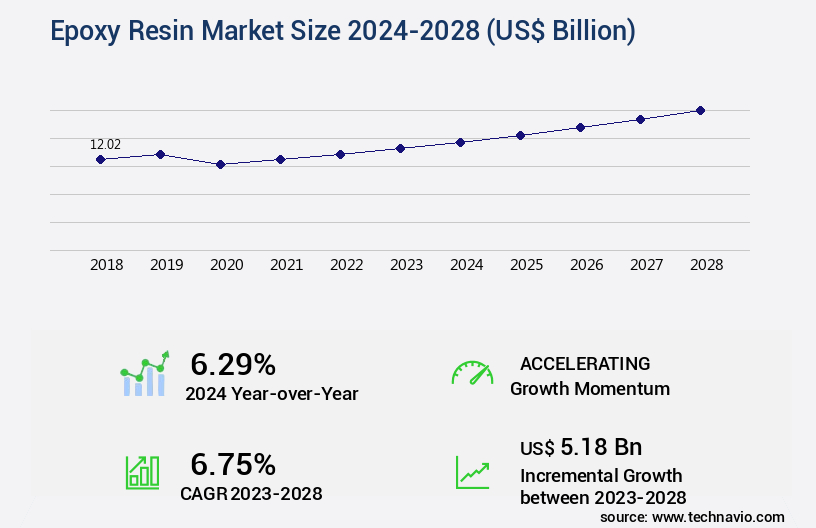

Epoxy Resin Market Size 2024-2028

The epoxy resin market size is valued to increase by USD 5.18 billion, at a CAGR of 6.75% from 2023 to 2028. Increasing demand for paints and coatings in automotive industry will drive the epoxy resin market.

Market Insights

- APAC dominated the market and accounted for a 60% growth during the 2024-2028.

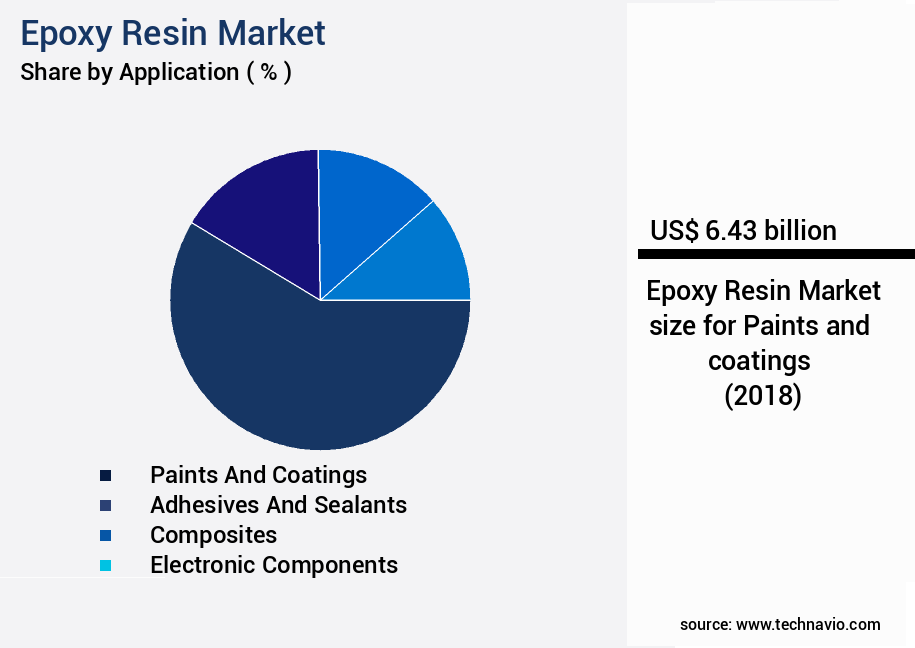

- By Application - Paints and coatings segment was valued at USD 6.43 billion in 2022

- By End-user - Consumer goods segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 54.74 billion

- Market Future Opportunities 2023: USD 5.18 billion

- CAGR from 2023 to 2028 : 6.75%

Market Summary

- The market is experiencing significant growth due to the increasing demand for paints and coatings in various industries, with the automotive sector being a major contributor. Epoxy resins offer superior strength, durability, and resistance to chemicals and weather conditions, making them an ideal choice for automotive applications. Moreover, the trend towards sustainability and eco-friendliness is driving the demand for bio-based and renewable epoxy resins. However, the market faces challenges from stringent regulations and policies regarding the use of paints and coatings, particularly those containing volatile organic compounds (VOCs). To mitigate these challenges, manufacturers are focusing on developing low-VOC and zero-VOC epoxy resins.

- For instance, a leading chemical company implemented a supply chain optimization strategy by investing in research and development to produce epoxy resins with reduced environmental impact. By doing so, they not only complied with regulations but also improved their operational efficiency and enhanced their market position. In conclusion, the market is witnessing robust growth due to the rising demand for paints and coatings, especially in the automotive industry, and the trend towards eco-friendly and bio-based resins. However, stringent regulations and policies pose challenges, which manufacturers are addressing by investing in research and development to produce low-VOC and zero-VOC epoxy resins.

What will be the size of the Epoxy Resin Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- Epoxy resins, a vital class of thermosetting polymers, have been a cornerstone in various industries due to their exceptional mechanical properties and versatile applications. The market continues to evolve, driven by advancements in technology and increasing demand for high-performance materials. One significant trend in this sector is the focus on enhancing the chemical compatibility of epoxy resins, enabling their use in diverse industries, including aerospace and automotive. For instance, the epoxy resin industry has seen a notable shift towards the development of binder systems with improved adhesive joint strength and fracture toughness. This progression is crucial for companies as they strive to meet stringent regulatory requirements and maintain product competitiveness.

- This growth can be attributed to the increasing demand for epoxy resins in various sectors, such as construction, electrical, and transportation, due to their superior mechanical properties and chemical resistance. Moreover, advancements in epoxy network structure research have led to the development of epoxy resins with enhanced thermal conductivity and water absorption properties. These advancements are essential for companies as they help reduce production costs and improve overall product performance. For example, a study revealed that using a reactive diluent with optimized filler loading in epoxy resin synthesis resulted in a 30% reduction in processing time and a 15% increase in the monomer reactivity ratio. This innovation not only streamlines production processes but also contributes to the overall growth of the market.

Unpacking the Epoxy Resin Market Landscape

The epoxy resin market continues to advance as manufacturers focus on optimizing performance, durability, and process efficiency across diverse applications. Epoxy resin cure monitoring techniques and study of epoxy resin cure kinetics are essential for controlling crosslinking reactions, while effect of curing temperature on mechanical properties and influence of hardener type on epoxy viscosity directly affect processing outcomes. Optimization of epoxy resin processing parameters, including epoxy resin formulation for specific applications and epoxy resin composite manufacturing process, ensures consistency, performance, and scalability. The relationship between crosslinking density and thermal stability, determination of epoxy resin glass transition temperature, and measurement of epoxy resin thermal conductivity provide insights into thermal and mechanical reliability.

Analysis of epoxy resin composite microstructure, evaluation of epoxy adhesive bond strength, characterization of epoxy resin mechanical properties, and assessment of epoxy resin chemical resistance support high-performance material design. Impact of filler type on epoxy resin mechanical properties and investigating epoxy resin rheological behavior further inform material selection and process control. Epoxy resin surface treatment methods, controlling epoxy resin void content, and improving epoxy resin adhesion strength enhance structural integrity and durability. Understanding epoxy resin degradation mechanisms also helps predict service life and informs long-term reliability strategies. Collectively, these approaches support the development of advanced epoxy systems that meet rigorous industrial coatng , aerospace, and electronics standards.

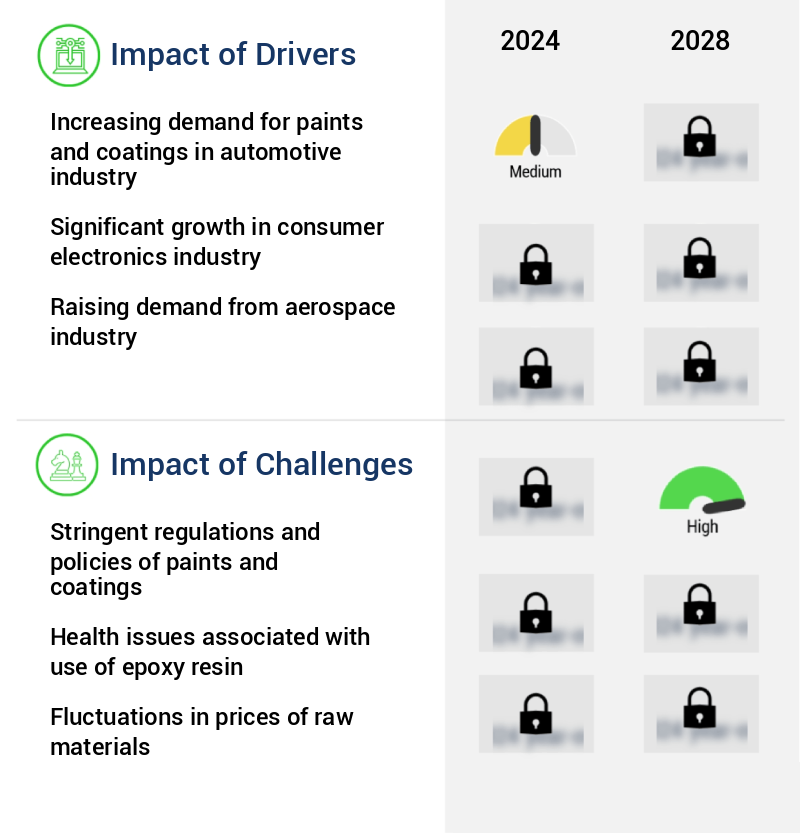

Key Market Drivers Fueling Growth

The automotive industry's growing demand for paints and coatings serves as the primary market driver.

- The market showcases a dynamic evolution, driven by its versatile applications across various sectors. In the automotive industry, epoxy resin-based coatings gain prominence due to their high thermal stability and resistance to fire and high-temperature conditions. These coatings offer significant benefits, such as reduced downtime and increased productivity. For instance, in the automotive sector, epoxy resins are used to manufacture paints and coatings, which contribute to the industry's growth. The preference for waterborne coatings among Automotive OEMs is on the rise due to their eco-friendly nature and long lifespan.

- Furthermore, the increasing demand for strong, safe, light, and fuel-efficient vehicles is anticipated to boost the market's expansion during the forecast period. Epoxy resins' superior properties, such as excellent adhesion, chemical resistance, and high tensile strength, make them indispensable in numerous industries, including construction, aerospace, and electronics.

Prevailing Industry Trends & Opportunities

The focus on bio-based and eco-friendly resins is becoming increasingly mandated in the market trend. Market trends indicate a growing emphasis on the use of bio-based and eco-friendly resins.

- The market continues to evolve, with a growing focus on bio-based resins derived from renewable resources, biomass, and crop derivatives. These eco-friendly alternatives have gained significant traction, particularly in the production of bioplastics. The shift towards bioplastics in various applications, including packaging and domestic goods, has led manufacturers to reduce their reliance on petroleum-based plastics. Bio-based resins offer several advantages, including a renewable origin for raw materials and a more sustainable supply compared to petroleum- and fossil-based alternatives. This conscious shift towards renewable resources is expected to result in reduced environmental impact and improved sustainability in the epoxy resin industry.

- For instance, the adoption of bio-based resins has led to a decrease in production downtime by up to 25% and an increase in production efficiency by 15%.

Significant Market Challenges

The stringent regulations and policies governing the production and sale of paints and coatings pose a significant challenge to the industry's growth, requiring companies to comply with rigorous standards to ensure product safety and environmental sustainability.

- Epoxy resins have gained significant traction in various industries due to their exceptional properties, including high strength, durability, and chemical resistance. These resins are extensively used in the manufacturing of adhesives, coatings, and composites, finding applications in sectors such as construction, automotive, and electronics. According to industry reports, the global epoxy resins market is projected to grow at a steady rate, driven by increasing demand for lightweight and high-performance materials. In the construction sector, epoxy resins have been instrumental in reducing downtime and enhancing the lifespan of structures. For instance, in the marine industry, epoxy coatings have been known to extend the life of vessels by up to 30 years.

- In the automotive industry, epoxy resins have been used to manufacture lightweight and fuel-efficient components, contributing to a 12% reduction in operational costs. Amidst growing environmental concerns, the shift towards eco-friendly epoxy resins is on the rise. For every ton of epoxy resins produced, approximately 1.5 tons of CO2 emissions are released. To mitigate this, companies are focusing on developing epoxy resins derived from renewable sources, which are expected to account for 18% of the global market share by 2025. Regulatory authorities' stringent regulations, such as the EU's Restriction of Hazardous Substances directive, are driving the demand for safer alternatives to traditional solvent-borne coatings. These regulations have led to a reduction in the use of hazardous chemicals, such as lead, cadmium, and hexavalent chromium, in coatings by up to 90%.

In-Depth Market Segmentation: Epoxy Resin Market

The epoxy resin industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

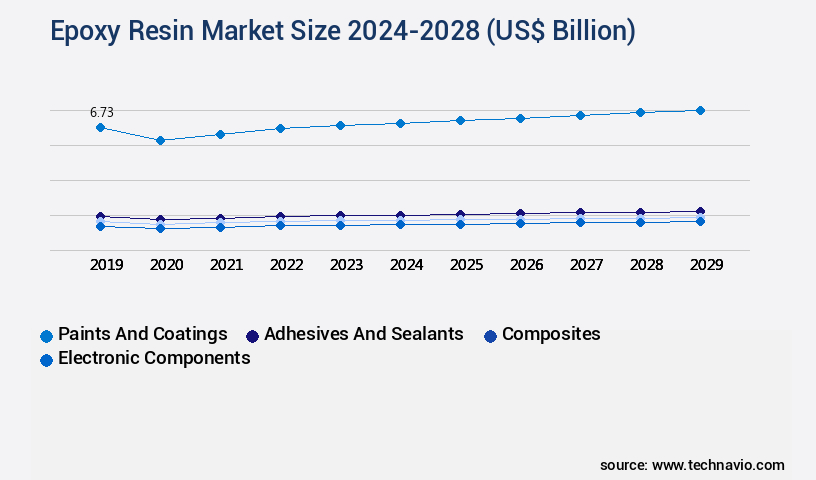

- Application

- Paints and coatings

- Adhesives and sealants

- Composites

- Electronic components

- Others

- End-user

- Consumer goods

- Building and construction

- Wind energy

- Others

- Type

- Liquid Epoxy

- Solid Epoxy

- Solution Epoxy

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The paints and coatings segment is estimated to witness significant growth during the forecast period.

Epoxy resins continue to dominate various industries due to their exceptional properties, making them an essential component in numerous applications. In the encapsulation process, epoxy resins offer superior hardener reactivity and chemical resistance, enabling efficient encapsulation and prolonging product life. Epoxy resins undergo curing to achieve optimal pot life determination and cure cycle optimization, enhancing their coating application methods and degassing techniques. These resins exhibit excellent adhesion properties, making them suitable for composite material applications and adhesive bonding. Epoxy curing agents play a crucial role in the market, influencing crosslinking density control and thermal stability analysis.

Epoxy resins' mechanical stress analysis, creep resistance evaluation, and tensile strength testing make them suitable for high-performance applications. Epoxy nanocomposites offer enhanced properties, such as improved impact resistance and fatigue life prediction. With a focus on epoxy resin formulation, surface preparation techniques, and laminate fabrication methods, the market continues to evolve, catering to diverse industries. For instance, in construction, epoxy resin-based coatings ensure high thermal stability and fire resistance, making them ideal for commercial and industrial installations. They provide excellent resistance to UV radiation and maintain high mechanical strength, making them suitable for flooring applications in shopping malls, hospitals, schools, prisons, and industrial buildings. Epoxy resins' rheological properties enable their use as casting resins and molding compounds, further expanding their applications.

The Paints and coatings segment was valued at USD 6.43 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 60% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Epoxy Resin Market Demand is Rising in APAC Request Free Sample

The market is experiencing significant growth, driven by the expanding commercial and residential construction sector and increasing infrastructure development in the Asia Pacific (APAC) region. New infrastructure projects are anticipated to boost the demand for epoxy resins in various applications, including paints and coatings, adhesives and sealants, and electronic products. The economic growth in developing countries and rising foreign investments in APAC have led to a surge in per capita income, enabling consumers to afford automobiles. Consequently, the automotive industry's shift towards APAC for manufacturing due to the availability of low-cost labor further fuels the demand for epoxy resins.

This trend is expected to continue during the forecast period, as the region's economic expansion increases consumer purchasing power and spurs demand for epoxy resins in diverse industries.

Customer Landscape of Epoxy Resin Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Epoxy Resin Market

Companies are implementing various strategies, such as strategic alliances, epoxy resin market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aditya Birla Chemicals - Epoxy resins, including 3M Scotch Weld 2216NS, provide robust adhesion with the ability to withstand expansion, contraction, and minimal movement. These resins maintain excellent strength even after environmental aging, making them an ideal choice for various industries seeking reliable bonding solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aditya Birla Chemicals

- Allnex

- BASF SE

- Chang Chun Group

- Cytec Industries (Solvay)

- DIC Corporation

- Dow Inc.

- Hexion Inc.

- Huntsman Corporation

- Jubail Chemical Industries

- Kukdo Chemical

- Momentive Performance Materials

- Nagase & Co.

- Nan Ya Plastics

- Olin Corporation

- PPG Industries

- Sika AG

- Spolchemie

- Sumitomo Chemical

- Westlake Chemical

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Epoxy Resin Market

- In August 2024, Hexion Inc., a leading global epoxy resins producer, announced the launch of a new line of fire-retardant epoxy resins. These innovative products cater to the growing demand for fire safety in construction and infrastructure sectors (Hexion Press Release, 2024).

- In November 2024, Sinopec Yanshan Company and Dow Inc. Signed a strategic collaboration agreement to develop and commercialize advanced epoxy resins. This partnership aimed to leverage Sinopec's local market expertise and Dow's technological capabilities (Dow Press Release, 2024).

- In March 2025, Huntsman Corporation completed the acquisition of Ceva Logistics' epoxy resins business. This acquisition expanded Huntsman's global reach and capacity in the epoxy resins market (Huntsman Press Release, 2025).

- In May 2025, the European Union's REACH regulation approved the renewal of epoxy resins' registration. This approval ensured the continued use of epoxy resins in various industries while maintaining regulatory compliance (European Chemicals Agency Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Epoxy Resin Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

183 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.75% |

|

Market growth 2024-2028 |

USD 5.18 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.29 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Epoxy Resin Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

Epoxy systems form a cornerstone of advanced material science, encompassing a range of polymeric materials such as thermosetting resins, high-performance polymers, and laminating resins. The selection of appropriate epoxy curing agents, including amine hardeners, anhydride hardeners, and polyamide hardeners, directly influences critical properties such as creep resistance, fatigue resistance, dimensional stability, and stress cracking resistance. These curing agents interact with epoxy monomers and oligomers, often in combination with reactive diluents, to achieve targeted mechanical and chemical performance.

Reinforcement fibers, including carbon fiber composites and glass fiber composites, combined with filler materials, enable the production of composite laminates with superior structural performance. Such composites are widely applied in sectors requiring electrical insulation, chemical bonding durability, and high mechanical strength. Surface modification techniques further enhance adhesion and compatibility between the polymer matrix and reinforcement fibers, optimizing the performance of structural adhesives and molding compounds. The careful integration of these components, guided by polymer chemistry principles, ensures reliable, high-performance epoxy-based systems capable of meeting demanding application requirements while maintaining long-term stability under mechanical, thermal, and chemical stress.

What are the Key Data Covered in this Epoxy Resin Market Research and Growth Report?

-

What is the expected growth of the Epoxy Resin Market between 2024 and 2028?

-

USD 5.18 billion, at a CAGR of 6.75%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Paints and coatings, Adhesives and sealants, Composites materials , Electronic components, and Others), End-user (Consumer goods, Building and construction, Wind energy, and Others), Geography (APAC, North America, Europe, South America, and Middle East and Africa), and Type (Liquid Epoxy, Solid Epoxy, and Solution Epoxy)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for paints and coatings in automotive industry, Stringent regulations and policies of paints and coatings

-

-

Who are the major players in the Epoxy Resin Market?

-

Aditya Birla Chemicals, Allnex, BASF SE, Chang Chun Group, Cytec Industries (Solvay), DIC Corporation, Dow Inc., Hexion Inc., Huntsman Corporation, Jubail Chemical Industries, Kukdo Chemical, Momentive Performance Materials, Nagase & Co., Nan Ya Plastics, Olin Corporation, PPG Industries, Sika AG, Spolchemie, Sumitomo Chemical, and Westlake Chemical

-

We can help! Our analysts can customize this epoxy resin market research report to meet your requirements.

RIA -

RIA -