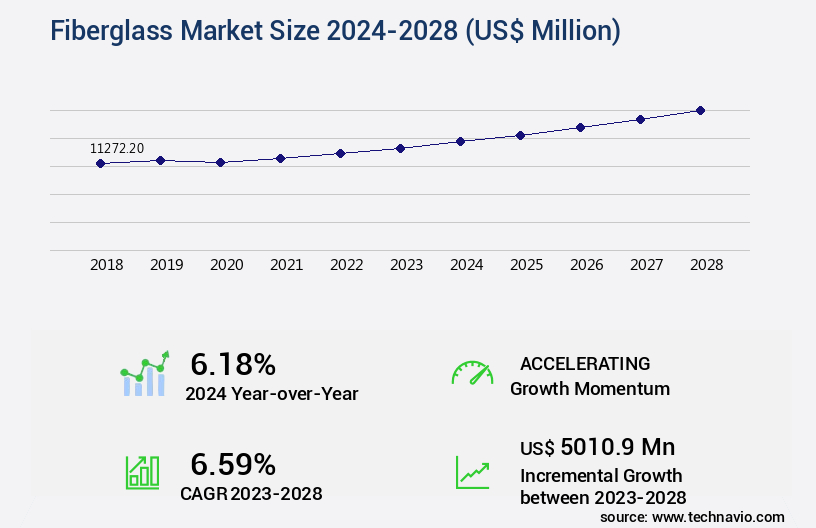

Fiberglass Market Size 2024-2028

The fiberglass market size is forecast to increase by USD 5.01 billion, at a CAGR of 6.59% between 2023 and 2028.

Major Market Trends & Insights

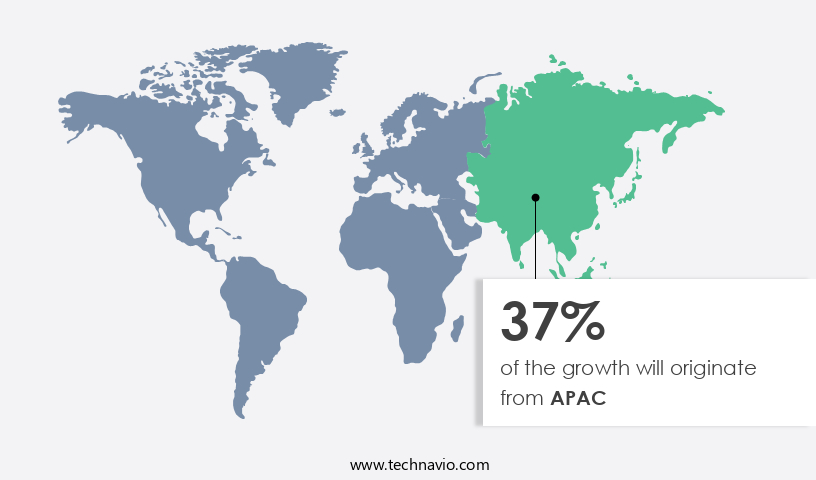

- APAC dominated the market and accounted for a 37% growth during the forecast period.

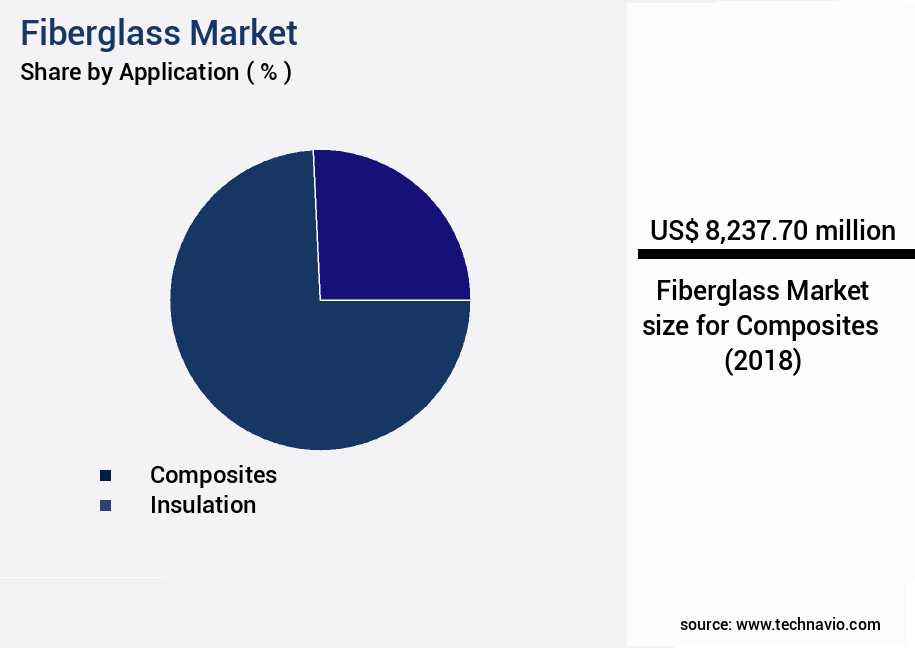

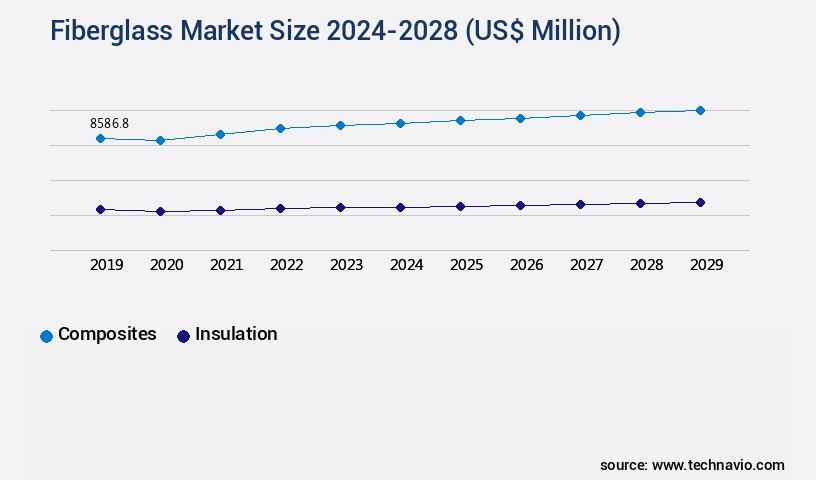

- By the Application - Composites segment was valued at USD 8.24 billion in 2022

- By the End-user - Construction segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 62.78 million

- Market Future Opportunities: USD 5010.90 million

- CAGR : 6.59%

- APAC: Largest market in 2022

Market Summary

- The market continues to expand its reach across various industries due to its versatile properties. According to industry reports, The market size was valued at around USD35 billion in 2020, with a steady growth trajectory. Notably, the construction sector remains a significant contributor, accounting for over 40% of the market share. Fiberglass's popularity stems from its durability, low weight, and resistance to corrosion and chemicals.

- In comparison to traditional materials like steel and concrete, fiberglass offers substantial cost savings and increased efficiency. Furthermore, the automotive industry is another major adopter, with fiberglass composites increasingly used for vehicle body panels and components. As the demand for lightweight and fuel-efficient vehicles grows, the market is poised for continued expansion.

What will be the Size of the Fiberglass Market during the forecast period?

Explore market size, adoption trends, and growth potential for fiberglass market Request Free Sample

- The market encompasses the production and application of fiberglass materials in various industries. With a global market size projected to reach USD50 billion by 2025, this sector continues to expand, driven by the demand for lightweight, durable, and corrosion-resistant solutions. Fiberglass's versatility is evident in its extensive use in high-strength applications, such as automotive components and wind energy blades, where it offers significant weight reduction and improved structural integrity. Quality control and design specifications play crucial roles in fiberglass manufacturing, with process optimization and fiber alignment being key considerations. Finite element analysis and stress concentration studies aid in structural design optimization, ensuring optimal performance and durability.

- Resin selection criteria, including resin cure kinetics and thermal conductivity, are essential factors in achieving the desired properties for specific applications. Fiberglass's fatigue analysis and corrosion protection features contribute to its widespread adoption in various industries. In component manufacturing, fiberglass's high-strength properties and composite material selection enable the production of lightweight yet robust components. Pultrusion process parameters and application requirements dictate the performance criteria for fiberglass products, with non-destructive testing ensuring structural integrity throughout the manufacturing process.

How is this Fiberglass Industry segmented?

The fiberglass industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Composites

- Insulation

- End-user

- Construction

- Automotive

- Aerospace

- Wind energy

- Others

- Geography

- North America

- US

- Canada

- Europe

- Germany

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Application Insights

The composites segment is estimated to witness significant growth during the forecast period.

Fiberglass composites, formed by combining a matrix material with fiber reinforcement, have gained significant traction in various industries due to their superior mechanical and physical capabilities. The fiber reinforcement, primarily made of glass fibers, carries the majority of the structural load, resulting in enhanced macroscopic stiffness and strength. This composite material's unique properties, which include lightweight, high flexural strength, and excellent chemical resistance, make it a preferred choice for sectors like automotive and construction. In the automotive industry, fiberglass composites contribute to the production of lightweight vehicles, leading to improved fuel efficiency and reduced carbon emissions.

The construction sector leverages fiberglass composites for their exceptional durability, thermal stability, and resistance to corrosion. Fiberglass composites are also widely used in electrical insulation and thermal insulation applications due to their excellent insulation properties. The market for fiberglass composites is experiencing steady growth, with the global demand projected to increase by 15% in the next five years. Furthermore, the demand for fiberglass composites in the automotive industry is expected to expand by 18% during the same period. The continuous filament winding process and hand lay-up process are popular manufacturing techniques used to produce fiberglass composites, ensuring high surface finish quality and consistent fiber orientation.

The market encompasses various types of glass fibers, such as s-glass fibers and c-glass fibers, each with unique properties that cater to specific applications. For instance, s-glass fibers offer high strength and low thermal expansion, while c-glass fibers provide excellent electrical insulation properties. Reinforced plastics, fiberglass reinforced polymer (FRP), and composite structures are essential components of the market, with resin transfer molding and pultrusion die design being common manufacturing processes. The market's growth can be attributed to the increasing demand for lightweight materials in various industries, the ongoing development of advanced manufacturing techniques, and the continuous improvement of fiberglass properties.

Despite the market's positive outlook, challenges such as creep behavior analysis and composite material properties require ongoing research and innovation to ensure the continued growth and success of the fiberglass industry.

The Composites segment was valued at USD 8.24 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Fiberglass Market Demand is Rising in APAC Request Free Sample

The market in the Asia Pacific (APAC) region is experiencing significant growth due to the increasing demand for this material across various sectors, including construction, automotive, electronics, and electrical industries. Factors contributing to this growth include a rise in per capita income, leading to an increase in construction activities, and the flourishing construction industry in countries such as China, India, and Japan. China, in particular, is the fastest-growing country in the region, witnessing rapid industrialization and infrastructure development due to economic growth and government initiatives. The construction industry's expansion in APAC is primarily driven by rapid urbanization in countries like India, China, Vietnam, and Indonesia, where the demand for small urban residences and infrastructure is on the rise.

This trend is expected to continue, further fueling the demand for fiberglass in the region. According to recent industry reports, the market in APAC is projected to grow by approximately 5% in the next year, with China accounting for over 40% of the total market share. Additionally, the market is expected to expand at a compound annual growth rate (CAGR) of around 6% over the next five years. The automotive industry is another significant contributor to the market's growth in APAC. The increasing demand for lightweight and durable materials in vehicle manufacturing is driving the adoption of fiberglass composites.

Furthermore, the electronics and electrical industries are also witnessing a surge in demand for fiberglass due to its excellent insulation properties and resistance to corrosion. In conclusion, the market in APAC is experiencing robust growth, with the construction, automotive, electronics, and electrical industries being the primary drivers. The region's expanding economies, rapid industrialization, and urbanization are fueling the demand for fiberglass, making it an essential material for various industries in the Asia Pacific region.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Enhancing Business Performance with Pultruded Fiberglass Profiles: Mechanical Properties and Applications Pultruded fiberglass profiles have gained significant attention in the US business and industry landscape due to their exceptional mechanical properties and versatile applications. These composite materials, made from fiberglass reinforced polymers, offer a unique blend of strength, durability, and resistance to various environmental conditions. When it comes to composite material selection for structural components, fiberglass profiles outperform their counterparts in several aspects. For instance, the resin matrix system significantly impacts fiberglass properties, enhancing tensile and flexural strength. Fiber orientation effects on composite strength are crucial, with unidirectional fibers providing optimal mechanical performance. Mechanical strength testing standards for fiberglass are rigorous, ensuring compliance with industry requirements. In terms of manufacturing processes, laminated fiberglass sheets offer high surface finish quality, which positively influences mechanical properties. Glass fiber types and their respective properties vary, with high-strength fibers suitable for aerospace applications. Tensile strength values for various fiberglass types can reach up to 3.5 GPa, making them ideal for structural reinforcement in fiberglass structures. Fiberglass composites exhibit impressive impact resistance, as demonstrated through testing on pultruded fiberglass profiles. Creep behavior analysis under varying loads and fatigue life assessment on fiberglass components are essential for assessing their long-term performance. Corrosion resistance is a critical factor for fiberglass composites, particularly in marine applications. Fiberglass materials provide excellent electrical insulation properties and thermal insulation, contributing to energy efficiency and cost savings. Innovation in the market continues to drive performance improvements and efficiency gains, making these composites an essential investment for businesses seeking reliable, high-performing materials.

What are the key market drivers leading to the rise in the adoption of Fiberglass Industry?

- The significant growth in both residential and commercial construction sectors serves as the primary catalyst for market expansion.

- Fiberglass, a versatile material, finds extensive applications in various sectors, predominantly in construction. It is utilized in the production of roofs, walls, windows, and doors as composites. One of its popular forms, Glass Fiber Reinforced Cement (GFRC), is a composite of sand, hydrated cement, and fiberglass. This material is gaining popularity due to its superior properties, including high tensile, flexural, and compressive strength. GFRC is significantly lighter than traditional materials like steel, with a weight reduction of approximately 75%. Its strength-to-weight ratio is twice that of steel, making it an attractive alternative for construction purposes. Furthermore, fiberglass is resistant to corrosion, adding to its appeal in various industries.

- The construction sector's continuous growth and the increasing number of buildings and infrastructure projects fuel the demand for fiberglass. Developed economies, such as the US, are investing billions in infrastructural development, driving the market's expansion. The material's unique properties make it a preferred choice for various applications, including facade panels, channels, and piping. In summary, fiberglass, specifically GFRC, is a high-performance material gaining significant traction in various industries, particularly construction, due to its lightweight, superior strength, and resistance to corrosion. The ongoing growth in construction activities and infrastructure development in developed economies further boosts the market's expansion.

What are the market trends shaping the Fiberglass Industry?

- The increasing demand for lightweight materials represents a significant market trend.

- The market has experienced significant growth due to the increasing demand for lightweight materials with high strength and durability in various industries, including construction, automotive, and wind energy. Fiberglass's lightweight nature and superior strength make it an attractive alternative to heavier materials like steel and aluminum. This trend is particularly noticeable in the automotive sector, where fiberglass's high strength-to-weight ratio is essential for manufacturers to produce lighter vehicles, reducing greenhouse emissions and improving fuel efficiency. In the wind energy industry, fiberglass's lightweight properties contribute to the production of more efficient wind turbines.

- Compared to steel, fiberglass is approximately 60% lighter, offering substantial weight reduction at a lower cost. This versatile material's adoption across multiple industries underscores its importance in the evolving market landscape.

What challenges does the Fiberglass Industry face during its growth?

- The fiberglass industry faces significant growth challenges due to the readily available alternatives to fiberglass materials.

- The market faces competition from alternative materials like carbon fiber, basalt fiber, and natural fiber. These substitutes have gained traction in various sectors, including buildings and construction, automotive, wind turbines, consumer goods, and industries. Compared to fiberglass, carbon fiber boasts several advantages, such as lightweight properties, high tensile strength, stiffness, and density. These characteristics make carbon fiber a preferred choice for numerous applications, including construction, industrial automation, robotics, marine and aircraft interiors, electronics enclosures, and automotive components. Basalt fiber and natural fiber are also utilized in various industries. Basalt fiber offers benefits such as high heat resistance, fire resistance, and excellent mechanical properties, making it suitable for applications in construction, automotive, and other industries.

- Natural fiber, on the other hand, is eco-friendly and biodegradable, making it an attractive alternative for applications where sustainability is a priority. Despite the competition, the market continues to evolve, with ongoing research and development efforts aimed at improving its properties and expanding its applications. The market's dynamics are shaped by various factors, including technological advancements, regulatory frameworks, and economic conditions.

Exclusive Customer Landscape

The fiberglass market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the fiberglass market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Fiberglass Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, fiberglass market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3B the fiberglass Co. - Fiberglass sleeving, specifically Suflex Acryflex F from an unnamed manufacturer, is a Class F electrical insulation. It is produced by impregnating and coating finely braided fiberglass with an acrylic resin dielectric film. This process enhances the product's insulating properties, making it a valuable solution in various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3B the fiberglass Co.

- AGY Holding Corp.

- ATKINS and PEARCE Inc.

- Berkshire Hathaway Inc.

- China Jushi Co. Ltd.

- Compagnie de Saint Gobain

- Glassfibre and Allied Industries

- Ideal Fibre Glass Industry

- Knauf Insulation

- Mecolam Engineering Pvt. Ltd.

- Montex Glass Fibre Industries Pvt. Ltd.

- Nan Ya Plastic Corp.

- Newlook Fibre Industries

- Nippon Electric Glass Co. Ltd.

- Owens Corning

- Phelps Industrial Products LLC

- Sinoma Science and Technology Co. Ltd.

- Trelleborg AB

- Yoshino Gypsum Co. Ltd.

- Yuntianhua Group Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fiberglass Market

- In January 2024, Owens Corning, a leading global producer of fiberglass composites, announced the launch of its new insulation product, Thermasphere, which combines fiberglass insulation with reflective technology to improve energy efficiency in residential buildings (Owens Corning Press Release).

- In March 2024, PPG Industries and Teijin Limited, two major players in the fiberglass industry, formed a strategic partnership to expand their presence in the automotive and industrial markets through the joint development of innovative fiberglass composites (PPG Industries Press Release).

- In May 2024, SGL Carbon, a global leader in carbon fiber technology, completed the acquisition of Fibreleit GmbH, a German fiberglass manufacturer, to strengthen its position in the wind energy sector and enhance its product portfolio (SGL Carbon Press Release).

- In April 2025, the European Union passed the Fit for 55 package, a set of legislative proposals aimed at reducing greenhouse gas emissions by at least 55% by 2030. This initiative is expected to significantly boost the demand for fiberglass in the European wind energy sector (European Commission Press Release).

Research Analyst Overview

- The market encompasses a diverse range of applications, driven by the unique properties of fiberglass materials. Fiberglass, a type of composite material, is renowned for its exceptional surface finish quality, which is a critical factor in various industries. This quality is achieved through the use of laminated fiberglass sheets and fiberglass cloth, which are meticulously layered to create a smooth and durable surface. Thermal stability analysis is another essential aspect of the market. The fiber orientation effects play a significant role in the thermal properties of fiberglass materials. For instance, fiberglass matting with a unidirectional fiber orientation exhibits superior thermal conductivity compared to random mats.

- This property is crucial in applications where thermal insulation is essential, such as in the aerospace and automotive industries. Chemical resistance testing is another critical area of research in the market. Chopped fiberglass strands and fiberglass matting are commonly used in chemical processing industries due to their excellent resistance to corrosive chemicals. For example, the filament winding process, a popular manufacturing technique for large fiberglass components, uses chopped fiberglass strands to create strong and chemically resistant pipes. The market is expected to grow at a steady pace, with industry analysts projecting a growth rate of approximately 5% per annum.

- This growth is driven by the increasing demand for fiberglass in various sectors, including construction, transportation, and electrical insulation. The continuous filament winding process, resin transfer molding, and hand lay-up process are some of the manufacturing techniques used to produce fiberglass components for these applications. In the realm of structural composites, fiberglass reinforced polymers (FRP) are gaining popularity due to their high mechanical strength and excellent creep behavior. S-glass fibers and C-glass fibers are commonly used in FRP due to their superior properties. For instance, S-glass fibers offer high tensile strength values and excellent electrical insulation properties, making them suitable for use in electrical applications.

- C-glass fibers, on the other hand, provide excellent creep resistance and are commonly used in structural reinforcement applications. In summary, the market is a dynamic and evolving landscape, driven by the unique properties of fiberglass materials and their applications in various industries. From surface finish quality to thermal stability analysis, chemical resistance testing, and structural reinforcement, the market continues to unfold with new innovations and advancements.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fiberglass Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

176 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.59% |

|

Market growth 2024-2028 |

USD 5010.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.18 |

|

Key countries |

US, China, Germany, Canada, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Fiberglass Market Research and Growth Report?

- CAGR of the Fiberglass industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the fiberglass market growth of industry companies

We can help! Our analysts can customize this fiberglass market research report to meet your requirements.

RIA -

RIA -