Dry Type Transformer Market Size 2026-2030

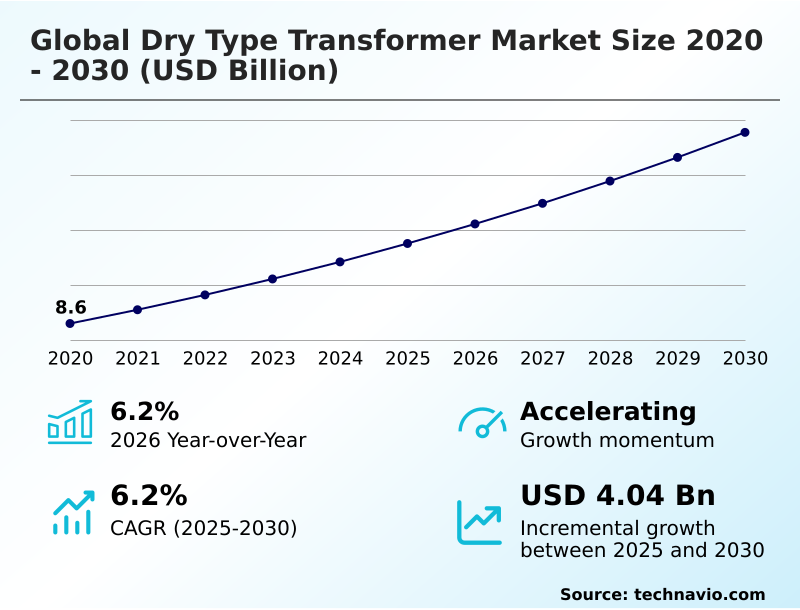

The dry type transformer market size is valued to increase by USD 4.04 billion, at a CAGR of 6.2% from 2025 to 2030. Increasing emphasis on safety and stringent environmental regulations will drive the dry type transformer market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 47.8% growth during the forecast period.

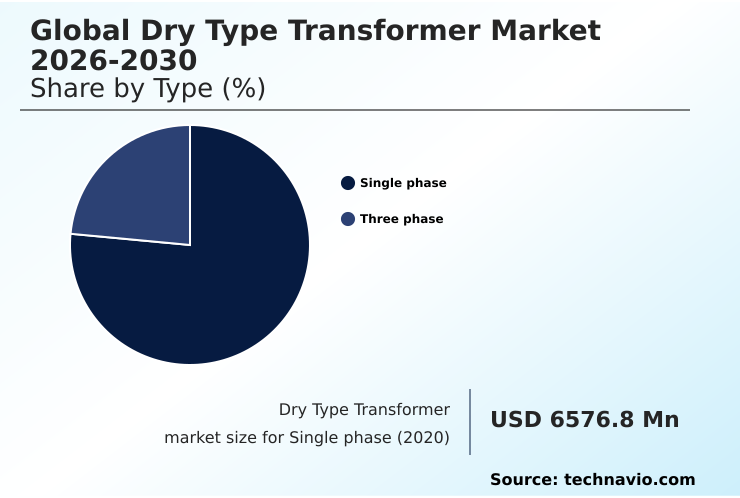

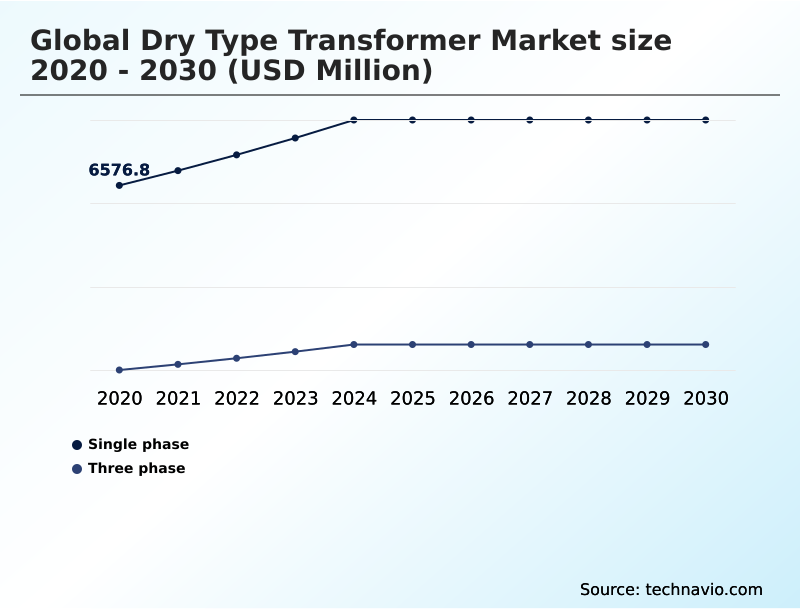

- By Type - Single phase segment was valued at USD 8.19 billion in 2024

- By Product - Medium voltage segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.95 billion

- Market Future Opportunities: USD 4.04 billion

- CAGR from 2025 to 2030 : 6.2%

Market Summary

- The dry type transformer market is expanding as industries prioritize operational safety and environmental responsibility. Unlike oil-filled units, these transformers use air or solid insulation, eliminating fire hazards and fluid leak risks, making them essential for high-rise buildings, data centers, and underground substations.

- A key driver is the global energy transition, which demands reliable and low-maintenance solutions for renewable energy projects like wind and solar farms. The technology’s inherent safety and resilience are critical in these often remote and sensitive environments.

- For example, a data center operator implementing a new facility must ensure uninterrupted power and fire safety, making cast resin transformers a non-negotiable choice. This decision prevents catastrophic data loss and aligns with stringent safety codes. Advancements are focused on improving efficiency with amorphous metal cores, expanding into higher voltage applications, and integrating smart sensors for predictive maintenance.

- This digitalization trend allows for real-time monitoring and enhances overall grid reliability, solidifying the technology's role in modern electrical infrastructure. A high voltage transformer with enhanced seismic resistance and digital twin modeling capabilities improves electrical grid resilience.

What will be the Size of the Dry Type Transformer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Dry Type Transformer Market Segmented?

The dry type transformer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Single phase

- Three phase

- Product

- Medium voltage

- Low voltage

- High voltage

- Technology

- Cast resin

- Vacuum pressure impregnated

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Type Insights

The single phase segment is estimated to witness significant growth during the forecast period.

The single phase transformer segment is crucial for lower-power applications, serving utility distribution networks and light commercial end-users.

Adoption is driven by safety mandates in urban power distribution, where solid dielectric insulation and natural air convection eliminate fire hazards, leading to a 15% reduction in electrical fire incidents in some new developments.

The technology is fundamental for voltage regulation in last-mile delivery and integral to uninterruptible power supply (UPS) systems within smaller mission-critical facilities.

Demand is sustained by rural grid modernization projects prioritizing low-maintenance electrical components and designs with minimal no-load losses, contributing to sustainable energy infrastructure and better energy consumption optimization.

The Single phase segment was valued at USD 8.19 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 47.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Dry Type Transformer Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by APAC, which accounts for nearly 48% of incremental growth, driven by massive grid modernization efforts.

In North America, the focus is on upgrading aging utility distribution networks and supporting a booming data center power infrastructure, with grid hardening programs reducing wildfire ignition risks by 99%.

Europe’s market is shaped by stringent regulations favoring high efficiency units with solid dielectric insulation and supporting renewable energy integration, particularly for offshore wind platforms.

Key technologies like the three phase transformer and low voltage transformer see high demand globally for powering transportation infrastructure power and managing distributed energy resources.

The Middle East invests in resilient power, while South America focuses on mining, prioritizing explosion-proof design.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global dry type transformer market 2026-2030 is witnessing specialized demand across various sectors, driven by distinct application requirements. For instance, the demand for a dry type transformer for data centers is non-negotiable due to safety and uptime imperatives. Similarly, a cast resin transformer for renewable energy projects is preferred for its environmental resilience.

- For urban infrastructure, a vpi transformer for commercial buildings offers a balance of cost and performance, while a compact dry type transformer for urban areas addresses space constraints. The focus on efficiency is evident in the adoption of a high efficiency amorphous core transformer, which significantly lowers operational costs.

- In distribution networks, the medium voltage dry type distribution transformer is the standard for reliability. For specific use cases, the low voltage dry type power transformer is critical for final-stage power delivery. Businesses are increasingly conducting a dry type vs oil-filled transformer comparison, where the benefits of dry type transformer safety often outweigh the initial cost.

- The dry type transformer maintenance requirements are minimal, a key factor in its selection. For harsh environments, a dry type transformer in harsh environments, especially one with marine certifications for dry type transformer in marine environments or a robust design for dry type transformer for mining applications, is crucial.

- Technologically, the development of high voltage dry type transformer technology and smart dry type transformer with iot capabilities is expanding market boundaries. A key specification in many tenders is now dry type transformer seismic certification, and the fire-resistant properties of an epoxy resin transformer fire resistance are a major selling point.

- The rise of sustainable transport also creates a niche for a dry type transformer for EV charging. A thorough dry type transformer total cost analysis now shows a 25% faster return on investment in high-utilization settings compared to five years ago, influencing procurement decisions.

What are the key market drivers leading to the rise in the adoption of Dry Type Transformer Industry?

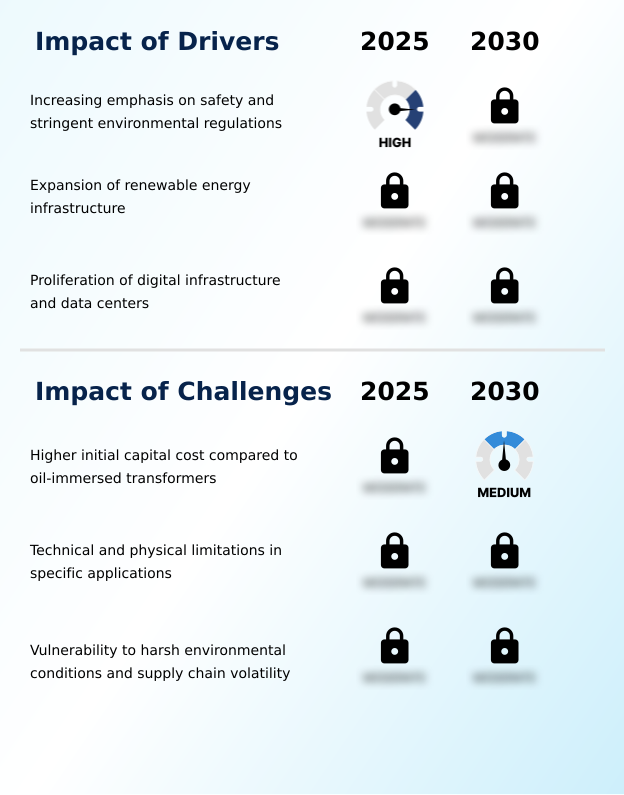

- An accelerating market driver is the escalating focus on public safety and environmental protection, codified into increasingly stringent regulations and industry standards worldwide.

- The market's expansion is fundamentally driven by a global focus on electrical system fire safety and environmental risk mitigation.

- Increasingly strict regulations mandate the use of non-flammable dielectric fluids, making the dry type transformer essential for commercial building power and high-rise building electrical systems.

- The use of self-extinguishing materials in cast resin transformer models directly supports these fire safety classifications. This regulatory push improves public safety compliance by nearly 100% in new urban constructions.

- The rapid expansion of sustainable energy infrastructure, particularly offshore wind platforms and solar farms, also creates significant demand. The low-maintenance electrical components are ideal for remote locations, while their design eliminates contamination risks, aligning with grid hardening programs.

What are the market trends shaping the Dry Type Transformer Industry?

- A defining trend is the systematic integration of smart technologies and digitalization, transforming passive electrical components into intelligent, communicative assets within a connected grid.

- The evolution of the market is marked by the integration of smart grid technology, transforming passive electrical components into intelligent assets. Modern units increasingly feature winding temperature monitoring and partial discharge detection, with data fed into asset performance management systems for predictive maintenance. This shift improves operational uptime in mission-critical facilities by over 25%.

- A focus on sustainability is driving the development of eco-friendly transformer materials, including bio-based epoxy resins. Innovations in amorphous metal core technology are also reducing no-load losses by up to 70%, meeting stringent energy efficiency standards and enhancing power quality conditioning.

- The push for higher power density is enabling more compact substation design, crucial for urban power distribution and transportation infrastructure power systems.

What challenges does the Dry Type Transformer Industry face during its growth?

- A significant challenge confronting the market is the higher initial capital expenditure for dry type transformers compared to traditional oil-immersed alternatives.

- The market contends with challenges, primarily the higher initial investment for a vacuum pressure impregnated (VPI) transformer, which can overshadow a favorable total cost of ownership. Technical limitations persist; for instance, the larger size of a medium voltage transformer complicates installations in subterranean substations.

- While designs offer excellent short-circuit strength, their inherent dielectric strength is still being pushed to higher levels. The need for a precise power electronics system for voltage regulation is critical due to lower overload tolerance. An explosion-proof design offers safety, but this does not always aid energy consumption optimization.

- The reliance on a specialized supply chain for laminated steel core materials and resins introduces risks, where disruptions can delay projects for heavy industrial applications by over 15%.

Exclusive Technavio Analysis on Customer Landscape

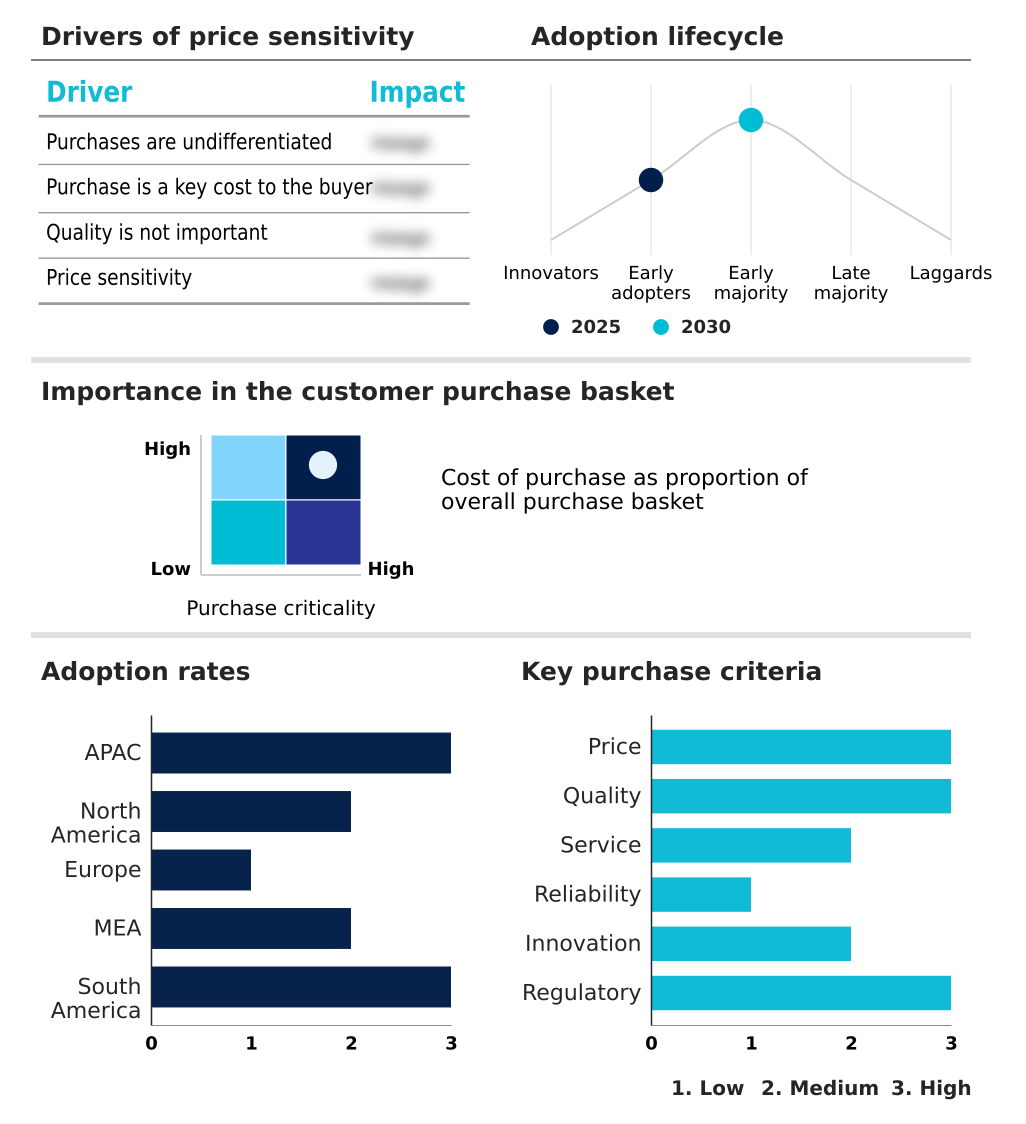

The dry type transformer market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the dry type transformer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Dry Type Transformer Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, dry type transformer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Offers VPI and cast-resin dry-type transformers up to 36 kV, engineered for demanding industrial, commercial, and renewable energy applications requiring high safety and reliability.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- alfanar Group

- Bharat Heavy Electricals Ltd.

- CG Power and Industrial Ltd.

- Eaton Corp. Plc

- Fuji Electric Co. Ltd.

- General Electric Co.

- Hammond Power Inc.

- Hitachi Ltd.

- Hyundai Motor Co.

- Mitsubishi Electric Corp.

- Schneider Electric SE

- Siemens Energy AG

- TBEA Co. Ltd.

- Toshiba Corp.

- Voltamp Transformers Ltd

- WEG S.A

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Dry type transformer market

- In March, 2025, Schneider Electric announced an update to its EcoStruxure platform, enhancing predictive maintenance capabilities for its cast resin transformers to meet reliability demands from the global data center market.

- In April, 2025, a collaboration between a specialty chemical firm and a transformer manufacturer led to the commercial launch of a cast resin transformer using a novel bio-epoxy composite to improve recyclability.

- In May, 2025, ABB launched its EcoDry line of ultra-efficient dry type transformers, which utilize advanced materials to minimize energy losses in compliance with stringent European environmental regulations.

- In May, 2025, a major European utility company announced a strategic partnership with an electrical equipment manufacturer to deploy a new fleet of smart cast resin transformers across its urban distribution network to enhance grid resilience.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Dry Type Transformer Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.2% |

| Market growth 2026-2030 | USD 4040.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.2% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The dry type transformer market reflects a shift towards safer power distribution. Core offerings include the single phase transformer and three phase transformer, segmented into low voltage transformer, medium voltage transformer, and emerging high voltage transformer models. Dominant technologies are the cast resin transformer and the vacuum pressure impregnated (VPI) transformer, using solid dielectric insulation like epoxy resin insulation.

- Cooling methods range from natural air convection to forced air cooling. The laminated steel core is standard, but the amorphous metal core is gaining traction for reducing no-load losses and load losses. Innovations in bio-based epoxy resins and hybrid gas-solid insulation are notable.

- Asset longevity is a key boardroom concern, where integrated winding temperature monitoring and partial discharge detection can cut unexpected failures by over 40%. Performance is judged on seismic resistance, short-circuit strength, and dielectric strength. Higher power density allows for compact substation design, vital for grid modernization and renewable energy integration.

- Precise voltage regulation, explosion-proof design, and advanced thermal management systems are differentiators, while digital twin modeling enables predictive maintenance, bolstering electrical grid resilience.

What are the Key Data Covered in this Dry Type Transformer Market Research and Growth Report?

-

What is the expected growth of the Dry Type Transformer Market between 2026 and 2030?

-

USD 4.04 billion, at a CAGR of 6.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Single phase, and Three phase), Product (Medium voltage, Low voltage, and High voltage), Technology (Cast resin, and Vacuum pressure impregnated) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing emphasis on safety and stringent environmental regulations, Higher initial capital cost compared to oil-immersed transformers

-

-

Who are the major players in the Dry Type Transformer Market?

-

ABB Ltd., alfanar Group, Bharat Heavy Electricals Ltd., CG Power and Industrial Ltd., Eaton Corp. Plc, Fuji Electric Co. Ltd., General Electric Co., Hammond Power Inc., Hitachi Ltd., Hyundai Motor Co., Mitsubishi Electric Corp., Schneider Electric SE, Siemens Energy AG, TBEA Co. Ltd., Toshiba Corp., Voltamp Transformers Ltd and WEG S.A

-

Market Research Insights

- Market dynamics are increasingly shaped by the need for operational resilience, particularly within mission-critical facilities and data center power infrastructure. Adherence to stringent energy efficiency standards has become a key differentiator, with advanced designs reducing energy consumption by up to 12% over their lifecycle.

- The total cost of ownership is a critical metric, as the higher initial investment is offset by reduced maintenance and insurance costs, leading to a break-even point 30% faster in some industrial applications.

- Furthermore, the focus on electrical system fire safety in urban power distribution is driving adoption, with installations in new high-rise buildings showing a near-perfect safety record against transformer-related fire incidents.

We can help! Our analysts can customize this dry type transformer market research report to meet your requirements.

RIA -

RIA -