Green Logistics Certification Services Market Size 2026-2030

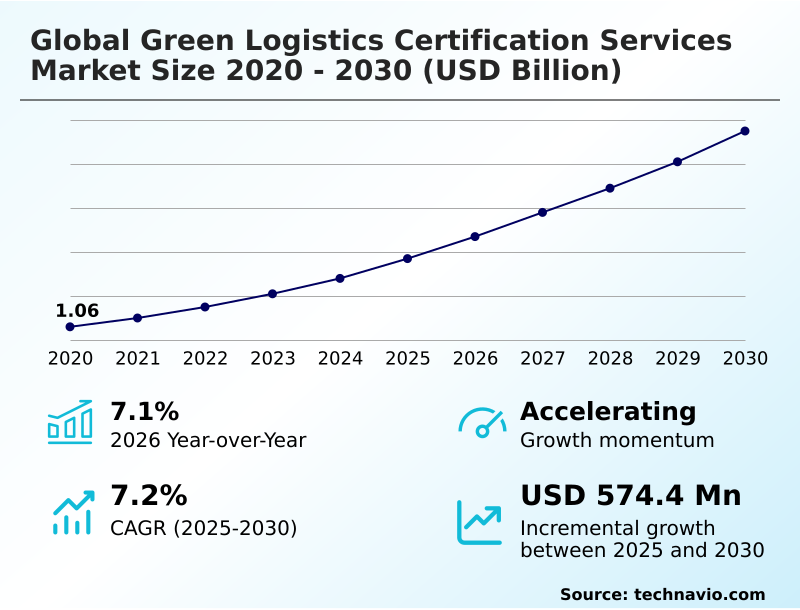

The green logistics certification services market size is valued to increase by USD 574.4 million, at a CAGR of 7.2% from 2025 to 2030. Escalating regulatory pressures and global decarbonization mandates will drive the green logistics certification services market.

Major Market Trends & Insights

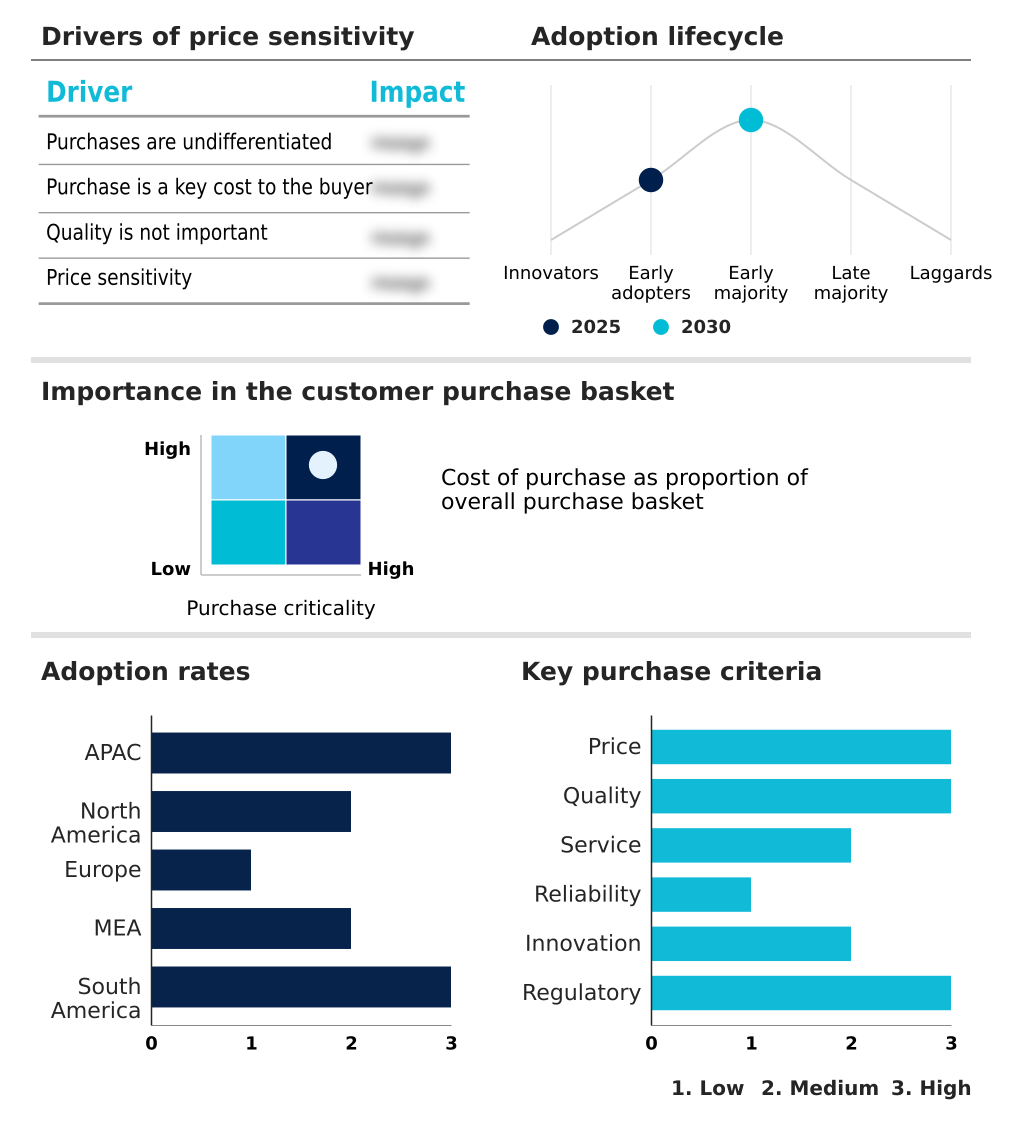

- APAC dominated the market and accounted for a 37.9% growth during the forecast period.

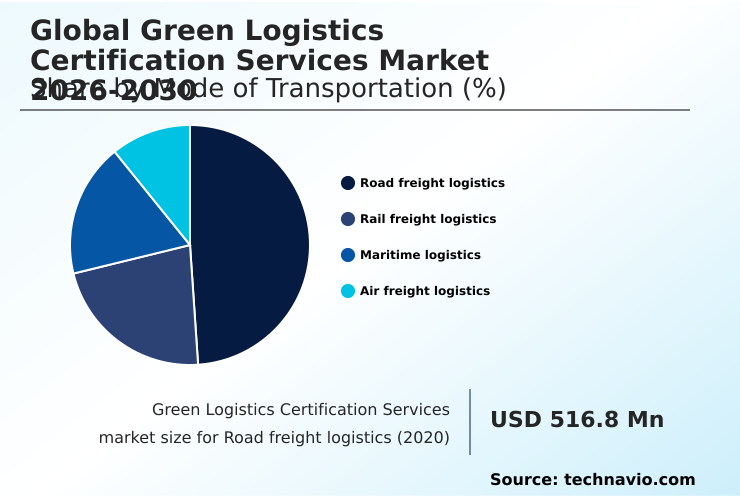

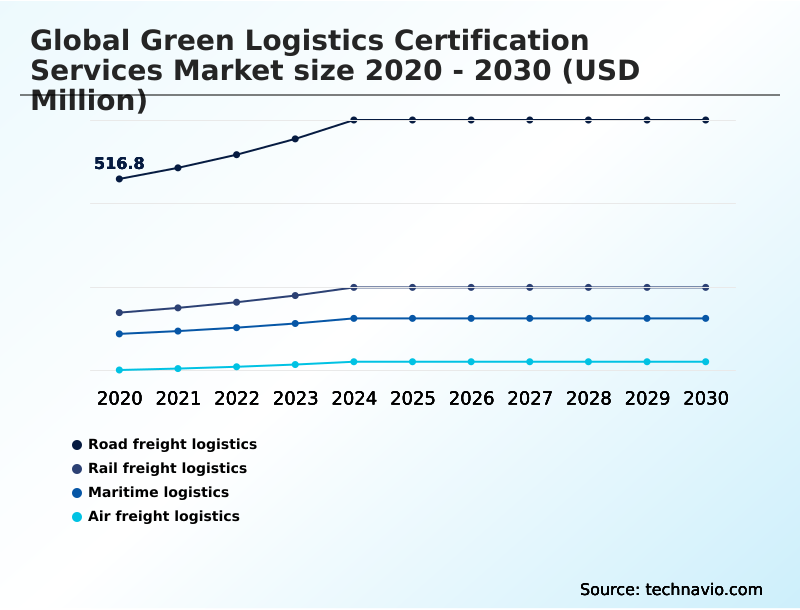

- By Mode of Transportation - Road freight logistics segment was valued at USD 641 million in 2024

- By End-user - Logistics service providers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 891.8 million

- Market Future Opportunities: USD 574.4 million

- CAGR from 2025 to 2030 : 7.2%

Market Summary

- The Green Logistics Certification Services Market is undergoing a significant transformation, propelled by a convergence of stringent regulatory mandates and corporate ESG strategies. Escalating pressures for transparency in scope 3 emissions reporting are compelling organizations to move beyond self-assessment toward independent, third-party validation of their environmental performance.

- This shift is creating a critical need for services that can provide credible carbon footprint verification and ensure compliance with frameworks like the logistics emissions council (GLEC) framework. Key trends include the integration of technology for predictive compliance monitoring and the expansion of certification to cover circular economy principles and reverse logistics capabilities.

- For example, a multinational retailer seeking to offer carbon neutral labeling on its products must ensure its entire supply chain, including last-mile delivery emissions, is certified. This involves a comprehensive green logistics audit of its partners, verifying everything from fleet emissions validation to warehouse sustainability assessment.

- However, the market's progress is moderated by the fragmentation of standards and the high implementation costs, which pose significant barriers for smaller logistics operators. This dynamic creates a landscape where certification is both a prerequisite for market access and a catalyst for operational efficiency.

What will be the Size of the Green Logistics Certification Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Green Logistics Certification Services Market Segmented?

The green logistics certification services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Mode of transportation

- Road freight logistics

- Rail freight logistics

- Maritime logistics

- Air freight logistics

- End-user

- Logistics service providers

- Retail and e-commerce companies

- Manufacturers and exporters

- Service type

- Carbon footprint certification

- Energy efficiency certification

- Sustainable supply chain certification

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Mode of Transportation Insights

The road freight logistics segment is estimated to witness significant growth during the forecast period.

The road freight logistics segment is central to the certification market, driven by intense scrutiny of greenhouse gas emissions.

Logistics operators seek third-party decarbonization verification to comply with evolving standards, such as those outlined in the freight decarbonization directive, and to provide sustainable supply chain assurance to clients.

The focus is on validating road freight logistics emissions through precise GHG emissions calculation and transparent reporting of environmental performance data.

Certification services assess a range of initiatives, from fleet emissions validation to the efficacy of eco-driving program validation, which has shown to improve fuel efficiency.

Frameworks like the smartway transport partnership are pivotal, offering scalable solutions for carbon footprint calculation that enable both large and small carriers to benchmark performance.

The Road freight logistics segment was valued at USD 641 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 37.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Green Logistics Certification Services Market Demand is Rising in APAC Request Free Sample

The geographic landscape is led by the APAC region, which is set to account for over 37% of the market's incremental growth, driven by its role as a global manufacturing hub. In this region, maritime and aviation certifications are critical.

Compliance with the carbon intensity indicator (CII) and energy efficiency existing ship index (EEXI) is essential for market access. Green shipping corridor standards are also promoting alternative marine fuels certification.

Similarly, demand for verifying sustainable aviation fuel (SAF) usage through book-and-claim systems is rising. In contrast, Europe's mature market focuses on rail freight decarbonization and stringent port emissions certification.

Across all regions, the demand for services like carbon neutral labeling and verification for emerging areas like green hydrogen logistics is growing, reflecting a global trend toward specialized, verifiable sustainability claims.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The demand for specialized verification services highlights the market's increasing maturity and complexity. Companies are moving beyond broad environmental statements to seek validation for highly specific operational activities. This includes services for verifying sustainable aviation fuel book-and-claim systems and auditing carbon intensity indicator compliance for maritime fleets.

- The focus on the complete product journey is evident in the need for certifying circular economy reverse logistics and meticulously assessing scope 3 supply chain emissions. For logistics providers, obtaining an ISO 14001 certification for freight forwarders has become a competitive necessity, with adoption rates in this segment being nearly double that of smaller, regional carriers.

- In infrastructure, securing a LEED certification for distribution centers is now a standard expectation for institutional investors. As consumer-facing pressures mount, there is a growing need for validating carbon neutrality for e-commerce delivery and obtaining certification for low-emission urban logistics zones.

- The market is also addressing future-facing and niche requirements, such as establishing green hydrogen transport safety certification protocols and conducting energy efficiency audits for cold chain logistics. Cross-border trade complexities are driving demand for services ensuring compliance with carbon border taxes. Specialized commodity chains require services like sustainable palm oil logistics certification.

- Technologically, the industry is leveraging blockchain for supply chain data integrity and AI for predictive emissions monitoring while also focusing on asset-specific needs like verifying emissions for dual-fuel vessels.

What are the key market drivers leading to the rise in the adoption of Green Logistics Certification Services Industry?

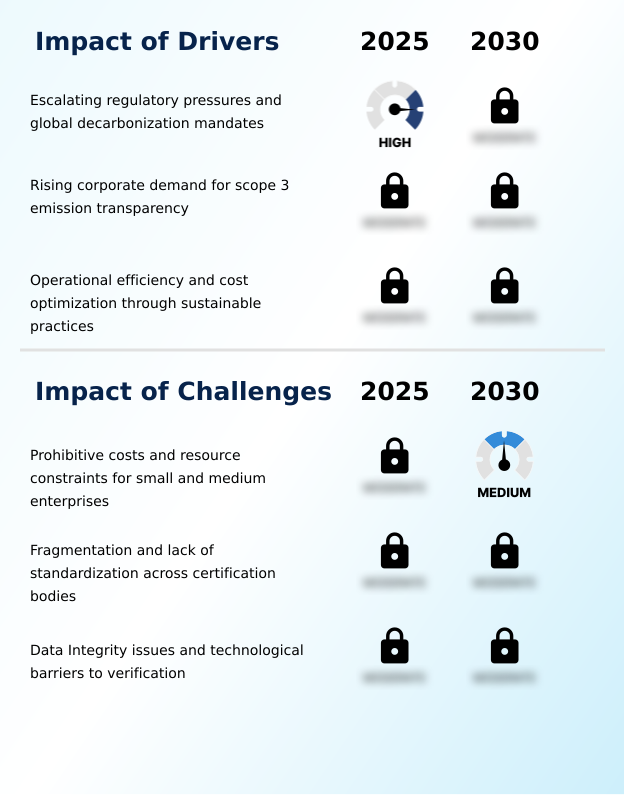

- Market growth is primarily driven by escalating regulatory pressures for mandatory reporting and global corporate mandates for decarbonizing entire supply chains.

- Intensifying regulatory frameworks are a primary market driver, with mandates like the corporate sustainability reporting directive (CSRD) compelling organizations to seek independent validation.

- This creates strong demand for sustainable transport certification to ensure compliance and avoid penalties under schemes like the carbon border adjustment mechanism (CBAM).

- The corporate focus on scope 3 emissions reporting is another significant factor, as companies now require their logistics partners to provide auditable carbon footprint verification. Utilizing the logistics emissions council (GLEC) framework has become a standard for this process.

- This pressure for supply chain traceability extends to sustainable packaging verification and carbon offset validation services, with certified providers gaining preferential status in procurement processes, often securing contracts over non-certified competitors.

What are the market trends shaping the Green Logistics Certification Services Industry?

- The market is fundamentally shifting toward integrating blockchain technology to ensure data integrity. This move addresses the risk of greenwashing by creating an immutable and transparent record of carbon data across the supply chain.

- Market trends are shifting from reactive audits to proactive validation through technology. The integration of blockchain is delivering immutable carbon transparency, which improves the accuracy of supply chain carbon accounting by over 25%. Concurrently, predictive compliance monitoring powered by AI is reducing compliance breaches by up to 30%, transforming the traditional green logistics audit.

- There is also an expanding focus on circular economy principles, where certification now includes a comprehensive lifecycle assessment of reverse logistics capabilities. This circular logistics verification is critical for managing last-mile delivery emissions and improving overall logistics ESG metrics, as companies adopting these models have demonstrated significant reductions in packaging waste.

What challenges does the Green Logistics Certification Services Industry face during its growth?

- Prohibitive costs and significant resource constraints for small and medium-sized enterprises represent a key challenge affecting widespread industry adoption and growth.

- Significant challenges persist, particularly the high cost of compliance for smaller operators, which can increase operational overhead by 15-20%. Pursuing green building certifications (LEED/BREEAM) or implementing ISO 50001 energy management systems requires substantial capital investment. This is also true for conducting a warehouse sustainability assessment against sustainable warehousing standards.

- Furthermore, the fragmentation of standards complicates validation; a logistics provider may need separate ISO 14001 environmental management certification and ISO 14064 greenhouse gas verification for different regions. This complexity is amplified in specialized areas like cold chain sustainability audit and biofuel usage verification, where data integrity for energy efficiency auditing across different modes hinders improvements in intermodal transport efficiency.

Exclusive Technavio Analysis on Customer Landscape

The green logistics certification services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the green logistics certification services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Green Logistics Certification Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, green logistics certification services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABS Group of Companies Inc. - Provides maritime decarbonization auditing and sustainable shipping performance verification, addressing key risks for entities engaged in global logistics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABS Group of Companies Inc.

- BRE Group

- British Standards Institution

- Bureau Veritas

- Clearyst GBB LLC

- Control union

- Cotecna Inspection SA

- DEKRA SE

- DHL International GmbH

- DNV Group AS

- EcoVadis

- Intertek Group Plc

- Jones Lang LaSalle Inc.

- LRQA Group Ltd.

- Peterson

- SGS SA

- The Carbon Trust

- Toitu Envirocare

- TUV Rheinland Group

- TUV SUD AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Green logistics certification services market

- In May, 2025, DNV launched a strategic initiative to integrate AI-driven remote auditing tools for maritime logistics certifications, aiming to enhance the credibility of continuous performance claims.

- In April, 2025, the International Standards Organization released updated guidance specifically for circular logistics flows, prompting increased demand for certifications validating reverse logistics and material recovery systems.

- In March, 2025, a coalition of major international e-commerce platforms announced a joint requirement that all last-mile logistics partners must achieve a specified tier of green certification to maintain their status on preferred company lists.

- In February, 2025, the Global Maritime Decarbonization Alliance introduced a unified certification standard for dual-fuel vessels on Trans-Pacific routes, seeking to harmonize various regional eco-labels into a single framework.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Green Logistics Certification Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.2% |

| Market growth 2026-2030 | USD 574.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.1% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, The Netherlands, Italy, Spain, Saudi Arabia, UAE, South Africa, Turkey, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is evolving into an essential component of corporate risk management and strategic planning. Boardroom decisions on capital allocation are increasingly influenced by the need for credible decarbonization verification to mitigate risks associated with the carbon border adjustment mechanism (CBAM) and the corporate sustainability reporting directive (CSRD).

- Achieving sustainable supply chain assurance now requires meticulous scope 3 emissions reporting, validated through independent carbon footprint verification. Firms achieving ISO 14001 environmental management certification demonstrate a commitment that resonates with investors. The process involves detailed GHG emissions calculation and energy efficiency auditing, often leading to ISO 50001 energy management adoption.

- For instance, obtaining green building certifications (LEED/BREEAM) has shown to increase asset valuation by up to 10%. Technology is enabling immutable carbon transparency and predictive compliance monitoring, enhancing supply chain traceability and the integrity of environmental performance data. Certification extends to circular economy principles by assessing reverse logistics capabilities via a lifecycle assessment.

- Specific standards like the smartway transport partnership, maritime's carbon intensity indicator (CII) and energy efficiency existing ship index (EEXI), and aviation's use of sustainable aviation fuel (SAF) with book-and-claim systems, are becoming mandatory. This drive for authenticity is also fueling demand for carbon neutral labeling, backed by ISO 14064 greenhouse gas verification.

What are the Key Data Covered in this Green Logistics Certification Services Market Research and Growth Report?

-

What is the expected growth of the Green Logistics Certification Services Market between 2026 and 2030?

-

USD 574.4 million, at a CAGR of 7.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Mode of Transportation (Road freight logistics, Rail freight logistics, Maritime logistics, and Air freight logistics), End-user (Logistics service providers, Retail and e-commerce companies, and Manufacturers and exporters), Service Type (Carbon footprint certification, Energy efficiency certification, and Sustainable supply chain certification) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating regulatory pressures and global decarbonization mandates, Prohibitive costs and resource constraints for small and medium enterprises

-

-

Who are the major players in the Green Logistics Certification Services Market?

-

ABS Group of Companies Inc., BRE Group, British Standards Institution, Bureau Veritas, Clearyst GBB LLC, Control union, Cotecna Inspection SA, DEKRA SE, DHL International GmbH, DNV Group AS, EcoVadis, Intertek Group Plc, Jones Lang LaSalle Inc., LRQA Group Ltd., Peterson, SGS SA, The Carbon Trust, Toitu Envirocare, TUV Rheinland Group and TUV SUD AG

-

Market Research Insights

- The market's dynamism is driven by a comprehensive need for validation across the entire supply chain. A green logistics audit now includes precise supply chain carbon accounting and reporting on logistics ESG metrics. Demand for sustainable transport certification is surging, with a focus on fleet emissions validation and verifying road freight logistics emissions to comply with the freight decarbonization directive.

- The logistics emissions council (GLEC) framework guides carbon footprint calculation. A warehouse sustainability assessment against sustainable warehousing standards has shown to reduce energy costs by over 10%. Verification extends to sustainable packaging verification, last-mile delivery emissions, and circular logistics verification. Specialized audits like a cold chain sustainability audit, biofuel usage verification, and eco-driving program validation are also key.

- In maritime, port emissions certification, alternative marine fuels certification, and adherence to green shipping corridor standards are critical. Meanwhile, sectors are preparing for green hydrogen logistics and rail freight decarbonization, while relying on carbon offset validation services to meet interim goals, improving intermodal transport efficiency.

We can help! Our analysts can customize this green logistics certification services market research report to meet your requirements.

RIA -

RIA -