High Voltage Equipment Market Size 2024-2028

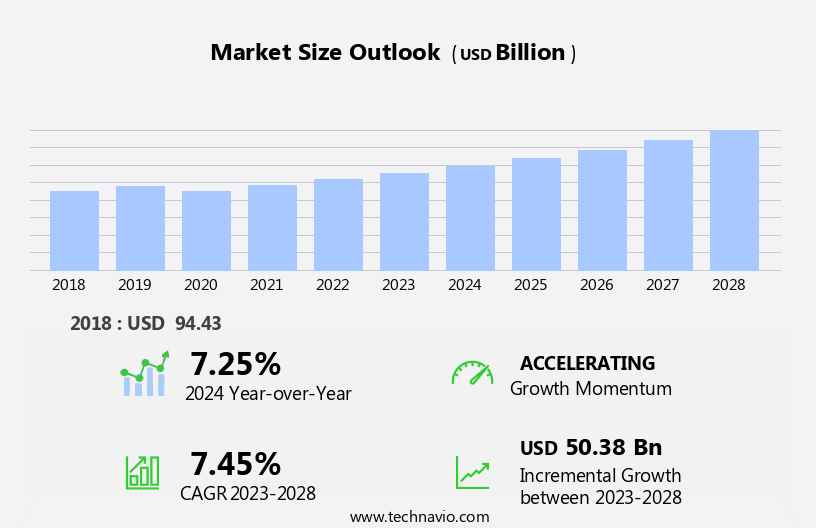

The high voltage equipment market size is forecast to increase by USD 50.38 billion at a CAGR of 7.45% between 2023 and 2028.

What will be the Size of the High Voltage Equipment Market During the Forecast Period?

How is this High Voltage Equipment Industry segmented and which is the largest segment?

The high voltage equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Power transmission

- Power distribution

- Type

- Transformer

- Switchgear

- Reactive power equipment

- Relay panel

- Others

- Geography

- APAC

- China

- India

- Europe

- Germany

- UK

- North America

- US

- South America

- Middle East and Africa

- APAC

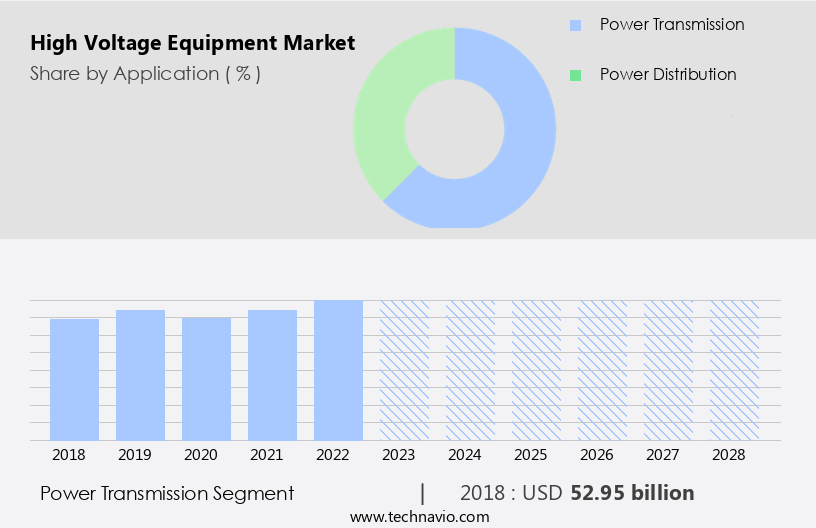

By Application Insights

- The power transmission segment is estimated to witness significant growth during the forecast period.

The market is experiencing notable growth due to several influential factors. The expanding industrialization and population growth necessitate increased electricity consumption, leading to the demand for efficient power transmission systems. High-voltage equipment, comprising transformers, circuit breakers, and switchgear, plays a pivotal role in facilitating the reliable and efficient transfer of electrical energy over extended distances. Furthermore, the integration of renewable energy sources, such as wind and solar power, into the grid necessitates robust high-voltage equipment to manage their intermittent nature. As countries prioritize transitioning to cleaner energy solutions, the demand for high-voltage equipment to support renewable energy integration continues to escalate.

This trend is particularly significant In the context of the power transmission segment, which is poised for substantial growth In the coming years.

Get a glance at the High Voltage Equipment Industry report of share of various segments Request Free Sample

The Power transmission segment was valued at USD 52.95 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

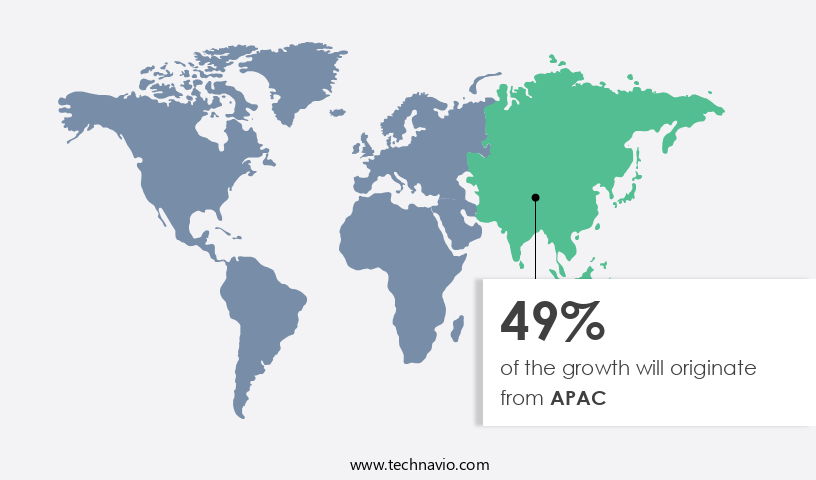

- APAC is estimated to contribute 49% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The Asia Pacific (APAC) region experiences significant electricity demand due to the expansion of electricity-consuming sectors and increasing urban population. Countries In the area are attracting private investments to meet the growing electricity needs, driven by rising standards of living and industrialization. China holds a substantial market share in APAC's high-voltage equipment sector. The region's population growth and urbanization, along with government initiatives for rural electrification, fuel the demand for electricity. High-voltage equipment plays a crucial role in power generation, transmission, and distribution, including solar and wind energy farms, transmission grids, electricity measurement, and electricity supply to various sectors such as commercial vehicles, heavy machinery, and uninterrupted power supplies.

Key applications include transformers, circuit breakers, switchgears, and various control equipment. The market is influenced by factors like economic uncertainty, capital expenditures, and the need for grid modernization and energy efficiency.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of High Voltage Equipment Industry?

Rising requirements for power from residential, industrial, and commercial sectors is the key driver of the market.

What are the market trends shaping the High Voltage Equipment Industry?

Evolution of smart grids is the upcoming market trend.

What challenges does the High Voltage Equipment Industry face during its growth?

Stringent environmental regulations associated with manufacturing of high-voltage equipment is a key challenge affecting the industry growth.

Exclusive Customer Landscape

The high voltage equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the high voltage equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, high voltage equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

ABB Ltd. - The company specializes in providing high-voltage equipment solutions, encompassing switchgear and breakers capable of handling voltages up to 1200 kV AC and 1100 kV DC. This equipment caters to the power industry's demands for reliable and efficient energy transmission and distribution. The company's offerings adhere to stringent safety and performance standards, ensuring optimal system performance and minimal downtime. With a focus on innovation and technological advancements, the company's solutions contribute to enhancing the overall efficiency and sustainability of power systems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- ALSTOM SA

- Bharat Heavy Electricals Ltd.

- CG Power and Industrial Solutions Ltd.

- DuPont de Nemours Inc.

- Eaton Corp. Plc

- Emerson Electric Co.

- ETEL TRANSFORMERS PTY LTD.

- Fuji Electric Co. Ltd.

- General Electric Co.

- Hitachi Ltd.

- Honeywell International Inc.

- Hubbell Inc.

- Hyundai Electric and Energy Systems Co. Ltd.

- Mitsubishi Electric Corp.

- Schneider Electric SE

- Siemens AG

- Sumitomo Electric Industries Ltd.

- TBEA Co. Ltd.

- Toshiba Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a wide range of technologies and applications withIn the electrical power industry. This sector plays a crucial role In the transmission and distribution of electricity, enabling the efficient transfer of power from generation sources to end-users. High voltage equipment is essential for various applications, including power generation, transmission grids, and electricity measurement. These systems facilitate the conversion, measurement, and control of electric currents to ensure the reliable and efficient delivery of electricity. Substations, transformers, circuit breakers, switchgears, and various control and protection devices are key components of this market. The growth of high voltage equipment is influenced by several factors, including industrialization expansion, economic uncertainty, and accessibility to electricity.

The increasing global population and the expansion of renewable energy sources, such as solar power, wind power, and hydropower, have led to a surge in electricity consumption and the need for advanced transmission and distribution systems. The aging power grids in many parts of the world necessitate modernization activities to address operational limitations, safety norms, and voltage level concerns. Smart grid technologies, such as real-time monitoring, optimization, and distribution sector automation, are increasingly being adopted to enhance the efficiency and reliability of electricity supply. Investment in high voltage equipment is driven by the need for energy storage systems, including batteries and pumped hydro storage, to ensure uninterrupted power supplies and support the integration of renewable energy sources into the grid.

The adoption of electric vehicles (EVs) and the expansion of charging infrastructure also contribute to the growth of this market. The market is diverse, with applications ranging from low voltage applications in commercial and residential settings to high voltage applications in industrial processes, transportation, and mining. The electrical industry continues to evolve, with digitization and electrified industrial operations driving innovation in this sector. The use of high voltage equipment in power generation and transmission also has environmental implications, as the reduction of carbon emissions is a key focus for many governments and industries. Renewable energy systems, such as solar energy and wind energy, are increasingly being integrated into the grid to support emission reduction efforts.

In conclusion, the market plays a vital role In the electrical power industry, enabling the efficient and reliable transmission and distribution of electricity. The market is driven by various factors, including industrialization expansion, renewable energy sources, and grid modernization activities. The ongoing evolution of the electrical industry and the integration of smart grid technologies are expected to continue shaping the growth of this market.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

179 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.45% |

|

Market growth 2024-2028 |

USD 50.38 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

7.25 |

|

Key countries |

US, China, India, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this High Voltage Equipment Market Research and Growth Report?

- CAGR of the High Voltage Equipment industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the high voltage equipment market growth of industry companies

We can help! Our analysts can customize this high voltage equipment market research report to meet your requirements.

RIA -

RIA -