UK Grocery Retail Market Size 2026-2030

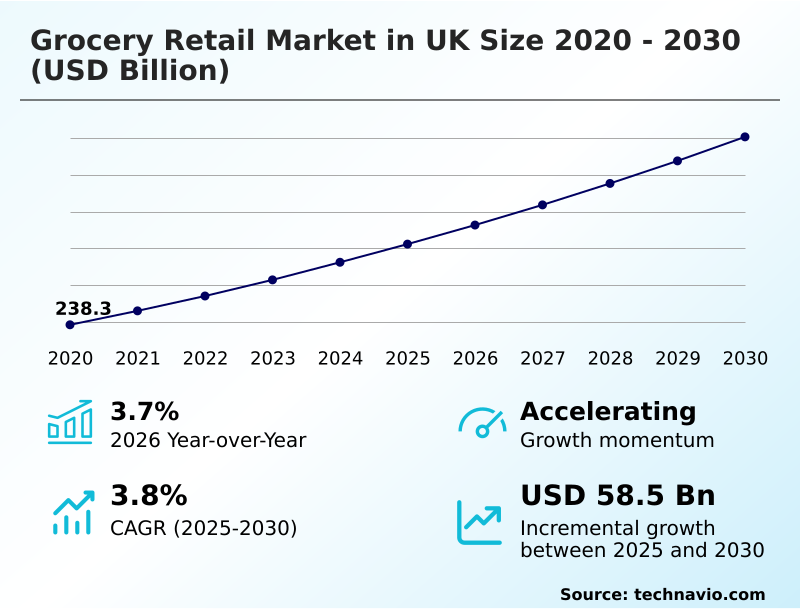

The uk grocery retail market size is valued to increase by USD 58.5 billion, at a CAGR of 3.8% from 2025 to 2030. Rapid urbanization and rising consumer spending will drive the uk grocery retail market.

Major Market Trends & Insights

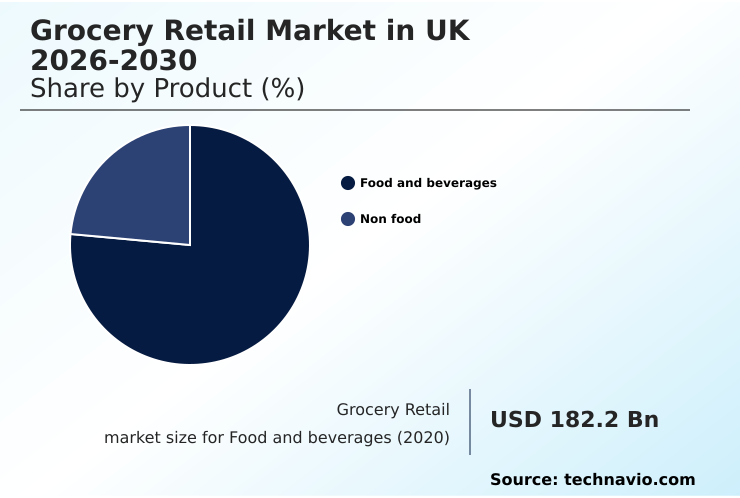

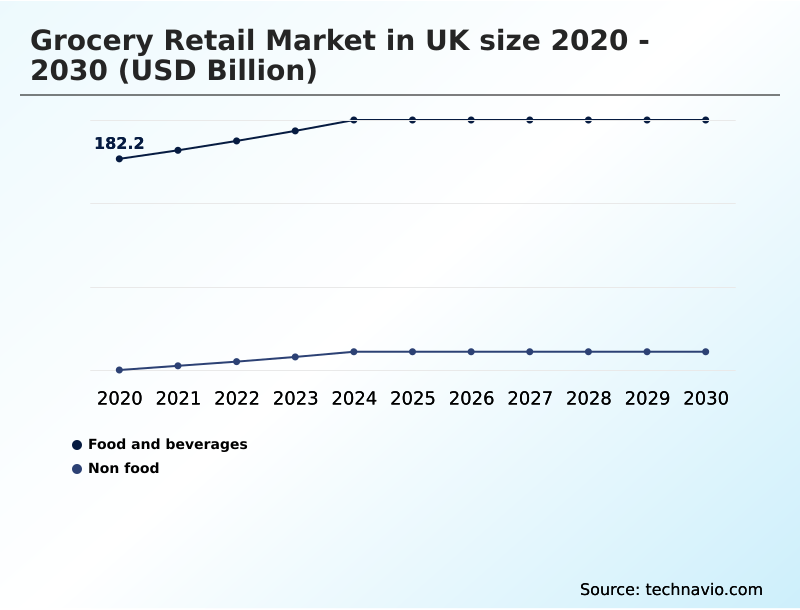

- By Product - Food and beverages segment was valued at USD 205.4 billion in 2024

- By Distribution Channel - Hypermarkets and supermarkets segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 102.5 billion

- Market Future Opportunities: USD 58.5 billion

- CAGR from 2025 to 2030 : 3.8%

Market Summary

- The grocery retail market in UK is navigating a period of profound transformation, driven by shifting consumer lifestyles and technological advancements. Key market dynamics include the rising demand for convenience, leading to the growth of ready-to-eat meal solutions and quick commerce platforms.

- Retailers are competing on more than just price, with an increasing emphasis on customer experience enhancement through innovative store layouts and hyper-personalized marketing. A significant trend is the expansion of private-label product development, as retailers build their own-brand product range to capture value-seeking consumers and improve margins.

- For example, a retailer might leverage an integrated supply chain and AI-driven demand forecasting to optimize stock levels of its premium own-label range, reducing food waste by over 10% while ensuring high availability of popular items. This scenario highlights the operational pivot towards data-driven merchandising and efficiency.

- However, the market faces challenges from supply chain disruption and the need for robust food safety compliance, pushing investments in technologies like blockchain based tracking to ensure supply chain traceability and maintain consumer trust in a competitive landscape. This strategic balancing act defines the current state of the industry.

What will be the Size of the UK Grocery Retail Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the UK Grocery Retail Market Segmented?

The uk grocery retail industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Food and beverages

- Non food

- Distribution channel

- Hypermarkets and supermarkets

- Convenience stores

- Discount stores

- Online

- Others

- End-user

- Household

- Commercial

- Institutional

- Geography

- Europe

- UK

- Europe

By Product Insights

The food and beverages segment is estimated to witness significant growth during the forecast period.

The food and beverages segment is the core of the grocery retail market in UK, shaped by disciplined consumer spending patterns and a focus on health.

Value-seeking consumer behavior continues to influence purchasing, but there is a growing rejection of ultra-processed items.

This shift propels private-label product development, with retailers investing in premium own-label range expansions that cater to at-home dining experiences; some premium lines have seen sales growth of 15%.

Retailers are enhancing fresh produce sourcing and expanding ready-to-eat meal solutions and plant-based food alternatives.

To manage margins, food waste reduction technology and optimized cold chain logistics are critical, balancing cost pressures with the demand for quality in food and beverage retailing. This focus on shopper mission analysis helps tailor offerings for different consumer needs.

The Food and beverages segment was valued at USD 205.4 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The grocery retail market in UK is grappling with several strategic imperatives. A key area is understanding the impact of AI on grocery stock management to mitigate profitability challenges in online grocery retail. This involves leveraging data analytics for grocery merchandising and hyper-personalization in grocery loyalty programs.

- In online operations, the primary focus is on optimizing last-mile logistics for quick commerce and addressing challenges in online grocery fresh produce delivery. The customer perception of online grocery substitutions remains a hurdle, requiring clear communication. The future of dark stores in urban logistics and the role of automation trends in grocery warehouse fulfillment are being actively explored.

- Another critical focus is implementing computer vision for frictionless checkout, which directly addresses the goal of enhancing in-store experience with digital tech.

- In terms of product strategy, comparing discount and traditional supermarket models reveals the power of private labels, leading to a deeper analysis of the role of private labels in customer retention and the consumer demand for plant-based food alternatives.

- On the operational front, strategies for reducing food waste in supermarkets, ensuring supply chain traceability for food safety, and effectively managing product recalls in the food sector are non-negotiable. Finally, ensuring sustainability in grocery retail packaging is becoming a core brand differentiator, with some retailers reporting a 10% higher customer loyalty score when they lead in this area.

What are the key market drivers leading to the rise in the adoption of UK Grocery Retail Industry?

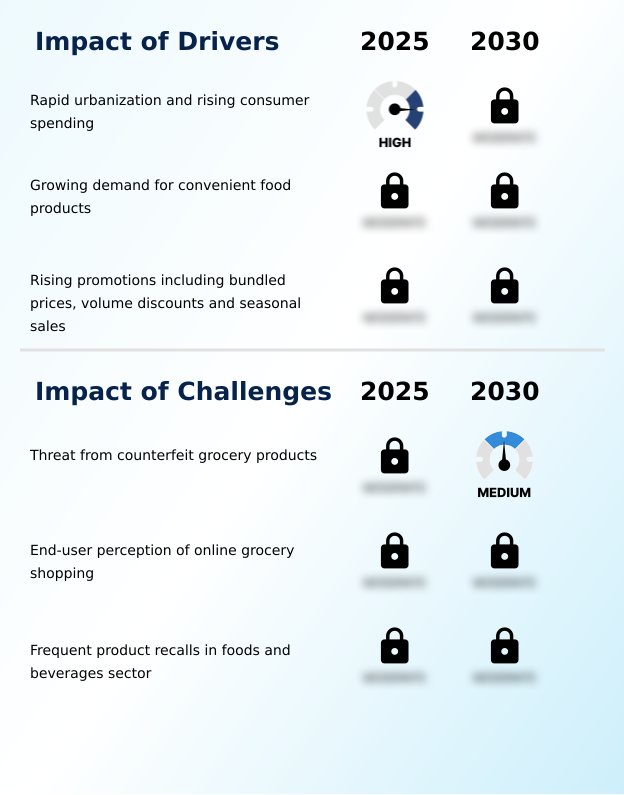

- Rapid urbanization, coupled with rising consumer spending, serves as a key driver for the market.

- Rising urbanization is a primary driver, reshaping the urban retail environment and influencing consumer spending patterns. This has spurred growth in the convenience store format, with households making up to 15% more frequent shopping trips for top-up needs.

- In response, retailers are optimizing discount store operations and hypermarket store layouts to cater to diverse missions. The expansion of the own-brand product range, especially entry-level private label lines, appeals to price-sensitive shoppers.

- AI-driven demand forecasting is crucial for managing inventory across the growing online grocery platform.

- Furthermore, promotional tactics like volume discount mechanics are highly effective, with nearly 30% of grocery purchases now made via deals, which are often communicated through a targeted customer loyalty program.

What are the market trends shaping the UK Grocery Retail Industry?

- Retailers are prioritizing innovative store layouts and enhancing offerings. This strategic shift is designed to amplify the overall customer experience.

- The grocery retail market in UK is defined by an omnichannel retail strategy where digital and physical channels merge. Retailers are adopting experiential retail concepts, including in-store food theatre, to create engaging environments.

- A key trend is the implementation of in-store automation technology, with digital shelf labeling and frictionless checkout systems improving efficiency; some retailers have seen online channels grow 1.9% even as physical store sales flattened. The rise of mobile commerce integration is critical, with scan-and-go mobile applications and quick commerce platform options becoming standard.

- This digital share of retail now approaches 27%. Data-driven merchandising informs promotional pricing strategy and seasonal sales campaign efforts, while the subscription-based model for delivery gains traction, reshaping customer loyalty.

What challenges does the UK Grocery Retail Industry face during its growth?

- The threat posed by counterfeit grocery products is a key challenge that affects the industry's growth.

- Supply chain complexities present significant challenges, with last-mile delivery optimization being a primary focus as fulfillment can account for up to 18% of an online order's total cost. Persistent supply chain disruption requires robust supplier relationship management.

- A major operational challenge is product recall management, which has seen administrative costs increase by over 25% due to complexities in tracking affected batches. To mitigate risks and ensure food safety compliance, firms are investing in advanced food traceability systems, including blockchain based tracking for immutable records. The threat of fakes necessitates better counterfeit product detection and tamper evident packaging.

- These issues can negatively impact basket size analysis metrics and erode consumer trust if not managed effectively.

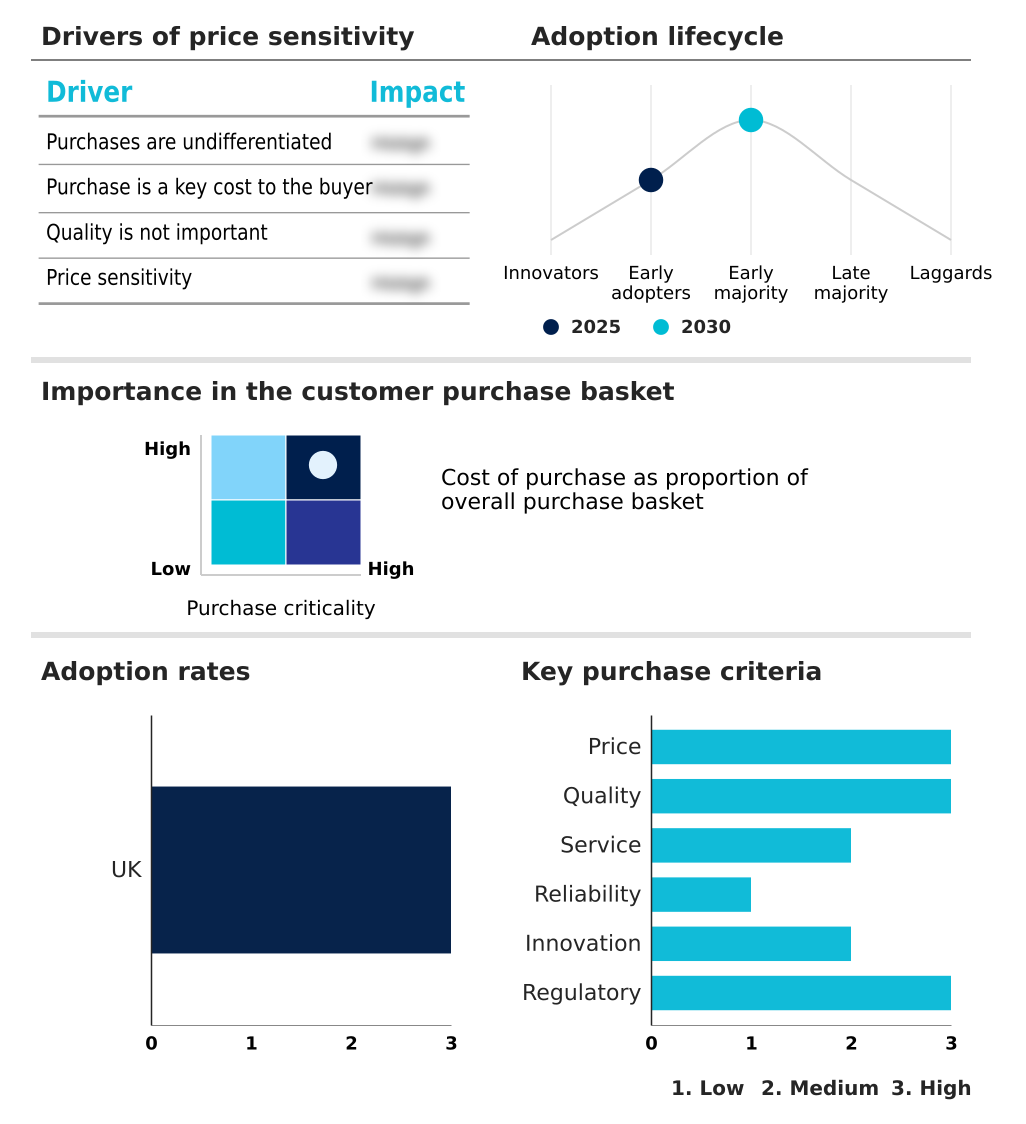

Exclusive Technavio Analysis on Customer Landscape

The uk grocery retail market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the uk grocery retail market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of UK Grocery Retail Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, uk grocery retail market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon.com Inc. - Key offerings include multi-format grocery retail, from physical supermarkets to integrated online delivery platforms, catering to diverse consumer needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon.com Inc.

- B and M Retail Ltd

- Carrefour SA

- Costco Wholesale Corp.

- EG Group

- EH Booth and Co. Ltd

- Farmfoods Ltd.

- Heron Foods Ltd.

- HOFER KG

- Iceland Foods Ltd.

- J Sainsbury plc

- Lidl US LLC

- Marks and Spencer Group

- McCormick and Co. Inc.

- Ocado Retail Ltd.

- Proudfoot Group

- SPAR UK Ltd.

- Tesco Plc

- Waitrose and Partners

- Wm Morrison Supermarkets Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Uk grocery retail market

- In March 2025, J Sainsbury plc reported its premium 'Taste the Difference' private-label range experienced a 15% sales increase, reflecting a strategic shift toward high-margin own-brand products.

- In November 2024, Ocado Retail Ltd. announced an expansion of its automated micro-fulfilment center network to reduce last-mile delivery costs and improve service speed in urban areas.

- In January 2025, Lidl US LLC revealed plans to integrate AI-powered inventory management systems across its UK stores to enhance supply chain efficiency and product availability.

- In April 2025, Tesco Plc formed a strategic partnership with a leading tech firm to pilot computer-vision-based checkout systems in its Express format stores, aiming to reduce friction for time-poor consumers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled UK Grocery Retail Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 189 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.8% |

| Market growth 2026-2030 | USD 58.5 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.7% |

| Key countries | UK |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The grocery retail market in UK is defined by a strategic pivot to technology-driven efficiency and hyper-personalized marketing. Boardroom decisions now center on investments in an omnichannel fulfillment strategy, integrating physical and digital assets. This involves deploying in-store automation technology, from the smart shopping cart and computer vision-based checkout to a full frictionless checkout system.

- Last-mile delivery optimization is being achieved through a network of automated micro-fulfilment center and dark store fulfillment models, supporting both click-and-collect service and the rapid quick commerce platform. AI-driven demand forecasting and inventory management software are now standard for managing everything from fresh produce sourcing to the ready-to-eat meal solutions.

- Retailers are leveraging a sophisticated promotional pricing strategy, including volume discount mechanics and seasonal sales campaigns, managed through customer loyalty programs. Private-label product development is a key focus, with an expanded own-brand product range that includes both entry-level private label and premium own-label range options to cater to all segments.

- This focus on own-brands has shown to improve margins by up to 5%. To ensure quality, robust supply chain traceability using cold chain logistics and food waste reduction technology is paramount.

What are the Key Data Covered in this UK Grocery Retail Market Research and Growth Report?

-

What is the expected growth of the UK Grocery Retail Market between 2026 and 2030?

-

USD 58.5 billion, at a CAGR of 3.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Food and beverages, and Non food), Distribution Channel (Hypermarkets and supermarkets, Convenience stores, Discount stores, Online, and Others), End-user (Household, Commercial, and Institutional) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Rapid urbanization and rising consumer spending, Threat from counterfeit grocery products

-

-

Who are the major players in the UK Grocery Retail Market?

-

Amazon.com Inc., B and M Retail Ltd, Carrefour SA, Costco Wholesale Corp., EG Group, EH Booth and Co. Ltd, Farmfoods Ltd., Heron Foods Ltd., HOFER KG, Iceland Foods Ltd., J Sainsbury plc, Lidl US LLC, Marks and Spencer Group, McCormick and Co. Inc., Ocado Retail Ltd., Proudfoot Group, SPAR UK Ltd., Tesco Plc, Waitrose and Partners and Wm Morrison Supermarkets Ltd.

-

Market Research Insights

- The market's digital transformation in retail is accelerating, driven by an omnichannel retail strategy that reshapes consumer spending patterns. As value-seeking consumer behavior intensifies, data-driven merchandising is critical, with firms seeing an 18% improvement in basket size analysis by optimizing their online grocery platform. This focus on customer experience enhancement is essential for building consumer trust and loyalty.

- E-commerce logistics are being refined to support the growing subscription-based model, which has shown a 25% higher retention rate than ad-hoc purchasing. Managing the integrated supply chain effectively is key to navigating supply chain disruption and ensuring food safety compliance, especially within food and beverage retailing.

- The evolution of the urban retail environment continues to favor the convenience store format for its accessibility.

We can help! Our analysts can customize this uk grocery retail market research report to meet your requirements.

RIA -

RIA -