Germany Pharmaceuticals Market Size 2024-2028

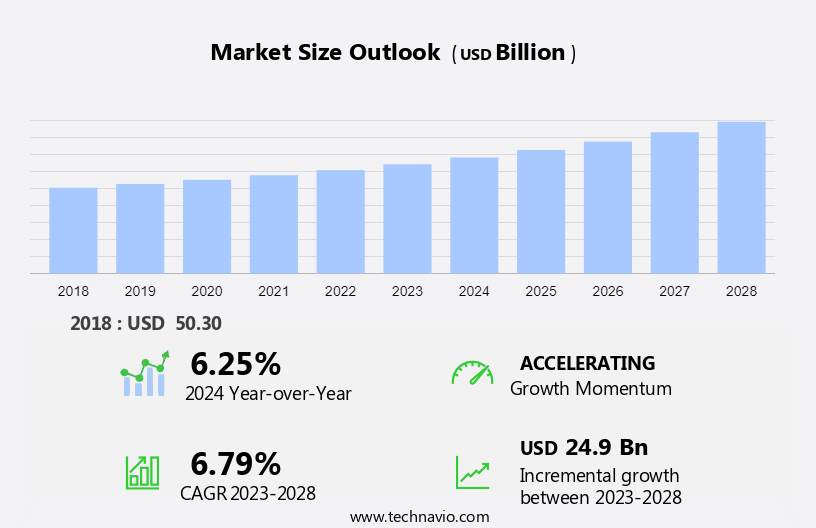

The Germany pharmaceuticals market size is forecast to increase by USD 24.9 billion at a CAGR of 6.79% between 2023 and 2028.

- The market exhibits strong growth due to significant investments in the industry and the burgeoning expansion of e-commerce. These factors contribute to the market's upward trajectory. Additionally, pricing and reimbursement policies play a crucial role in market growth. Germany's commitment to research and development, coupled with its advanced healthcare system, positions it as a key player in the global pharmaceutical industry. Simultaneously, the market's future looks promising, with continued investment in innovative technologies and a focus on patient-centric care. Overall, these trends present both opportunities and challenges for market participants, requiring strategic planning and adaptability to remain competitive.

What will be the size of the market during the forecast period?

- The market plays a significant role in the healthcare sector, providing essential drugs for medical and healthcare purposes. This market encompasses various types of pharmaceutical drugs, including biologics, vaccines, and traditional medicines. The demand for these drugs continues to grow due to the increasing prevalence of common diseases and the aging population's longer lifespans. Vaccines have gained prominence in recent times, particularly in the context of viruses. Pharmaceutical companies are investing heavily in research and development to create effective vaccines for various viruses. These vaccines are crucial in preventing the spread of diseases and ensuring public health. The market caters to diverse segments, such as hospital pharmacies, drug stores, and online pharmacies. In addition, if pharmaceutical companies are anticipating difficulties in pricing negotiations, which could prevent patients from benefiting from the potentially life-saving treatment of chronic diseases like cancer and cardiovascular disease, they may be reluctant to make their products available on Germany's market.

- Simultaneously, skilled workers with specialized skills are in high demand to manage the complexities of this industry. The benefits of pharmaceutical drugs extend beyond individuals, positively impacting society as a whole. Patients' characteristics, including genetic composition, influence the need for precision treatments. The market is dynamic, with constant advancements in technology and research leading to new treatments and therapies. The market's growth is driven by the increasing demand for healthcare services and the aging population's growing needs.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

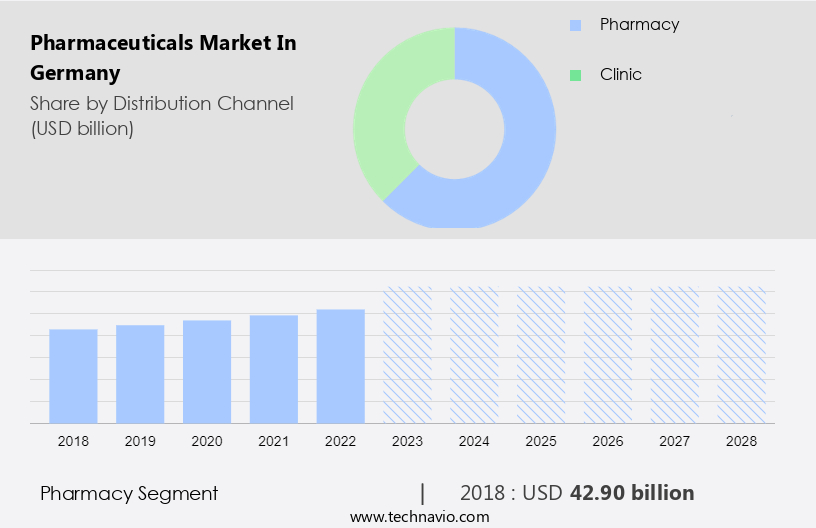

- Distribution Channel

- Pharmacy

- Clinic

- Type

- Prescription

- Non-prescription

- Geography

- Germany

By Distribution Channel Insights

- The pharmacy segment is estimated to witness significant growth during the forecast period.

The German pharmaceuticals market is dominated by the pharmacy segment, which held the largest market share in 2023. In Germany, pharmacies serve as the primary distribution channels for both prescription and over-the-counter medications. Under the Pharmacy Monopoly system, only licensed pharmacies are authorized to sell these drugs, ensuring their quality, safety, and availability to the public. Pharmacies in Germany are typically owned and operated by licensed pharmacists and include various types such as public, hospital, and mail-order pharmacies. Beyond dispensing medications, these establishments offer services like prescription counseling, patient consultations, medication management, and health-related advice.

Get a glance at the market share of various segments Request Free Sample

The pharmacy segment was valued at USD 42.90 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Germany pharmaceuticals Market?

High investment in the pharmaceutical industry is the key driver of the market.

- The market is a significant contributor to the global healthcare sector, driven by the country's advanced healthcare system, skilled workforce, and specialized skills in areas such as biopharmaceuticals and nanotechnology. Germany is home to numerous research organizations and medical equipment manufacturers, making it an attractive destination for pharmaceutical companies seeking innovation and new treatments for age-related disorders, viruses, and other diseases. In recent years, there has been a growing focus on personalized medicine and precision treatments, which require a deep understanding of patient characteristics and genetic composition.

- Simultaneously, this trend is reflected in investments by major pharmaceutical companies, such as Bayer's USD 1.6 billion investment in digitalization and new production facilities. The benefits of these investments extend beyond individuals, as they contribute to the development of new treatments and longer lifespans, ultimately improving societal health and reducing the strain on global healthcare systems. The market is poised for continued growth, with a focus on meeting unmet medical needs and addressing common diseases through the application of artificial intelligence, process modelling, and automation within the pharma workforce.

What are the market trends shaping the Germany Pharmaceuticals Market?

Strong growth of e-commerce is the upcoming trend in the market.

- The market has witnessed significant transformation due to the emergence of e-commerce platforms. Consumers now have the convenience of accessing a wide array of pharmaceutical drugs and healthcare products online, including vaccines and biologics, from the comfort of their homes. Online pharmacies, such as PharmEasy, have expanded their offerings beyond traditional drugstores, providing consumers with access to various medications, supplements, personal care products, and health-related items from manufacturers and brands. E-commerce enables consumers to compare prices and facilitates price transparency, leading to increased competition and potential cost savings. In comparison to conventional brick-and-mortar pharmacies, e-pharmacies like Pharm Easy offer a wider range of products.

- Simultaneously, the benefits of e-commerce extend beyond individuals, as it also contributes to the broader healthcare system by increasing access to medical purposes and healthcare purposes drugs for society. The aging population in Germany places a strain on global healthcare systems, necessitating innovation in the market. New treatments and research in areas such as nanotechnology, artificial intelligence, and process modelling are addressing unmet medical needs and tailor-made medicines, including precision and personalized treatments based on patient's characteristics and genetic composition. The pharma workforce is adapting to automation and computer science to meet the demands of this innovative market. The raw materials and biopharma production sectors are also evolving to meet the needs of this dynamic market.

What challenges does Germany Pharmaceuticals Market face during the growth?

Pricing and Reimbursement is a key challenge affecting the market growth.

- The market encompasses the production, distribution, and sale of Pharmaceutical Drugs and Biologics for medical and healthcare purposes. This market includes Hospital Pharmacies, Drugs Stores, and Online Pharmacies. The market in Germany is driven by the increasing demand for vaccines to combat viruses and age-related disorders. The benefits of Pharmaceuticals extend to individuals and society by addressing unmet medical needs and providing new treatments for diseases. Pharmaceutical companies face challenges in the German market due to the complex pricing and reimbursement system. The added therapeutic value of new treatments must be demonstrated to negotiate prices with statutory health insurance funds.

- This system can discourage companies from introducing their products in Germany, potentially limiting patient access to life-saving treatments for diseases such as cancer and heart disease. Lower prices for products may also discourage investment in research and development activities within the country. The market is influenced by the aging population, which strains global healthcare systems and increases the demand for drugs and medical equipment. The market is also impacted by Pharma innovation, including nanotechnology, artificial intelligence, and process modelling, which enable tailor-made medicines and personalized treatments based on patient characteristics and genetic composition. The Pharma workforce requires specialized skills to meet the demands of this evolving market. The market dynamics are further shaped by the raw materials used in Biopharma production and the role of research organizations in driving innovation.

Exclusive Germany Pharmaceuticals Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AbbVie Inc.

- Amgen Inc.

- AstraZeneca Plc

- Bayer AG

- Boehringer Ingelheim International GmbH

- Bristol Myers Squibb Co.

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- Fresenius SE and Co. KGaA

- GlaxoSmithKline Plc

- Johnson and Johnson Services Inc.

- MCM Klosterfrau Vertriebsgesellschaft mbH

- Merck KGaA

- Novartis AG

- Novo Nordisk AS

- Pfizer Inc.

- Sanofi SA

- STADA Arzneimittel AG

- Teva Pharmaceutical Industries Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is a significant contributor to the global healthcare sector, with a strong presence in the production and distribution of various pharmaceutical drugs. This market caters to individuals and society at large, addressing medical and healthcare purposes through various channels such as hospital pharmacies, drug stores, and online pharmacies. The market encompasses a diverse range of offerings, including pharmaceutical drugs, biologics, and vaccines. These solutions serve various purposes, from addressing acute and chronic conditions to preventing the spread of viruses and other diseases. The pharmaceutical industry in Germany is marked by innovation, with a focus on addressing unmet medical needs and developing new treatments for common age-related disorders. The pharmaceutical landscape in Germany is shaped by several factors. The aging population, with its increased demand for healthcare solutions, is a significant driver. The German healthcare system, known for its high standards, places a high value on the latest treatments and technologies. This creates a large patient pool, driving the demand for pharmaceuticals. The pharmaceutical industry in Germany is undergoing significant changes, with a growing emphasis on automation, computer science, and process modeling. These advancements aim to increase efficiency and productivity while reducing costs.

In summary, the industry also places a premium on specialized skills and the workforce, recognizing the importance of skilled workers in the production of complex pharmaceuticals and biologics. The market in Germany is another area of growth, driven by the increasing demand for personalized and precision medicines. These tailor-made solutions are designed to address the unique characteristics of individual patients, including their genetic composition and precision treatments for common diseases. The market is also influenced by the strain on healthcare systems worldwide. The need for affordable and effective treatments, coupled with the high cost of research and development, creates a complex market landscape. The market is strained due to the ongoing virus outbreaks and the unmet medical needs of various lung diseases.

However, the potential benefits of pharmaceuticals, from longer lifespans to improved quality of life, make the investment worthwhile. The pharmaceutical industry in Germany is at the forefront of innovation, with research organizations and medical equipment companies collaborating to develop new treatments and technologies. These advancements include the use of nanotechnology and artificial intelligence in drug development and production. In conclusion, the market is a dynamic and evolving landscape, shaped by various factors such as demographic trends, technological advancements, and the global healthcare system. The industry's focus on innovation, efficiency, and patient-centric solutions will continue to drive growth and shape the future of healthcare.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

130 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.79% |

|

Market growth 2024-2028 |

USD 24.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.25 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Germany

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -