Corp., Jenoptik AG, Lead Lasers, Lumentum Holdings Inc., Maxphotonics, Mitsubishi Electric Corp., MKS Instruments Inc., nLIGHT Inc., TOPTICA Photonics AG, TRUMPF SE Co. KG and Wuhan Raycus Fiber Laser Tech Co Ltd.

-

Market Research Insights

- The market is characterized by dynamic shifts toward smart manufacturing solutions and industrial automation systems. The adoption of laser processing for material processing applications such as precision welding and metal cutting continues to accelerate, with integrated systems reducing material waste by up to 15% compared to traditional methods.

- In high-value sectors, the demand for non-contact processing is driving innovation in micro-machining for medical device fabrication and semiconductor manufacturing. The use of multi-kilowatt systems in automated cutting cells is becoming standard in heavy industry, while specialized laser sources, including green and blue fiber lasers, are enabling breakthroughs in battery manufacturing.

- This rapid photonic innovation has led to systems that are over 50% more energy-efficient than legacy technologies, aligning with sustainability goals.

We can help! Our analysts can customize this fiber laser market research report to meet your requirements.

RIA -

RIA -