Hospital Command Center Platforms Market Size and Growth Forecast 2026-2030

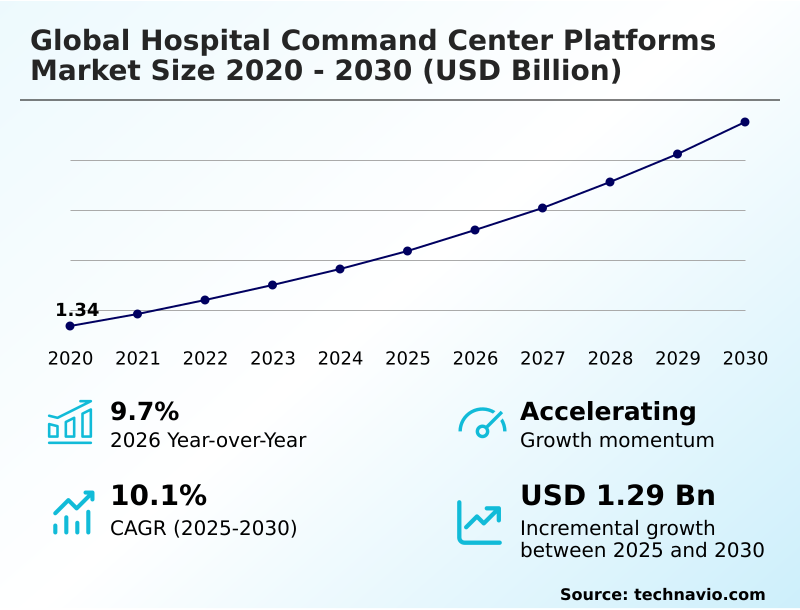

The Hospital Command Center Platforms Market size was valued at USD 2.09 billion in 2025 growing at a CAGR of 10.1% during the forecast period 2026-2030.

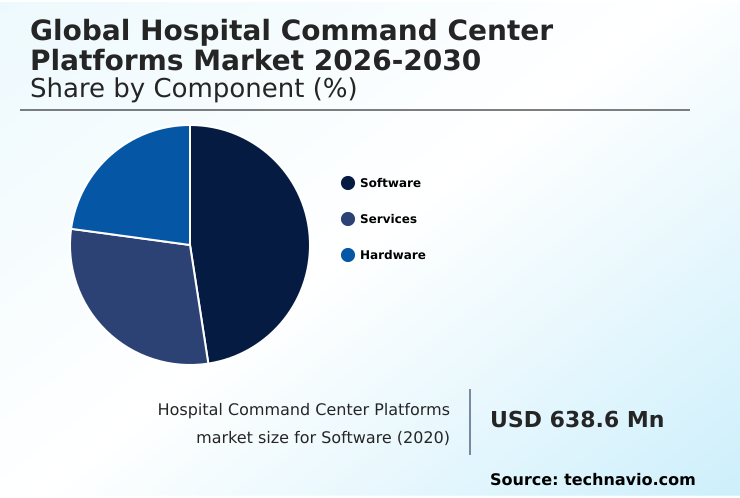

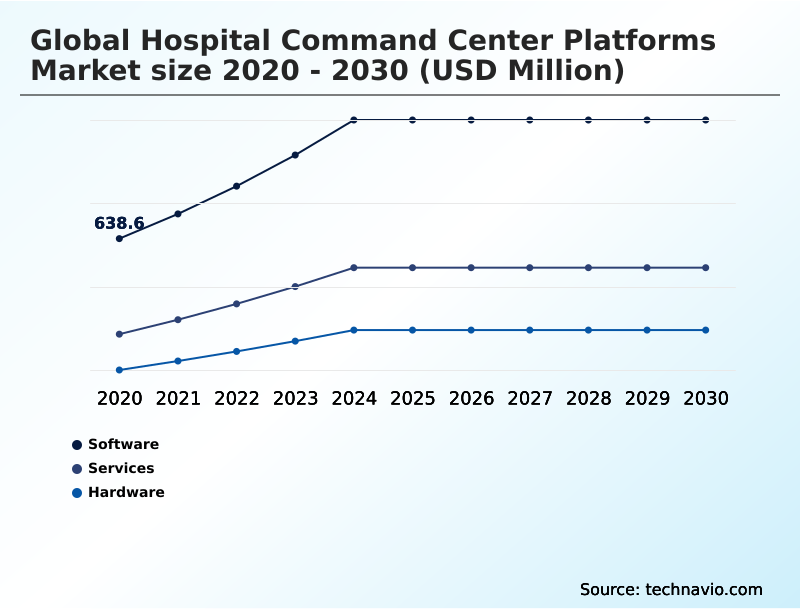

North America accounts for 45.1% of incremental growth during the forecast period. The Software segment by Component was valued at USD 938.2 million in 2024, while the Capacity management segment holds the largest revenue share by Application.

The market is projected to grow by USD 2.04 billion from 2020 to 2030, with USD 1.29 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Hospital Command Center Platforms Market Overview

The hospital command center platforms market is defined by the strategic imperative for healthcare institutions to enhance operational control and clinical oversight. These platforms leverage a predictive analytics engine to facilitate patient flow optimization and workforce orchestration, moving beyond reactive management. A core function is the seamless electronic health records integration, providing the rich dataset required for sophisticated clinical decision support. In a typical scenario, a large academic medical center deploys a command center to manage emergency department throughput; by using patient acuity scores and real-time location services, the facility can reduce patient wait times by over 15% and better align staffing with demand. Compliance with interoperability standards, such as HL7 FHIR, is non-negotiable, ensuring that data from various systems, including those for bed turnover management, can be aggregated for a unified operational view. This centralized monitoring capability allows for systematic improvements in care coordination and institutional efficiency.

Drivers, Trends, and Challenges in the Hospital Command Center Platforms Market

Strategic decision-making in the hospital command center platforms market is increasingly influenced by the need for comprehensive, data-driven oversight of clinical and operational workflows. As health systems grapple with improving hospital operational efficiency with data, the focus shifts to deploying solutions that offer not just retrospective reporting but also ai driven predictive analytics for patient surges.

This capability is crucial for proactive resource management. The implementation of systems for real time patient flow and bed management allows facilities to optimize capacity and reduce patient wait times, directly impacting both patient satisfaction and revenue.

For example, a multi-hospital system orchestrating patient care across multiple facilities can achieve a more balanced load, preventing any single emergency department from becoming overwhelmed. A key part of this is centralized resource allocation in healthcare, which ensures that staffing, equipment, and beds are deployed where the need is greatest.

All these data-driven processes must adhere to stringent regulations like the Health Insurance Portability and Accountability Act (HIPAA), which governs the use and transmission of protected health information. The effectiveness of these platforms is significantly greater than traditional, siloed management methods, with some integrated systems reducing patient length of stay by up to 20% compared to those without centralized orchestration.

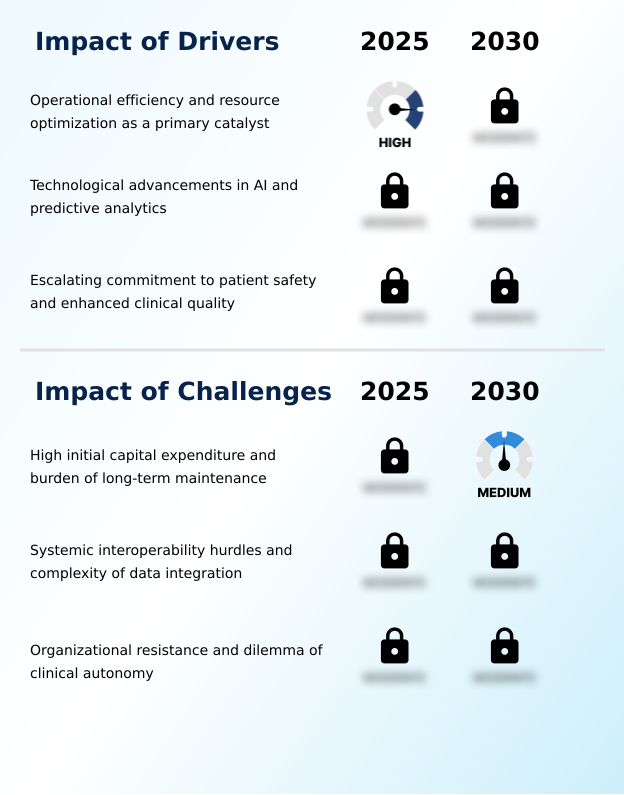

Primary Growth Driver: The critical need for operational efficiency and resource optimization is a primary driver for the hospital command center platforms market.

The primary driver for the adoption of hospital command center platforms is the urgent need for enhanced operational efficiency and resource optimization.

Healthcare providers are leveraging these systems for throughput optimization and to gain comprehensive operational visibility across the entire enterprise. By implementing sophisticated resource allocation algorithms and capacity management dashboards, hospitals can proactively manage patient flow and reduce costly bottlenecks.

The integration of advanced healthcare data analytics and clinical intelligence allows for a transition from retrospective analysis to predictive foresight, enabling better workforce orchestration and patient journey mapping.

A heightened focus on patient safety monitoring, a driver contributing to the market's 9.7% year-over-year growth, compels the use of centralized clinical surveillance to detect early warning signs and improve outcomes.

These platforms are becoming indispensable for maintaining both financial sustainability and high standards of care.

Emerging Market Trend: The integration of generative AI and natural language processing is a significant trend, reshaping the capabilities of hospital command center platforms.

Key trends are reshaping the functionality of hospital command center platforms, primarily through advanced software capabilities. The adoption of generative AI integration and natural language processing allows platforms to deliver narrative-based insights, automating tasks like discharge summary generation and enabling conversational inquiries for faster clinical decision support.

This shift supports the rise of virtual command centers, which leverage cloud technology to decouple operational oversight from a physical room. Such models are critical for enabling health system orchestration across wide geographic areas. Another significant development is the extension of monitoring into the home, with platforms managing hospital at home logistics and integrating remote patient monitoring data.

This convergence of acute care and remote management, underpinned by sophisticated mobile workflow solutions, is creating a more integrated, patient-centric healthcare ecosystem that relies on robust data aggregation platform technology.

Key Industry Challenge: The high initial capital expenditure and the long-term maintenance burden present a key challenge to market growth.

Significant challenges constrain the widespread adoption of hospital command center platforms, led by the high initial capital investment and ongoing maintenance costs. For many institutions, the total cost of ownership, which includes infrastructure, specialized labor, and software updates, is a major financial barrier. A more profound technical hurdle is the issue of systemic data interoperability in healthcare operations.

Integrating disparate legacy systems often requires extensive custom programming and navigating a landscape with a lack of standardized data protocols, which can compromise the effectiveness of even the most advanced predictive analytics engine. A technical audit in a major European consortium found over 40% of medical devices lacked the necessary APIs for real-time data streaming.

Furthermore, organizational resistance and concerns over clinical autonomy present a significant cultural challenge, as staff may perceive centralized monitoring as a threat, hindering the successful implementation of new clinical workflow automation.

Explore Full Market Dynamics Analysis Request Free Sample

Hospital Command Center Platforms Market Segmentation

The hospital command center platforms industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Component Segment Analysis

The software segment is estimated to witness significant growth during the forecast period.

The software segment, which accounts for a substantial 49.6% of the hospital command center platforms market, serves as the core intelligence layer. These platforms utilize data integration middleware to synthesize information from disparate sources, enabling comprehensive operational visibility.

Through advanced resource allocation algorithms, facilities can optimize bed turnover management and streamline clinical workflow automation. The integration with electronic health records is fundamental, providing the data foundation for predictive analytics engines that inform capacity management dashboards.

As required by the Health Insurance Portability and Accountability Act (HIPAA), these software solutions incorporate robust security for patient data.

This focus on data-driven operations allows for proactive discharge planning automation, which is critical for managing patient throughput and reducing length of stay.

The Software segment was valued at USD 938.2 million in 2024 and showed a gradual increase during the forecast period.

Hospital Command Center Platforms Market by Region: North America Leads with 45.1% Growth Share

North America is estimated to contribute 45.1% to the growth of the global market during the forecast period.

The geographic landscape of the hospital command center platforms market is characterized by varying adoption maturity, with North America leading at over 45% of market growth.

This region's focus is on health system orchestration and leveraging clinical intelligence for population health management across large, integrated networks.

In Europe, which contributes nearly 24% to growth, the emphasis is on regional coordination and compliance with GDPR for data handling.

APAC is the fastest-growing region, with an expected CAGR of 10.7%, driven by new smart hospital projects and the adoption of virtual command centers to bridge care gaps.

These regional hubs increasingly rely on robust healthcare workflow automation to manage resources. In all regions, the ability to support hospital at home logistics is becoming a key differentiator, expanding the command center's scope beyond the traditional hospital walls.

Customer Landscape Analysis for the Hospital Command Center Platforms Market

The hospital command center platforms market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hospital command center platforms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Hospital Command Center Platforms Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the hospital command center platforms market industry.

ABOUT Healthcare Inc. - Offerings include platforms for real-time patient flow management and capacity visualization, enabling centralized coordination across the care continuum.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABOUT Healthcare Inc.

- AlayaCare

- Appian Corp.

- Ascom Holding AG

- CenTrak Inc.

- Epic Systems Corp.

- GE HealthCare Technologies

- Health Catalyst Inc.

- Honeywell International Inc.

- Koninklijke Philips NV

- LeanTaaS Inc.

- Medical Information Tech Inc.

- Merative L.P.

- Microsoft Corp.

- Oracle Corp.

- Qventus Inc.

- Salesforce Inc.

- Siemens Healthineers AG

- Spok Holdings Inc.

- Stryker Corp.

- TeleTracking Tech Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Hospital Command Center Platforms Market

- In April 2025, Epic Systems Corporation announced the release of a specialized generative artificial intelligence tool integrated within its command center suite that automatically identifies and communicates potential bottlenecks in a patient's clinical journey.

- In April 2025, Oracle Health introduced an advanced orchestration update to its command center software which utilizes proprietary machine learning to automate the scheduling of specialized clinical personnel across multi-state hospital networks.

- In May 2025, Microsoft announced a significant expansion of its Cloud for Healthcare portfolio, introducing specialized command center orchestration tools that allow hospitals to utilize high-performance computing for predicting patient discharge timelines across regional networks.

- In March 2025, Siemens Healthineers introduced an advanced orchestration layer for its platform that utilizes generative artificial intelligence to suggest immediate staffing adjustments based on predicted patient arrivals.

Research Analyst Overview: Hospital Command Center Platforms Market

The hospital command center platforms market is driven by the imperative to enhance clinical and operational control through data synthesis. Boardroom decisions on capital expenditure are increasingly tied to a platform's ability to deliver measurable throughput optimization and improve patient flow optimization.

The core of these systems is a predictive analytics engine that enables dynamic capacity management dashboards, moving facilities beyond static reporting. These platforms depend on robust electronic health records integration and adherence to interoperability standards to enable effective clinical workflow automation.

For instance, the use of real-time data streaming and patient acuity scores allows for proactive workforce orchestration and bed turnover management. Furthermore, the integration of generative ai integration and ambient sensing technology is enhancing clinical surveillance capabilities.

A critical consideration for procurement is the platform's data integration middleware, which must securely manage real-time location services and facilitate discharge planning automation while complying with data privacy mandates like the General Data Protection Regulation (GDPR). The software component dominates the market, contributing nearly 50% of the total revenue, underscoring its central role in modern healthcare operations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hospital Command Center Platforms Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.1% |

| Market growth 2026-2030 | USD 1288.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, Australia, India, South Korea, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Hospital Command Center Platforms Market: Key Questions Answered in This Report

-

What is the expected growth of the Hospital Command Center Platforms Market between 2026 and 2030?

-

The Hospital Command Center Platforms Market is expected to grow by USD 1.29 billion during 2026-2030, registering a CAGR of 10.1%. Year-over-year growth in 2026 is estimated at 9.7%%. This acceleration is shaped by operational efficiency and resource optimization as a primary catalyst, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Services, and Hardware), Application (Capacity management, Emergency response, Staffing and workforce management, Quality and safety monitoring, and Others), Deployment (Cloud based, and On premises) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Software segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 45.1% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, Australia, India, South Korea, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Egypt and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is operational efficiency and resource optimization as a primary catalyst, which is accelerating investment and industry demand. The main challenge is high initial capital expenditure and burden of long-term maintenance, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Hospital Command Center Platforms Market?

-

Key vendors include ABOUT Healthcare Inc., AlayaCare, Appian Corp., Ascom Holding AG, CenTrak Inc., Epic Systems Corp., GE HealthCare Technologies, Health Catalyst Inc., Honeywell International Inc., Koninklijke Philips NV, LeanTaaS Inc., Medical Information Tech Inc., Merative L.P., Microsoft Corp., Oracle Corp., Qventus Inc., Salesforce Inc., Siemens Healthineers AG, Spok Holdings Inc., Stryker Corp. and TeleTracking Tech Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Hospital Command Center Platforms Market Research Insights

Market dynamics are shaped by the pressure to improve operational efficiency metrics. North America leads regional contributions, accounting for over 45% of the incremental growth, driven by advanced healthcare data analytics and the need to manage costs. In contrast, APAC is the fastest-growing region, with a focus on building new digital infrastructure.

A key aspect of clinical operations management is patient transfer coordination, where platforms must ensure data integrity under regulations like GDPR. For instance, in a health system orchestration scenario, data aggregation platforms must seamlessly connect multiple facilities.

The adoption of predictive staffing models and care pathway analysis tools is critical for optimizing resources and improving emergency department throughput, reflecting a shift toward more proactive, data-informed healthcare management.

We can help! Our analysts can customize this hospital command center platforms market research report to meet your requirements.

RIA -

RIA -