Heart Valves In Pediatric Patients Market Size 2025-2029

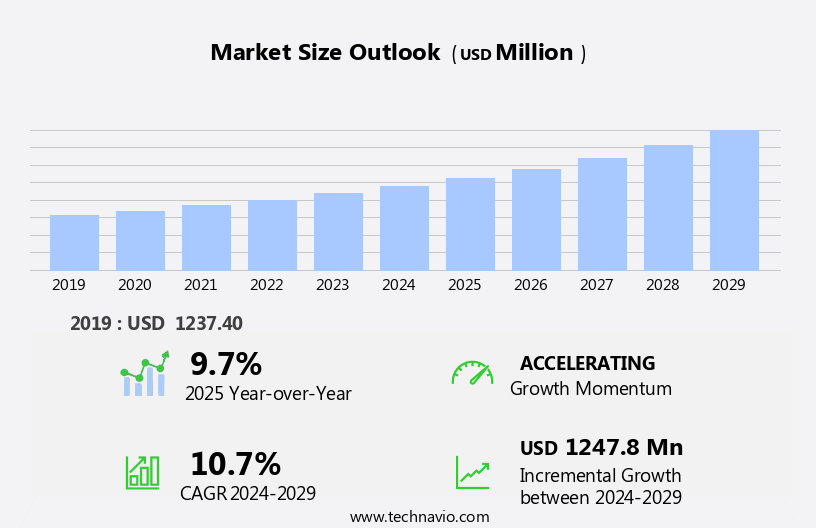

The heart valves in pediatric patients market size is forecast to increase by USD 1.25 billion, at a CAGR of 10.7% between 2024 and 2029.

- The market is experiencing significant growth due to the rising incidence of congenital heart defects (CHDs) among pediatric populations. CHDs are the most common type of birth defect, affecting approximately 1 in every 100 children worldwide. This increasing prevalence creates a substantial demand for advanced heart valve solutions. Another key trend in the market is the growing focus on the development of minimally invasive heart valve replacement techniques. These approaches offer numerous benefits, including reduced surgical trauma, shorter hospital stays, and faster recovery times. This shift towards less invasive procedures is expected to drive market growth and attract new players. Furthermore, the increasing shortage of skilled medical professionals, particularly in developing regions, can limit market penetration and growth potential.

- However, the market also faces challenges, primarily due to the increasing shortage of skilled medical professionals specialized in pediatric cardiology and cardiac surgery. This shortage may limit the availability of specialized care for pediatric patients, potentially hindering market expansion. Companies seeking to capitalize on market opportunities and navigate these challenges effectively should focus on collaborations, partnerships, and investments in training and education programs to address the skills gap. These innovative approaches offer reduced surgical risk, faster recovery times, and improved patient outcomes, making them increasingly attractive to healthcare providers and families.

What will be the Size of the Heart Valves In Pediatric Patients Market during the forecast period?

- The pediatric heart valves market is characterized by continuous evolution and dynamic market activities. Biological valves, such as those derived from porcine or bovine sources, continue to be utilized in valve implantation procedures due to their potential for improved hemodynamics and reduced thrombosis risk. However, the development of mechanical valves, including tissue and mechanical options, offers advantages in terms of durability and valve positioning precision. Valve surgery research is a significant area of focus, with ongoing investigations into valve function, valve performance, and valve outcomes. The pediatric heart valves market encompasses the latest advancements, research, and treatment options for valve disorders in children.

- Transcatheter valve replacement techniques have gained traction, offering minimally invasive alternatives to traditional valve surgery. Valve longevity remains a critical concern, with ongoing research into valve degeneration and valve chordae tendineae. Valve insufficiency, valve dysfunction, valve thrombosis, and valve stenosis are common complications, necessitating ongoing valve management strategies. Valve ring and valve leaflet repair techniques are being refined to improve valve durability and reduce the need for valve replacement.

- Transcatheter heart valve replacements, which involve inserting valves through catheters, are gaining popularity due to their advantages, such as reduced trauma, quicker recovery, and lower risk of complications.

How is this Heart Valves In Pediatric Patients Industry segmented?

The heart valves in pediatric patients industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Aortic valve

- Pulmonary valve

- Others

- Product

- Heart valve replacement devices

- Heart valve repair devices

- End-user

- Hospitals

- Specialty clinics

- ASCs

- Academic and research institutes

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

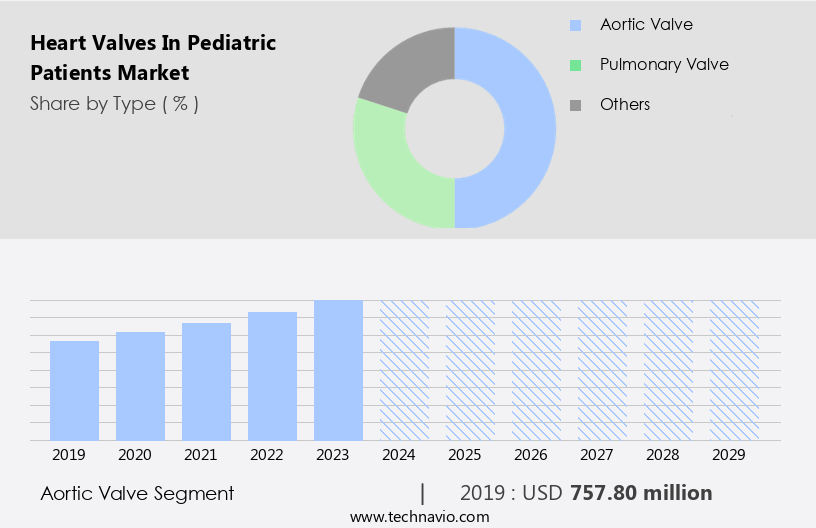

The aortic valve segment is estimated to witness significant growth during the forecast period. Aortic valves play a crucial role in regulating blood flow between the left ventricle and the aorta in pediatric patients. Dysfunction of the aortic valve, including stenosis and regurgitation, can significantly impact cardiovascular health. Aortic valve stenosis occurs when the heart's aortic valve, situated between the left ventricle and the aorta, becomes obstructed due to the entanglement of its constituent leaflets. This impedes the valve's complete separation, increasing the left ventricle's workload and potentially reducing the amount of blood ejected to the body. Valve repair and replacement techniques are essential interventions for restoring proper blood circulation and preventing complications.

Mechanical and tissue valves, such as porcine and pericardial valves, are commonly used for valve replacement. Valve hemodynamics, positioning, and papillary muscle function are critical factors in valve outcomes. Minimally invasive surgery and transcatheter valve replacement offer alternatives to traditional open-heart procedures. Valve function, performance, and longevity are essential considerations for valve management. Valve complications, including calcification, thrombosis, stenosis, and insufficiency, can impact valve durability and require reintervention or reoperation. Valve degeneration and chordae tendineae dysfunction can also contribute to valve dysfunction. Cardiac imaging techniques, such as cardiac MRI and cardiac CT, aid in valve evaluation and monitoring.

Valve size and positioning are essential factors in valve implantation and replacement techniques. Pediatric cardiology specialists focus on managing congenital heart diseases and optimizing valve function and outcomes. Valve repair techniques, including ring annuloplasty and leaflet repair, are employed to restore valve function without the need for replacement. Valve sizing and follow-up are essential components of valve management to ensure optimal valve performance and patient outcomes.

The Aortic valve segment was valued at USD 757.80 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

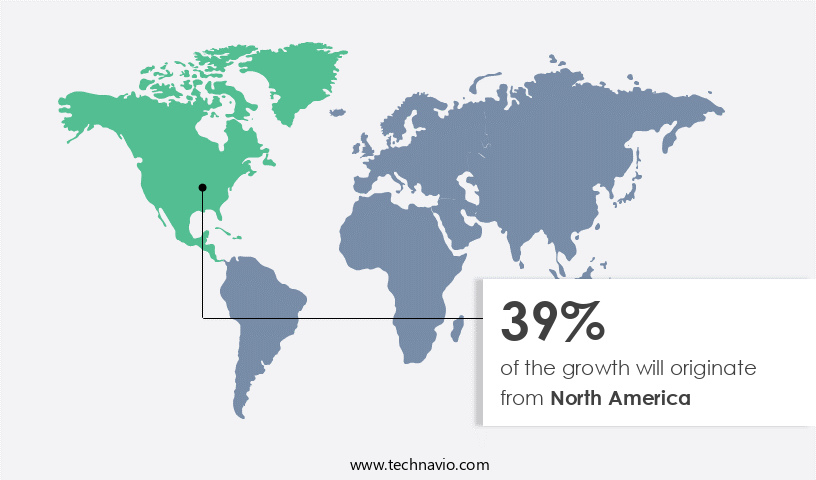

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the realm of pediatric healthcare, the North American market holds a significant stance in the heart valves sector. Boasting advanced medical facilities, renowned pediatric cardiology centers, and a robust regulatory framework, the US and Canada lead the way in shaping the future of pediatric cardiac care. The prevalence of congenital heart diseases in the pediatric population is a major driver for the demand of sophisticated medical interventions, particularly heart valve treatments. Valve degeneration and calcification are ongoing challenges, leading to clinical trials and research into valve preservation and valve prosthesis materials.

Tissue valves, such as porcine and pericardial valves, and mechanical valves, offer varying advantages in terms of valve performance and durability. Valve complications, including regurgitation, thrombosis, stenosis, and calcification, are closely monitored to ensure optimal valve outcomes. Valve management, including implantation, positioning, and follow-up, is a critical aspect of pediatric cardiac care. Minimally invasive surgery and transcatheter valve replacement have emerged as promising alternatives to traditional heart valve replacement. Valve imaging techniques, including cardiac MRI and cardiac CT, provide valuable insights into valve hemodynamics and valve sizing. Pediatric cardiology, a specialized field, plays a pivotal role in the diagnosis and treatment of heart valve conditions.

Congenital heart diseases, such as mitral valve regurgitation, aortic valve stenosis, and tricuspid valve insufficiency, are common in pediatric patients. Valve repair techniques, including valve ring replacement and chordae tendineae repair, are essential for addressing valve dysfunction. The heart valve market in North America is expected to grow, driven by ongoing research and advancements in valve technology. Valve replacement techniques, such as aortic valve replacement and pulmonary valve replacement, continue to evolve, with a focus on improving valve durability and patient outcomes. Valve longevity and degeneration are major areas of research, as is the development of biocompatible valves to minimize the risk of complications.

The North American market for heart valves in pediatric patients is a dynamic and evolving landscape, shaped by advances in medical research, technology, and pediatric cardiology. The focus on improving valve function, durability, and patient outcomes continues to drive innovation and growth in this sector.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Heart Valves In Pediatric Patients Industry?

- The increasing prevalence of congenital heart defects (CHDs) in the pediatric population serves as the primary market driver. Congrations on your interest in heart valve conditions and treatments in pediatric patients in the US. Congenital heart defects (CHDs), present at birth, can significantly impact heart valve structure and function. Approximately 40,000 infants annually are affected by these defects in the US, with over two million individuals living with them, ranging from infancy to adulthood. CHDs can involve heart valves, walls, arteries, or veins, and their severity varies. Following early-life heart procedures to improve blood flow to the lungs, some pediatric patients may experience pulmonary regurgitation due to a non-functioning pulmonary valve. Valve repair or implantation, using tissue or mechanical valves, is essential to address such complications.

- Valve performance, valve cusps, valve annulus, and valve survival are crucial factors in valve management. Valve repair aims to preserve the native valve structure, while valve implantation involves replacing the damaged valve with a new one. Tissue valves, derived from animal or human donors, and mechanical valves, made of synthetic materials, offer unique advantages and challenges in terms of valve function and recovery. Valve complications, such as valve regurgitation and valve thrombosis, can occur following valve surgery. Mitral valve conditions, including mitral valve regurgitation and mitral stenosis, are common in pediatric patients. Ensuring proper valve function and minimizing complications are essential for optimal patient outcomes.

What are the market trends shaping the Heart Valves In Pediatric Patients Industry?

- The market is shifting towards the development of minimally invasive solutions, which is an emerging trend. It is essential for businesses to focus increasingly on this area to remain competitive. The pediatric heart valves market has seen significant advancements with a focus on minimally invasive heart valve replacement procedures. Minimally invasive techniques, such as transcatheter valve implantation, are gaining popularity in the market. These procedures involve inserting heart valves through catheters, typically accessed via blood vessels, avoiding the need for open-chest surgeries. This approach offers numerous benefits, including reduced trauma, quicker recovery, and a lower risk of complications, which are essential in the sensitive realm of pediatric cardiac interventions. Companies are heavily investing in R&D to perfect and enhance minimally invasive technologies designed specifically for pediatric patients.

- Valve hemodynamics and valve positioning are critical factors influencing valve outcomes. Pediatric cardiology, a subspecialty of cardiology, deals with the diagnosis and management of congenital heart disease, making the development of effective and safe valve solutions a priority. Prosthetic valves, such as porcine and pericardial valves, are commonly used in valve surgery. However, the issue of valve calcification remains a challenge, necessitating ongoing research and innovation. Valve surgery outcomes are crucial in the pediatric population, as the long-term impact on growth and development must be considered. Minimally invasive valve surgery is expected to offer improved outcomes due to reduced trauma and quicker recovery.

What challenges does the Heart Valves In Pediatric Patients Industry face during its growth?

- The scarcity of adequately skilled medical professionals poses a significant challenge to the expansion and progression of the healthcare industry. The pediatric heart valves market faces a significant challenge due to the scarcity of skilled medical professionals. The increasing demand for specialized care for pediatric heart conditions necessitates the expertise of pediatric cardiologists and cardiac surgeons. However, the shortage of these professionals can lead to delays in diagnosis, inadequate treatment, and suboptimal outcomes for pediatric patients. Valve conditions in pediatric patients can manifest in various forms, including valve insufficiency, valve dysfunction, valve thrombosis, valve stenosis, and valve degeneration. These conditions can impact the biological valves, such as the pulmonary valve, and require surgical intervention or transcatheter valve replacement. Advancements in technology have led to the development of non-invasive diagnostic tools like cardiac MRI and cardiac CT, enabling early detection and monitoring of valve conditions.

- However, the precision and expertise required for valve surgery remain critical. Valve longevity is also a concern, as valve chordae tendineae can weaken over time, leading to valve degeneration. Valve ring replacement and other surgical interventions require a high level of expertise and precision. The long-term success of these procedures depends on the skills of the medical team and the quality of the valve replacement materials. Therefore, the shortage of skilled professionals in pediatric cardiology and cardiac surgery can significantly impact the market's growth and the quality of care for pediatric patients with heart valve conditions.

Exclusive Customer Landscape

The heart valves in pediatric patients market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the heart valves in pediatric patients market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, heart valves in pediatric patients market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The company specializes in providing advanced pediatric heart valve solutions, including the Masters HP 15mm rotatable mechanical heart valve.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Artivion Inc.

- Boston Scientific Corp.

- Braile Biomedica

- Colibri Heart Valve LLC

- Edwards Lifesciences Corp.

- JenaValve Technology Inc.

- Lepu Medical Technology Beijing Co. Ltd.

- LivaNova PLC

- Massachusetts Institute of Technology

- Medtronic Plc

- Shockwave Medical Inc.

- TTK Healthcare Ltd.

- Xeltis AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Heart Valves In Pediatric Patients Market

- In February 2025, Edwards Lifesciences, a leading global provider of medical devices, announced the U.S. Food and Drug Administration (FDA) approval of its Sapien 3 Ultra Transcatheter Heart Valve for use in pediatric patients with aortic valve stenosis. This approval marks a significant advancement in the treatment options for this patient population (Edwards Lifesciences Press Release, 2025).

- In November 2024, Medtronic and Boston Scientific, two major players in the heart valve market, entered into a definitive agreement to combine their cardiovascular and structural heart businesses. This merger is expected to create a leading company in the heart valve space, strengthening their portfolios and expanding their reach (Medtronic Press Release, 2024).

- In January 2024, Abbott Laboratories received FDA approval for its Melody Transcatheter Pulmonic Valve for use in pediatric patients with pulmonic valve regurgitation. This approval marked Abbott's entry into the pediatric heart valve market, broadening the company's product offerings and addressing an unmet medical need (Abbott Laboratories Press Release, 2024).

- In June 2023, the European Commission approved the Medtronic Intrepid Dual Cartridge Transcatheter Aortic Valve Replacement System for use in Europe. This approval signified a technological advancement in the heart valve market, as the Intrepid System offers the ability to deliver two valve sizes in a single procedure, potentially reducing the number of procedures required for pediatric patients.

Research Analyst Overview

The pediatric heart valves market encompasses a range of products and services, including valve-related industry regulations, cardiac catheterization, hospitalizations, exercise capacity, patient satisfaction, and various surgical procedures such as the Ross procedure and transapical approach. Pulmonary hypertension, a common condition in pediatric patients, significantly impacts valve-related healthcare costs and clinical pathways. Patient support, education, and experience are crucial factors, with bioprosthetic and mechanical valves offering different functional statuses and potential complications like infection, bleeding, stroke, arrhythmia, and ethical considerations.

The Heart Valves in Pediatric Patients Market is advancing rapidly, focusing on innovative solutions like bioprosthetic valves and mechanical valves to improve outcomes in congenital heart surgery. The transfemoral approach is gaining traction as a minimally invasive option. Addressing concerns such as valverelated stroke, valverelated infection, valverelated bleeding, and valverelated arrhythmia is critical to enhancing safety. Preventing valverelated death and optimizing valverelated functional status and valverelated exercise capacity remain top priorities. Hospitals are reducing valverelated hospitalizations and mitigating valverelated societal impact while improving valverelated patient satisfaction and valverelated patient experience. Enhanced valverelated patient education, valverelated patient empowerment, and valverelated patient support are reshaping care models. Refining valverelated clinical pathways, implementing valverelated best practices, and addressing valverelated ethical considerations are essential for market growth.

Heart failure, a significant challenge in pediatric cardiology, necessitates best practices and patient empowerment for optimal outcomes. Valve-related healthcare costs, clinical pathways, and patient experience are key trends shaping the market. The Heart Valves in Pediatric Patients Market is advancing rapidly, focusing on innovative solutions like biological valves, mechanical valves, and prosthetic valves for congenital heart defects. Specialized tissue valves, including porcine valves, bovine valves, and pericardial valves, offer enhanced durability and biocompatibility. The role of valve papillary muscles in valve function is crucial, influencing outcomes in young patients. Procedures such as valve reintervention and valve reoperation ensure long-term success, while continuous valve monitoring and valve follow-up aid in post-surgical care. Addressing valve surgery complications and optimizing valve surgery recovery are priorities for improving patient outcomes.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Heart Valves In Pediatric Patients Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

224 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.7% |

|

Market growth 2025-2029 |

USD 1.25 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.7 |

|

Key countries |

US, China, Germany, Canada, France, UK, Japan, India, Italy, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Heart Valves In Pediatric Patients Market Research and Growth Report?

- CAGR of the Heart Valves In Pediatric Patients industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the heart valves in pediatric patients market growth of industry companies

We can help! Our analysts can customize this heart valves in pediatric patients market research report to meet your requirements.

RIA -

RIA -