Gynecological Cancers Therapeutics Market Size 2024-2028

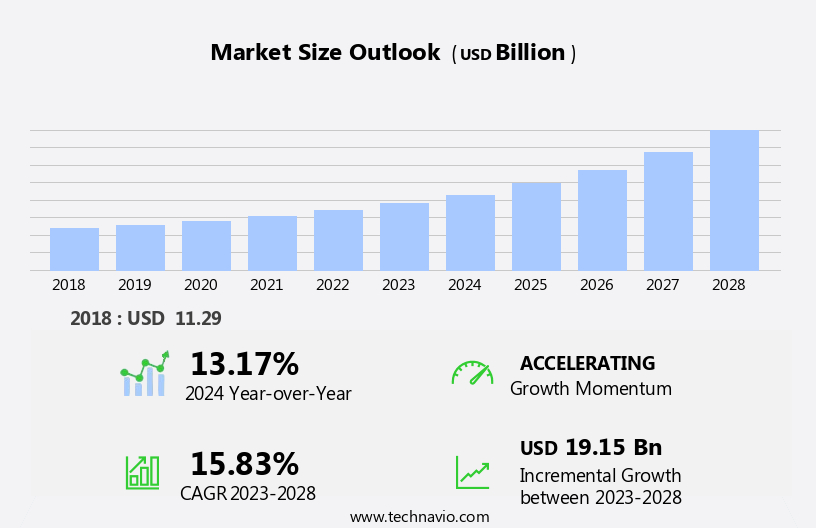

The gynecological cancers therapeutics market size is forecast to increase by USD 19.15 billion at a CAGR of 15.83% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing incidence of gynecological cancers. According to the World Health Organization, an estimated 389,000 new cases and 129,000 deaths occurred in 2020. This trend is expected to continue, driven by factors such as aging populations, rising awareness, and improved diagnostic methods. Another key driver in the market is the emergence of novel therapies. The development of targeted therapies, immunotherapies, and gene therapies is providing new treatment options for patients, leading to improved outcomes and increased survival rates. However, the high cost of these advanced therapies poses a significant challenge for both patients and healthcare systems.

- Affordability remains a critical concern, particularly in developing countries where access to healthcare is limited. In conclusion, the market is experiencing robust growth due to the rising incidence of gynecological cancers and the emergence of innovative therapies. However, the high cost of treatment remains a significant challenge that must be addressed to ensure accessibility and affordability for patients. Companies seeking to capitalize on market opportunities and navigate challenges effectively should focus on developing cost-effective treatment options while maintaining therapeutic efficacy.

What will be the Size of the Gynecological Cancers Therapeutics Market during the forecast period?

- The market is characterized by continuous evolution and dynamic market activities. genetic testing plays a pivotal role in identifying the genetic predisposition to various gynecological cancers, driving research funding towards precision medicine and personalized treatment plans. Patient support organizations are increasingly focusing on improving quality of life for patients undergoing cancer diagnosis and treatment. Cancer screening initiatives, including Molecular Diagnostics, are essential for early detection and prevention of gynecological cancers such as uterine, ovarian, cervical, vaginal, and vulvar cancers. Clinical trials and drug development are ongoing, with a focus on targeted therapy and hormonal treatments. Healthcare policy and regulatory frameworks are evolving to accommodate the needs of women's reproductive health, with a growing emphasis on patient care and patient advocacy.

- Machine learning and Data Analytics are transforming cancer diagnosis and treatment, enabling healthcare providers to deliver more accurate and effective care. Drug discovery and approval processes are underway for various gynecological cancers, with a focus on improving cancer survival rates and reducing recurrence. Digital health technologies, including telemedicine and remote monitoring, are enhancing patient care and access to healthcare services. The landscape of gynecological cancers therapeutics is ever-changing, with ongoing research and innovation in areas such as drug development, cancer prevention, and precision oncology. The future holds great promise for improving patient outcomes and advancing women's health.

How is this Gynecological Cancers Therapeutics Industry segmented?

The gynecological cancers therapeutics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Uterine cancer

- Ovarian cancer

- Cervical cancer

- Others

- Modality

- Chemotherapy

- Targeted therapy

- Hormonal therapy

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

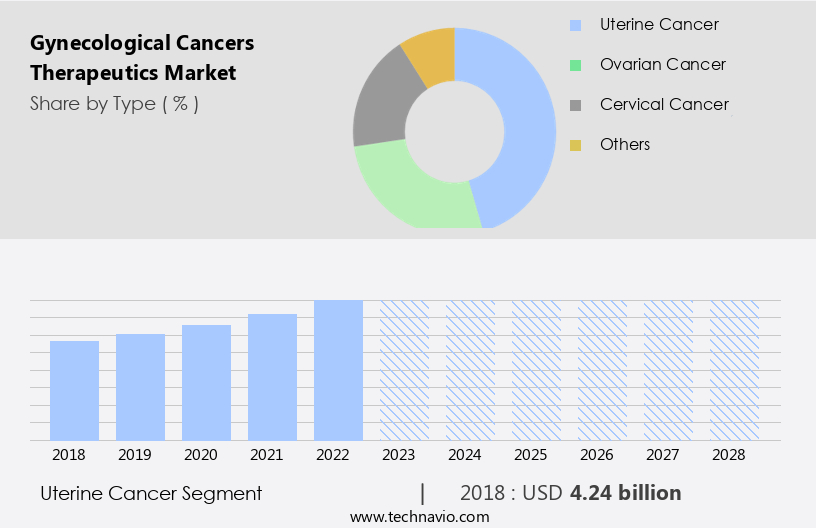

By Type Insights

The uterine cancer segment is estimated to witness significant growth during the forecast period.

Uterine cancer, specifically endometrial cancer, arises from the inner lining of the uterus and is the fourth most common cancer among women in the US, with approximately 65,950 new cases expected to be diagnosed in 2022, according to the American Cancer Society. Genetic testing plays a crucial role in identifying the underlying causes and potential risk factors for uterine cancer. Research funding from various organizations and healthcare policy initiatives drives advancements in molecular diagnostics and clinical trials for early cancer detection and precision medicine. Patient support groups and advocacy organizations provide essential resources for patients, ensuring quality of life during cancer diagnosis and treatment.

Drug development and approval processes prioritize targeted therapy and hormonal treatments for uterine cancer, while machine learning and artificial intelligence facilitate data analytics and personalized medicine. Healthcare providers and Medical Devices contribute to improved patient care and reproductive health, with a focus on cancer prevention, screening, and cancer recurrence management. Ovarian and vaginal cancers, along with cervical and vulvar cancers, are also significant concerns within gynecological cancers. Clinical research and drug discovery efforts continue to advance our understanding of these complex diseases and pave the way for innovative treatments and improved cancer survival rates.

The Uterine cancer segment was valued at USD 4.24 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

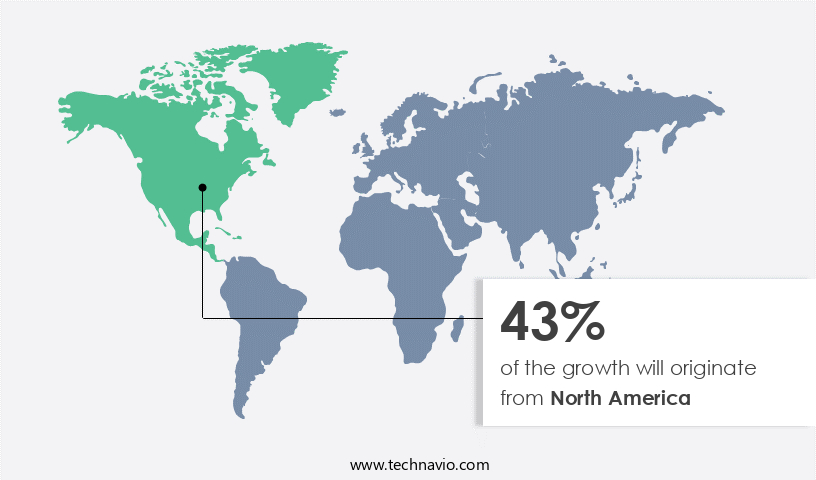

North America is estimated to contribute 43% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In North America, the market is experiencing significant growth due to several key factors. The increasing incidence of gynecological cancers, such as ovarian and cervical cancers, is a major driver of market expansion. For instance, in the US alone, it is estimated that over 14,000 women will be diagnosed with cervical cancer, and over 4,000 may succumb to the disease in 2022, despite undergoing screening and treatment. Similarly, ovarian cancer, which causes more deaths than any other gynecological cancer, is a significant concern. Government initiatives and favorable reimbursement schemes are also contributing to market growth. For example, the US National Cancer Institute (NCI) has launched several initiatives to improve cancer diagnosis and treatment, including the Precision Medicine Initiative and the Cancer Moonshot program.

Additionally, the availability of new drugs for gynecological cancers, such as targeted therapies and hormonal treatments, is driving market growth. Furthermore, advancements in technology, such as machine learning and artificial intelligence, are enabling the development of more effective diagnostic tools and personalized treatment plans. Molecular diagnostics and genetic testing are becoming increasingly important in the diagnosis and treatment of gynecological cancers, as they allow for more precise identification of cancer types and subtypes. Patient advocacy groups and healthcare providers are also playing a crucial role in raising awareness about gynecological cancers and improving patient care. Clinical trials and research funding are essential for advancing cancer treatment and improving patient outcomes.

The focus on precision medicine and personalized treatment plans is leading to better quality of life for patients and increased cancer survival rates. The market for gynecological cancers therapeutics is also being shaped by regulatory developments, such as drug approvals and drug regulations. For instance, the US Food and Drug Administration (FDA) has approved several new drugs for gynecological cancers in recent years, including drugs for ovarian, cervical, and endometrial cancers. In conclusion, the market in North America is experiencing significant growth due to the increasing incidence of gynecological cancers, government initiatives, favorable reimbursement schemes, and technological advancements. The availability of new drugs and regulatory approvals, as well as the focus on precision medicine and patient care, are also contributing to market expansion.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Gynecological Cancers Therapeutics Industry?

- The rising prevalence of gynecological cancers serves as the primary market driver.

- Gynecological cancers, which include cervical, ovarian, uterine, vaginal, and vulvar cancers, are among the most common types of cancer diagnosed in women after breast cancer in the US. According to the Centers for Disease Control and Prevention (CDC), approximately 71,500 new cases and 26,500 deaths are attributed to gynecological cancers annually in the US. The risk of developing these cancers increases with age. Advancements in genetic testing, molecular diagnostics, and cancer screening are crucial in early detection and improving the quality of life for patients. Research funding and patient support organizations play a significant role in advancing precision medicine and developing new treatments for gynecological cancers.

- The increasing incidence of gynecological cancers, particularly cervical, uterine, and ovarian cancer, can be attributed to risk factors such as obesity, viral infections, smoking, and immune system deficiency. It is essential to prioritize cancer prevention and early detection through regular screenings and lifestyle modifications to reduce the risk of developing gynecological cancers. In conclusion, the advancements in cancer research and diagnostics, coupled with increased awareness and funding, offer hope for improving the lives of those affected by gynecological cancers. By focusing on early detection and prevention, we can reduce the number of new cases and deaths attributed to these cancers.

What are the market trends shaping the Gynecological Cancers Therapeutics Industry?

- The emergence of novel therapies is a significant market trend, reflecting the ongoing advancements in healthcare and scientific research. Innovative treatments are increasingly shaping the industry landscape, offering new hope for patients and driving growth in various sectors.

- Gynecological cancers, including uterine and ovarian varieties, pose significant challenges in patient care and reproductive health. However, the landscape of therapeutics is evolving, with a focus on cancer prevention and innovative treatments. Clinical trials are ongoing to discover and develop safer drugs for gynecological cancers, leading to the emergence of advanced therapies such as gene therapy, hormonal therapy, and chimeric antigen receptor (CAR) T-Cell Therapy. Gene therapy holds great promise against gynecological cancers, particularly ovarian cancer. This approach utilizes various strategies, such as immunopotentiation, angiogenesis inhibition, pharmacological resistance alteration, gene restoration or destruction, suicide genes, and oncolytic virotherapy.

- These strategies aim to combat gynecological cancers more effectively and with fewer side effects. Machine learning and healthcare policy initiatives are also playing crucial roles in advancing gynecological cancer therapeutics. By analyzing vast amounts of data, machine learning algorithms can help identify potential drug targets and personalized treatment plans for patients. Additionally, healthcare policies that prioritize cancer research and patient care contribute to the overall progress in this field. In conclusion, the ongoing research and development efforts in gynecological cancer therapeutics are yielding significant advancements. Innovative therapies like gene therapy, hormonal therapy, and CAR T-cell therapy are emerging as promising options for treating gynecological cancers, such as ovarian and uterine cancer.

- The integration of technologies like machine learning and healthcare policy initiatives is further accelerating progress in this field.

What challenges does the Gynecological Cancers Therapeutics Industry face during its growth?

- The escalating costs of treatment represent a significant obstacle to the expansion and growth of the industry.

- Gynecological cancers, including cervical and vulvar cancers, necessitate prolonged treatment, leading to substantial economic burdens for patients. The high cost is primarily due to the advanced procedures involved in the development of targeted therapies, such as Monoclonal Antibodies. These therapies, which include biologics, undergo intricate manufacturing processes that significantly increase their production costs and, consequently, their sales prices. Patient advocacy groups are pushing for more affordable treatment options and increased drug regulation to ensure the approval of cost-effective alternatives.

- Precision oncology, a key area of focus in cancer treatment, is expected to bring about more targeted and effective therapies, potentially reducing overall treatment costs. Despite these efforts, the financial burden on patients with gynecological cancers remains a significant challenge.

Exclusive Customer Landscape

The gynecological cancers therapeutics market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gynecological cancers therapeutics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, gynecological cancers therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - The company specializes in gynecological cancers therapeutics, including Elahere (mirvetuximab soravtansine-gynx), an innovative antibody-drug conjugate (ADC) approved for platinum-resistant ovarian cancer (PROC). This first-in-class ADC targets folate receptor alpha (FolR?), a protein overexpressed in many gynecological cancers. By selectively binding to FolR?, Elahere delivers a potent cytotoxic payload, enhancing tumor cell destruction while minimizing harm to healthy cells. This targeted approach offers a promising solution for women with PROC, who have limited treatment options and poor prognosis. Elahere's approval marks a significant milestone in the ongoing fight against gynecological cancers, demonstrating the company's commitment to advancing cancer care through groundbreaking therapies.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Amgen Inc.

- Apotex Inc.

- AstraZeneca Plc

- Bayer AG

- Bristol Myers Squibb Co.

- Cipla Ltd.

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- GlaxoSmithKline Plc

- Hikma Pharmaceuticals Plc

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- Sanofi SA

- Takeda Pharmaceutical Co. Ltd.

- Teva Pharmaceutical Industries Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Gynecological Cancers Therapeutics Market

- In February 2024, Roche Holding AG announced the US Food and Drug Administration (FDA) approval of its new targeted therapy, Polatuzumab Vedotin-piiq, in combination with bendamustine and a rituximab regimen for the treatment of relapsed or refractory diffuse large B-cell lymphoma (DLBCL) in adult patients. This approval expanded the company's oncology portfolio and addressed an unmet medical need in the market (Roche Press Release, 2024).

- In March 2025, Pfizer Inc. And Merck KGaA, Darmstadt, Germany, entered into a strategic collaboration to develop and commercialize avelumab, an investigational fully human anti-programmed death-ligand 1 (PD-L1) antibody, for the treatment of various gynecological cancers, including ovarian and endometrial cancers. This collaboration combined Pfizer's commercial capabilities with Merck KGaA's expertise in immuno-oncology, aiming to bring innovative treatments to patients (Pfizer Press Release, 2025).

- In June 2024, AstraZeneca plc completed the acquisition of Alexion Pharmaceuticals Inc. For approximately USD30 billion. This acquisition granted AstraZeneca access to Alexion's portfolio of complement-dependent therapeutic products, including Ultomiris, a long-acting C5 complement inhibitor for the prevention of paroxysmal nocturnal hemoglobinuria (PNH) and atypical hemolytic uremic syndrome (aHUS) in adult and pediatric patients. This acquisition expanded AstraZeneca's presence in the market, particularly in the area of rare diseases (AstraZeneca Press Release, 2024).

- In October 2025, the European Commission approved the use of Keytruda (pembrolizumab), an anti-PD-1 therapy from Merck & Co. Inc., for the treatment of recurrent or advanced endometrial carcinoma that has progressed following prior platinum-containing chemotherapy. This approval marked the first PD-1 inhibitor to receive approval for this indication in Europe and represented a significant advancement in the treatment landscape for endometrial cancer patients (Merck Press Release, 2025).

Research Analyst Overview

The market is witnessing significant advancements, driven by the integration of disease management strategies and patient education. Neoadjuvant therapy, a crucial component of disease management, is gaining traction due to its ability to improve treatment outcomes and reduce the need for extensive surgeries. Tumor heterogeneity poses a challenge in developing effective therapies, leading to the exploration of immune checkpoint inhibitors and car T-cell therapy. However, managing side effects and drug interactions remains a concern. The tumor microenvironment and cancer stem cells are increasingly being recognized as key targets for novel therapies, including cytotoxic agents, parp inhibitors, and angiogenesis inhibitors. Personalized treatment plans, enabled by cancer genomics and next-generation sequencing, are revolutionizing care.

Health outcomes, including quality-adjusted life years, are the ultimate goal, with adjuvant therapy and palliative care playing essential roles in improving patient empowerment and survival rates. Liquid biopsies offer promising opportunities for early detection and monitoring disease progression. Overall, the market is dynamic, with ongoing research and innovation shaping the future of cancer care.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Gynecological Cancers Therapeutics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 15.83% |

|

Market growth 2024-2028 |

USD 19.15 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

13.17 |

|

Key countries |

US, Canada, Germany, UK, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Gynecological Cancers Therapeutics Market Research and Growth Report?

- CAGR of the Gynecological Cancers Therapeutics industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the gynecological cancers therapeutics market growth of industry companies

We can help! Our analysts can customize this gynecological cancers therapeutics market research report to meet your requirements.

RIA -

RIA -