Gastrointestinal Bleeding Treatment Market Size 2024-2028

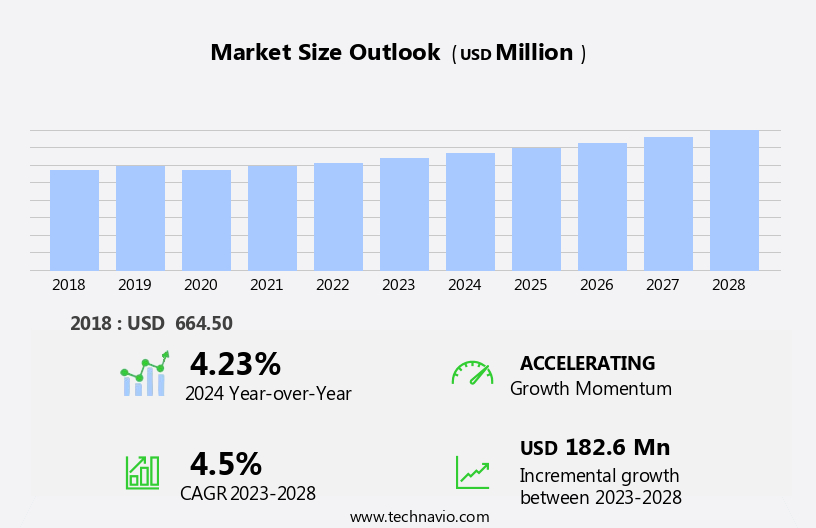

The gastrointestinal bleeding treatment market size is forecast to increase by USD 182.6 billion at a CAGR of 4.5% between 2023 and 2028.

- The market is experiencing significant growth due to several key factors. The increasing prevalence of gastrointestinal diseases and favorable initiatives from governments and healthcare organizations to improve diagnosis and treatment are driving market growth. Furthermore, the funding for research studies and advancements in endoscopic devices contribute to the market's expansion. However, high treatment costs remain a challenge for patients and payers, potentially limiting market growth. Overall, the market is expected to witness steady growth In the coming years, as advancements in technology and increasing awareness of gastrointestinal health drive demand for effective treatment options.

What will be the Size of the Gastrointestinal Bleeding Treatment Market During the Forecast Period?

- The market In the US is experiencing significant growth due to the increasing prevalence of gastrointestinal disorders and an aging population. Flexible endoscopy, a diagnostic and treatment modality, plays a crucial role in addressing acute and chronic cases of gastrointestinal bleeding. Cancer screening and surveillance programs have become essential in early detection and treatment of tumors In the esophagus, stomach, small intestine, colon, and other digestive organs. Healthcare workers in healthcare facilities are employing advanced treatment programs to diagnose and perform endoscopic hemostasis for various causes, including gastric cancers, tumors, and chronic diseases such as diverticulosis, gastritis, peptic ulcers, and inflammatory bowel disease.

- The geriatric population, with a higher risk of gastrointestinal disorders and comorbidities, is a significant market driver. Anticoagulant prescriptions also contribute to the market growth due to the increased risk of gastrointestinal bleeding in patients taking these medications.

How is this Gastrointestinal Bleeding Treatment Industry segmented and which is the largest segment?

The gastrointestinal bleeding treatment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

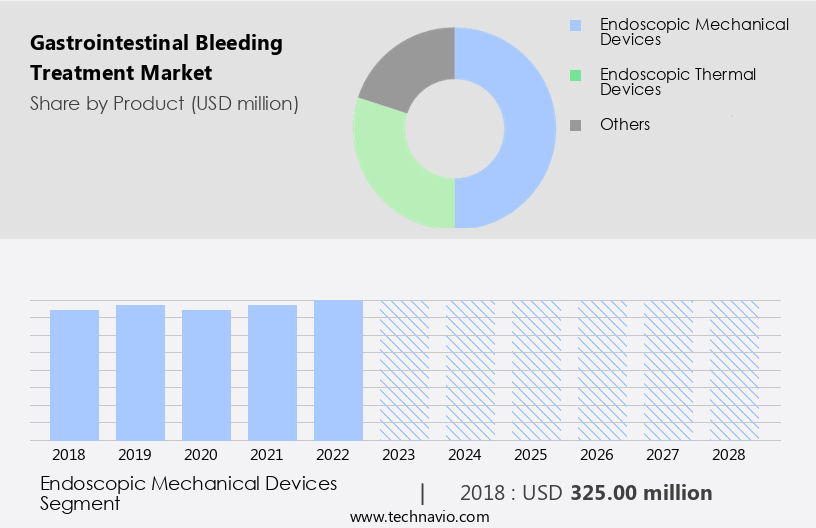

- Endoscopic mechanical devices

- Endoscopic thermal devices

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

By Product Insights

- The endoscopic mechanical devices segment is estimated to witness significant growth during the forecast period.

The market is primarily driven by the increasing use of endoscopic mechanical devices for treating bleeding In the upper GI tract. These devices are preferred due to the rise in minimally invasive surgeries and their application in various endoscopic procedures for non-hemostatic purposes, such as closure In the GI tract, post-operative anastomotic leakage prevention, and fixing of stents. Endoscopic mechanical devices are effective in achieving hemostasis in small mucosal or submucosal defects In the upper GI tract, bleeding ulcers with arteries less than 2 mm, and polyps less than 1 cm. The geriatric population, with a higher prevalence of chronic diseases like gastric cancers and tumors, contributes significantly to the market growth.

Gastroenterologists are the primary users of these devices, and companies like Fujifilm Healthcare are at the forefront of providing advanced endoscopic solutions. The skilled labor required for operating these devices ensures a steady demand for them In the healthcare industry.

Get a glance at the Gastrointestinal Bleeding Treatment Industry report of share of various segments Request Free Sample

The Endoscopic mechanical devices segment was valued at USD 325.00 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

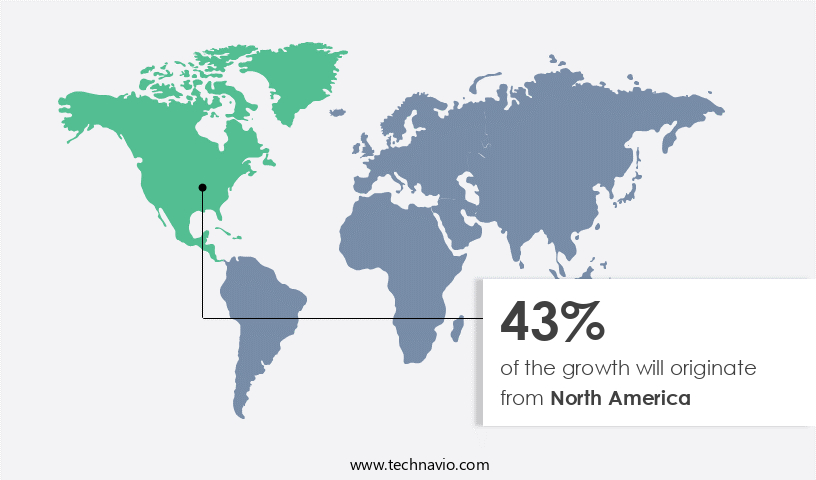

- North America is estimated to contribute 43% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market is projected to expand at a moderate pace over the forecast period. Factors fueling market growth include the increasing adoption of advanced technologies for GI bleeding treatment, a rising prevalence and incidence of GI diseases, a growing geriatric population, and availability of reimbursement policies for endoscopic procedures. Additionally, heightened awareness among patients regarding various diseases and the importance of preventive healthcare contributes to market expansion. Technological advancements, such as AI and clinical trials, are transforming the diagnosis and treatment of conditions like rectal cancer, colon cancer, esophageal diseases, stomach ulcers, small intestine disorders, and colorectal polyps.

Market Dynamics

Our gastrointestinal bleeding treatment market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Gastrointestinal Bleeding Treatment Industry?

Favorable initiatives and increasing prevalence of gastrointestinal diseases is the key driver of the market.

- The market In the US is experiencing significant growth due to the rising prevalence of gastrointestinal disorders, including esophageal, gastric, and colorectal cancers, peptic ulcers, and inflammatory bowel diseases. According to the American Cancer Society, an estimated 149,500 new cases of colorectal cancer were diagnosed in 2020. The aging population, with its increased susceptibility to chronic diseases such as diverticulosis, gastritis, and gastroesophageal reflux disease (GERD), is a significant contributor to this trend. Healthcare facilities and workers are increasingly focusing on early diagnosis and treatment procedures, such as flexible endoscopy and endoscopic hemostasis, to prevent complications and improve patient outcomes.

- Fujifilm Healthcare, Ambu, and other medical technology companies are investing in sophisticated imaging and AI technologies to enhance diagnostic techniques and improve patient safety. The OECD reports that healthcare spending on chronic diseases accounts for over 70% of total healthcare expenditures, making it a priority area for innovation and investment. Lifestyle factors, such as smoking and binge drinking, also play a role In the development of gastrointestinal disorders and the need for treatment. Regulatory support and clinical trials are ongoing to develop innovative treatments and improve patient care. The gastrointestinal anatomy, from the esophagus to the small intestine and colon, requires specialized expertise and skilled labor, making it a complex and evolving field in healthcare.

What are the market trends shaping the Gastrointestinal Bleeding Treatment Industry?

Funding for GI research studies and endoscopic devices is the upcoming market trend.

- The market is witnessing significant investment from healthcare facilities and workers to advance diagnostic techniques and treatment programs for various gastrointestinal disorders. For instance, the American College of Gastroenterology (ACG) has been funding clinical research in gastroenterology through grants and awards. In 2019, they allocated USD1,007,420 for innovative patient-oriented research, leading to new diagnostic and therapeutic interventions. This includes research on gastrointestinal cancers, tumors, ulcers, and chronic diseases In the geriatric population. Medical technology companies, such as Fujifilm Healthcare, are developing sophisticated imaging and endoscopic hemostasis devices to enhance diagnosis and treatment procedures for gastrointestinal bleeding. These advanced tools aid In the detection and removal of polyps, ulcers, and tumors In the digestive organs, including the esophagus, stomach, small intestine, colon, and rectum.

- Prevention and surveillance programs are essential in managing gastrointestinal disorders, especially for chronic cases. Lifestyle factors, such as smoking and binge drinking, contribute to an increased risk of gastrointestinal anatomy disorders. Healthcare organizations, like the Cancer Society, are promoting screening programs for colon, rectal, and colorectal cancer. Gastroenterologists and skilled labor are in high demand due to the increasing number of acute and chronic gastrointestinal cases. The OECD reports that the aging population is a significant contributor to the rising healthcare spending on gastrointestinal disorders. Comorbidities, such as anticoagulant prescriptions, further complicate the treatment process. AI and capsule endoscopy are emerging technologies that offer innovative treatment solutions for gastrointestinal disorders.

- Clinical trials are underway to evaluate their effectiveness in diagnosing and treating various gastrointestinal conditions, such as diverticulosis, gastritis, and inflammatory bowel disease. Regulatory support and patient safety are crucial in ensuring the success of gastrointestinal bleeding treatment programs. The focus on patient safety and advanced diagnostic techniques will continue to drive market growth in this sector.

What challenges does the Gastrointestinal Bleeding Treatment Industry face during its growth?

High treatment costs is a key challenge affecting the industry growth.

- The market is experiencing growth due to the increasing prevalence of gastrointestinal disorders, such as ulcers, tumors, diverticulosis, and inflammatory bowel disease, particularly In the geriatric population and those with chronic diseases like gastritis and peptic ulcers caused by Helicobacter pylori infection. Cancer screening and surveillance programs for esophageal, gastric, colon, and rectal cancers are also driving market growth. Flexible endoscopy, a crucial diagnostic technique, enables effective diagnosis and treatment procedures for gastrointestinal bleeding. However, high costs associated with these devices, healthcare facilities, and skilled labor pose challenges, especially in developing and emerging economies. Endoscopic hemostasis, a sophisticated imaging technology, and capsule endoscopy are innovative treatment options.

- Healthcare workers and institutions must navigate complex budget allocation procedures and equipment maintenance considerations when procuring these devices. Lifestyle factors like smoking and binge drinking contribute to gastrointestinal disorders, further increasing the market demand. Regulatory support and patient safety concerns are essential considerations In the market.

Exclusive Customer Landscape

The gastrointestinal bleeding treatment market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gastrointestinal bleeding treatment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, gastrointestinal bleeding treatment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Boston Scientific Corp. - The company provides a comprehensive solution for gastrointestinal bleeding treatment In the US market. Our offerings encompass advanced technologies and devices such as polypectomy tools, retrieval devices, band ligators, clips, endoluminal surgery devices, enteral access and feeding tubes, fiducial markers, forceps, and guidewires. These solutions enable healthcare professionals to effectively diagnose and treat various causes of gastrointestinal bleeding, ensuring optimal patient outcomes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Boston Scientific Corp.

- Conmed Corp.

- Cook Group Inc.

- EndoClot Plus Inc.

- Erbe Elektromedizin GmbH

- Mayo Foundation for Medical Education and Research

- Medtronic Plc

- Olympus Corp.

- Ovesco Endoscopy AG

- STERIS plc

- University Hospitals

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market: A Comprehensive Overview The gastrointestinal (GI) bleeding treatment market encompasses various diagnostic and therapeutic interventions aimed at managing bleeding In the digestive organs. This market caters to healthcare facilities and gastroenterologists, who are at the forefront of providing care for patients suffering from acute and chronic GI bleeding. Flexible endoscopy plays a pivotal role In the diagnosis and treatment of GI bleeding. This minimally invasive procedure allows healthcare workers to examine the GI tract, identify the source of bleeding, and perform endoscopic hemostasis. The geriatric population is a significant focus in this market due to the increased prevalence of gastrointestinal disorders, such as gastric cancers, tumors, and ulcers, in this demographic.

The GI tract, comprised of the esophagus, stomach, small intestine, and colon, is susceptible to various conditions that may result in bleeding. These include peptic ulcers, pylori infection, diverticulosis, gastritis, and inflammatory bowel disease. Chronic diseases, such as chronic liver disease and anticoagulant prescriptions, can also increase the risk of GI bleeding. Prevention plays a crucial role in managing GI bleeding. Screening programs for cancer, such as colon cancer, rectal cancer, and colorectal cancer, are essential in early detection and treatment. Lifestyle factors, including smoking and binge drinking, can contribute to the development of GI disorders and should be addressed through public health initiatives.

The healthcare spending on GI bleeding treatment is influenced by various factors, including the increasing aging population, regulatory support, and innovative treatment options. Medical technology advancements, such as capsule endoscopy and sophisticated imaging, have improved diagnostic techniques and patient safety. The GI bleeding treatment market is characterized by a growing demand for skilled labor and specialized equipment. Companies, such as Fujifilm Healthcare, are investing in research and development to address this need. The market is also witnessing an increasing focus on AI and clinical trials to improve treatment outcomes and patient care. In conclusion, the GI bleeding treatment market is a dynamic and evolving landscape that caters to the diagnosis, treatment, and prevention of bleeding In the digestive organs.

The market is influenced by various factors, including demographic trends, lifestyle factors, healthcare spending, and medical technology advancements. Gastroenterologists and healthcare facilities play a vital role in providing care for patients with acute and chronic GI bleeding, ensuring optimal patient outcomes.

|

Gastrointestinal Bleeding Treatment Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

134 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.5% |

|

Market growth 2024-2028 |

USD 182.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.23 |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Gastrointestinal Bleeding Treatment Market Research and Growth Report?

- CAGR of the Gastrointestinal Bleeding Treatment industry during the forecast period

- Detailed information on factors that will drive the Gastrointestinal Bleeding Treatment growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the gastrointestinal bleeding treatment market growth of industry companies

We can help! Our analysts can customize this gastrointestinal bleeding treatment market research report to meet your requirements.

RIA -

RIA -