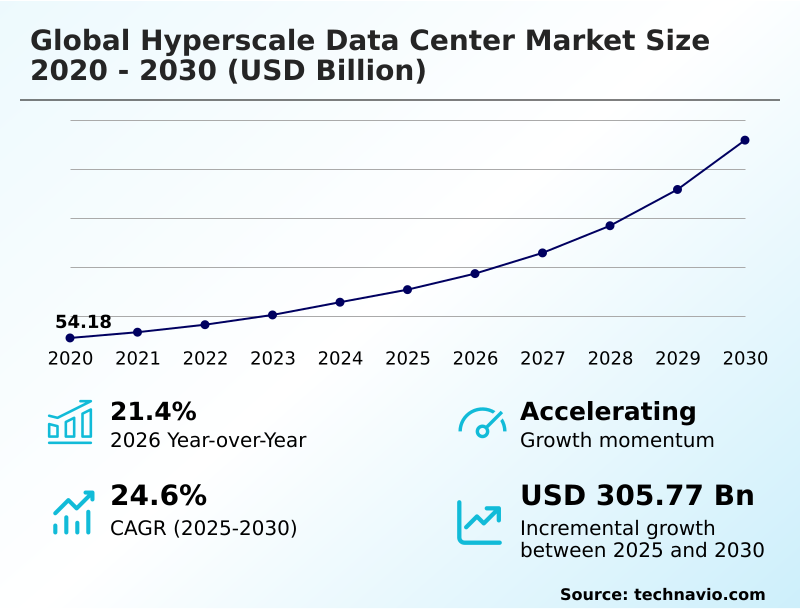

Hyperscale Data Center Market Size 2026-2030

The hyperscale data center market size is valued to increase by USD 305.77 billion, at a CAGR of 24.6% from 2025 to 2030. Exponential demand for generative AI workloads will drive the hyperscale data center market.

Major Market Trends & Insights

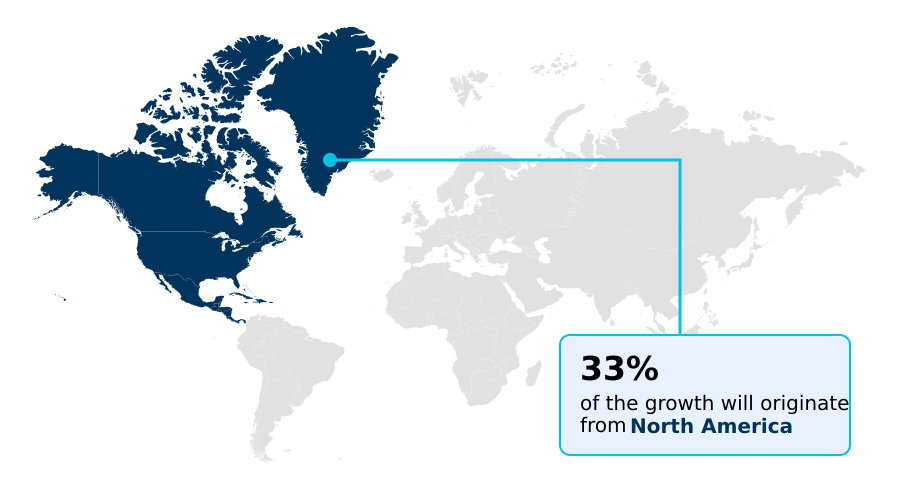

- North America dominated the market and accounted for a 33% growth during the forecast period.

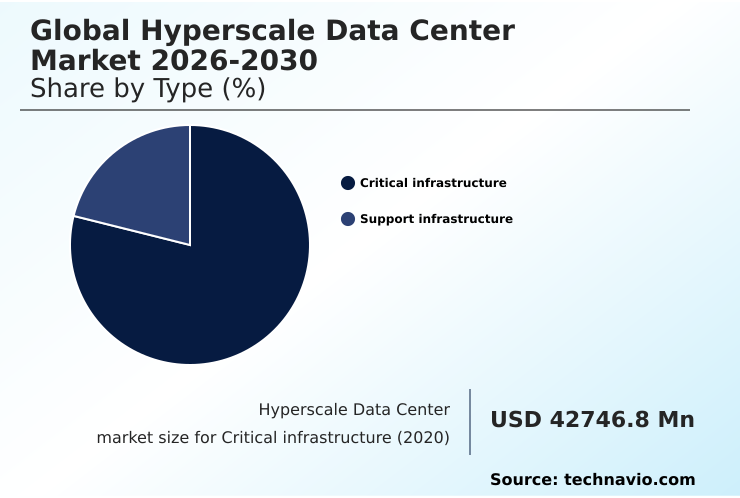

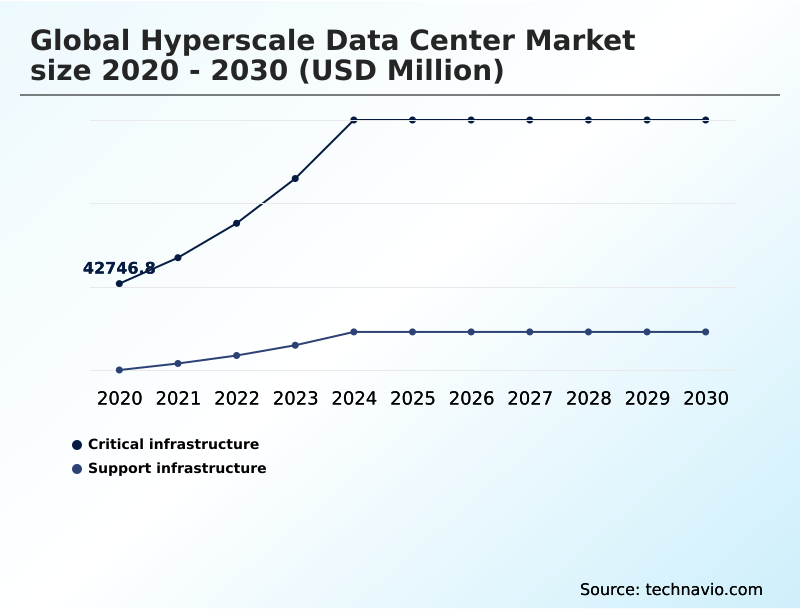

- By Type - Critical infrastructure segment was valued at USD 102.06 billion in 2024

- By End-user - BFSI segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 404.61 billion

- Market Future Opportunities: USD 305.77 billion

- CAGR from 2025 to 2030 : 24.6%

Market Summary

- The hyperscale data center market is undergoing a profound transformation, moving beyond traditional cloud services to become the engine of the AI revolution. This shift is driven by the need for high-performance computing clusters capable of training and deploying complex large language models.

- A key dynamic is the growing enforcement of data residency laws, compelling operators to build sovereign cloud regions that comply with national regulations. For instance, a global logistics firm must now utilize localized hyperscale infrastructure to process real-time IoT data from its fleet, ensuring compliance while optimizing supply chain efficiency.

- Simultaneously, sustainability has become a critical operational mandate, pushing the industry toward carbon-free energy sources and innovative designs like waste-heat recovery systems. These facilities are no longer just real estate assets; they are advanced, automated factories for computation, balancing immense power demands with environmental responsibility.

- The convergence of these forces is reshaping site selection, facility design, and the very economics of digital infrastructure, making it a critical bottleneck and value driver in the modern economy.

What will be the Size of the Hyperscale Data Center Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Hyperscale Data Center Market Segmented?

The hyperscale data center industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Critical infrastructure

- Support infrastructure

- End-user

- BFSI

- Energy

- IT

- Others

- Capacity

- 10-50 MW

- 50-100 MW

- Above 100 MW

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- UK

- Germany

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of World (ROW)

- North America

By Type Insights

The critical infrastructure segment is estimated to witness significant growth during the forecast period.

The critical infrastructure segment is fundamentally evolving, driven by the intense demands of AI workload optimization. Legacy server designs are being supplanted by rack-scale integrated systems that combine graphical processing units, specialized accelerators, and data processing units into cohesive clusters.

This architectural shift, essential for generative AI infrastructure and other mission-critical workloads, supports advanced networking fabrics like 800-gigabit ethernet, which is crucial for preventing data bottlenecks. The use of custom server rail kits facilitates the deployment of these high-density configurations.

These new architectures are delivering up to a 40% improvement in data throughput, enabling organizations to accelerate complex computations and gain a competitive edge. This transformation underscores a market-wide move toward specialized, high-performance hardware designed for the AI era.

The Critical infrastructure segment was valued at USD 102.06 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Hyperscale Data Center Market Demand is Rising in North America Get Free Sample

The geographic landscape of the hyperscale data center market is undergoing significant diversification, driven by power constraints in primary hubs and the strategic need for global connectivity nodes.

While North America continues to lead, contributing 33% of the incremental growth, APAC is a close second at 31.48%, fueled by rapid digital transformation.

This trend is compelling operators to pursue secondary market expansion into regions with available power and land.

The deployment of new subsea cable systems is also opening fresh corridors, supporting tier 2 market growth and enabling cloud-native architectures in previously underserved areas.

This decentralization addresses data localization mandates and improves low-latency delivery, which is essential for digital sovereignty requirements and the proliferation of edge integration. Strategic investments in these new regions are critical for building network resilience and tapping into high-growth economies.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Analyzing the global hyperscale data center market 2026-2030 drivers reveals that the impact of generative AI on facility design is the foremost catalyst, compelling a complete re-evaluation of power and cooling.

- The global hyperscale data center market 2026-2030 trends point toward sustainable energy in hyperscale data centers, with a notable rise in agreements for nuclear energy for AI data centers to ensure stable, carbon-free power. However, the global hyperscale data center market 2026-2030 challenges are significant, as power grid constraints on data center construction create multi-year delays.

- The construction cost for AI-ready facilities is escalating, reflecting the complexity of integrating high-performance networking for AI clusters and advanced cooling. Examining direct-to-chip vs immersion cooling trade-offs has become standard, with facilities engineered for these technologies showing divergent operational expenditures; some achieve double-digit percentage point improvements in power usage effectiveness over legacy designs.

- AI inference server high density requirements necessitate liquid cooling for high performance compute. Furthermore, data sovereignty impact on cloud architecture is driving investment in sovereign cloud security and compliance protocols and modular data centers for edge computing, especially to comply with data residency laws in the European Union.

- This is fueling emerging markets hyperscale data center investment, where subsea cable impact on regional connectivity is unlocking new potential. Meanwhile, practices like waste heat reuse in urban data centers and the use of battery storage systems for grid stability are becoming crucial for obtaining operational licenses.

What are the key market drivers leading to the rise in the adoption of Hyperscale Data Center Industry?

- The exponential demand for generative AI workloads serves as the primary engine propelling market expansion.

- The market's primary driver is the insatiable demand for generative AI workloads, which is compelling a shift toward an AI factory design.

- This requires facilities to support high-density power racks and advanced cooling, as generative AI infrastructure increases power density requirements by up to 10x compared to traditional workloads.

- A second powerful driver is the rise of sovereign cloud and data localization mandates, which has spurred a 40% increase in regional data center construction to meet digital sovereignty requirements. This trend transforms data centers into critical national security infrastructure.

- Lastly, rapid digital transformation in emerging economies is fueling secondary market expansion. The move to cloud-native architectures in these regions, combined with new subsea cable systems, is creating a self-reinforcing cycle of digital ecosystem growth.

What are the market trends shaping the Hyperscale Data Center Industry?

- The proliferation of generative AI and high-density compute clusters is reshaping infrastructure requirements. This shift drives a fundamental redesign of facilities to accommodate unprecedented power and cooling demands.

- Key trends are reshaping the global hyperscale data center market, led by the transition to sustainable energy and advanced thermal management. To meet carbon-neutrality goals, operators are implementing closed-loop liquid cooling systems and dry cooling technologies, with the adoption of liquid cooling services reducing water usage by over 90% in new builds.

- This focus on environmental stewardship is coupled with the strategic decentralization of footprints to address digital sovereignty requirements. The construction of modular data center designs in new regions ensures compliance with data localization mandates and supports low-latency delivery. This approach has been shown to cut time-to-market for new capacity by up to 25%.

- These shifts in AI factory design ensure that modern infrastructure is resilient, efficient, and aligned with both regulatory pressures and performance demands for generative AI infrastructure.

What challenges does the Hyperscale Data Center Industry face during its growth?

- Escalating power scarcity and prolonged grid interconnection delays present the most significant challenge to market growth.

- The most formidable challenge is escalating power scarcity, as grid interconnection delays have extended project timelines by an average of 18-24 months in primary markets. This forces operators to invest in on-site dispatchable generation or pursue behind-the-meter generation.

- A second challenge is intensifying environmental regulation, with new IT equipment performance standards and mandates for water usage effectiveness complicating design and operations. This is particularly true in water-stressed regions, where closed-loop liquid cooling systems are becoming mandatory.

- Finally, supply chain volatility and construction cost inflation remain persistent issues, with costs for AI-ready facilities running approximately 10% higher than traditional builds due to the demand for specialized components like high-density power distribution units and the scarcity of skilled labor.

Exclusive Technavio Analysis on Customer Landscape

The hyperscale data center market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the hyperscale data center market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Hyperscale Data Center Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, hyperscale data center market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Cloud - Key offerings provide globally scaled infrastructure designed for massive compute, storage, big data, and AI workloads, enabling rapid and on-demand resource expansion for enterprises.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Cloud

- Amazon.com Inc.

- CoreSite Realty Corp.

- CyrusOne LLC

- Digital Realty Trust Inc.

- Equinix Inc.

- Google LLC

- HCL Technologies Ltd.

- IBM Corp.

- KDDI Corp.

- Meta Platforms Inc.

- Microsoft Corp.

- Nippon Telegraph and Corp.

- OVH Groupe SA

- Rackspace Technology Inc.

- SAP SE

- Scaleway SAS

- Tata Communications Ltd.

- Tencent Holdings Ltd.

- Vantage Data Centers Management

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Hyperscale data center market

- In October 2024, Google signed a Master Plant Development Agreement with Kairos Power to purchase nuclear energy, securing a carbon-free power supply for its expanding AI data centers in the United States.

- In May 2024, Google commenced construction on a $2 billion data center and cloud region in Selangor, Malaysia, to support surging regional demand for cloud and AI services.

- In March 2025, Microsoft initiated a massive construction project in Ohio to build a dedicated cluster for advanced neural network training, signaling a shift toward specialized hyperscale sites.

- In April 2025, Amazon Web Services entered a long-term agreement with a nuclear energy provider in Pennsylvania, securing a dedicated, carbon-free electricity supply for its East Coast operations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Hyperscale Data Center Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 24.6% |

| Market growth 2026-2030 | USD 305772.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 21.4% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, UK, Germany, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, South Africa, UAE, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The hyperscale data center market is defined by a fundamental redesign of its physical layer to support next-generation computing. The industry is rapidly deploying high-performance computing clusters powered by graphical processing units and other specialized accelerators.

- This transition necessitates a move to rack-scale integrated systems and high-density power racks, supported by advanced thermal management like direct-to-chip cooling, immersion cooling techniques, and rear-door heat exchangers. To meet sustainability goals, operators are integrating carbon-free energy sources, including small modular reactors and battery-energy storage systems, alongside waste-heat recovery systems.

- The adoption of rack-scale integrated systems has enabled a 30% increase in compute density per square foot. Architectures are shifting to accommodate high-density power distribution units and coolant distribution units, often within a hybrid infrastructure model.

- This evolution is driven by the need to create an AI factory design capable of handling immense computational loads while navigating grid interconnection delays and data residency laws through strategic behind-the-meter generation and sovereign cloud regions.

What are the Key Data Covered in this Hyperscale Data Center Market Research and Growth Report?

-

What is the expected growth of the Hyperscale Data Center Market between 2026 and 2030?

-

USD 305.77 billion, at a CAGR of 24.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Critical infrastructure, and Support infrastructure), End-user (BFSI, Energy, IT, and Others), Capacity (10-50 MW, 50-100 MW, and Above 100 MW) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Exponential demand for generative AI workloads, Escalating power scarcity and grid interconnection delays

-

-

Who are the major players in the Hyperscale Data Center Market?

-

Alibaba Cloud, Amazon.com Inc., CoreSite Realty Corp., CyrusOne LLC, Digital Realty Trust Inc., Equinix Inc., Google LLC, HCL Technologies Ltd., IBM Corp., KDDI Corp., Meta Platforms Inc., Microsoft Corp., Nippon Telegraph and Corp., OVH Groupe SA, Rackspace Technology Inc., SAP SE, Scaleway SAS, Tata Communications Ltd., Tencent Holdings Ltd. and Vantage Data Centers Management

-

Market Research Insights

- The market is shaped by the convergence of digital sovereignty requirements and the push for infrastructure-as-a-service. A focus on environmental stewardship is driving carbon-neutral operations, with some operators reducing energy consumption by over 20%. As data localization mandates intensify, secondary market expansion and tier 2 market growth are accelerating.

- This supports the deployment of cloud-native architectures and hybrid cloud architectures, with colocation service providers playing a key role in building out global connectivity nodes and interconnection hubs. To meet demands for public sector cloud adoption and the financial technology sector, operators prioritize low-latency delivery and network density.

- These efforts facilitate digital ecosystem growth and support mission-critical workloads, with unified cloud management platforms enabling up to a 30% improvement in operational efficiency across diverse deployments.

We can help! Our analysts can customize this hyperscale data center market research report to meet your requirements.

RIA -

RIA -