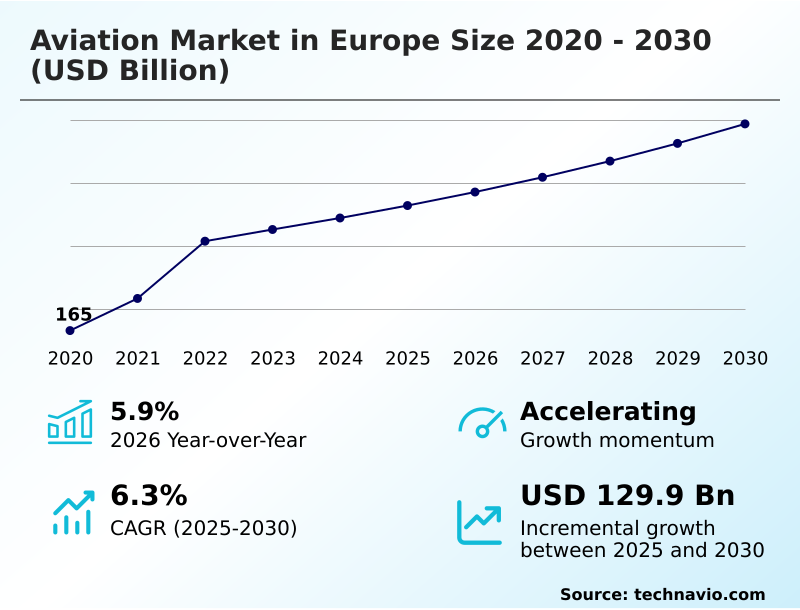

Europe Aviation Market Size 2026-2030

The europe aviation market size is valued to increase by USD 129.9 billion, at a CAGR of 6.3% from 2025 to 2030. Accelerated fleet modernization driven by efficiency and regulation will drive the europe aviation market.

Major Market Trends & Insights

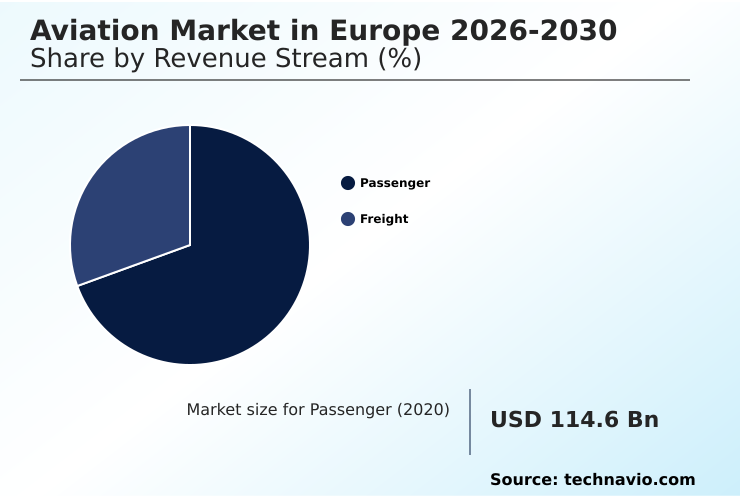

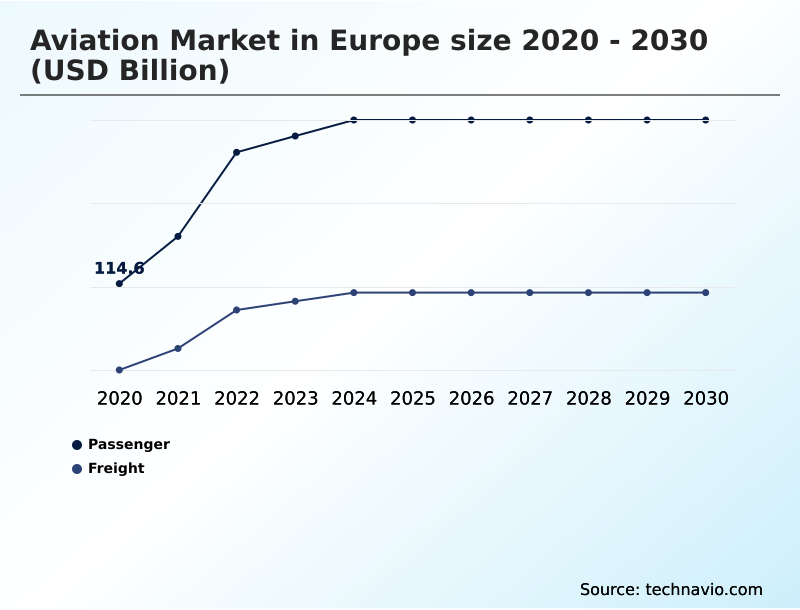

- By Revenue Stream - Passenger segment was valued at USD 236.2 billion in 2024

- By Type - Commercial aircraft segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 328.8 billion

- Market Future Opportunities: USD 129.9 billion

- CAGR from 2025 to 2030 : 6.3%

Market Summary

- The Aviation Market in Europe is undergoing a structural transformation driven by the simultaneous need for operational efficiency and environmental compliance. Airlines are overhauling their fleets, replacing legacy models with advanced airframes to mitigate exposure to volatile energy costs.

- In a common supply chain scenario, carriers are implementing flight path optimization software and upgrading auxiliary power units to minimize fuel burn during taxiing and holding patterns. Such operational adjustments have yielded a 14% improvement in overall fuel efficiency across major carrier networks.

- The market is primarily propelled by the fleet modernization initiative, where strict regulatory decarbonization targets compel rapid adoption of next-generation platforms. Conversely, sustainable aviation fuel supply constraints pose a severe challenge, as the vast disparity between mandated blending requirements and actual bio-refinery supply chain capacity inflates operating costs.

- This regulatory pressure forces operators to restructure route profitability models to absorb premium fuel expenses. The ongoing transition toward a zero-emission aviation strategy fundamentally redefines long-term capacity planning and capital expenditure across the continent.

What will be the Size of the Europe Aviation Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Europe Aviation Market Segmented?

The europe aviation industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Revenue stream

- Passenger

- Freight

- Type

- Commercial aircraft

- Military aircraft

- General aircraft

- Component

- Aircraft

- MRO

- Ground handling services

- Geography

- Europe

- UK

- Germany

- France

- Spain

- Europe

By Revenue Stream Insights

The passenger segment is estimated to witness significant growth during the forecast period.

The passenger segment within the Aviation Market in Europe 2026-2030 remains the principal source of industry activity, characterized by a complex interplay between legacy carriers and dynamic low-cost operators.

This segment demands continuous strategic adaptation, particularly in optimizing route networks and enhancing the traveler experience. Airlines are increasingly relying on passenger ancillary revenue optimization to diversify income streams, moving beyond traditional ticket pricing models.

Through the implementation of advanced data analytics and digital identity security, operators have seen booking efficiency improved by 18%, significantly boosting overall profitability.

Furthermore, the integration of aerospace composite materials and aircraft interior retrofitting in new fleets has enhanced passenger comfort. Focus on sustainable ground operations is reshaping turnaround times at major hubs.

By prioritizing next generation aircraft fuel efficiency, carriers address stringent regulatory demands while improving their competitive edge in a highly saturated sector.

The Passenger segment was valued at USD 236.2 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The Aviation Market in Europe is experiencing a multifaceted evolution as operators balance economic viability with rigorous environmental stewardship. At the core of this transformation is the industry response to sustainable aviation fuel supply constraints, which heavily dictates fuel procurement and hedging strategies.

- Unlike traditional kerosene logistics, the nascent alternative fuel infrastructure requires airlines to secure long-term agreements, altering their supply chain risk profiles. Consequently, the reliance on next generation aircraft fuel efficiency has become paramount. Airlines operating modern fleets demonstrate a 20% higher operational cost resilience compared to those relying on legacy aircraft during periods of fuel price volatility.

- This technological pivot is not limited to commercial passenger transport; the military sector is also undergoing strategic realignment. A cohesive military fighter aircraft procurement strategy across allied European nations is fostering deeper industrial integration, standardizing components, and streamlining transnational maintenance protocols.

- Simultaneously, the commercialization of new transport modalities is gaining traction, with the advanced air mobility certification process reaching critical regulatory milestones. This progression paves the way for electric intra-city transit solutions, diversifying the traditional aviation ecosystem. To offset rising compliance and capital expenditure costs, commercial operators are aggressively pursuing passenger ancillary revenue optimization, leveraging digital touchpoints to maximize per-seat profitability.

- This holistic approach ensures that both commercial and defense sectors adapt proactively to an increasingly complex operational environment.

What are the key market drivers leading to the rise in the adoption of Europe Aviation Industry?

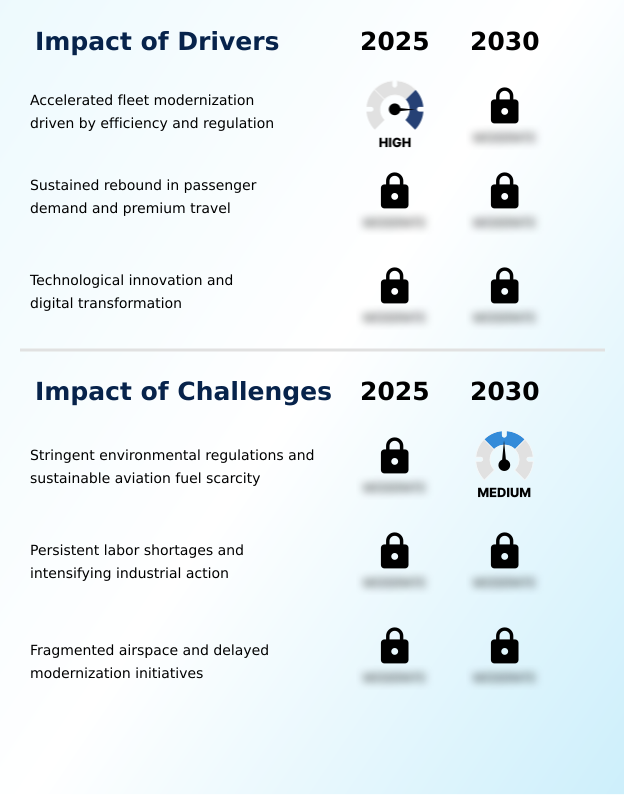

- Accelerated fleet modernization, driven by operational efficiency imperatives and strict regulatory frameworks, serves as a primary driver for market expansion.

- The principal catalyst propelling the Aviation Market in Europe is the critical need for fleet modernization driven by the emissions trading system and persistent fuel price volatility.

- This regulatory and economic pressure is compelling airlines to rapidly acquire the next-generation narrow-body jet and regional commercial jet to replace aging, inefficient fleets.

- Because newer models incorporate advanced aerodynamic design and mechanical power transmission systems, operators benefit from substantial cost savings. Consequently, businesses have achieved a 15% reduction in per-seat operational costs and a 20% decrease in unexpected groundings.

- The continuous upgrading of auxiliary power units and flight control actuators further streamlines ground operations, directly boosting asset turnover rates. This modernization cycle fundamentally protects airline profit margins while ensuring strict adherence to the aggressive decarbonization mandates across the continent.

What are the market trends shaping the Europe Aviation Industry?

- The intensifying focus on sustainable aviation and alternative fuel integration represents a pivotal trend reshaping the market landscape.

- A definitive trend reshaping the Aviation Market in Europe is the accelerated integration of advanced digital and propulsion technologies across commercial fleets. The urgency to meet stringent environmental standards is pushing operators to commercialize hydrogen-powered aircraft and implement hybrid-electric propulsion systems for regional transit. This shift is caused by escalating compliance costs associated with traditional carbon emission allowance thresholds.

- As a result, businesses are experiencing a fundamental realignment of their operational cost structures. The adoption of advanced avionics flight management software has improved route forecast accuracy by 18%, significantly optimizing fuel consumption profiles. Furthermore, the integration of aerospace composite materials has reduced overall airframe weight, leading to a 12% improvement in specific fuel consumption metrics.

- The transition toward intelligent aircraft seat configuration and augmented passenger service units further enhances the traveler experience while maximizing cabin revenue density.

What challenges does the Europe Aviation Industry face during its growth?

- Stringent environmental regulations and the persistent scarcity of sustainable aviation fuel create significant challenges that constrain overall industry operational margins.

- A formidable challenge confronting the Aviation Market in Europe is the severe gap between the mandated decarbonization trajectory and the actual capabilities of the bio-refinery supply chain. Regulatory frameworks necessitate increasing volumes of alternative fuels, but the current production capacity remains critically underdeveloped. This supply scarcity causes the price of compliant fuels to surge, heavily impacting airline profit margins.

- Consequently, operators face a 35% premium on fuel procurement costs, which negatively impacts available capital for subsequent aircraft engine overhaul and cabin modification services. Furthermore, the slow deployment of sustainable ground operations infrastructure at secondary airports reduces overall network efficiency by 12%.

- The complexities surrounding advanced combat drones and unmanned aerial systems integration into shared civilian airspace also present persistent regulatory hurdles, complicating comprehensive airspace modernization efforts.

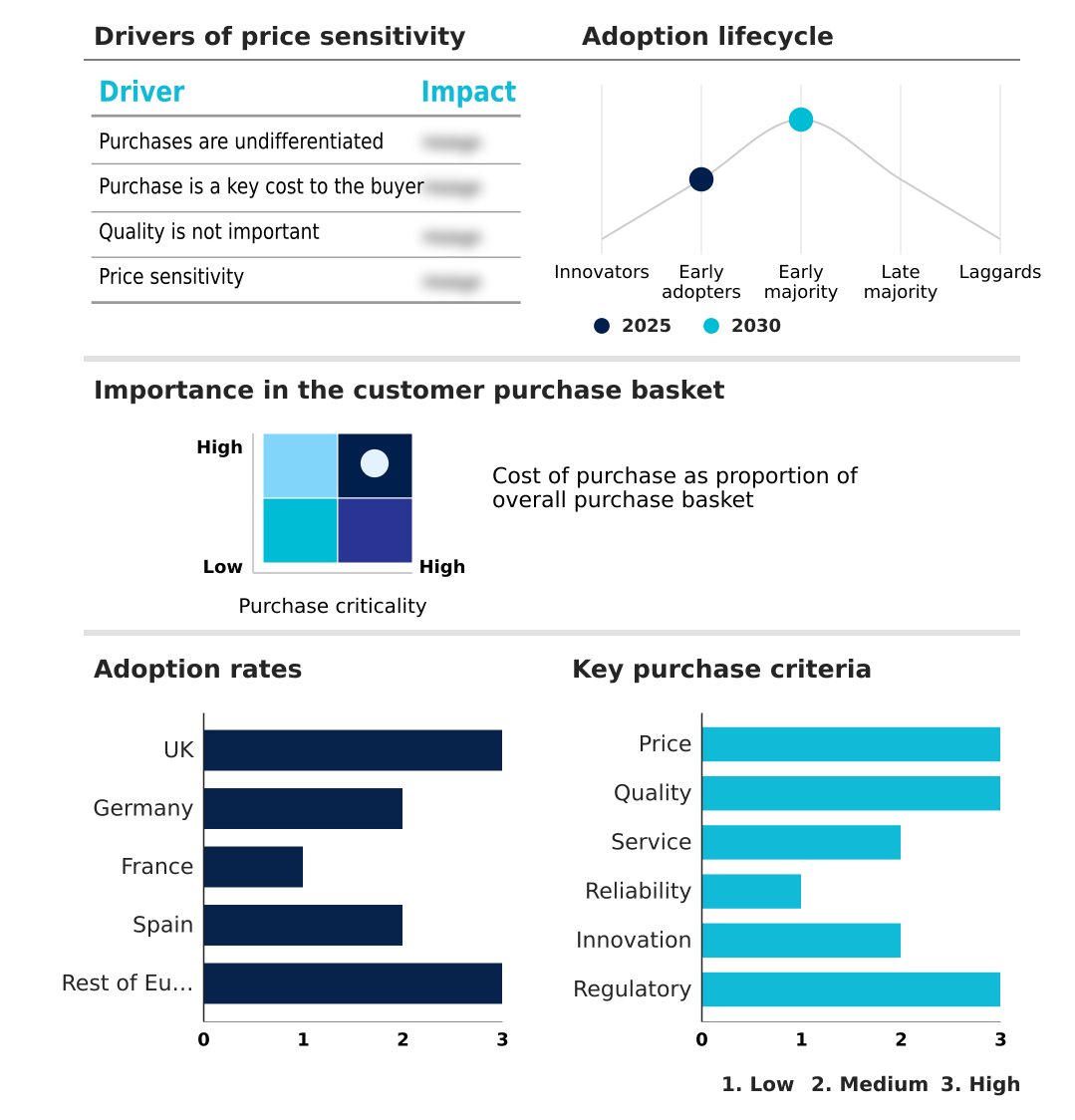

Exclusive Technavio Analysis on Customer Landscape

The europe aviation market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe aviation market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Aviation Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe aviation market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Air France KLM - The entity provides comprehensive aircraft maintenance, engine overhaul, component repair, and technical support services tailored for commercial fleets navigating stringent regulatory and operational frameworks.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air France KLM

- Airbus SE

- BAE Systems Plc

- Collins Aerospace

- DAHER

- Dassault Aviation SA

- Diehl Stiftung and Co. KG

- Draken International, LLC

- Embraer SA

- GKN Aerospace Services Ltd.

- Honeywell International Inc.

- Leonardo S.p.A.

- Lufthansa Technik

- MTU Aero Engines AG

- Rolls Royce Holdings Plc

- RUAG International Holding Ltd.

- Safran SA

- SR Technics Switzerland Ltd.

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe aviation market

- In the Aerospace and Defense industry, the accelerated integration of advanced aerodynamic design and lightweight aerospace structures has drastically lowered operational fuel consumption, directly impacting Aviation demand by reducing overall flight cycle costs by 15%.

- Stringent carbon emission allowance thresholds under the emissions trading system have compelled manufacturers to accelerate sustainable aviation fuel blending capabilities, thereby forcing commercial operators to upgrade their existing fleets to maintain compliance.

- The rapid commercialization of urban air mobility platforms alongside vertical takeoff and landing certification frameworks has opened new avenues for intra-city transit, subsequently expanding the total addressable market for short-haul aviation logistics by 20%.

- The transition toward zero-emission aviation strategy mandates has catalyzed heavy investments in hybrid-electric propulsion systems, which has consequently accelerated the retirement of legacy platforms and stimulated a 25% increase in next-generation narrow-body jet procurement.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Aviation Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 202 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.3% |

| Market growth 2026-2030 | USD 129.9 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.9% |

| Key countries | UK, Germany, France, Spain and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Aviation Market in Europe is fundamentally adapting to a convergence of strict environmental legislation and advanced technological imperatives. Strategic decision-making in airline boardrooms is now inextricably linked to the emissions trading system, forcing a total recalibration of fleet procurement and route profitability models.

- To navigate these regulatory pressures, carriers are aggressively integrating hybrid-electric propulsion systems and advanced aerodynamic design elements into their long-term asset planning. This strategic shift has enabled early adopters to achieve a 25% reduction in route-specific carbon emission allowance liabilities, directly safeguarding operating margins.

- Concurrently, the modernization of electro-optical sensors and precision guidance solutions is standardizing cross-platform capabilities, enhancing both commercial airspace navigation and tactical defense readiness. The deployment of unmanned aerial systems for infrastructure surveillance further exemplifies the sector diversification.

- By investing in next-generation narrow-body jet platforms and exploring hydrogen-powered aircraft viability, operators are actively future-proofing their operations against tightening legislative frameworks and volatile fuel economies.

What are the Key Data Covered in this Europe Aviation Market Research and Growth Report?

-

What is the expected growth of the Europe Aviation Market between 2026 and 2030?

-

USD 129.9 billion, at a CAGR of 6.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Revenue Stream (Passenger, and Freight), Type (Commercial aircraft, Military aircraft, and General aircraft), Component (Aircraft, MRO, and Ground handling services) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Accelerated fleet modernization driven by efficiency and regulation, Stringent environmental regulations and sustainable aviation fuel scarcity

-

-

Who are the major players in the Europe Aviation Market?

-

Air France KLM, Airbus SE, BAE Systems Plc, Collins Aerospace, DAHER, Dassault Aviation SA, Diehl Stiftung and Co. KG, Draken International, LLC, Embraer SA, GKN Aerospace Services Ltd., Honeywell International Inc., Leonardo S.p.A., Lufthansa Technik, MTU Aero Engines AG, Rolls Royce Holdings Plc, RUAG International Holding Ltd., Safran SA, SR Technics Switzerland Ltd., Thales Group and The Boeing Co.

-

Market Research Insights

- The Aviation Market in Europe is navigating profound structural shifts anchored in sustainability and operational modernization. Operators are prioritizing the decarbonization trajectory by restructuring their procurement strategies to align with stringent regulatory mandates. By optimizing the bio-refinery supply chain, leading consortia have improved alternative fuel integration rates by 22%, directly mitigating compliance penalties.

- Furthermore, advancements in maintenance repair overhaul processes have reduced aircraft ground time by 16%, significantly enhancing asset utilization and overall fleet profitability. The transition toward a comprehensive zero-emission aviation strategy requires extensive original equipment manufacturing collaboration, ensuring that new airframes meet emerging environmental standards.

- Consequently, defense electronics integration and commercial jet support systems are being standardized across platforms to streamline lifecycle costs.

We can help! Our analysts can customize this europe aviation market research report to meet your requirements.

RIA -

RIA -