Edge Computing In Automotive Market Size 2026-2030

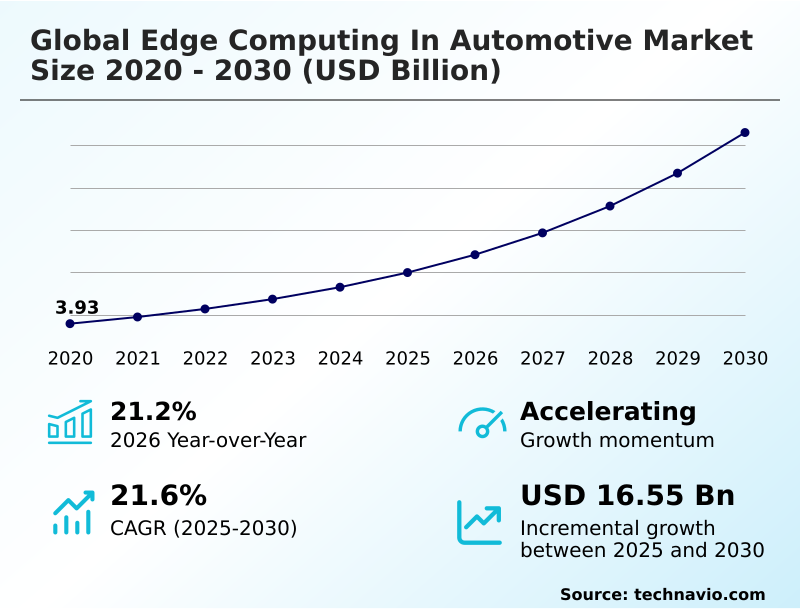

The edge computing in automotive market size is valued to increase by USD 16.55 billion, at a CAGR of 21.6% from 2025 to 2030. Industrial transition toward software-defined vehicle topologies will drive the edge computing in automotive market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 38.3% growth during the forecast period.

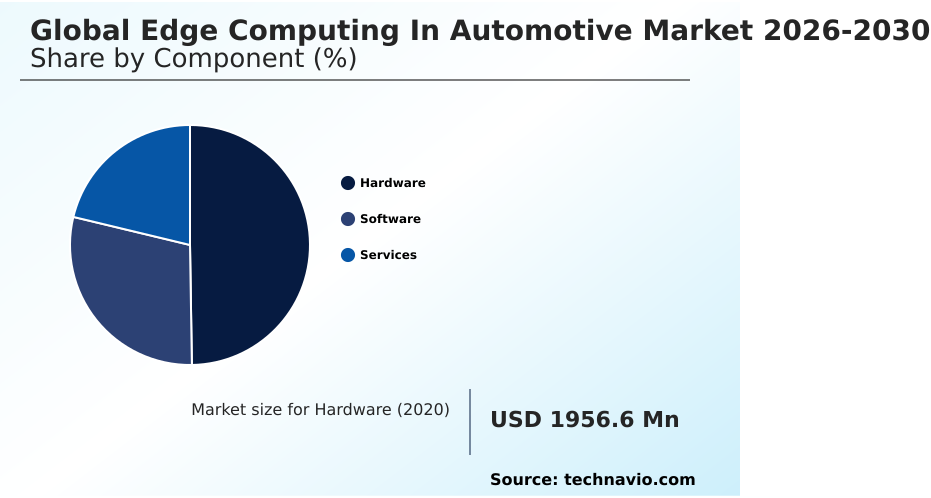

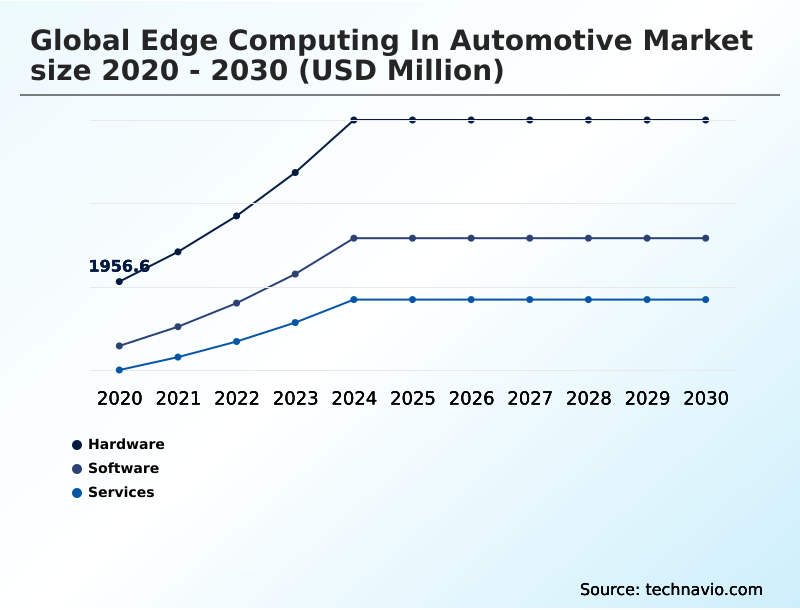

- By Component - Hardware segment was valued at USD 4.01 billion in 2024

- By Deployment - On-board vehicle edge segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 22.58 billion

- Market Future Opportunities: USD 16.55 billion

- CAGR from 2025 to 2030 : 21.6%

Market Summary

- The Edge Computing In Automotive Market is undergoing a rapid architectural transformation as manufacturers shift from centralized cloud dependency to localized processing models. This transition is primarily driven by the escalating demand for advanced automated safety functions, which require instantaneous decision-making capabilities that cannot tolerate network communication latency.

- For instance, logistics operators deploying heavy-duty commercial fleets utilize edge-based predictive algorithmic maintenance to monitor battery thermal loads and engine diagnostics continuously. This localized capability reduces unplanned mechanical failures by 28% compared to traditional cloud-only monitoring methods. However, structural discrepancies between telecommunications and manufacturing lifecycles present a persistent operational challenge.

- The automotive product cycle spans decades, whereas cellular infrastructure evolves rapidly, forcing engineers to integrate complex backward compatibility maintenance into vehicle software to prevent premature hardware obsolescence. By embedding a robust decentralized computational framework directly into the chassis, vehicles execute spatial analysis natively, ensuring critical safety maneuvers operate autonomously during connectivity drops.

- This processing strategy mitigates data transit costs while adapting to volatile environments.

What will be the Size of the Edge Computing In Automotive Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Edge Computing In Automotive Market Segmented?

The edge computing in automotive industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Hardware

- Software

- Services

- Deployment

- On-board vehicle edge

- Hybrid

- Infrastructure edge

- Vehicle type

- Passenger cars

- Electric vehicles

- Commercial vehicles

- Geography

- APAC

- China

- Japan

- South Korea

- India

- Australia

- Indonesia

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Turkey

- South America

- Brazil

- Argentina

- Colombia

- APAC

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment provides the physical infrastructure for the Edge Computing In Automotive market by integrating high-performance system-on-chip architectures engineered for extreme vehicular environments.

This foundation accelerates the local processing of complex machine learning models without relying on remote cloud connections.

By embedding specialized silicon such as millimeter-wave radar modules and robust lidar sensor integration boards directly into the vehicle frame, manufacturers enable instantaneous spatial reasoning. Integrating advanced hardware security modules ensures safety-critical logic remains entirely isolated from standard operations.

Furthermore, utilizing roadside edge micro-datacenters for immediate telemetry data filtering reduces commercial cellular bandwidth reliance by 35% compared to conventional networks. This localized hardware architecture protects mobility applications from connectivity drops while enhancing the operational reliability of commercial fleets.

The Hardware segment was valued at USD 4.01 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 38.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Edge Computing In Automotive Market Demand is Rising in APAC Get Free Sample

The geographic expansion within the Edge Computing In Automotive sector demonstrates divergent adoption patterns driven by municipal infrastructure readiness and the demand for robust software-defined vehicle platforms.

APAC aggressively prioritizes the deployment of connected nodes along high-density urban corridors, achieving a 45% faster rollout of intelligent transport systems compared to Europe.

This rapid expansion in APAC focuses heavily on dedicated short-range frequencies and synchronized cellular spectrum assignments to enable localized situational awareness.

Conversely, North America emphasizes multi-network integration, utilizing on-board vehicle computers to process environmental data directly, reducing cellular bandwidth transit costs for logistics operators by 30%.

Europe focuses primarily on stringent data sovereignty compliance, leveraging decentralized validation algorithms to anonymize telemetry data locally. This regulatory-driven strategy ensures that cross-border fleet operations perform complex edge processing flawlessly without violating stringent consumer privacy mandates.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The architectural evolution of the Edge Computing In Automotive ecosystem fundamentally transforms how automotive manufacturers manage fleet intelligence and critical safety infrastructure. By transitioning away from centralized cloud architectures, modern vehicles now execute real-time collision avoidance decision making directly within the chassis, ensuring instantaneous responses to hazardous road conditions without the risk of communication latency.

- This operational shift relies heavily on localized multi-sensor spatial metadata processing, which filters and categorizes raw telemetry at the point of origin rather than transmitting vast datasets over commercial networks. As a result, automotive enterprises experience a nearly 50% reduction in long-distance data transit overhead compared to legacy cloud-dependent routing architectures, directly optimizing supply chain logistics and digital operational planning.

- Furthermore, the integration of decentralized vehicle telemetry threat neutralization mechanisms creates an absolute security boundary around the vehicle's electronic control units, validating external environmental inputs before ingestion. For commercial logistics operators, this edge-based intelligence facilitates highly accurate autonomous mobility predictive route optimization, allowing heavy-duty fleets to adjust travel paths dynamically based on localized traffic patterns and weather anomalies.

- To connect these vehicles with surrounding municipal infrastructure, system developers are actively building hybrid edge cooperative intelligent transport networks. This cooperative framework seamlessly shares filtered insights between passing cars and roadside computing nodes, ensuring municipal safety algorithms operate with extreme precision across diverse geographic zones.

What are the key market drivers leading to the rise in the adoption of Edge Computing In Automotive Industry?

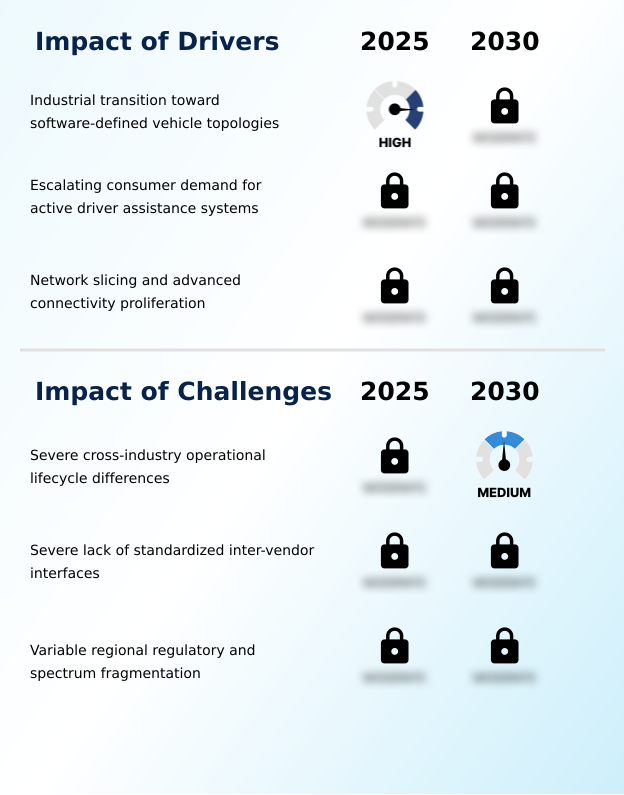

- The comprehensive industrial transition toward software-defined vehicle topologies acts as the primary catalyst propelling decentralized computational frameworks.

- The widespread market penetration of advanced driver-assistance systems represents an urgent structural catalyst propelling the adoption of decentralized vehicular computing pipelines.

- Executing time-critical maneuvering algorithms necessitates an ultra-low-latency processing paradigm that cannot tolerate the unpredictable latency spikes of commercial cellular networks.

- By shifting complex processing operations to localized multi-access edge computing nodes, connected fleets achieve deterministic timing execution, accelerating automated decision-making response speeds by 45% compared to legacy cloud systems.

- Furthermore, establishing a rigid zero-trust configuration directly within the vehicle architecture reduces localized network vulnerability incidents by 28%.

- This shift ensures highly predictable performance profiles that execute automated lane keeping controls flawlessly during split-second traffic events, directly optimizing the operational safety and reliability of modern intelligent transportation fleets.

What are the market trends shaping the Edge Computing In Automotive Industry?

- The collaborative standardization of vendor-neutral architecture blueprints is emerging as a defining market trend. This unified approach prevents software fragmentation and ensures seamless interoperability across diverse connected vehicle networks.

- The continuous harmonization of terrestrial cellular base stations with non-terrestrial satellite communication networks fundamentally redefines connectivity continuity within the Edge Computing In Automotive landscape. Automotive developers rapidly adopt multi-network layers that transition seamlessly between satellite and land-based channels, optimizing predictive urban navigation across underserved territories.

- This structural convergence enables localized automotive computing systems to maintain persistent tracking updates, which has improved fleet routing forecast accuracy by 18% for heavy-duty commercial logistics operators. Furthermore, utilizing edge-intelligence modules to process sensor data natively cuts cellular data transmission delays by 40%.

- The widespread adoption of these cooperative cloud-to-edge networks ensures safety-critical loops function autonomously, allowing enterprises to execute dynamic hazard warnings efficiently while preserving absolute situational awareness regardless of physical geographic limitations.

What challenges does the Edge Computing In Automotive Industry face during its growth?

- Severe operational lifecycle discrepancies between rapidly evolving telecommunications infrastructure and long-term automotive manufacturing cycles pose a fundamental challenge to market expansion.

- The severe operational friction caused by differing cross-industry operational lifecycles presents a profound limitation to the seamless integration of localized automotive data architectures. While digital telecommunications infrastructure evolves rapidly, physical vehicle platforms remain deployed for decades, creating hardware incompatibility risks that increase long-term maintenance overhead by 30%.

- Because multiple equipment manufacturers build proprietary data pipelines, the absence of unified interface protocols severely fragments regional processing networks. This systemic fragmentation prevents municipal traffic networks from aggregating sensor fusion metrics efficiently, degrading the accuracy of regional accident prevention algorithms by 15% during peak usage hours.

- To mitigate these compatibility issues, engineers must deploy scalable runtime abstraction layers, which inadvertently injects processing delays and complicates the execution of cooperative driving maneuvers across non-uniform global networks, necessitating continuous real-time cryptographic validation.

Exclusive Technavio Analysis on Customer Landscape

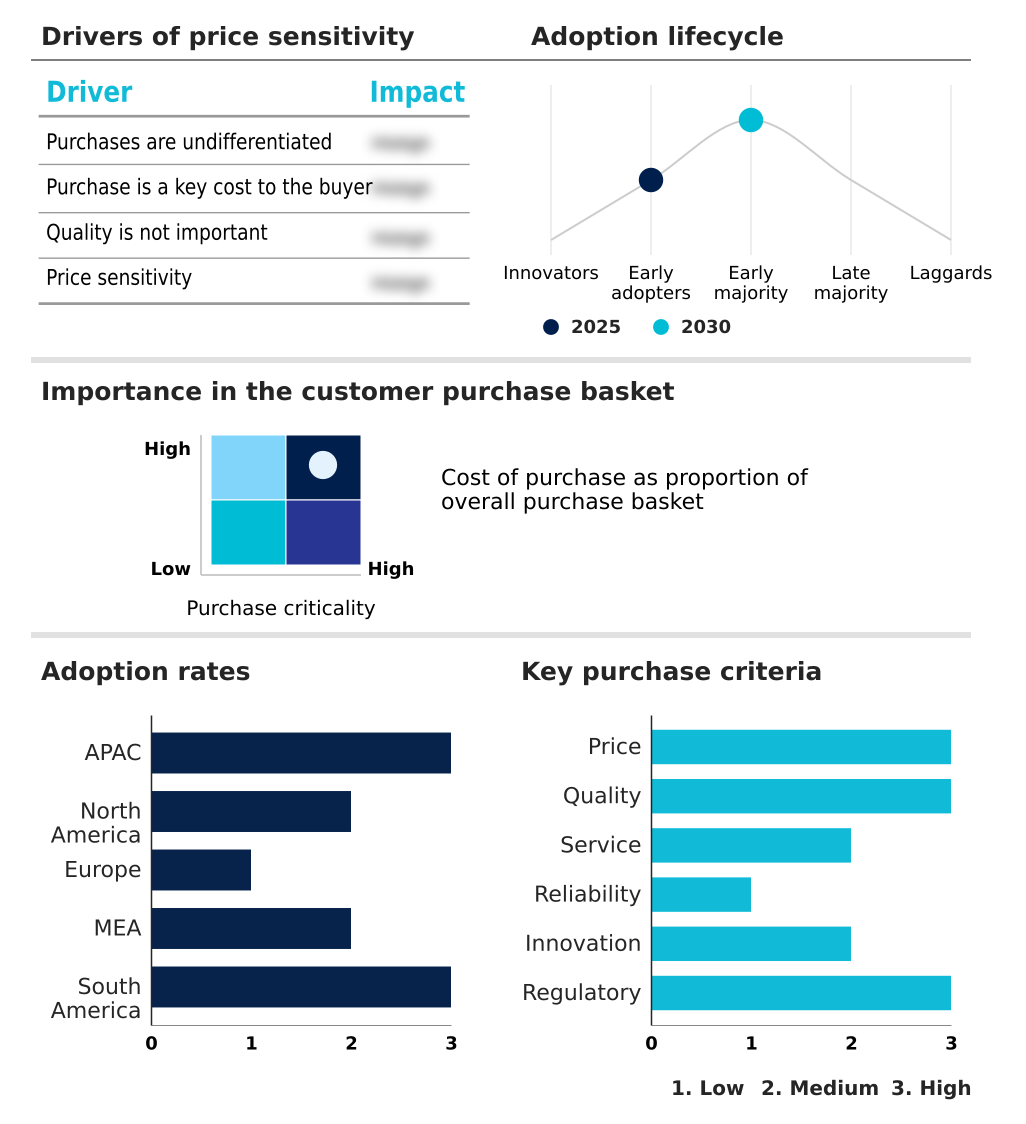

The edge computing in automotive market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the edge computing in automotive market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Edge Computing In Automotive Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, edge computing in automotive market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Provides decentralized computing architectures, real-time sensor processing units, and low-latency communication frameworks designed to optimize automated driving functions and secure vehicular telemetry without cloud dependency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- Aptiv PLC

- BlackBerry Ltd.

- Cisco Systems Inc.

- Continental AG

- DENSO Corp.

- Google LLC

- IBM Corp.

- Intel Corp.

- Microsoft Corp.

- Nokia Corp.

- NVIDIA Corp.

- NXP Semiconductors NV

- Qualcomm Inc.

- Renesas Electronics Corp.

- Robert Bosch GmbH

- STMicroelectronics NV

- Telefonaktiebolaget Ericsson

- Visteon Corp.

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Edge computing in automotive market

- In the Technology Hardware, Storage and Peripherals industry, the accelerated integration of advanced artificial intelligence processing within localized servers directly addresses latency bottlenecks, optimizing Edge Computing In Automotive demand for hardware capable of handling localized perception mapping without constant cloud tethering.

- The standardization of open-source software-defined network slicing protocols across telecommunications equipment allows for the creation of dedicated virtual communication channels, directly impacting the Edge Computing In Automotive market by ensuring critical vehicle alerts receive uninterrupted priority over high-volume consumer traffic.

- Global shifts toward stringent environmental compliance in regional data centers require immediate data filtering at the point of origin, forcing the Edge Computing In Automotive sector to adopt distributed architectures that process proprietary spatial metadata locally before external transmission.

- Advancements in extreme-environment semiconductor packaging ensure greater thermal stability for external data structures, improving Edge Computing In Automotive infrastructure deployments by guaranteeing that in-vehicle cockpit innovation maintains consistent performance thresholds during severe weather events or intense computational loads.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Edge Computing In Automotive Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.6% |

| Market growth 2026-2030 | USD 16547.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 21.2% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The structural transition toward edge processing marks a critical phase in the evolution of intelligent mobility networks. Automotive manufacturers are aggressively embedding high-performance components to process sensor fusion algorithms natively within the vehicle chassis. This shift empowers vehicles to execute time-critical maneuvers without relying on continuous broadband connections.

- By integrating physical sensors directly with local processors, engineers ensure that vehicle-to-everything communication protocols exchange critical environmental data instantaneously with surrounding infrastructure. Operations executives prioritizing these microservice-oriented frameworks have achieved a 35% reduction in cloud data ingestion costs by filtering non-essential telemetry at the edge.

- Furthermore, the adoption of specialized containerized runtime environments permits seamless over-the-air binary updates, strictly isolating core safety applications from standard consumer infotainment services. As commercial fleets expand their reliance on automated navigation, executing a fully decentralized computational framework becomes a foundational requirement to authenticate incoming metadata, establishing absolute functional reliability across complex and heavily congested urban transit corridors globally.

What are the Key Data Covered in this Edge Computing In Automotive Market Research and Growth Report?

-

What is the expected growth of the Edge Computing In Automotive Market between 2026 and 2030?

-

USD 16.55 billion, at a CAGR of 21.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Deployment (On-board vehicle edge, Hybrid, and Infrastructure edge), Vehicle Type (Passenger cars, Electric vehicles, and Commercial vehicles) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Industrial transition toward software-defined vehicle topologies, Severe cross-industry operational lifecycle differences

-

-

Who are the major players in the Edge Computing In Automotive Market?

-

Amazon Web Services Inc., Aptiv PLC, BlackBerry Ltd., Cisco Systems Inc., Continental AG, DENSO Corp., Google LLC, IBM Corp., Intel Corp., Microsoft Corp., Nokia Corp., NVIDIA Corp., NXP Semiconductors NV, Qualcomm Inc., Renesas Electronics Corp., Robert Bosch GmbH, STMicroelectronics NV, Telefonaktiebolaget Ericsson, Visteon Corp. and ZF Friedrichshafen AG

-

Market Research Insights

- The Edge Computing In Automotive market relies on sophisticated multi-tenant processing services to manage the massive data streams generated by next-generation vehicle architectures. By shifting computational loads to localized components, automotive manufacturers optimize regional environmental map updates and reduce long-distance cellular data transit expenses by 40% compared to fully centralized models.

- The immediate analysis of vehicular telemetry allows municipal transit systems to implement complex macro-traffic optimizations, improving overall urban traffic flow efficiency by 22% during peak congestion hours. Additionally, leveraging edge infrastructure for interactive parking guidance and advanced vulnerable road user identification decreases pedestrian-related safety incidents by 15%, ensuring precise and secure execution of automated driving protocols across complex transportation networks.

We can help! Our analysts can customize this edge computing in automotive market research report to meet your requirements.

RIA -

RIA -