Next Generation Sequencing Market Size 2024-2028

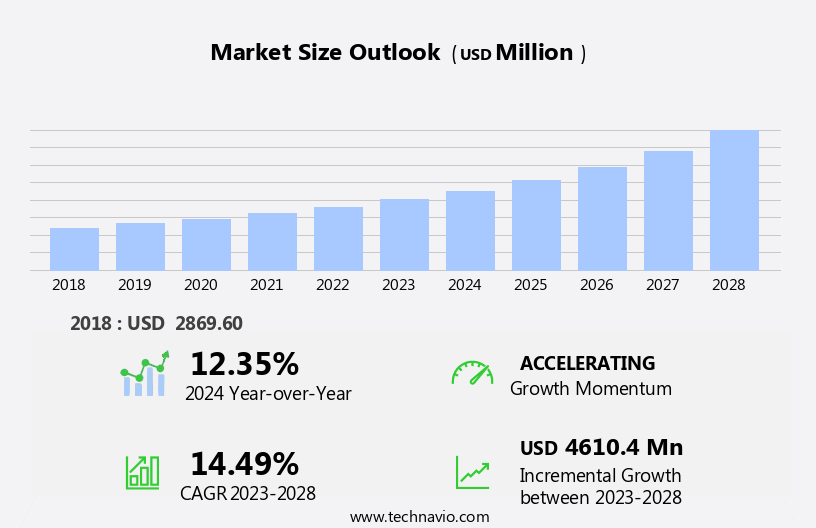

The next generation sequencing market size is forecast to increase by USD 4.61 billion, at a CAGR of 14.49% between 2023 and 2028.

- The Next Generation Sequencing (NGS) market is experiencing significant growth, driven by the increasing utilization of NGS methods in various applications, including diagnostics, research, and personalized medicine. Advancements in NGS techniques have led to faster and more cost-effective sequencing, enabling broader access to genetic information and fueling innovation in fields such as agriculture, environmental research, and forensics. However, the market faces challenges, primarily in the area of clinical validation for direct-to-consumer genetic tests. As the availability of genetic information expands, ensuring the accuracy and reliability of test results becomes increasingly important.

- Addressing these concerns through rigorous clinical validation processes and regulatory compliance will be crucial for market participants to build trust and credibility with consumers and healthcare providers. Companies that effectively navigate these challenges and continue to innovate in NGS technology and applications will be well-positioned to capitalize on the market's growth potential.

What will be the Size of the Next Generation Sequencing Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The next generation sequencing (NGS) market continues to evolve, driven by advancements in sequencing platforms and data analysis techniques. Seamlessly integrated solutions are transforming the landscape, connecting entities such as sequence databases, RNA sequencing, targeted sequencing, and NGS applications. Copy number variation and reference genomes are critical components of genome assembly, ensuring quality control and accuracy. Methylation analysis, sequencing platforms, and data analysis are intricately linked, enabling the identification of epigenetic modifications and enhancing genomic understanding. Reproductive genomics, exome sequencing, data visualization, gene expression analysis, forensic genomics, infectious disease genomics, and variant calling are integral parts of the NGS ecosystem.

Sequence alignment, PACBI sequencing, DNA extraction, Ion Torrent sequencing, base calling, and single-cell sequencing are additional techniques expanding the scope of NGS applications. Agricultural genomics, clinical interpretation, library preparation, Illumina sequencing, whole genome sequencing, variant annotation, cancer genomics, mutation detection, read mapping, and microbial sequencing are all areas benefiting from NGS technology. Structural variation and nanopore sequencing are emerging technologies pushing the boundaries of genomic research. The NGS market's continuous dynamism reflects the ongoing unfolding of market activities and evolving patterns, with each entity playing a crucial role in the broader genomic research landscape.

How is this Next Generation Sequencing Industry segmented?

The next generation sequencing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Academic research

- Clinical research

- Pharmaceutical and biotechnology companies

- Others

- Product

- Consumables

- Equipment

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

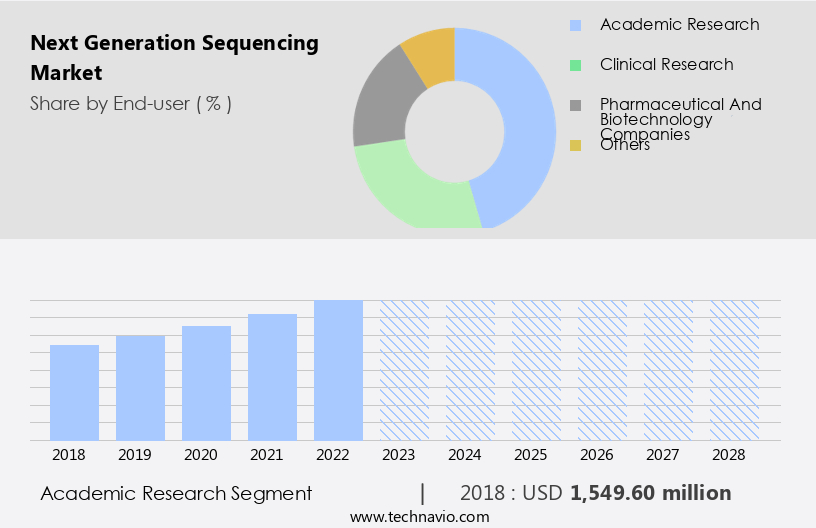

By End-user Insights

The academic research segment is estimated to witness significant growth during the forecast period.

The next generation sequencing (NGS) market encompasses various applications and technologies, including RNA sequencing, targeted sequencing, and genome assembly. Academic research institutions, such as universities and research organizations, represent a significant market segment. Researchers in this sector employ NGS for diverse purposes, including drug discovery, personalized medicine, and clinical diagnostics. NGS enables the rapid sequencing of vast genetic data volumes, facilitating the analysis of genetic variations and elucidating disease mechanisms. Key factors fueling the adoption of NGS in academic research include decreasing sequencing costs, user-friendly software, and the growing demand for personalized and precision medicine. NGS applications extend to reproductive genomics, exome sequencing, and gene expression analysis.

Data visualization tools and clinical interpretation services aid researchers in making sense of the massive data generated. NGS platforms, such as PacBio sequencing, Ion Torrent sequencing, and Illumina sequencing, cater to different sequencing needs. Library preparation, DNA extraction, and base calling are essential processes in NGS workflows. Methylation analysis, copy number variation, and structural variation detection are crucial NGS applications in fields like forensic genomics, cancer genomics, and infectious disease genomics. Variant calling, sequence alignment, and mutation detection are integral to identifying genetic variations. Microbial sequencing and read mapping are essential for microbiome research. Nanopore sequencing offers long-read sequencing capabilities, enhancing genome assembly and variant analysis.

NGS technologies are revolutionizing various industries, including agriculture, where they aid in crop improvement and breeding programs. In summary, the market is dynamic and evolving, driven by technological advancements, decreasing costs, and the growing demand for personalized and precision medicine.

The Academic research segment was valued at USD 1.55 billion in 2018 and showed a gradual increase during the forecast period.

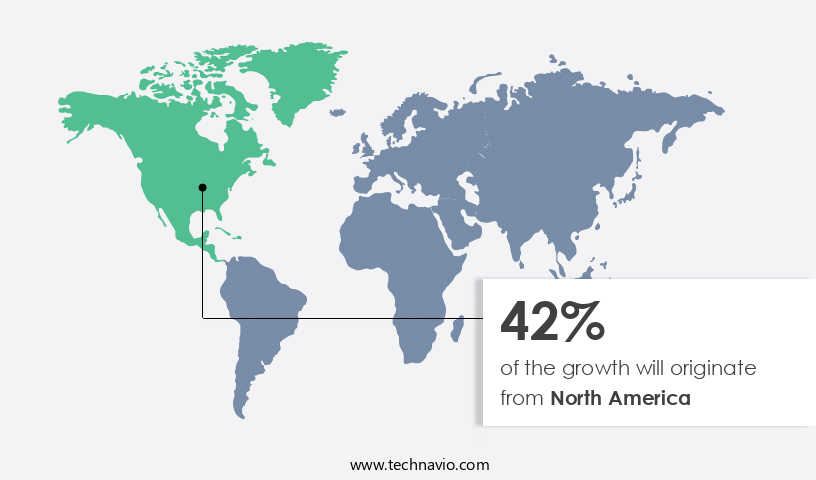

Regional Analysis

North America is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The Next Generation Sequencing (NGS) market in North America is experiencing significant growth due to the decreasing cost of genome sequencing, enabling earlier diagnosis of diseases such as cancer. Major players like Illumina, Thermo Fisher Scientific, and PerkinElmer, along with the emphasis on genome mapping programs, are driving market expansion in the region. However, growth is anticipated to be slower than the global market during the forecast period. In the United States, the adoption of advanced DNA sequencing technology is escalating, fueled by a focus on gene therapy and personalized medicine initiatives. NGS applications, including RNA sequencing, targeted sequencing, and whole genome sequencing, are revolutionizing fields such as reproductive genomics, exome sequencing, and infectious disease genomics.

Technologies like PacBio sequencing, Ion Torrent sequencing, and nanopore sequencing are transforming genome assembly, methylation analysis, variant calling, and read mapping. Library preparation, quality control, and data analysis are crucial components of the NGS workflow. Additionally, NGS is making strides in forensic genomics, cancer genomics, mutation detection, and structural variation analysis. The agricultural sector is also benefiting from NGS in the areas of gene expression analysis and agricultural genomics. Data visualization tools are essential for interpreting the vast amounts of data generated by NGS, while clinical interpretation and variant annotation are crucial for translating raw data into actionable insights.

Overall, the NGS market is a dynamic and evolving landscape, with new applications and technologies continually emerging to advance our understanding of the genome and its role in health and agriculture.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Next Generation Sequencing Industry?

- The significant expansion in the application of Next-Generation Sequencing (NGS) techniques is the primary catalyst fueling market growth.

- Next Generation Sequencing (NGS) market has witnessed significant advancements, driven by the development of sequence databases and sophisticated NGS applications. RNA sequencing and targeted sequencing are among the key NGS techniques used for studying gene expression and identifying genetic variations. The availability of reference genomes and genome assembly tools has facilitated the analysis of copy number variation and methylation. Quality control measures ensure accurate results in NGS analysis. NGS offers several advantages over traditional methods, including higher throughput, reduced cost, and enhanced sensitivity. The capability to sequence millions of DNA fragments per run simultaneously enables the detection of rare variants and mutations with greater accuracy.

- NGS applications extend beyond human genetics, finding applications in agriculture, environmental research, and microbiology. NGS market participants, such as Illumina, QIAGEN, Thermo Fisher Scientific, Bio-Rad Laboratories, Danaher, and PerkinElmer, leverage these advantages to offer comprehensive diagnostic services and research solutions. The technology's ability to provide a more comprehensive understanding of genetic information has revolutionized the field of genomics, leading to numerous breakthroughs in medical research and diagnostics.

What are the market trends shaping the Next Generation Sequencing Industry?

- Advances in Next-Generation Sequencing (NGS) techniques are currently shaping the market trend in the scientific community. The implementation of these innovative technologies is revolutionizing various industries, including healthcare and agriculture, by enabling more accurate and efficient genetic analysis.

- Next Generation Sequencing (NGS) market has witnessed substantial growth due to the revolutionary impact of sequencing platforms in various fields of genomics. The Human Genome Project (HGP), initiated in 1990, paved the way for companies like Illumina, QIAGEN, Thermo Fisher Scientific, Bio-Rad Laboratories, Danaher, and PerkinElmer, and researchers to explore the function, structure, and organization of a complete human genome. NGS applications have expanded beyond research, reaching clinical environments for disease diagnosis and treatment outcomes. These techniques have significantly contributed to understanding genetic variations causing disorders, particularly in areas like reproductive genomics, exome sequencing, gene expression analysis, forensic genomics, and infectious disease genomics.

- Technological advancements in NGS have resulted in a significant reduction in sequencing costs, making it accessible to smaller laboratories. NGS platforms offer data analysis tools, data visualization, and variant calling capabilities, enhancing the overall research experience. The ability to process large genomic data sets efficiently and accurately is a key driver for the growth of the NGS market. In summary, the NGS market has experienced significant growth due to its wide applicability in various fields of genomics and the technological innovations that have made it more accessible and cost-effective. These advancements have led to improved diagnostic capabilities and a deeper understanding of genetic disorders.

What challenges does the Next Generation Sequencing Industry face during its growth?

- The absence of clinical validation poses a significant challenge to the expansion of the direct-to-consumer genetic testing industry. This issue, which is of great concern to industry professionals, hinders the acceptance and trust of these tests among consumers and healthcare providers alike.

- Next-generation sequencing (NGS) technology has revolutionized the field of genomics, offering significant advancements in areas such as sequence alignment, library preparation, base calling, and single-cell sequencing. PACBIO and Ion Torrent sequencing are among the leading NGS technologies, providing high-quality data for various applications. However, the clinical utility of NGS in direct-to-consumer genetic testing has faced challenges due to concerns over the clinical validity of the results. The complexity of NGS data necessitates the involvement of experts, such as genetic counselors and medical practitioners, for accurate interpretation. Moreover, disease risk predictions from NGS tests do not account for environmental and lifestyle factors, which are crucial determinants of health outcomes.

- These factors increase the need for consultation costs, making the tests less cost-effective for consumers. In agricultural genomics, NGS has facilitated the identification of genetic markers for crop improvement, contributing to increased productivity and sustainability. However, the high cost and technical complexity of NGS limit its widespread adoption in this sector. The advancements in NGS technology continue to drive innovation in various fields, including clinical diagnostics and research. As the technology matures, it is expected to become more accessible and affordable, enabling broader applications and transforming the way we understand and address health and agricultural challenges.

Exclusive Customer Landscape

The next generation sequencing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the next generation sequencing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, next generation sequencing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

10X Genomics Inc. - This company leads in next-generation sequencing technology, featuring Chromium single cell, Visium spatial, and Xenium in situ methods. Their innovative approaches advance genetic research, enabling more precise and comprehensive analysis.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 10X Genomics Inc.

- Azenta Inc.

- BGI Genomics Co. Ltd.

- Bio Rad Laboratories Inc.

- Eurofins Scientific SE

- F. Hoffmann La Roche Ltd.

- Illumina Inc.

- Konica Minolta Inc.

- Laboratory Corp. of America Holdings

- Merck KGaA

- Nabsys Inc.

- OPKO Health Inc.

- Oxford Nanopore Technologies plc

- Perkin Elmer Inc.

- PierianDx Inc.

- Psomagen Inc.

- QIAGEN NV

- Standard BioTools Inc.

- Takara Bio Inc.

- Thermo Fisher Scientific Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Next Generation Sequencing Market

- In January 2024, Illumina, a leading player in the Next Generation Sequencing (NGS) market, announced the launch of its new NovaSeq S4 System, which offers increased sequencing capacity and faster turnaround times compared to its previous models. This development was aimed at enhancing the company's position in the high-throughput NGS market (Illumina, 2024).

- In March 2024, Thermo Fisher Scientific and 10x Genomics entered into a strategic collaboration to integrate 10x Genomics' Chromium Genome Engineering solutions with Thermo Fisher's Oncomine Dx Target Test, a cancer diagnostic test. This collaboration aimed to improve the accuracy and efficiency of cancer diagnostics (Thermo Fisher Scientific, 2024).

- In May 2024, Pacific Biosciences, a key NGS technology provider, raised USD350 million in a funding round led by Fidelity Management and Research Company. This significant investment was intended to support the company's research and development efforts, including the advancement of its Single Molecule, Real-Time (SMRT) Sequencing technology (Pacific Biosciences, 2024).

- In April 2025, the U.S. Food and Drug Administration (FDA) granted marketing authorization to Oxford Nanopore Technologies for its MinION Mk1C portable NGS system. This approval marked the first time a portable NGS system received FDA clearance, making it accessible for use in various settings, including point-of-care diagnostics and research applications (Oxford Nanopore Technologies, 2025).

Research Analyst Overview

- The Next Generation Sequencing (NGS) market is experiencing significant growth, driven by the integration of gene therapy, predictive testing, and precision medicine in various sectors. Newborn screening, carrier screening, and therapeutic monitoring are key applications benefiting from NGS's ability to provide comprehensive genetic information. Data security is a critical concern as massive parallel sequencing generates vast amounts of sensitive data, necessitating HIPAA and regulatory compliance. Cloud computing and data storage solutions facilitate efficient data management and analysis. Sequencing error correction and data interpretation software are essential for accurate results in prognostic and diagnostic testing.

- Genome editing and biomarker discovery are also driving innovation, while sample preparation automation streamlines the process. The market's dynamics are influenced by the ongoing reduction in sequencing costs and the increasing importance of turnaround time in drug development. Ethical considerations remain a significant challenge, requiring ongoing dialogue and regulatory oversight.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Next Generation Sequencing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

181 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.49% |

|

Market growth 2024-2028 |

USD 4610.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.35 |

|

Key countries |

US, Germany, Canada, China, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Next Generation Sequencing Market Research and Growth Report?

- CAGR of the Next Generation Sequencing industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the next generation sequencing market growth of industry companies

We can help! Our analysts can customize this next generation sequencing market research report to meet your requirements.

RIA -

RIA -