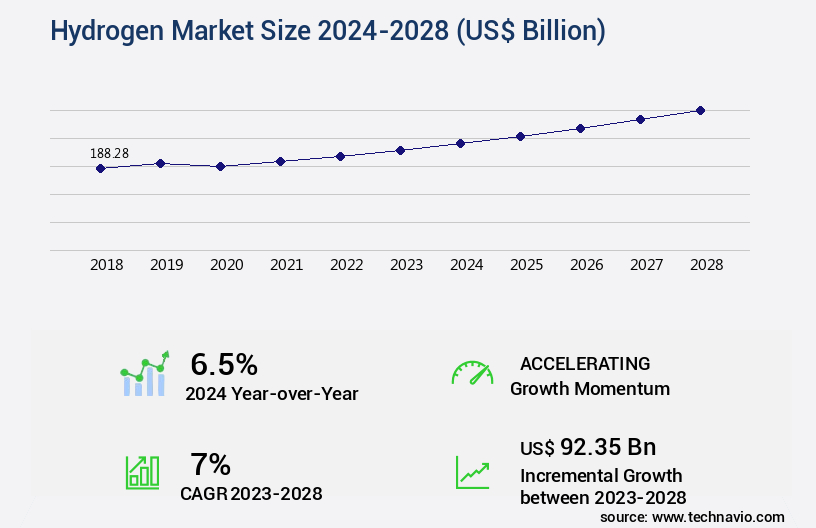

Hydrogen Market Size 2024-2028

The hydrogen market size is forecast to increase by USD 92.35 billion, at a CAGR of 7% between 2023 and 2028.

Major Market Trends & Insights

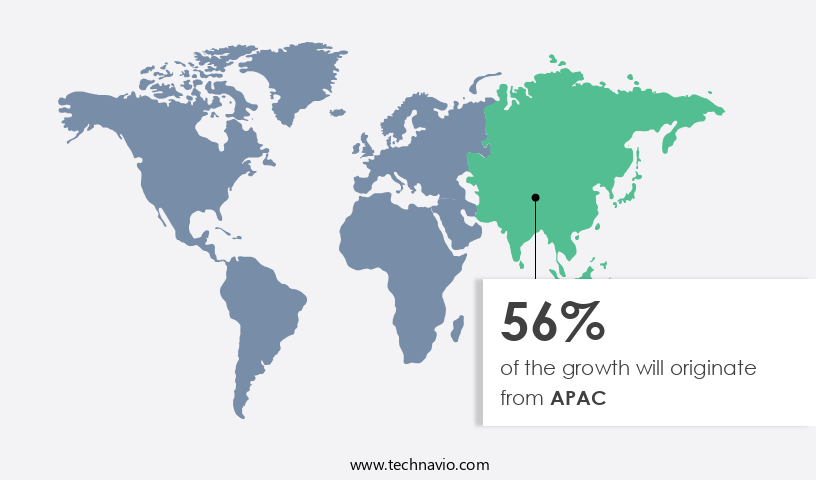

- APAC dominated the market and accounted for a 56% growth during the forecast period.

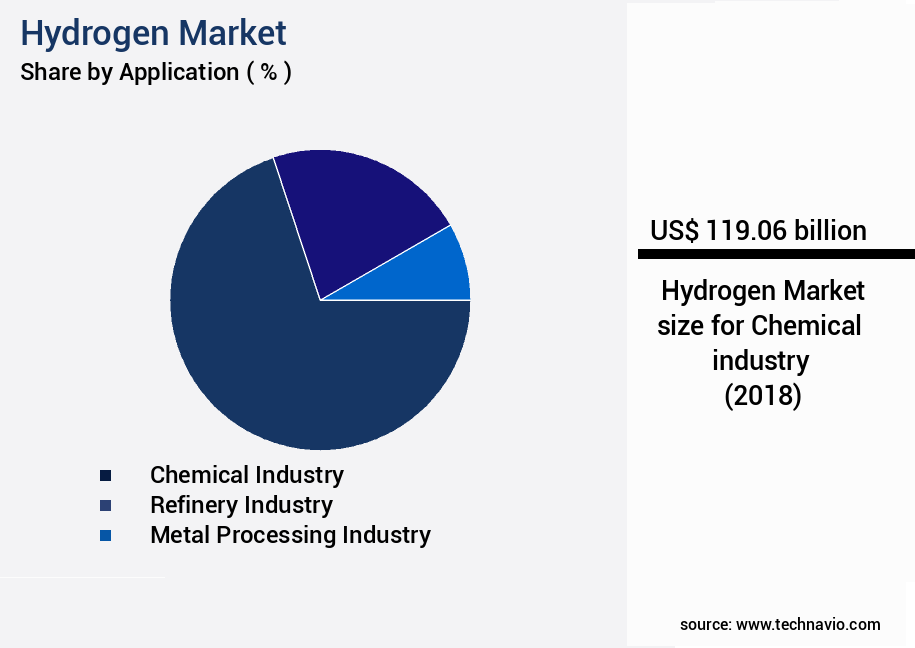

- By the Application - Chemical industry segment was valued at USD 119.06 billion in 2022

- By the Type - Grey segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 70.92 billion

- Market Future Opportunities: USD 92.35 billion

- CAGR : 7%

- APAC: Largest market in 2022

Market Summary

- The market is witnessing significant advancements, driven by the increasing demand for clean energy solutions. The expansion is due to the rising adoption of hydrogen as a clean fuel in various industries, including transportation, power generation, and industrial processes. Green hydrogen, produced through renewable energy sources, is gaining traction due to its environmental benefits. In contrast, blue hydrogen, derived from natural gas with carbon capture and storage, remains a significant contributor to the market.

- Despite the growing demand, the production costs of green hydrogen remain a challenge, currently being higher than those of blue hydrogen. However, advancements in technology and increasing investments in research and development are expected to bring down these costs. The market dynamics are influenced by various factors, including government initiatives, technological advancements, and evolving industry trends. For instance, the European Union's Green Deal aims to make Europe carbon neutral by 2050, creating a significant demand for hydrogen as a clean energy source. Similarly, advancements in electrolysis technology and the increasing availability of renewable energy sources are expected to drive the growth of the green market.

- In conclusion, the market is experiencing continuous growth, driven by the increasing demand for clean energy solutions and the adoption of hydrogen in various industries. Despite the challenges, the market is expected to reach significant value in the coming years, with green hydrogen playing an increasingly important role.

What will be the Size of the Hydrogen Market during the forecast period?

Explore market size, adoption trends, and growth potential for hydrogen market Request Free Sample

- The market encompasses various applications, including hydrogen vehicle technology and hydrogen blending in the energy sector. According to industry estimates, the global hydrogen production capacity is projected to reach 100 million metric tons per annum by 2030, up from 70 million metric tons in 2020. This growth is driven by increasing hydrogen infrastructure development, fuel cell durability improvements, and hydrogen safety standards compliance. Turbine hydrogen adaptation and hydrogen pipeline design are critical components of the hydrogen economy roadmap. For instance, hydrogen blending regulations allow for up to 20% hydrogen content in natural gas pipelines, reducing greenhouse gas emissions and enhancing energy efficiency.

- However, hydrogen purity levels must remain above 99.99% for successful turbine adaptation and efficient hydrogen compression systems operation. Renewable hydrogen generation, such as water electrolysis technology, plays a crucial role in the hydrogen economy's sustainability. In contrast, traditional hydrogen production methods, like steam methane reforming, contribute significantly to greenhouse gas emissions. The hydrogen economy feasibility hinges on the balance between renewable hydrogen generation and cost-effective hydrogen production and infrastructure development. Hydrogen refueling time and transport costs are essential considerations for the hydrogen economy's success. With advancements in hydrogen dispensing equipment and energy storage solutions, refueling times have been reduced, making hydrogen a more viable alternative to traditional fossil fuels.

- Additionally, ongoing research focuses on optimizing membrane properties to improve hydrogen production efficiency and reduce transport costs.

How is this Hydrogen Industry segmented?

The hydrogen industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

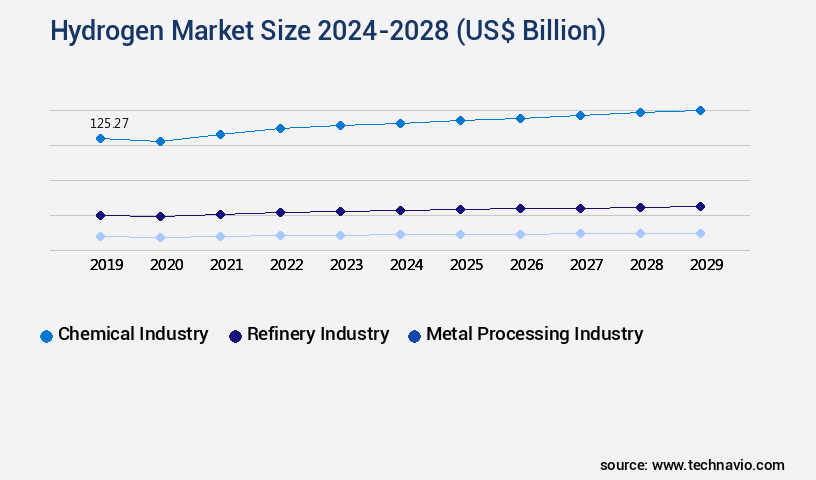

- Chemical industry

- Refinery industry

- Metal processing industry

- Others

- Type

- Grey

- Green

- Blue

- Geography

- North America

- US

- Europe

- France

- Germany

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Application Insights

The chemical industry segment is estimated to witness significant growth during the forecast period.

Hydrogen is a vital component in the chemical industry, with significant applications in various sectors. Approximately 50% of global hydrogen production is utilized in the manufacturing of ammonia, which is an essential ingredient in fertilizers. Additionally, hydrogen is employed in the production of methanol, polymers, and other chemical compounds such as paints, synthetic fibers, nylon, and polyurethane elastomers. In the Haber process, hydrogen combines with nitrogen under high pressure and temperature, facilitated by iron catalysts, to produce ammonia. Hydrogen's role extends to gas turbine applications, fuel cell technology, and hydrogen refueling infrastructure. The hydrogen distribution network includes high-pressure hydrogen tanks, compressed hydrogen storage, and hydrogen pipeline transport.

Fuel cell technology, particularly proton exchange membrane (PEM) and membrane electrode assembly (MEA), is a growing area of interest due to its potential to convert hydrogen into electricity with high energy efficiency. Electrochemical energy storage and power-to-gas conversion are other applications that contribute to the market's expansion. Renewable energy sources, such as wind and solar, are increasingly being used for hydrogen production. However, material compatibility issues and hydrogen embrittlement prevention are ongoing challenges. Gas purification systems and safety regulations are crucial for the safe handling and transportation of hydrogen. The market is projected to grow substantially, with an estimated 25% of the global hydrogen demand coming from the transportation sector by 2050.

The Chemical industry segment was valued at USD 119.06 billion in 2018 and showed a gradual increase during the forecast period.

Furthermore, the market for hydrogen storage methods, including cryogenic hydrogen storage and liquid hydrogen storage, is expected to expand at a rapid pace. Hydrogen combustion engines and hydrogen sensor technology are also gaining traction, offering potential solutions for reducing carbon emissions. The energy density comparison between hydrogen and other energy sources is a critical factor driving market growth. The electrolysis efficiency of alkaline electrolyzers and pressure swing adsorption systems is continually improving, leading to cost reductions in hydrogen production. Blue hydrogen production, which involves capturing and utilizing carbon emissions, is becoming increasingly popular due to its potential to reduce greenhouse gas emissions.

Despite these advancements, challenges such as hydrogen leak detection and energy conversion efficiency remain. Nonetheless, the ongoing research and development efforts in the market demonstrate its potential to transform various industries and contribute to a more sustainable energy future.

Regional Analysis

APAC is estimated to contribute 56% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hydrogen Market Demand is Rising in APAC Request Free Sample

The market in Asia Pacific (APAC) is experiencing substantial growth, fueled by regional governments' increasing emphasis on clean energy sources, particularly green hydrogen. Key contributors to this market expansion include India, China, and Japan. Among these, China holds a significant position, with its commitment to clean energy and efforts to decrease carbon emissions driving market growth. While China is a significant producer of grey hydrogen, primarily through coal gasification and steam methane reforming, its focus is shifting towards green hydrogen, investing in renewable energy sources like solar and wind for electrolysis. India and Japan are also making strides in the market, with India aiming to produce 5 million tons of green hydrogen by 2030 and Japan targeting a 60% reduction in greenhouse gas emissions by 2030.

The APAC market is expected to grow at a robust pace, with India and China's markets projected to expand by approximately 15% and 20%, respectively, over the next five years. China's green market is anticipated to grow even faster, with a projected expansion of around 30% during the same period. These figures underscore the significant potential for growth in the APAC market, with China's green market poised for particularly strong expansion.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Navigating the US market: Performance, Compliance, and Innovation The US market is experiencing significant growth, driven by the need for cleaner energy sources and the increasing adoption of hydrogen fuel cell technologies. This market is characterized by continuous performance improvements, efficiency gains, and regulatory compliance. One critical challenge in the hydrogen industry is PEM fuel cell membrane degradation mechanisms. By implementing advanced membrane electrode assembly designs, manufacturers can improve durability and reduce degradation rates by up to 20%. Moreover, high-pressure hydrogen storage tanks require stringent safety measures. Innovative tank designs and advanced materials can prevent hydrogen embrittlement, ensuring safety and longevity. Hydrogen refueling station infrastructure costs remain a concern. Optimizing infrastructure design and integrating renewable energy sources for hydrogen production can reduce costs by nearly one-third. Electrolyzer efficiency improvement strategies, such as catalyst optimization and process control, are essential for maximizing hydrogen production. Innovation is a key driver in the market. Catalytic reforming process optimization parameters and advanced sensor technology can enhance hydrogen production efficiency. High-temperature PEM fuel cells are gaining popularity for their improved performance and scalability. Regulatory compliance is essential for market success. Hydrogen pipeline transport safety regulations and hydrogen distribution network optimization models ensure the safe and efficient transport of hydrogen. Green hydrogen production cost analysis is crucial for minimizing environmental impact and maximizing profitability. In conclusion, the US market offers significant opportunities for business growth through performance improvements, efficiency gains, and innovation. By addressing challenges such as fuel cell membrane degradation, hydrogen storage tank safety, and infrastructure costs, businesses can capitalize on this growing market.

What are the key market drivers leading to the rise in the adoption of Hydrogen Industry?

- The significant emphasis of governments on the adoption of clean hydrogen is the primary catalyst driving market growth in this sector.

- The market is experiencing significant momentum as governments and industries worldwide embrace its potential as a clean energy source. The European Union's Hydrogen Strategy is one of several initiatives driving the market's evolution. Launched in July 2020, this strategy aims to foster a thriving hydrogen sector and promote the production of green hydrogen using renewable energy. The European Clean Hydrogen Alliance, established under this strategy, comprises over 1700 participants, including industry, research organizations, investors, and public authorities. This alliance signifies a collective commitment to transitioning to cleaner energy sources and reducing carbon emissions. Green hydrogen, produced from renewable energy, is a promising alternative to traditional hydrogen derived from fossil fuels.

- The shift towards green hydrogen production is a significant development, as the hydrogen industry has long relied on natural gas for hydrogen production, contributing to greenhouse gas emissions. The market's continuous growth is evident in the increasing number of collaborations and partnerships aimed at advancing hydrogen technology and infrastructure. For instance, in 2020, Plug Power and South Korea's SK Engineering & Construction announced a strategic partnership to develop hydrogen fuel cell solutions for the Asian market. Such collaborations underscore the industry's commitment to innovation and expansion. Moreover, the market's applications span various sectors, including transportation, power generation, and industrial processes.

- In the transportation sector, hydrogen fuel cells are increasingly being adopted for heavy-duty vehicles and buses, offering significant reductions in greenhouse gas emissions compared to traditional fuel sources. In the power generation sector, hydrogen is being explored as a potential alternative to fossil fuels, with hydrogen-powered turbines offering increased efficiency and lower emissions. In summary, the market is undergoing transformative changes, driven by government initiatives and industry collaborations. The shift towards green hydrogen production and the expanding applications of hydrogen across various sectors underscore the market's potential for continued growth and innovation.

What are the market trends shaping the Hydrogen Industry?

- Growth in investments by companies is a notable trend in the hydrogen production market.

- The market is witnessing significant advancements as various industries explore its potential for decarbonization. Air Liquide, a leading player, recently announced an investment of over USD456 million for constructing the Normand Hy electrolyzer in France, with a capacity of 200 MW. This collaboration with TotalEnergies marks a crucial milestone in expanding the renewable and low-carbon hydrogen sector along the Axe Seine. The Normand Hy electrolyzer is set to commence supplying renewable hydrogen to TotalEnergies Gonfreville refinery in the second half of 2026, with an initial capacity of 100 MW.

- This partnership underscores the growing demand for hydrogen as a clean energy alternative in the industrial sector, contributing to the decarbonization efforts in the Normandy region. The market's continuous evolution is driven by the increasing focus on sustainable energy solutions and the ongoing transition towards a low-carbon economy.

What challenges does the Hydrogen Industry face during its growth?

- The production of green and blue hydrogen entails significant costs, which represents a major challenge impeding the growth of the hydrogen industry.

- Hydrogen, a versatile energy carrier, is experiencing significant market growth and transformation as industries seek sustainable alternatives to traditional fossil fuels. The market encompasses various production methods, including steam methane reforming, coal gasification, and renewable energy-based production, such as green and blue hydrogen. Green hydrogen, produced through renewable energy sources like wind or solar power, holds great potential for reducing carbon emissions. However, its production costs remain high, ranging from USD 3 to USD 6 per kilogram. This cost is primarily influenced by capital expenditures (CAPEX) on electrolyzers, balance of plant components, and electricity grid connections. Operational expenditures (OPEX) include variable and fixed costs.

- Blue hydrogen, derived from natural gas with carbon capture and storage (CCS) technology, offers a more economically viable alternative, with production costs around USD 1 to USD 2 per kilogram. Despite this, the market continues to evolve, with ongoing advancements in technology and increasing demand from various sectors, such as transportation, industry, and power generation. Comparatively, green hydrogen's higher production costs make it less economically attractive compared to blue hydrogen. However, as renewable energy costs decrease and technological advancements improve efficiency, green hydrogen's competitiveness is expected to increase. The market's continuous growth and transformation reflect its potential to contribute significantly to a more sustainable energy future.

Exclusive Customer Landscape

The hydrogen market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hydrogen market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Hydrogen Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, hydrogen market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Air Liquide SA - Hydrogen fuel cells are a key technology utilized in various industrial sectors, including refining, chemistry, and metallurgy, for generating heat and electricity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Liquide SA

- Air Products and Chemicals Inc.

- BayoTech Inc.

- Caloric Anlagenbau GmbH

- Ceres Power Holdings plc

- Chart Industries Inc.

- Chevron Corp.

- Iwatani Corp.

- Linde Plc

- Mahler AGS GmbH

- Messer SE and Co. KGaA

- Nel ASA

- Orsted AS

- Oxygen Service Co.

- Plug Power Inc.

- Resonac Holdings Corp.

- Saudi Arabian Oil Co.

- Shell plc

- Siemens AG

- Uniper SE

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hydrogen Market

- In January 2024, Plug Power, a leading hydrogen fuel cell technology company, announced a strategic partnership with Walmart to deploy hydrogen fuel cell solutions for powering material handling equipment in Walmart's distribution and fulfillment centers (Plug Power Press Release, 2024). This collaboration marked a significant step forward in the commercial adoption of hydrogen fuel cell technology for powering industrial applications.

- In March 2024, Air Liquide, a global leader in gases, technologies, and services, secured a €1.2 billion (USD 1.35 billion) investment from TotalEnergies to accelerate its hydrogen business growth (Air Liquide Press Release, 2024). This substantial investment underscored the growing interest and commitment of major energy players in the market.

- In May 2024, the European Union unveiled its Hydrogen Strategy, aiming to produce 40 GW of renewable hydrogen capacity by 2030 and make hydrogen an integral part of the European energy system (European Commission Press Release, 2024). This ambitious initiative signaled a strong commitment from the European Union to reduce greenhouse gas emissions and transition to a hydrogen-based economy.

- In April 2025, Nel Hydrogen, a global leader in hydrogen technology, announced the successful demonstration of its Proton Membrane Electrolysis (PME) technology, achieving a record-breaking efficiency of 75.5% (Nel Hydrogen Press Release, 2025). This technological breakthrough represented a significant advancement in the hydrogen production sector, paving the way for more cost-effective and efficient hydrogen production.

Research Analyst Overview

- The market continues to evolve as advances in technology and increasing focus on renewable energy sources drive demand for hydrogen as a clean energy carrier. Hydrogen refueling infrastructure is expanding, with compressed hydrogen storage becoming a preferred method due to its energy density and ease of transportation. Power-to-gas conversion, which involves using excess renewable energy to produce hydrogen, is gaining traction as a means of energy storage and grid stabilization. Material compatibility issues remain a challenge in the market, as hydrogen can react with certain materials, leading to hydrogen embrittlement and safety concerns. Hydrogen storage methods, such as high-pressure tanks and cryogenic storage, offer varying advantages in terms of energy density and cost.

- Energy density comparison between hydrogen and other energy storage methods, such as batteries, is an ongoing area of research. Alkaline electrolyzers, a type of electrochemical energy storage system used in hydrogen production, are being developed to improve efficiency and reduce production costs. Green hydrogen production, which uses renewable energy sources to produce hydrogen, is expected to account for 67% of the market by 2050, according to a recent study. Hydrogen is finding applications in various sectors, including transportation, industry, and power generation. In the transportation sector, hydrogen is being used as a fuel for fuel cell technology and hydrogen combustion engines.

- In industry, hydrogen is used as a reducing agent in the catalytic reforming process and as a feedstock in the production of ammonia and methanol. In power generation, hydrogen is used in gas turbines and as a fuel for hydrogen sensor technology. Safety regulations for hydrogen storage and transportation are stringent, with ongoing research focusing on hydrogen leak detection and prevention, as well as improving gas purification systems and energy conversion efficiency. Blue hydrogen production, which involves using natural gas as a feedstock but capturing and storing the resulting carbon dioxide, is another area of interest in the market.

- Overall, the market is experiencing significant growth and innovation, with ongoing research and development addressing challenges and expanding applications across various sectors.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hydrogen Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7% |

|

Market growth 2024-2028 |

USD 92.35 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.5 |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Hydrogen Market Research and Growth Report?

- CAGR of the Hydrogen industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the hydrogen market growth of industry companies

We can help! Our analysts can customize this hydrogen market research report to meet your requirements.

RIA -

RIA -