Driver Assistance Systems Market Size 2026-2030

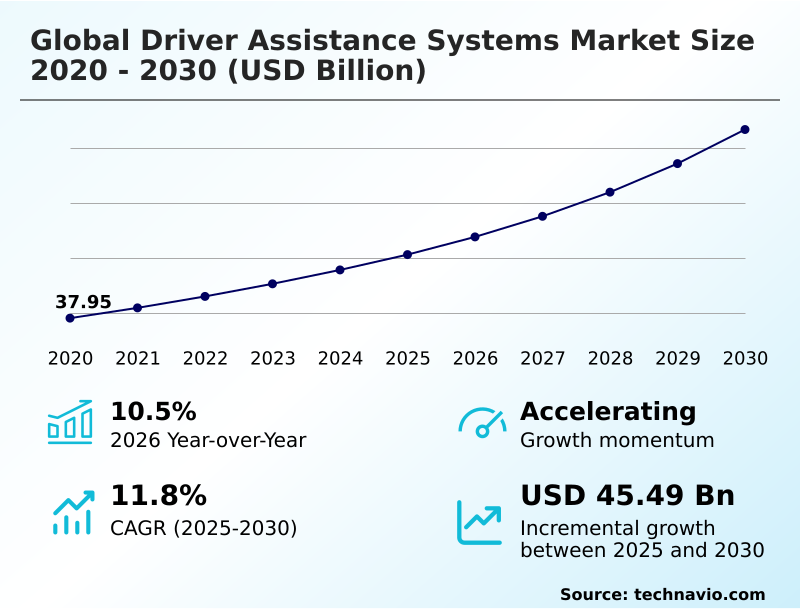

The driver assistance systems market size is valued to increase by USD 45.49 billion, at a CAGR of 11.8% from 2025 to 2030. Stringent government regulations and evolving safety standards will drive the driver assistance systems market.

Major Market Trends & Insights

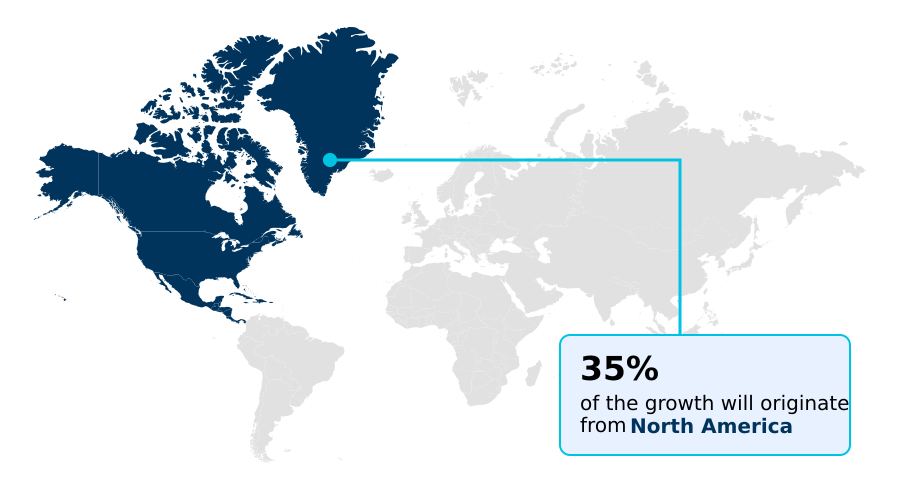

- North America dominated the market and accounted for a 35.4% growth during the forecast period.

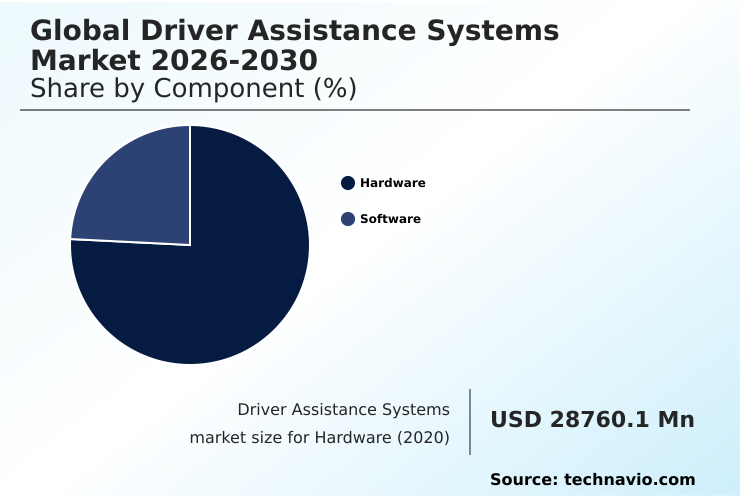

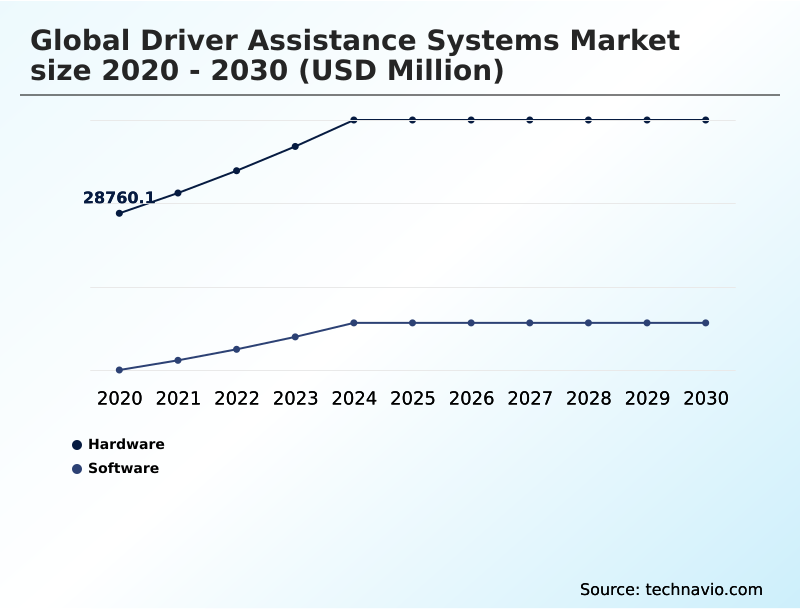

- By Component - Hardware segment was valued at USD 40.41 billion in 2024

- By Type - Adaptive cruise control segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 68.60 billion

- Market Future Opportunities: USD 45.49 billion

- CAGR from 2025 to 2030 : 11.8%

Market Summary

- The driver assistance systems market is undergoing a significant transformation, moving beyond basic warnings to active vehicle control and predictive intervention. This evolution is driven by the convergence of stringent safety regulations and rising consumer demand for intelligent, convenient features.

- A pivotal trend is the architectural shift toward software-defined vehicles, which rely on centralized domain controllers and high-performance system-on-chips to process vast amounts of sensor data in real time. This enables the continuous improvement of functions like highway piloting and automated parking through over-the-air updates.

- However, the industry grapples with challenges related to the high cost of implementation and the complexity of sensor recalibration after minor accidents. For instance, logistics companies are navigating this by adopting modular active safety technologies that enhance fleet safety and operational efficiency by reducing accident-related downtime, balancing the initial investment against long-term risk mitigation and lower insurance premiums.

- The integration of deep learning algorithms is critical for overcoming these hurdles, particularly in validating system performance against unpredictable edge cases and ensuring reliability in adverse weather conditions.

What will be the Size of the Driver Assistance Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Driver Assistance Systems Market Segmented?

The driver assistance systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Hardware

- Software

- Type

- Adaptive cruise control

- Automatic emergency braking

- Lane departure warning

- Blind spot detection

- Others

- Vehicle type

- Passenger cars

- Commercial vehicles

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment forms the physical backbone, including a suite of sensors such as high-definition cameras, ultrasonic sensors, and increasingly, light detection and ranging (LiDAR).

The evolution from distributed electronic control units (ECU) to centralized domain controllers is reshaping vehicle architecture, demanding greater processing power for real-time data analysis.

Advancements in 4D imaging radar and solid-state LiDAR are expanding the total addressable market by improving perception capabilities.

However, this complexity affects the total cost of ownership, as the need for precise sensor recalibration following minor incidents has driven repair expenses up by over 30% for some equipped models.

OEMs focus on managing bill-of-materials costs through economies of scale, balancing the integration of advanced hardware with consumer price sensitivity and the need for high safety ratings.

The Hardware segment was valued at USD 40.41 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Driver Assistance Systems Market Demand is Rising in North America Get Free Sample

The geographic landscape is diverse, with regions prioritizing different active safety technologies. Europe leads in mandating vulnerable road user protection and driver monitoring systems, fostering the development of Level 3 autonomy within a defined operational design domain.

In North America, consumer demand for convenience drives high adoption of hands-free driving. APAC is a hub for rapid innovation, using synthetic data training to adapt automatic emergency braking for dense urban traffic.

In commercial sectors, features like active side guard assist and trailer sway control are crucial, with adoption in some fleets reducing side-collision incidents by 20%.

In contrast, markets in South America are standardizing foundational systems like electronic stability control and hill-start assist, while specialized features like pro trailer backup assist gain traction in utility vehicle segments.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions within the global driver assistance systems market 2026-2030 are increasingly influenced by nuanced technical and operational factors. The discussion around lane departure warning vs lane keeping highlights the industry's progression from passive alerts to active intervention, a shift mirrored in the development of automatic emergency braking for pedestrians and adaptive cruise control with stop-and-go functionality.

- The benefits of 4D imaging radar are becoming evident in its ability to enhance sensor fusion for urban driving. As vehicles evolve, the debate over centralized vs distributed ECU architecture is central to enabling the software-defined vehicle, with zonal architecture in electric vehicles emerging as a dominant trend.

- This architecture facilitates OTA updates for safety systems but also amplifies the importance of cybersecurity in software-defined vehicles and ensuring GDPR compliance for driver data. Operationally, the cost of ADAS sensor recalibration has become a significant factor for insurers and repair networks, with costs for Level 2 systems rising more than 25% faster than for non-equipped vehicles.

- This impacts everything from the optimal blind spot detection sensor location to the methods for validating ADAS against edge cases. Persistent issues like phantom braking causes and solutions and poor LiDAR performance in heavy rain continue to drive R&D.

- Furthermore, the growth of Level 2 highway driving assist and AI in in-cabin sensing systems, especially for driver monitoring for drowsiness detection, underscores the move toward more sophisticated, proactive safety measures, including V2X for collision avoidance and predictive speed assist using maps.

What are the key market drivers leading to the rise in the adoption of Driver Assistance Systems Industry?

- Stringent government regulations and evolving safety standards are key drivers accelerating market adoption.

- The democratization of advanced technologies is a primary driver, with features like adaptive cruise control, highway piloting, and surround-view monitoring becoming standard. This widespread adoption of Level 2 autonomy is expanding the market as consumers prioritize intelligent safety.

- Innovations in deep learning algorithms enable predictive intervention, improving collision avoidance rates by up to 25% in complex scenarios. The relentless pace of innovation supports real-time data processing and future vehicle-to-everything communication.

- Stringent regulatory compliance mandates, including intelligent speed assistance and pedal misapplication control, solidify market demand.

- As automated parking features become more common, they help build consumer trust, which is essential for the acceptance of higher levels of automation and new mobility solutions.

What are the market trends shaping the Driver Assistance Systems Industry?

- A key market trend is the transition toward centralized zonal architectures, which enables the development of software-defined vehicles.

- The market is experiencing a structural shift toward zonal architectures, which are foundational to the software-defined vehicle. This enables manufacturers to deploy over-the-air updates, continuously improving features like hands-free driving and predictive speed assist. The proliferation of systems offering a hands-off, eyes-on experience leverages crowd-sourced fleet data to enhance navigation, with some platforms improving route efficiency by 15%.

- Concurrently, the focus is expanding inward with advanced in-cabin sensing and smart cockpit features. Powered by human insight AI, these systems perform cognitive load analysis to ensure safe hand-over procedures from autonomous modes.

- This evolution prioritizes occupant well-being, transforming the vehicle into a guardian that monitors driver readiness and health, a transition that has improved distraction detection accuracy by over 40%.

What challenges does the Driver Assistance Systems Industry face during its growth?

- High implementation costs and the complexity of post-collision repairs present a key challenge affecting industry growth.

- Significant challenges persist despite technological gains. Cybersecurity risks are paramount, as connectivity to the controller area network bus leads to attack surface expansion and data privacy concerns under frameworks like the General Data Protection Regulation.

- The reliability of systems like pedestrian detection systems and blind spot detection in adverse environmental conditions remains a hurdle, with some reverse automatic emergency braking systems showing a failure rate increase of 60% in simulated winter conditions. Issues such as phantom braking, where sensor fusion misinterprets benign objects, erode consumer confidence.

- The complexity of edge case validation for features like lane departure warning requires extensive testing to ensure systems perform reliably across all potential driving scenarios.

Exclusive Technavio Analysis on Customer Landscape

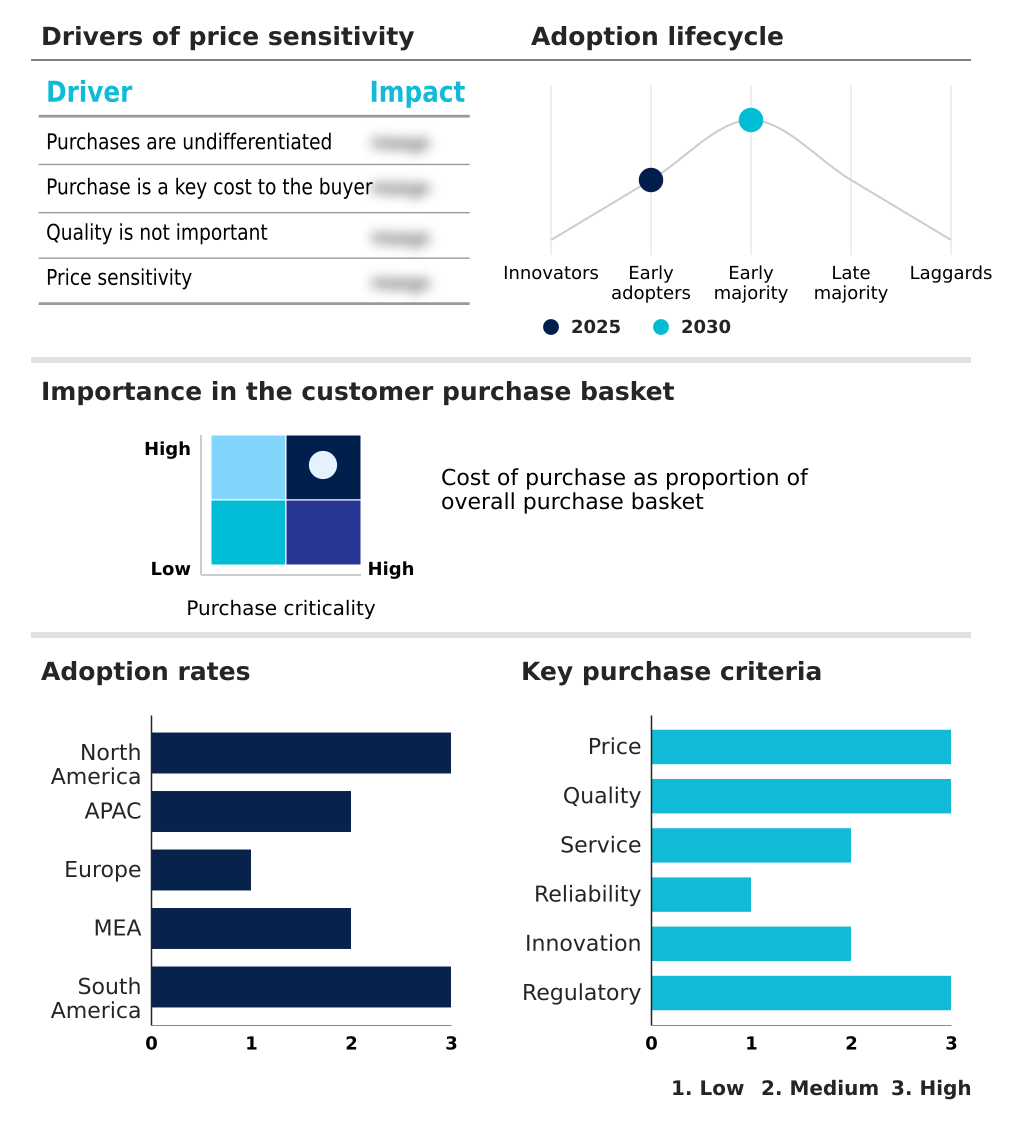

The driver assistance systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the driver assistance systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Driver Assistance Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, driver assistance systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AISIN Corp. - Offerings include integrated systems with surround-view, emergency brake assist via radar/camera fusion, and advanced controllers for enhanced safety and automated driving.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AISIN Corp.

- Aptiv Plc

- Autoliv Inc.

- Continental AG

- DENSO Corp.

- Ficosa Internacional SA

- HELLA GmbH and Co. KGaA

- Hyundai Mobis Co. Ltd.

- Infineon Technologies AG

- Joyson Safety Systems GmbH

- Magna International Inc.

- Mobileye Technologies Ltd.

- NVIDIA Corp.

- Panasonic Holdings Corp.

- Renesas Electronics Corp.

- Robert Bosch GmbH

- Texas Instruments Inc.

- Valeo SA

- Veoneer Inc.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Driver assistance systems market

- In January, 2025, the National Highway Traffic Safety Administration issued a final confirmation on its automatic emergency braking mandate, solidifying the implementation timeline and compelling automakers to accelerate validation of next-generation braking algorithms.

- In March, 2025, Mobileye launched its Surround ADAS platform, a scalable solution designed to bring hands-free Level 2 capabilities to mass-market vehicles using a cost-optimized camera suite and computing architecture.

- In April, 2025, Qualcomm Technologies announced the commercial availability of its Snapdragon Digital Chassis solution, which integrates driver assistance and cockpit functions into a single system-on-chip to reduce costs and increase computational power.

- In May, 2025, General Motors began rolling out its enhanced Ultra Cruise system, powered by a new central compute architecture developed with Qualcomm, capable of handling 95% of driving scenarios by processing data from over twenty sensors.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Driver Assistance Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.8% |

| Market growth 2026-2030 | USD 45492.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.5% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The driver assistance systems market is defined by a rapid technological churn, where the value proposition is migrating from hardware to intelligent software. The integration of active safety technologies like automatic emergency braking and lane departure warning is now table stakes, with differentiation shifting to the sophistication of sensor fusion and deep learning algorithms.

- Boardroom decisions now center on the transition to zonal architectures and the software-defined vehicle, a move essential for deploying over-the-air updates and features like highway piloting. This requires mastering high-performance system-on-chips and centralized domain controllers. The adoption of 4D imaging radar, solid-state LiDAR, and high-definition cameras enhances perception, supporting functions from blind spot detection to vulnerable road user protection.

- A key challenge is managing the controller area network bus to prevent issues like phantom braking. Advanced systems, including driver monitoring systems for in-cabin sensing and Level 3 autonomy, depend on synthetic data training and human insight AI.

- The deployment of reverse automatic emergency braking and automated parking features showcases how systems utilizing ultrasonic sensors and predictive intervention improve safety, with some achieving a 40% reduction in low-speed incidents. The evolution toward hands-free driving and predictive speed assist marks the next frontier in Level 2 autonomy.

What are the Key Data Covered in this Driver Assistance Systems Market Research and Growth Report?

-

What is the expected growth of the Driver Assistance Systems Market between 2026 and 2030?

-

USD 45.49 billion, at a CAGR of 11.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, and Software), Type (Adaptive cruise control, Automatic emergency braking, Lane departure warning, Blind spot detection, and Others), Vehicle Type (Passenger cars, and Commercial vehicles) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Stringent government regulations and evolving safety standards, High implementation costs and repair complexity

-

-

Who are the major players in the Driver Assistance Systems Market?

-

AISIN Corp., Aptiv Plc, Autoliv Inc., Continental AG, DENSO Corp., Ficosa Internacional SA, HELLA GmbH and Co. KGaA, Hyundai Mobis Co. Ltd., Infineon Technologies AG, Joyson Safety Systems GmbH, Magna International Inc., Mobileye Technologies Ltd., NVIDIA Corp., Panasonic Holdings Corp., Renesas Electronics Corp., Robert Bosch GmbH, Texas Instruments Inc., Valeo SA, Veoneer Inc. and ZF Friedrichshafen AG

-

Market Research Insights

- The market's dynamics are shaped by the rapid democratization of advanced features and the push for greater automation. As automakers compete on safety ratings, the adoption of sophisticated systems is accelerating across all vehicle segments, expanding the total addressable market.

- This trend is supported by achieving economies of scale in sensor manufacturing, which has lowered bill-of-materials costs by over 10% for certain high-volume components. Concurrently, data privacy concerns and cybersecurity risks are shaping development, with platforms now engineered to meet stringent General Data Protection Regulation standards.

- This focus on security has led to a 25% reduction in identified vulnerabilities in the latest generation of connected modules. Ensuring consumer trust through robust edge case validation and reliable performance in adverse environmental conditions remains a central focus, as functional dependability directly influences purchasing decisions and brand reputation.

We can help! Our analysts can customize this driver assistance systems market research report to meet your requirements.

RIA -

RIA -