Electric Service Companies Market Size 2024-2028

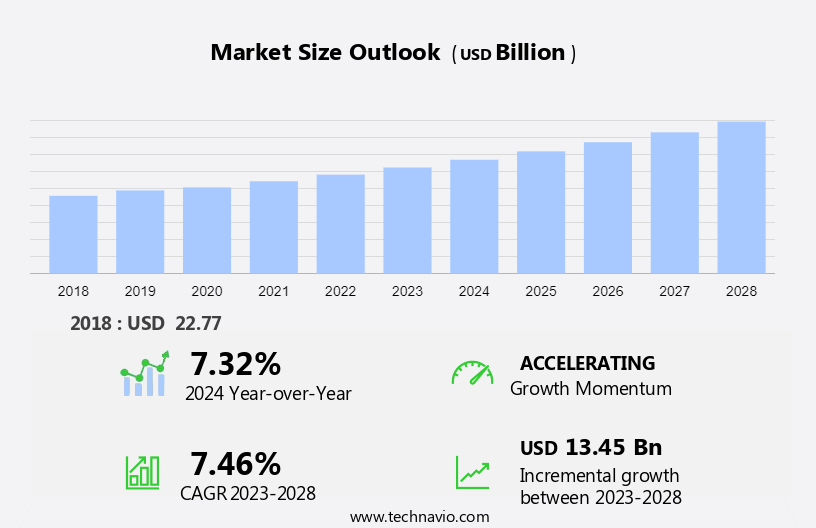

The electric service companies market size is forecast to increase by USD 13.45 billion at a CAGR of 7.46% between 2023 and 2028.

- The market is experiencing significant growth, driven by several key trends and factors. One of the primary drivers is the increasing deployment of smart grid technologies, which enable more efficient energy management and distribution. Another trend is the rising adoption of electrification, as more industries and sectors shift towards electric power to reduce carbon emissions and improve sustainability. However, this market also faces challenges, including the growing risk of cybersecurity threats, which can compromise the integrity of the power grid and disrupt services. As the demand for reliable and secure electric services continues to grow, electric service companies must adapt to these trends and challenges to remain competitive and meet the evolving needs of their customers.

What will the size of the market be during the forecast period?

- The electric service industry encompasses various aspects of electrical power generation, transmission, distribution, and utilization. This sector plays a crucial role in meeting the energy demands of residential, commercial, and infrastructural developments. Energy efficiency and conservation are significant trends shaping the electric service industry. The increasing awareness of energy management and the need to reduce energy consumption have led to the widespread adoption of energy-efficient equipment, such as lighting systems and HVAC systems. Retrofitting buildings with energy-efficient solutions is a growing trend, as it not only helps reduce energy consumption but also lowers operational costs. Modern electrical systems are integrating advanced technologies to optimize energy usage. Renewable energy solutions, such as solar panels and wind turbines, are becoming increasingly popular for electrical power generation. These sources of energy are not only environmentally friendly but also offer cost savings in the long run. Renewable energy sources, including solar and wind, are gaining traction as viable alternatives to traditional energy sources, such as fossil fuels.

- The development of electrical components and systems to effectively harness and distribute renewable energy is crucial for the growth of this sector. Electrical power transmission and distribution networks are undergoing significant upgrades to accommodate the integration of renewable energy sources into the grid. High-voltage transmission lines are being installed to efficiently transport electricity over long distances. The rise of smart buildings and the increasing popularity of electric vehicles are further driving the demand for advanced electrical systems. Energy management software is being used to optimize energy usage in buildings, while electrical infrastructure development is essential for the widespread adoption of electric vehicles. In conclusion, the electric service industry is undergoing a transformation, driven by the need for energy efficiency and the integration of renewable energy sources. The adoption of energy-efficient equipment, the development of advanced electrical systems, and the integration of renewable energy sources into the grid are key trends shaping the future of this sector.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

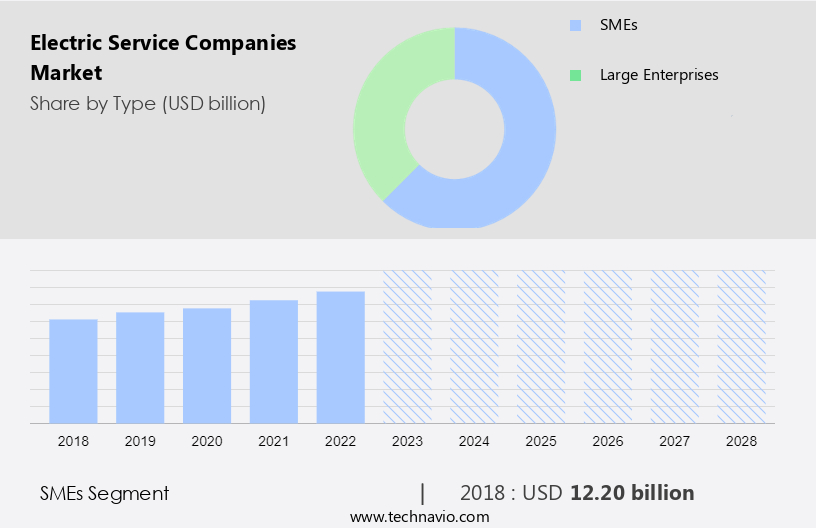

- Type

- SMEs

- Large enterprises

- End-user

- Commercial

- Industrial

- Residential

- Geography

- North America

- US

- APAC

- China

- India

- Europe

- Germany

- France

- South America

- Middle East and Africa

- North America

By Type Insights

- The SMEs segment is estimated to witness significant growth during the forecast period.

Electric service companies in the United States are experiencing significant growth due to the increasing demand for installation, maintenance, and repair services for various electrical systems. Factors such as population growth, urbanization, industrial development, and infrastructure expansion are driving this demand. Advanced technologies, including smart homes, commercial systems, interconnected grids, and smart grid technology, are revolutionizing the power system integration and energy security landscape. SMEs can capitalize on these trends by offering value-added services such as troubleshooting, repairs, and maintenance for electrical components and systems. Moreover, the adoption of innovative technologies like energy management systems, renewable energy solutions, and electric vehicle infrastructure presents new business opportunities for SMEs.

Further, by embracing these technologies, SMEs can improve operational efficiency and offer energy-efficient solutions that cater to the growing awareness of energy conservation and sustainability. Furthermore, energy audit services, energy-efficient equipment, and energy management consulting are essential services that businesses and consumers are investing in to reduce their carbon footprint and contribute to environmental stewardship. In conclusion, the electric service industry in the US is witnessing a swell in demand for various services, from installation and maintenance to repairs and upgrades. SMEs that invest in innovative technologies and offer value-added services can capitalize on this trend and contribute to the development of a sustainable and efficient energy infrastructure.

Get a glance at the market report of share of various segments Request Free Sample

The SMEs segment was valued at USD 12.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

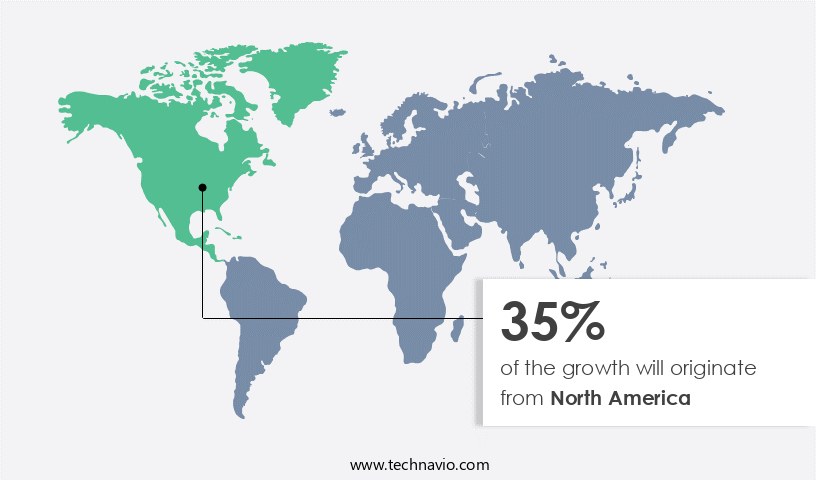

- North America is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The electrical grid forms the backbone of modern electrical systems, with substations, voltage transformers, distribution lines, and various electrical components playing crucial roles in stable power distribution. Electric service companies cater to diverse sectors, including residential settings, commercial establishments, and industrial operations, employing electricians, lighting specialists, and technicians for installations, maintenance, repairs, and troubleshooting. In residential settings, electricians install and maintain electrical panels, switches, circuit breakers, and lighting systems. Commercial and industrial electricians handle more complex installations, such as electrical systems for commercial buildings, interconnected grids, and smart grid technology for power system integration. The growing trend towards smart homes and smart buildings necessitates the development of modern electrical systems, which include electrical software services and energy management systems.

Additionally, the increasing adoption of electric vehicles (EVs) and charging infrastructure further boosts the demand for electrical services, as does the shift towards energy security and carbon reduction strategies. Institutional electrical service providers offer energy audits, electrical engineering, and electrical hardware solutions to help businesses and organizations reduce their electricity consumption patterns and improve energy efficiency. Maintenance services and repairs are essential to ensure the longevity and optimal performance of electrical systems, while smart city initiatives and infrastructure development create new opportunities for electrical service companies. Overall, the economic growth in North America, population expansion, and urbanization trends contribute to the increasing demand for electric services, making it a promising industry for investment and expansion.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Electric Service Companies Market?

The growing deployment of smart grid technologies is the key driver of the market.

- Electric service companies in the US offer a range of specialized services to support the implementation and optimization of smart grid technologies. These services encompass the installation, integration, maintenance, and enhancement of advanced metering infrastructure (AMI), distribution automation, grid analytics, and demand response systems. By providing expertise in system design, engineering, and testing, electric service companies ensure the seamless integration and interoperability of these smart grid components and systems into existing infrastructure. Moreover, the deployment of smart grids is frequently part of larger grid modernization initiatives aimed at upgrading outdated infrastructure, increasing grid resilience, and improving operational efficiency. In this context, electric service companies play a vital role in integrating renewable energy sources, such as wind, solar, biomass, and clean energy technologies, into the grid.

- They also specialize in the installation and maintenance of energy-saving systems, energy management solutions, and electrical power generation systems, including solar panels, wind turbines, and high-voltage transmission lines. Electric service companies' services are essential for enhancing the overall performance and reliability of the electrical power grid. Their expertise in electrical power generation, residential wiring, and electrical service ensures that businesses and households can effectively manage their energy consumption and reduce their carbon footprint. By partnering with electric service companies, organizations and individuals can optimize their energy usage, minimize costs, and contribute to a more sustainable energy future.

What are the market trends shaping the Electric Service Companies Market?

Increasing adoption of electrification is the upcoming trend in the market.

- Electric service companies in the United States are experiencing growth due to the increasing adoption of electric vehicles (EVs) and the electrification of transportation infrastructure. These companies offer services related to the installation, maintenance, and management of EV charging stations and grid integration. The expansion of EV charging infrastructure opens up opportunities for electric service providers to offer specialized services and broaden their customer base. Moreover, the shift towards electric heating, cooling, and HVAC systems in residential, commercial, and industrial buildings fuels demand for electric service companies. They provide installation, maintenance, and repair services for electric heating systems, heat pumps, and air conditioning units.

- As buildings adopt electric heating and cooling solutions, electric service companies can leverage this trend to offer energy-efficient solutions and enhance their service offerings. The electrical industry encompasses various components such as lighting, switches, circuit breakers, electrical panels, and electrical engineering. Electrical hardware and software services are essential for stable power distribution and efficient electrical systems. Commercial and industrial electricians play a crucial role in installing and maintaining electrical systems for businesses, while institutional electrical service caters to schools, hospitals, and other large institutions.

What challenges does Electric Service Companies Market face during the growth?

Rising cybersecurity risks is a key challenge affecting the market growth.

- Electric service companies play a vital role in providing energy to homes and businesses across the United States. They utilize various energy sources, including fossil fuels such as coal and natural gas, nuclear energy, hydroelectric power, wind energy, solar energy, and geothermal energy, to generate electricity. The electrical grid, which consists of power plants, substations, voltage transformers, distribution lines, and other infrastructure, is essential for delivering electricity to residential and commercial settings. However, the increasing digitization and connectivity of electric grids have introduced new vulnerabilities. Malicious actors, including hackers, cybercriminals, and state-sponsored groups, may target electric service companies to disrupt operations, steal sensitive information, or cause physical damage.

- These cyber-attacks can lead to power outages, equipment failures, and service interruptions, negatively impacting customers. Critical systems such as Supervisory Control and Data Acquisition (SCADA) systems, grid control centers, and communication networks are particularly vulnerable. Disruptions to these systems can cause significant disruptions to electric service delivery. For instance, a cyber-attack on a SCADA system could lead to the mismanagement of power generation and distribution, resulting in power outages or even equipment damage. In conclusion, electric service companies face a growing threat from cyber-attacks. These attacks can cause significant disruptions to electric service delivery, negatively impacting customers and the economy.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alpiq Holding Ltd.

- Center Line Electric Inc.

- Eaton Corp. Plc

- Electric Services Inc.

- Enel Spa

- Facility Solutions Group

- General Electric Co.

- George Brazil Plumbing and Electrical

- GREENWAY ELECTRICAL

- Helix Electric

- Honeywell International Inc.

- Johnson Controls

- MMR Group

- Nextera Energy Inc.

- Schneider Electric SE

- Toko Electrical Construction Co. Ltd.

- Veolia Environnement SA

- Iberdrola SA

- Mister Sparky Franchising SPE LLC

- Siemens AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Electric service companies play a crucial role in meeting the energy demands of modern society. With the increasing focus on energy conservation and efficiency, these companies are at the forefront of providing solutions for both residential and commercial settings. They offer a range of services from electrical power generation using renewable energy sources like wind and solar, to energy management and optimization. Energy efficiency projects, such as retrofitting buildings with energy-efficient equipment and lighting systems, are a key area of focus. HVAC systems and lighting retrofits are common practices to reduce energy consumption and improve performance. Renewable energy integration, including the installation and maintenance of solar panels and wind turbines, is another important service. Electric service companies also provide energy management software and services, including energy consumption tracking and performance optimization. They offer energy audit services to help identify areas of improvement and provide solutions for energy security measures during energy crises.

In addition to electrical power generation and management, these companies provide electrical engineering services for stable power distribution and maintenance of electrical components. They employ electricians, technicians, and maintenance services for repairs and troubleshooting in both residential and commercial settings. Electric service companies are also involved in the development of modern electrical systems, including smart homes and buildings, and the integration of electric vehicles and charging infrastructure. They provide installation, maintenance, and repair services for electrical hardware and components, as well as smart grid technologies like self-healing grids and power system integration. Investment in infrastructure development and the integration of renewable energy systems, energy storage systems, and industrial automation are key areas of growth for electric service companies. They offer a range of solutions for energy security, power conversion, and battery storage systems to prevent equipment failure and ensure reliable power distribution.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.46% |

|

Market growth 2024-2028 |

USD 13.45 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.32 |

|

Key countries |

US, China, India, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -