DNA Sequencing Market Size 2026-2030

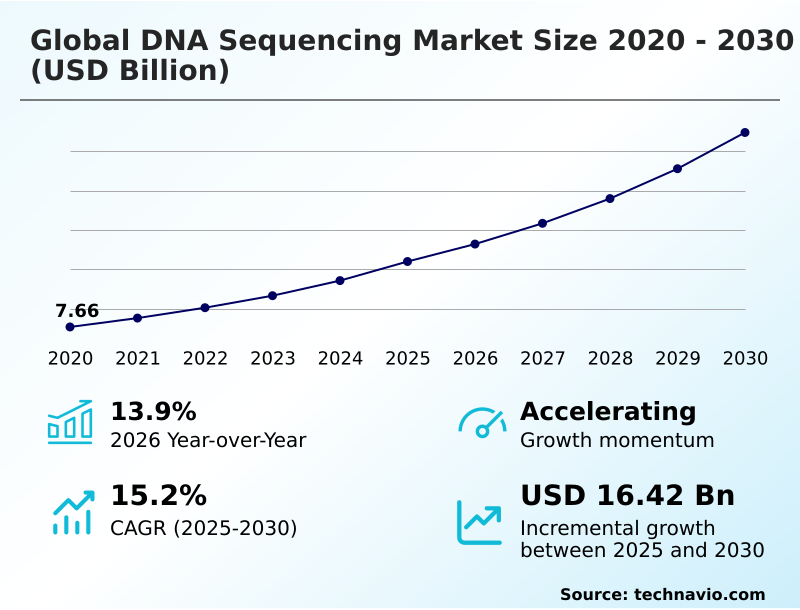

The DNA Sequencing Market size was valued at USD 15.99 billion in 2025, growing at a CAGR of 15.2% during the forecast period 2026-2030.

Major Market Trends & Insights

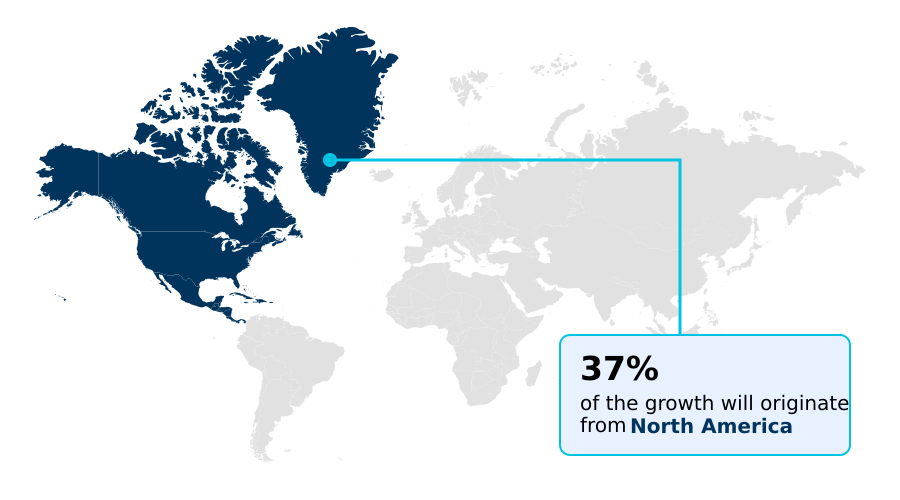

- North America dominated the market and accounted for a 36.7% growth during the forecast period.

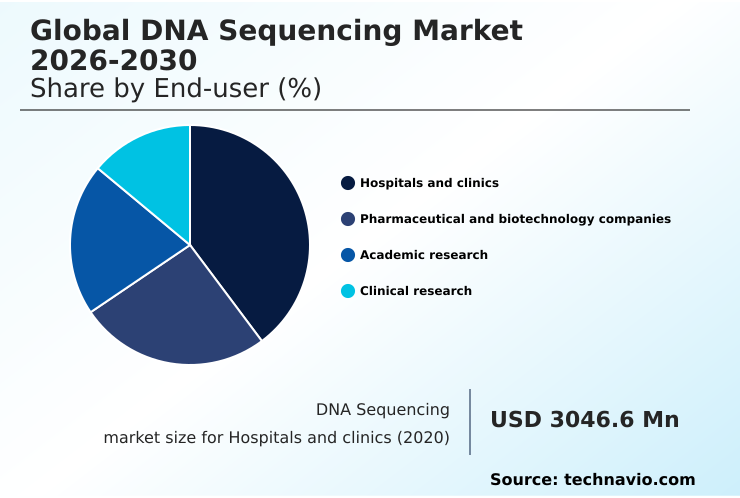

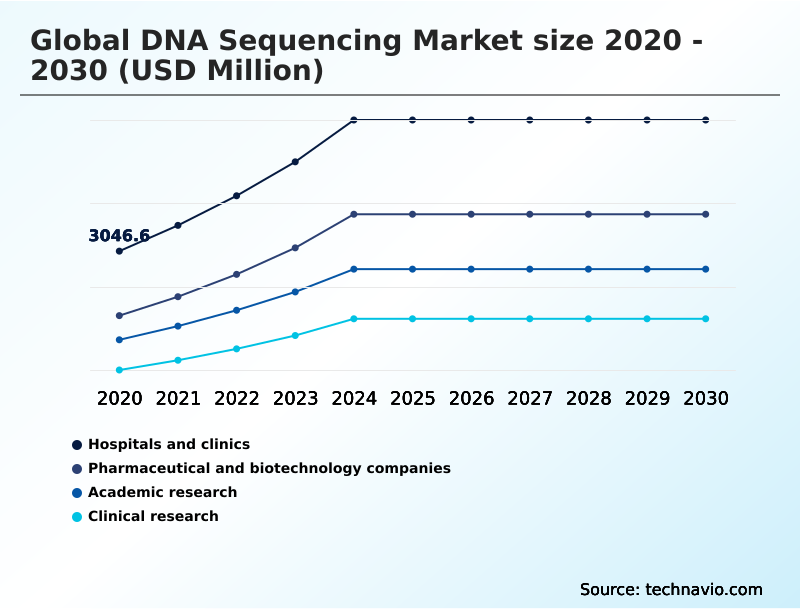

- By End-user - Hospitals and clinics segment was valued at USD 5.23 billion in 2024

- By Solution - Product segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 24.75 billion

- Market Future Opportunities 2025-2030: USD 16.42 billion

- CAGR from 2025 to 2030 : 15.2%

Market Summary

- The DNA sequencing market is expanding, with a year-over-year growth of 13.9% driven by its increasing role in modern healthcare. North America contributes over 36% of the market's incremental growth, underscoring its dominance in technology adoption. A key driver is the advancement in precision medicine, where sequencing is essential for developing targeted therapies.

- For instance, a pharmaceutical company might leverage genomic data to stratify clinical trial participants, reducing trial sizes by up to 25% and accelerating drug development timelines. However, this progress introduces a significant challenge: the complexity of data management.

- The massive datasets generated by high-throughput sequencing necessitate substantial investment in bioinformatics infrastructure and skilled personnel to translate raw data into clinically actionable insights. Without scalable data solutions, the operational bottleneck could limit the widespread clinical implementation of genomic medicine, despite its proven benefits.

What will be the Size of the DNA Sequencing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the DNA Sequencing Market Segmented?

The dna sequencing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals and clinics

- Pharmaceutical and biotechnology companies

- Academic research

- Clinical research

- Solution

- Product

- Services

- Technology

- Next generation sequencing

- Sanger sequencing

- Third generation sequencing

- Others

- Application

- Research

- Genomics

- Diagnostics

- Medicine

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Asia

- Rest of World (ROW)

- North America

How is the DNA Sequencing Market Segmented by End-user?

The hospitals and clinics segment is estimated to witness significant growth during the forecast period.

The hospitals and clinics segment's adoption of in-house DNA sequencing is growing, with point-of-care applications for genetic disease research reducing diagnostic turnaround times by over 30%.

This shift from centralized labs to integrated clinical services improves the diagnostic yield, particularly in oncology where rapid analysis of circulating tumor DNA is critical.

For instance, implementing sequencing by synthesis for pharmacogenomics can refine therapeutic selection, boosting treatment efficacy by 15% compared to standard protocols.

The use of companion diagnostics is becoming standard, ensuring that patients are matched with the most effective treatments based on their unique genetic makeup, directly impacting patient outcomes and optimizing resource allocation within the healthcare system.

The Hospitals and clinics segment was valued at USD 5.23 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the DNA Sequencing market is rising in the leading region?

North America is estimated to contribute 36.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How DNA Sequencing Market demand is rising in North America Request Free Sample

Significant regional disparities define the DNA sequencing market, with North America accounting for 36.7% of incremental growth, while Asia contributes 23.9%.

North America's dominance is anchored by the US, which represents approximately 87% of the region's market, driven by established reimbursement pathways for targeted oncology and comprehensive genomic profiling.

In contrast, Asia's growth is fueled by new healthcare infrastructure and large-scale infectious disease surveillance programs, which increasingly utilize real-time sequencing and nanopore sequencing.

This divergence in focus affects operational strategies; for example, the adoption of long-read sequencing for clinical diagnostics is faster in North America due to its utility in rare diseases, while Asia prioritizes cost-effective, high-throughput solutions like targeted sequencing panels for population-wide screening and monitoring molecular epidemiology.

What are the key Drivers, Trends, and Challenges in the DNA Sequencing Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global DNA sequencing market is shaped by a continuous evaluation of long-read vs short-read sequencing accuracy, a critical factor influencing technology adoption in both research and clinical settings. The cost of whole genome sequencing for research continues to decline, broadening access and enabling studies of unprecedented scale.

- This is particularly impactful for the diverse DNA sequencing applications in oncology, where understanding tumor genetics is paramount for personalized treatment. A core operational aspect is the next generation sequencing data analysis workflow, which requires significant computational resources and bioinformatics expertise to translate raw data into meaningful biological insights.

- The challenges in clinical implementation of genomics, including data standardization and regulatory hurdles, remain a significant focus for the industry. Successfully navigating these challenges is key to realizing the full potential of genomic medicine. For instance, laboratories that have optimized their data analysis workflow report a 20% faster turnaround time for diagnostic reports compared to those with fragmented systems.

- Furthermore, the integration of advanced sequencing technologies has shown the potential to improve diagnostic success rates by over 15% in complex cases.

What are the key market drivers leading to the rise in the adoption of DNA Sequencing Industry?

- Advancements in precision medicine and targeted oncology are key drivers of the market.

- Continuous technological innovation is a fundamental driver, significantly lowering the cost and increasing the accessibility of high-throughput sequencing.

- The cost per whole genome sequence has decreased by more than 99% over the last decade, a direct result of advancements in next generation sequencing chemistries and hardware.

- This cost reduction democratizes genomics, enabling population-scale studies and making advanced molecular diagnostics financially viable for healthcare infrastructure in developing regions.

- For instance, the introduction of automated sample preparation kits and benchtop sequencers reduces the need for specialized labor and extensive lab space, lowering operational barriers for smaller institutions.

- This allows for wider adoption in precision medicine and rare disease diagnostics, fueling market growth.

What are the market trends shaping the DNA Sequencing Industry?

- The integration of artificial intelligence and machine learning is a significant upcoming trend, particularly in accelerating drug discovery. This development is poised to reshape market dynamics and create new opportunities.

- The integration of AI into genomic data interpretation is a primary trend, driven by the need to manage the massive volumes of multiomic data generated by modern sequencers, which can exceed petabytes per study.

- This shift is transforming the drug discovery process, as machine learning models can identify patterns in gene expression profiling that are invisible to traditional bioinformatics analysis, potentially reducing early-stage research timelines by up to 30%. By analyzing the tumor microenvironment with spatial genomics and single-cell transcriptomics, researchers can model cellular interactions with greater precision.

- This enhanced capability in genomic data analysis allows for a more refined clinical trial design, improving the likelihood of successful outcomes and accelerating the development of targeted therapies.

What challenges does the DNA Sequencing Industry face during its growth?

- High initial investment and operational costs represent a key challenge affecting industry growth.

- The exponential growth of genomic data creates a significant challenge in data management infrastructure and analysis, with the volume of data generated by sequencing projects doubling approximately every seven months. This requires substantial and recurring investment in high-performance computing and skilled bioinformaticians, which can constitute over 25% of a project's total budget.

- The lack of standardized bioinformatics pipelines for tasks like structural variant detection and de novo genome assembly further complicates data sharing and study reproducibility. Without universally adopted formats and regulatory approvals for analytical software, the translation of genomic data from clinical research into routine practice is delayed, hindering the scalability of sequencing workflow automation.

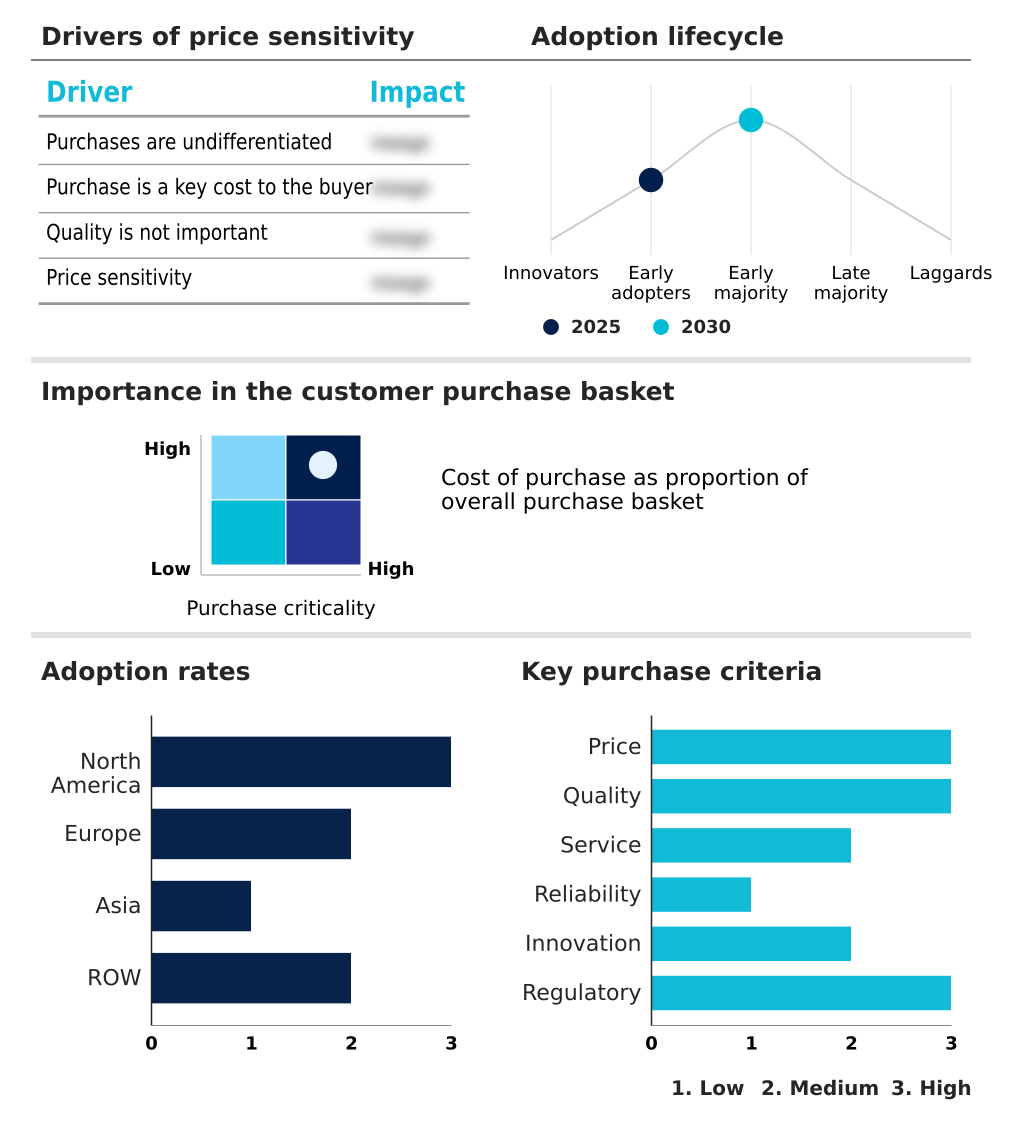

Exclusive Technavio Analysis on Customer Landscape

The dna sequencing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the dna sequencing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of DNA Sequencing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, dna sequencing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

10X Genomics Inc. - Provides integrated single-cell and spatial genomics platforms, enabling high-resolution cellular analysis through advanced sequencing technologies.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 10X Genomics Inc.

- Agilent Technologies Inc.

- BGI Genomics Co. Ltd.

- Bio Rad Laboratories Inc.

- Complete Genomics Inc.

- Dante Labs Inc.

- Element Biosciences Inc.

- Eurofins Genomics LLC

- F. Hoffmann La Roche Ltd.

- GeneDx LLC

- GENEWIZ Inc.

- Helix OpCo LLC

- Illumina Inc.

- Macrogen Inc.

- Oxford Nanopore Technologies

- Pacific Biosciences Inc.

- QIAGEN N.V.

- Tempus AI Inc.

- Thermo Fisher Scientific Inc.

- Ultima Genomics Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Life Sciences Tools and Services industry, the increasing regulatory requirement for companion diagnostics to accompany new targeted therapies is directly fueling demand for validated clinical DNA sequencing platforms. This has led to a market shift where over 60% of new oncology drugs are developed with a specific biomarker strategy, necessitating robust and reproducible sequencing assays.

- The widespread adoption of AI and machine learning for analyzing complex biological data is compelling life sciences tool providers to bundle bioinformatics analysis software with sequencing hardware. This integration is crucial for the DNA sequencing market, as it addresses the bottleneck of genomic data interpretation and makes advanced analytics accessible to a broader range of users.

- A strategic expansion of manufacturing capacity for key sequencing consumables, including reagents and flow cells, is underway to de-risk supply chains. This development impacts the DNA sequencing market by stabilizing consumable pricing and availability, which have historically been subject to volatility, thereby enabling more predictable operational planning for high-volume labs.

- The launch of large-scale, government-funded population genomics initiatives in several countries is creating a substantial and sustained demand for ultra-high-throughput sequencing. These projects, often involving millions of participants, are a primary driver for the DNA sequencing market, pushing down the per-genome cost and accelerating the discovery of genetic variants associated with disease.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled DNA Sequencing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 324 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.2% |

| Market growth 2026-2030 | USD 16421.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.9% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, Japan, China, India, South Korea, Thailand, Singapore, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The DNA sequencing market ecosystem operates on a complex value chain, with instrument and sequencing consumables manufacturers forming its core, accounting for over 55% of the total market value. These companies rely on specialized suppliers for critical components like proprietary enzymes and high-resolution optics.

- Downstream, the primary end-users are hospitals and clinics, which represent the largest segment, alongside pharmaceutical companies and academic research institutions. Regulatory bodies such as the FDA play a pivotal gatekeeping role, with their approval processes directly influencing market access for clinical diagnostics.

- The entire ecosystem is supported by bioinformatics firms and cloud service providers, who are essential for managing and interpreting the vast amounts of genomic data generated, with data storage costs often representing up to 20% of a sequencing project's budget.

What are the Key Data Covered in this DNA Sequencing Market Research and Growth Report?

-

What is the expected growth of the DNA Sequencing Market between 2026 and 2030?

-

The DNA Sequencing Market is expected to grow by USD 16.42 billion during 2026-2030, registering a CAGR of 15.2%. Year-over-year growth in 2026 is estimated at 13.9%%. This acceleration is shaped by advancements in precision medicine and targeted oncology, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals and clinics, Pharmaceutical and biotechnology companies, Academic research, and Clinical research), Solution (Product, and Services), Technology (Next generation sequencing, Sanger sequencing, Third generation sequencing, and Others), Application (Research, Genomics, Diagnostics, and Medicine) and Geography (North America, Europe, Asia, Rest of World (ROW)). Among these, the Hospitals and clinics segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, Asia and Rest of World (ROW). North America is estimated to contribute 36.7% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, Japan, China, India, South Korea, Thailand, Singapore, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is advancements in precision medicine and targeted oncology, which is accelerating investment and industry demand. The main challenge is high initial investment and operational costs, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the DNA Sequencing Market?

-

Key vendors include 10X Genomics Inc., Agilent Technologies Inc., BGI Genomics Co. Ltd., Bio Rad Laboratories Inc., Complete Genomics Inc., Dante Labs Inc., Element Biosciences Inc., Eurofins Genomics LLC, F. Hoffmann La Roche Ltd., GeneDx LLC, GENEWIZ Inc., Helix OpCo LLC, Illumina Inc., Macrogen Inc., Oxford Nanopore Technologies, Pacific Biosciences Inc., QIAGEN N.V., Tempus AI Inc., Thermo Fisher Scientific Inc. and Ultima Genomics Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the DNA sequencing market is intensely focused on innovation, with companies investing heavily in R&D, a factor rated as having high criticality. This strategic focus is highlighted by portfolio realignments, such as Pacific Biosciences' divestment of its short-read assets to Illumina to concentrate on the long-read sequencing market.

- This move reflects a broader industry trend of specialization, where firms align their technology with specific applications, such as clinical diagnostics or complex research. The development of advanced platforms is a direct response to the industry's need for higher accuracy and greater throughput, which can improve diagnostic yield by more than 15% in certain applications.

- Companies are adapting to these pressures by streamlining workflows and enhancing data analysis capabilities to maintain a competitive edge.

We can help! Our analysts can customize this dna sequencing market research report to meet your requirements.

RIA -

RIA -