Hydrodesulfurization Catalysts Market Size 2024-2028

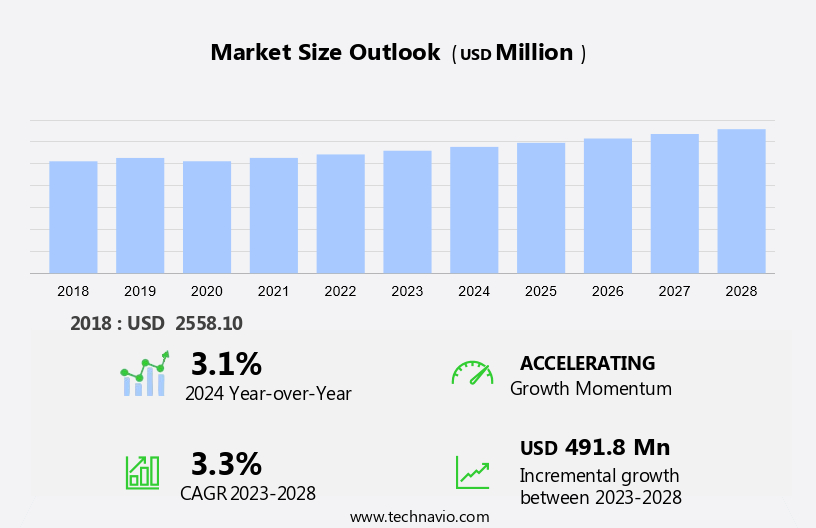

The hydrodesulfurization catalysts market size is forecast to increase by USD 491.8 million at a CAGR of 3.3% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing demand for ultra-low sulfur diesel (ULSD) and ultra-low sulfur fuel oil (ULSFO) to mitigate the environmental impact of sulfur dioxide (SO2) emissions, which contribute to heart diseases, respiratory diseases, and lung cancer. Stringent regulations mandate the reduction of sulfur content in naphtha, petrol, gasoline, kerosene, and diesel to meet emission standards. The HDS process utilizes hydrogen and cobaltâmolybdenum catalysts to remove sulfur from these fuels. However, the high cost of HDS technology remains a challenge for market growth. In the US, the Environmental Protection Agency (EPA) sets the sulfur content limit for diesel fuel at 15 parts per million (ppm), and the American Petroleum Institute (API) sets the limit for gasoline at 10 ppm. As the demand for cleaner fuels continues to rise, the HDS catalysts market is expected to witness steady growth.

What will be the Size of the Market During the Forecast Period?

- The hydrodesulfurization (HDS) catalyst market plays a crucial role in reducing major air pollutants from petroleum refineries and various industries. HDS catalysts are essential components in the hydrotreating process, which is used to remove sulfur compounds from petroleum distillates and natural gas. Air pollution, a significant environmental concern, is primarily caused by the combustion of fossil fuels in various devices, including motor vehicles and industrial facilities. Major air pollutants, such as ozone (O3), carbon monoxide (CO), and nitrogen dioxide (NO2), contribute to smog, acid rain, and other health issues. To mitigate these environmental concerns, stringent sulfur emission regulations have been imposed on petroleum refineries and industries. The production of cleaner automotive fuels, such as low-sulfur fuels and ultra-low sulfur (ULS) fuels, has become a priority. Hydrodesulfurization catalysts are instrumental in achieving these goals. Hydrodesulfurization catalysts are employed in the refining of various petroleum products, including gasoline, diesel fuel, jet fuel, marine fuels, and heating oils. These catalysts facilitate the removal of sulfur compounds, resulting in the production of cleaner fuels that meet the sulfur emission regulations. Ruthenium disulfide (Rus2) and catalysts containing cobalt and molybdenum are commonly used hydrodesulfurization catalysts.

- The hydrotreating process, which involves the reaction of hydrogen and the feedstock in the presence of a catalyst, effectively removes sulfur from the feedstock. The HDS catalyst market is driven by the increasing demand for low-sulfur fuels and the need to comply with sulfur emission regulations. Natural gas processing is also a significant application area for hydrodesulfurization catalysts, as natural gas often contains sulfur compounds that need to be removed before it can be used as a clean fuel source. In conclusion, the hydrodesulfurization catalyst market plays a vital role in addressing air pollution by enabling the production of cleaner fuels from petroleum refineries and natural gas processing facilities. The demand for hydrodesulfurization catalysts is expected to grow as stricter sulfur emission regulations are implemented and the need for cleaner fuels continues to increase.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

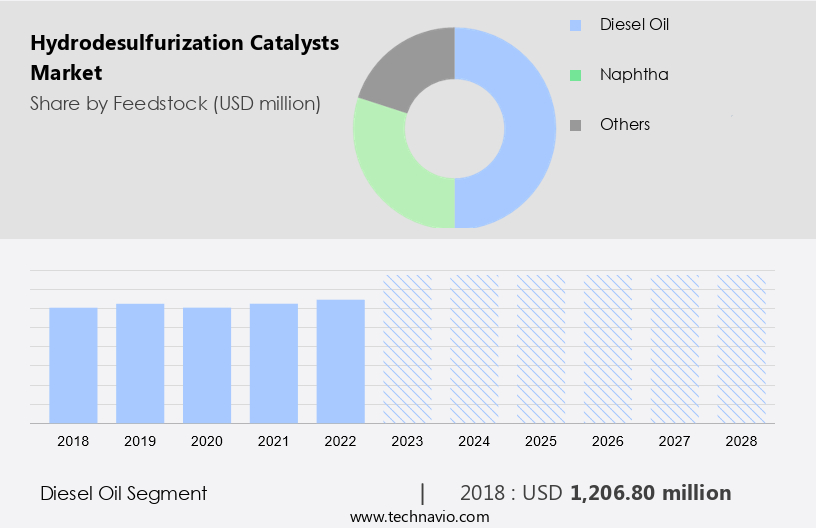

- Feedstock

- Diesel oil

- Naphtha

- Others

- Geography

- North America

- Canada

- US

- APAC

- China

- Europe

- Germany

- Italy

- South America

- Middle East and Africa

- North America

By Feedstock Insights

- The diesel oil segment is estimated to witness significant growth during the forecast period.

Hydrodesulfurization (HDS) is a critical process in refining liquid oil fractions to eliminate impurities, including sulfur, metals, oxygen, and nitrogen. Hydrodesulfurization catalysts play a pivotal role in this process. The growing emphasis on renewable energy and sustainable transportation has led to stricter regulations on air quality, driving the demand for hydrodesulfurization catalysts. In particular, the hydrotreating process is extensively used for sulfur removal in natural gas processing, producing low-sulfur fuels such as ultra-low sulfur (ULS) diesel, marine fuels, heating oils, and jet fuels. The US, Canada, the UK, Germany, and France are among the countries implementing regulations to control sulfur emissions from transportation fuels.

Get a glance at the market report of share of various segments Request Free Sample

The diesel oil segment was valued at USD 1.21 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

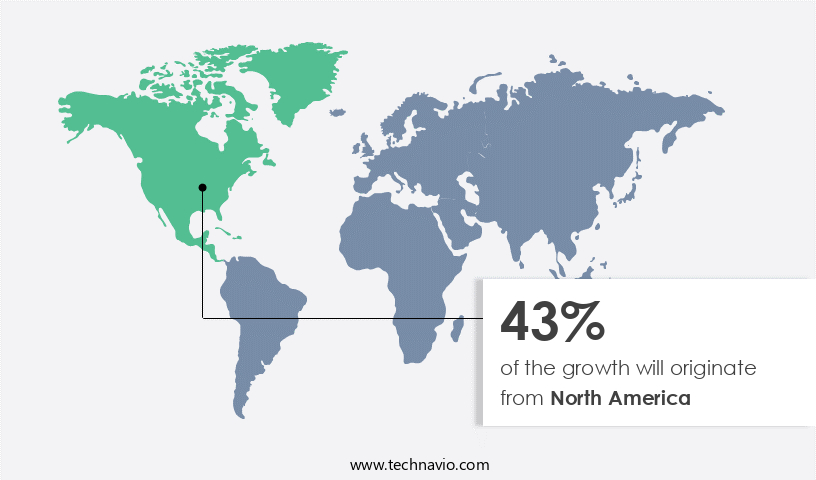

- North America is estimated to contribute 43% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The hydrodesulfurization (HDS) catalysts market in North America is anticipated to experience substantial growth due to rigorous environmental regulations and the increasing demand for ultralow sulfur fuels. In the US, the Environmental Protection Agency (EPA) enforced stricter regulations on emissions through the National Ambient Air Quality Standards (NAAQS) for greenhouse gases in 2015. These regulations are driving the need for HDS catalysts, which help in improving engine efficiency, reducing greenhouse gas emissions, and removing organic sulfur compounds from fuels such as natural gas, gasoline, jet fuel, and fuel oils. Furthermore, the automotive sector in North America is expanding, with a focus on producing lightweight, high-performance, and fuel-efficient vehicles. The rising automotive production in this region is expected to fuel the demand for hydrodesulfurization catalysts, particularly platinum catalysts, which are widely used in diesel desulfurization processes to produce high octane gasoline.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Hydrodesulfurization Catalysts Market?

Stringent regulations concerning environmental pollution is the key driver of the market.

- In response to stringent emissions regulations set by the European Commission (EC) and US Environmental Protection Agency (EPA), the transportation industry in the US and Europe is focusing on reducing fuel sulfur content. The EC enacted Directive 2008/50/EC to ensure cleaner air and ambient quality in Europe, while the US adheres to the 40 Code of Federal Regulations (CFR) 79 for fuel additive registration. These regulations mandate that any fuel additive should not exceed a sulfur content of 15 parts per million (ppm) by weight in the fuel at a concentration below or equal to 0. The US EPA and European regulations ensure that fuel additives meet these standards to minimize sulfur emissions.

What are the market trends shaping the Hydrodesulfurization Catalysts Market?

Increasing demand for ULSD is the upcoming trend in the market.

- In the realm of cleaner energy and reduced emissions, the utilization of Ultra Low Sulfur Diesel (ULSD) has gained significant traction. ULSD, a refined diesel fuel with sulfur content as low as 15 parts per million (ppm), plays a crucial role in decreasing harmful exhaust emissions from diesel engines. This reduction in emissions, in conjunction with emission control devices in both on-road and off-road vehicles, brings exhaust gases comprised of particulate matter and ozone precursors close to zero levels. The adoption of ULSD has resulted in over 90% reduction in emissions from these vehicles. Furthermore, ULSD necessitates the addition of fuel additives, including cetane improvers, antioxidants, and corrosion inhibitors.

- The implementation of ULSD not only improves overall engine performance but also plays a vital role in mitigating health concerns, such as heart diseases, respiratory diseases, and lung cancer, associated with high sulfur diesel emissions. Sulfur dioxide (SO2), a primary component of these emissions, is a known contributor to these health issues. Catalysts, specifically hydrodesulphurisation (HDS) catalysts, play a pivotal role in the refining process of diesel fuel to produce ULSD. These catalysts, primarily made of cobalt-molybdenum, hydrogenate and remove sulfur compounds, resulting in the production of cleaner diesel fuel.

What challenges does Hydrodesulfurization Catalysts Market face during the growth?

The high cost of technology is a key challenge affecting the market growth.

- The implementation of stricter regulations against air pollution has led to an increased focus on Hydrodesulfurization (HDS) in various industries, including petroleum refineries and motor vehicles. Major air pollutants, such as ozone (O3), carbon monoxide (CO), and nitrogen dioxide (NO2), are significant contributors to environmental degradation and health concerns. HDS plays a crucial role in reducing these pollutants by removing sulfur from fuels. However, the production and distribution of sulfur-free fuels come with a higher cost compared to traditional fuels.

- Petroleum refineries face substantial capital expenses for upgrading existing HDS units, purchasing precious metal catalysts, and installing new HDS units to adhere to sulfur regulations. Moreover, transportation operations necessitate investments for efficient fuel transportation to customers. Collectively, these factors contribute to the elevated prices of sulfur-free fuels, potentially hindering their widespread adoption and, subsequently, the growth of the market during the forecast period.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albemarle Corp.

- Arkema

- ART advanced refractory technologies GmbH

- Axens

- BASF SE

- Clariant International Ltd

- Dorf Ketal Chemicals I Pvt. Ltd.

- Exxon Mobil Corp.

- Honeywell International Inc.

- IFP Energies nouvelles

- JGC Holdings Corp.

- Johnson Matthey Plc

- KNT Group

- PetroChina Co. Ltd.

- Shell plc

- Sie Neftehim LLC

- Sinopec Shanghai Petrochemical Co. Ltd.

- Topsoes AS

- UNICAT Catalyst Technologies LLC

- W. R. Grace and Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Hydrodesulfurization (HDS) is a critical process used in petroleum refineries and natural gas processing to remove major air pollutants, including hydrogen sulfide (H2S), sulfur dioxide (SO2), and organic sulfur compounds. These pollutants contribute to air pollution, leading to health issues such as heart diseases, respiratory diseases, and lung cancer. HDS plays a significant role in producing sulfur-free fuels for combustion devices, including motor vehicles, industrial facilities, and marine vessels. The hydrotreating process employs noble metal catalysts, such as cobaltâmolybdenum, nickel, ruthenium, and tungsten, to facilitate the conversion of sulfur-containing compounds into hydrogen sulfide. This process is essential for the production of cleaner automotive fuels like sulfur-free diesel, ultra-low-sulfur diesel (ULSD), and sulfur-free petrochemicals.

HDS also contributes to the Green Deal and climate change initiatives by reducing sulfur emissions and promoting sustainable transportation. The hydrodesulfurization catalyst market is driven by stringent emission reduction regulations and the increasing demand for low-sulfur fuels, including ULS and ULS diesel. The market also caters to the needs of various industries, including natural gas processing, petroleum refineries, and marine fuels, to produce cleaner fuels and heating oils. The hydrotreating process is also used to desulfurize jet fuels and gasoline to meet the growing demand for cleaner fuels and address environmental concerns. The hydrodesulfurization process is a crucial step in refinery processes to produce high octane gasoline and platinum catalysts for diesel desulfurization.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

140 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.3% |

|

Market growth 2024-2028 |

USD 491.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.1 |

|

Key countries |

US, China, Germany, Canada, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -