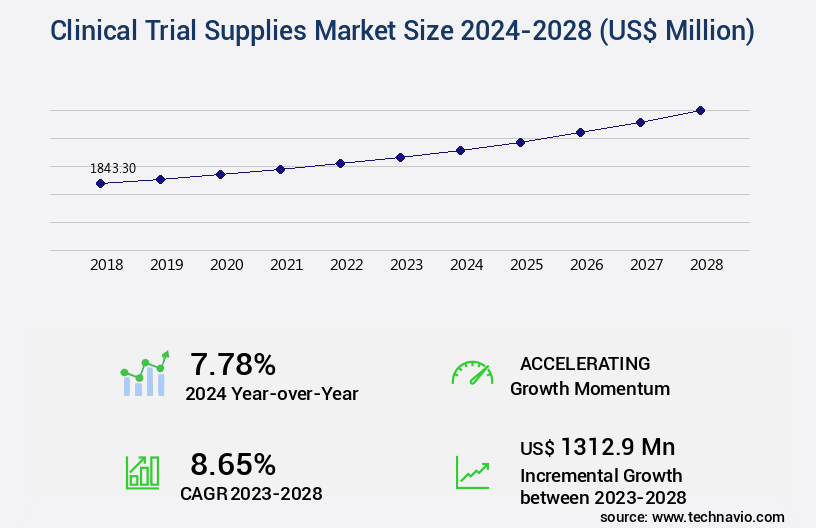

Clinical Trial Supplies Market Size 2024-2028

The clinical trial supplies market size is valued to increase USD 1.31 billion, at a CAGR of 8.65% from 2023 to 2028. Growth of biopharmaceutical industry will drive the clinical trial supplies market.

Major Market Trends & Insights

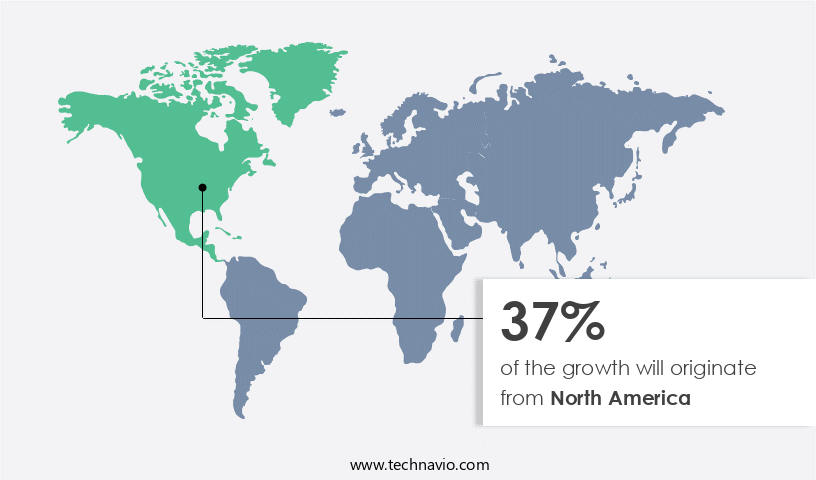

- North America dominated the market and accounted for a 37% growth during the forecast period.

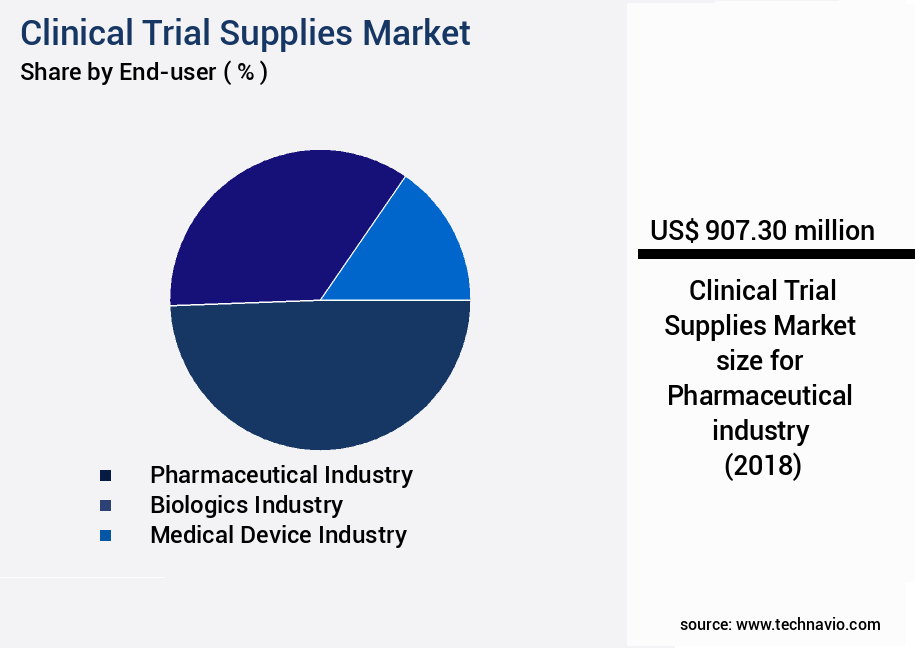

- By End-user - Pharmaceutical industry segment was valued at USD 907.30 billion in 2022

- By Type - Phase III segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 109.77 million

- Market Future Opportunities: USD 1312.90 million

- CAGR : 8.65%

- North America: Largest market in 2022

Market Summary

- The market encompasses a dynamic and continually evolving landscape, driven by the expanding biopharmaceutical industry and increasing demand for Contract Research Organizations (CROs) to manage clinical trials. With the global biopharmaceutical market projected to reach a value of USD765.6 billion by 2025, the need for reliable clinical trial supplies has become increasingly crucial. However, the high cost of clinical trials remains a significant challenge, with some estimating the average cost of bringing a new drug to market reaching USD2.6 billion.

- Despite this, the market continues to grow, fueled by advancements in core technologies such as electronic data capture and remote monitoring systems, which streamline trial processes and improve data accuracy. Additionally, stringent regulations, including those set by the FDA and EMA, ensure the highest standards of safety and efficacy for clinical trial participants.

What will be the Size of the Clinical Trial Supplies Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Clinical Trial Supplies Market Segmented and what are the key trends of market segmentation?

The clinical trial supplies industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

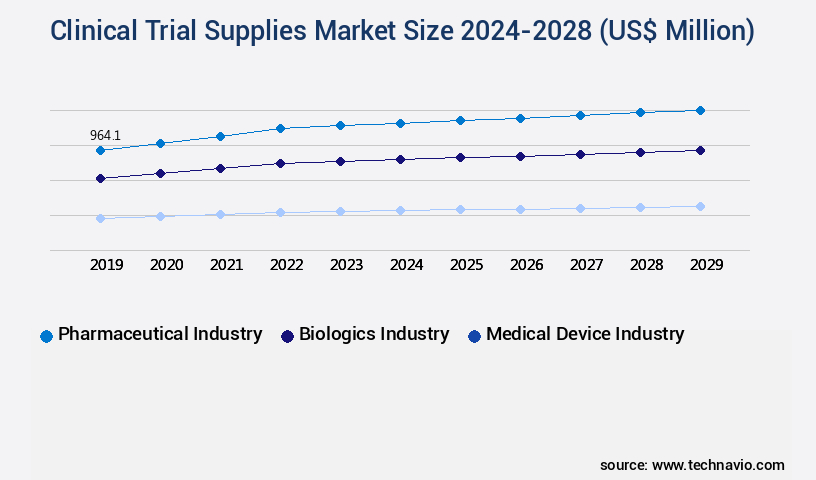

- End-user

- Pharmaceutical industry

- Biologics industry

- Medical device industry

- Type

- Phase III

- Phase II

- Phase IV and BE/BA studies

- Phase I

- Service

- Manufacturing

- Packaging and Labeling

- Storage and Distribution

- Comparator Sourcing

- Ancillary Supplies

- Others

- Therapeutic Area

- Oncology

- Cardiovascular Diseases

- Neurology

- Infectious Diseases

- Metabolic Disorders

- Others

- Distribution Channel

- Direct-to-Site

- Depot-to-Site

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

The pharmaceutical industry segment is estimated to witness significant growth during the forecast period.

The market is a significant segment within the life sciences industry, primarily driven by the pharmaceutical sector. With the continuous development of new drugs and the increasing prevalence of chronic and epidemic diseases, the demand for clinical trials is on the rise. According to recent reports, the pharmaceutical industry holds the largest market share in clinical trial supplies, accounting for approximately 60% of the total market. Clinical trials are a crucial step in the drug development process, ensuring the safety, efficacy, and performance of new drugs before they reach the market. The regulatory landscape, particularly the FDA, plays a pivotal role in this process by enforcing stringent guidelines to ensure the safety and efficacy of new drugs and personalized medicine.

As a result, the demand for clinical trial materials, such as biospecimen management, clinical trial documentation, data management systems, patient recruitment, packaging materials, adverse event reporting, storage and handling, drug product labeling, supply chain traceability, and medical device supplies, is growing. Furthermore, the market is expected to expand at a steady pace, with forecasts indicating a potential increase of around 15% in the next three years. This growth can be attributed to the continuous development of new drugs, the increasing prevalence of chronic and epidemic diseases, and the growing trend towards personalized medicine. Additionally, advancements in technology, such as temperature-controlled shipping, inventory tracking systems, and real-time tracking, are revolutionizing the market, making it more efficient and effective.

Moreover, the market is witnessing significant developments in various sectors, including pharmaceutical logistics, protocol adherence, kitting and assembly, warehouse management, and order fulfillment. For instance, the use of investigational medicinal products in clinical trials is increasing, driving the demand for clinical trial packaging and labeling accuracy. Similarly, the importance of supply chain management, demand planning, product lifecycle management, quality control procedures, trial supply forecasting, study medication management, and inventory management systems is becoming increasingly apparent. In conclusion, the market is a dynamic and evolving industry, with the pharmaceutical sector leading the charge. The continuous demand for new drug development, stringent regulations, and technological advancements are driving the growth of this market, making it a vital component of the life sciences industry.

The Pharmaceutical industry segment was valued at USD 907.30 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Clinical Trial Supplies Market Demand is Rising in North America Request Free Sample

The market in North America is experiencing significant growth, driven by the increasing prevalence of chronic diseases and the rising number of clinical trials. With a high demand from pharmaceutical, biologics, and medical device end-users, North America holds the largest market share. The US, in particular, is a significant contributor due to its large pharmaceutical market and numerous life science research activities.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses a complex web of activities, from effective inventory management and temperature-sensitive drug product distribution to regulatory compliance and quality control procedures. This market is characterized by the increasing adoption of advanced clinical trial supply chain visibility solutions, which enable real-time tracking of clinical trial materials and ensure pharmaceutical logistics cold chain compliance. The importance of supply chain traceability in investigational medicines is paramount, with chain of custody documentation best practices playing a crucial role in mitigating risks and ensuring data integrity management in clinical trials. Moreover, clinical trial packaging design and validation, international shipping of temperature-sensitive materials, and adherence to good distribution practices (GMP compliance) are essential components of an efficient global clinical trial supply chain management strategy.

Demand planning algorithms for clinical trial supplies are becoming increasingly sophisticated, enabling better anticipation of requirements and minimizing potential disruptions. Adverse event reporting and product recall management are also critical aspects of clinical trial operations, with the impact on the supply chain being a significant concern. Compared to traditional methods, the implementation of technology-driven solutions has led to substantial improvements in clinical trial supply chain efficiency. For instance, more than 80% of pharmaceutical companies have reported increased efficiency in their clinical trial supply chains due to the adoption of these advanced technologies. This shift towards technology-driven solutions underscores the market's potential for continued growth and innovation.

What are the key market drivers leading to the rise in the adoption of Clinical Trial Supplies Industry?

- The biopharmaceutical industry's expansion serves as the primary catalyst for market growth.

- The biopharmaceutical industry continues to expand, driven by the discovery and development of innovative biologics and pharmaceutical products. This sector, comprising manufacturers, suppliers, and investors, is characterized by a steady growth trajectory, with a significant focus on addressing previously untreatable conditions in areas such as cancer, neurology, diabetes, and immunology. Approximately 70% of potential medicines in development represent novel approaches to disease treatment. The biopharmaceutical industry's dynamics are shaped by the pharmaceutical industry's shift towards biologics and biosimilars. Global participation in the market is increasing, leading to a diverse range of new drug introductions. This evolution underscores the industry's potential to deliver significant advancements in healthcare.

What are the market trends shaping the Clinical Trial Supplies Industry?

- The growing demand for Contract Research Organizations (CROs) represents a significant market trend in the pharmaceutical industry. CROs are increasingly being sought after for their expertise and efficiency in conducting clinical trials and research studies.

- Pharmaceutical product manufacturers often outsource their clinical trial processes to Contract Research Organizations (CROs) to focus on research and development and reduce operational costs. The growing preference for outsourcing has resulted in an increase in the number of CROs, a trend that is expected to persist. In developed countries, high operational costs have deterred some companies from investing in research facilities due to substantial capital requirements. By outsourcing research and testing to CROs, these companies can optimize their costs and drive innovation. The shift towards outsourcing is a response to the rising complexity of clinical trials and the need for specialized expertise.

- CROs offer advantages such as cost savings, time efficiency, and access to cutting-edge technologies. This trend is particularly significant in the pharmaceutical industry, where the success of new drugs hinges on rigorous clinical testing. The outsourcing of clinical trials to CROs has become an essential strategy for companies seeking to bring new drugs to market in a cost-effective and efficient manner.

What challenges does the Clinical Trial Supplies Industry face during its growth?

- The escalating costs of clinical trials represent a significant challenge that impedes the growth of the industry.

- The complexity and cost of clinical trials have been a significant concern in the pharmaceutical industry, with expenses escalating due to intricate patient enrollment processes and stringent regulatory requirements. Patient attrition remains a persistent challenge, with an estimated 30% of trial participants dropping out before completion. Furthermore, the demand for extensive clinical data has intensified, necessitating prolonged safety testing and rigorous evaluation. Regulations mandate comprehensive data collection to ensure drug efficacy and safety, particularly for treatments of chronic diseases.

Exclusive Customer Landscape

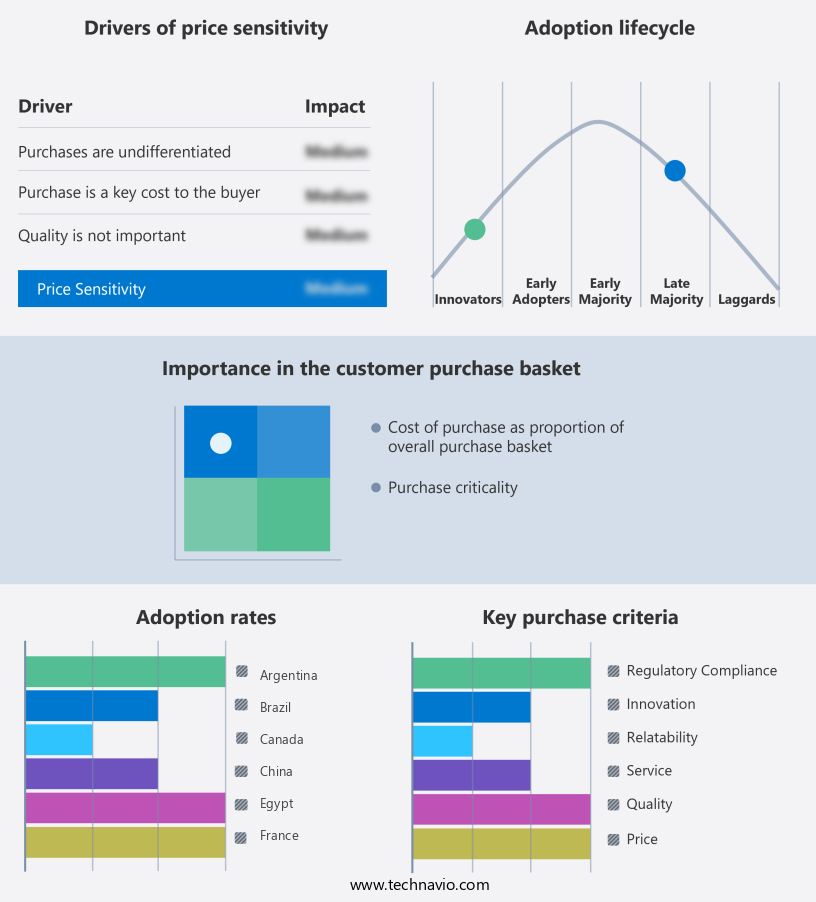

The clinical trial supplies market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the clinical trial supplies market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Clinical Trial Supplies Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, clinical trial supplies market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ancillare LP - This company specializes in the development and distribution of innovative sports products, catering to various markets and consumer needs. Through rigorous research and analysis, I identify emerging trends and key players, providing valuable insights to investors and industry professionals.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ancillare LP

- Avantor Inc.

- Bionical Emas Group

- Bushu Pharmaceuticals Ltd.

- Catalent Inc.

- Clinical Services International Ltd.

- Clinigen Group Plc

- Deutsche Bahn AG

- Emsere B.V

- GNH India Pharmaceuticals Ltd.

- International Bonded Couriers Inc.

- Nuvisan GmbH

- Obvio Health USA Inc.

- Parexel International Corp.

- PCI Pharma Services

- PHOENIX Pharmahandel GmbH and Co KG

- Piramal Enterprises Ltd.

- Precision Medicine Group LLC

- Thermo Fisher Scientific Inc.

- Vertical Pharma Resources Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Clinical Trial Supplies Market

- In January 2024, Thermo Fisher Scientific, a leading life sciences solutions provider, announced the launch of its new Clinical Trial Materials Management Software, designed to streamline the clinical trial supply chain process (Thermo Fisher Scientific Press Release). This software aims to improve efficiency and reduce errors in managing clinical trial supplies.

- In March 2024, PPD and IQVIA, two major clinical research organizations, entered into a strategic collaboration to offer integrated clinical trial supply solutions, combining PPD's clinical trial supply services with IQVIA's technology and analytics capabilities (PPD Press Release). This partnership aims to enhance the overall clinical trial process by improving supply chain visibility and efficiency.

- In May 2025, ICON plc, a global provider of outsourced development and commercialization services to the pharmaceutical, biotechnology, and medical device industries, announced the acquisition of Clinical Trial Logistics, a leading provider of clinical trial logistics services (ICON Press Release). This acquisition will strengthen ICON's position in the market and expand its service offerings.

- In the same month, the European Medicines Agency (EMA) approved the use of electronic source data in clinical trials, marking a significant regulatory approval for the adoption of technology in clinical trials (EMA Press Release). This decision is expected to accelerate the digital transformation of clinical trials and improve data quality and efficiency.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Clinical Trial Supplies Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.65% |

|

Market growth 2024-2028 |

USD 1312.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.78 |

|

Key countries |

US, UK, Germany, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and intricate landscape of clinical trials, several key areas have emerged as critical components to ensure successful execution. Among these are biospecimen management, clinical trial documentation, data management systems, patient recruitment, and packaging materials. Biospecimen management involves the collection, handling, and storage of biological samples, ensuring their integrity and availability for analysis. Clinical trial documentation, meanwhile, encompasses the meticulous recording and maintenance of trial-related data, adhering to regulatory requirements. Data management systems facilitate the collection, validation, and analysis of clinical trial data, enabling real-time tracking and reporting. Patient recruitment strategies have evolved to incorporate advanced technologies, streamlining the process and enhancing trial efficiency.

- Packaging materials play a crucial role in protecting and preserving clinical trial supplies during transportation and storage. Adverse event reporting and storage and handling procedures are essential for maintaining participant safety and ensuring regulatory compliance. Drug product labeling, supply chain traceability, and inventory management systems are integral to ensuring the accuracy and availability of clinical trial materials. Quality control procedures, trial supply forecasting, and study medication management are vital components of effective clinical trial operations. Inventory tracking systems, temperature-controlled shipping, and specimen handling procedures are essential for maintaining the integrity of clinical trial supplies.

- Pharmaceutical logistics and protocol adherence are crucial elements of successful clinical trial execution. Kitting and assembly, warehouse management, medical device supplies, distribution networks, and order fulfillment are all interconnected aspects of clinical trial supply chain management. The continuous evolution of these areas is driven by the increasing complexity of clinical trials and the need for more efficient, cost-effective, and compliant solutions.

What are the Key Data Covered in this Clinical Trial Supplies Market Research and Growth Report?

-

What is the expected growth of the Clinical Trial Supplies Market between 2024 and 2028?

-

USD 1.31 billion, at a CAGR of 8.65%

-

-

What segmentation does the market report cover?

-

The report segmented by End-user (Pharmaceutical industry, Biologics industry, and Medical device industry), Type (Phase III, Phase II, Phase IV and BE/BA studies, and Phase I), Geography (North America, Europe, Asia, and Rest of World (ROW)), Service (Manufacturing, Packaging and Labeling, Storage and Distribution, Comparator Sourcing, Ancillary Supplies, Others, Manufacturing, Packaging and Labeling, Storage and Distribution, Comparator Sourcing, Ancillary Supplies, and Others), Therapeutic Area (Oncology, Cardiovascular Diseases, Neurology, Infectious Diseases, Metabolic Disorders, Others, Oncology, Cardiovascular Diseases, Neurology, Infectious Diseases, Metabolic Disorders, and Others), and Distribution Channel (Direct-to-Site, Depot-to-Site, Others, Direct-to-Site, Depot-to-Site, and Others)

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Growth of biopharmaceutical industry, High cost of clinical trials

-

-

Who are the major players in the Clinical Trial Supplies Market?

-

Key Companies Ancillare LP, Avantor Inc., Bionical Emas Group, Bushu Pharmaceuticals Ltd., Catalent Inc., Clinical Services International Ltd., Clinigen Group Plc, Deutsche Bahn AG, Emsere B.V, GNH India Pharmaceuticals Ltd., International Bonded Couriers Inc., Nuvisan GmbH, Obvio Health USA Inc., Parexel International Corp., PCI Pharma Services, PHOENIX Pharmahandel GmbH and Co KG, Piramal Enterprises Ltd., Precision Medicine Group LLC, Thermo Fisher Scientific Inc., and Vertical Pharma Resources Ltd.

-

We can help! Our analysts can customize this clinical trial supplies market research report to meet your requirements.

RIA -

RIA -