Industrial Adhesives Market Size 2024-2028

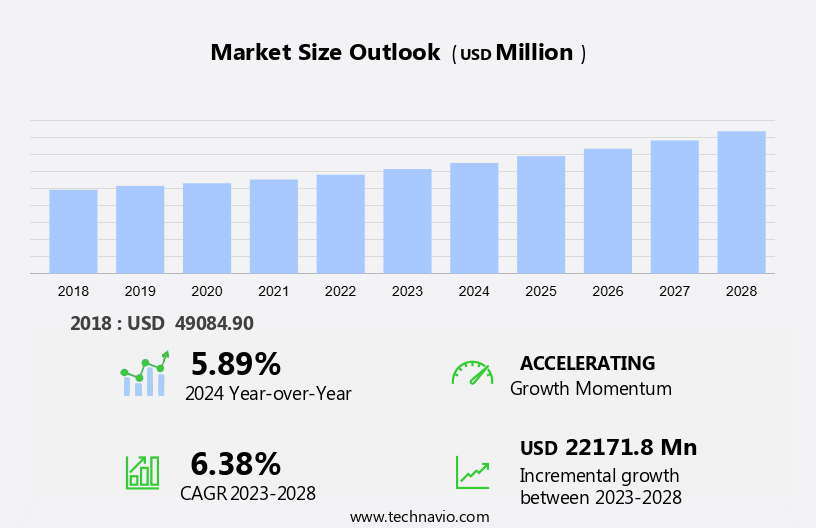

The industrial adhesives market size is forecast to increase by USD 22.17 billion at a CAGR of 6.38% between 2023 and 2028.

- The market is witnessing significant growth due to several key trends. One of these trends is the increasing replacement of mechanical fasteners with industrial adhesives in various industries, including automotive and construction, to reduce production costs and improve product quality. Another trend is the rise in automation and implementation of Industry 4.0, leading to an increased demand for industrial adhesives in manufacturing processes. Additionally, the price rise is driving market growth as manufacturers seek cost-effective alternatives to meet their production needs. These factors, among others, are expected to contribute to the market's expansion In the coming years. These offer numerous benefits, including increased productivity, improved bond strength, and reduced manufacturing costs, making them an essential component in various industries.

What will be the Size of the Market During the Forecast Period?

- The market encompasses a wide range of products used for bonding various substrates in diverse industries. Cohesion and adhesion are key factors driving market growth, as these materials enable the joining of dissimilar materials and enhance product performance. Applications span across sectors such as glass bonding, welding alternatives like adhesives versus rivets, fuel economy improvements in automotive manufacturing, furniture assembly, and non-woven fabrics production. Product offerings include polyurethane, epoxy, vinyl, acrylic, water-based, solvent-based, and hot-melt adhesives.

- Each type caters to specific application requirements, with water-based and solvent-based adhesives gaining traction due to their eco-friendliness. Market size is substantial, with continuous expansion fueled by advancements in technology and increasing demand for high-performance adhesives. Overall, the market is a dynamic and evolving sector, providing solutions for cohesion and adhesion needs across various industries.

How is this Industry segmented and which is the largest segment?

The industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Building and woodworking

- Packaging

- Transportation

- Pressure-sensitive products

- Others

- Technology

- Water-based adhesives

- Solvent-based adhesives

- Hot melt adhesives

- Reactive adhesives

- Geography

- APAC

- China

- Japan

- North America

- US

- Europe

- Germany

- UK

- Middle East and Africa

- South America

- APAC

By End-user Insights

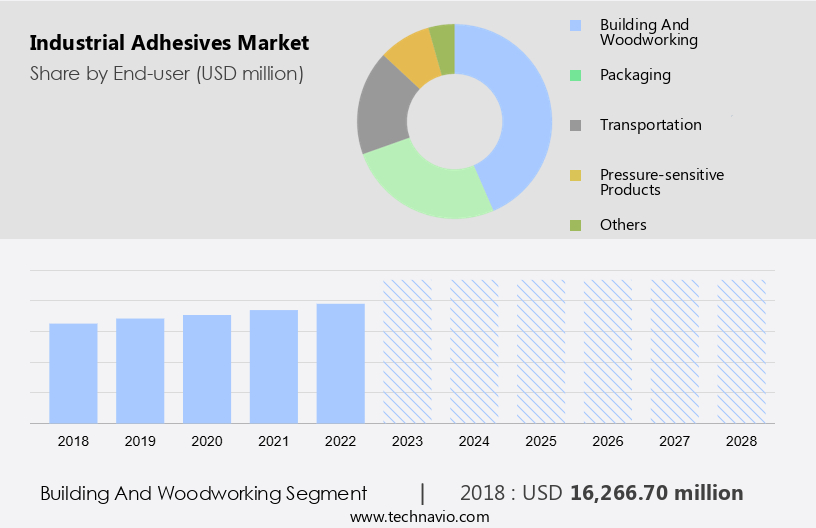

- The building and woodworking segment is estimated to witness significant growth during the forecast period.

Industrial adhesives play a crucial role in various industries, particularly in building and woodworking, due to their wide range of applications. These adhesives are used in flooring, waterproofing, tiling, carpeting, insulation, wall coverings, roofing, and construction projects for bonding, maintenance, renovation, and repair in residential, commercial, and civil constructions. In construction, industrial adhesives serve as a strong bonding agent between materials and are also used as raw materials in concrete mixtures, slabs, coatings, and other applications. Their use enhances construction projects' durability and ability to withstand harsh weather conditions. Key industries utilizing industrial adhesives include automotive, electronics, medical devices, furniture, and non-woven fabrics.

Get a glance at the market report of share of various segments Request Free Sample

The building and woodworking segment was valued at USD 16.27 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

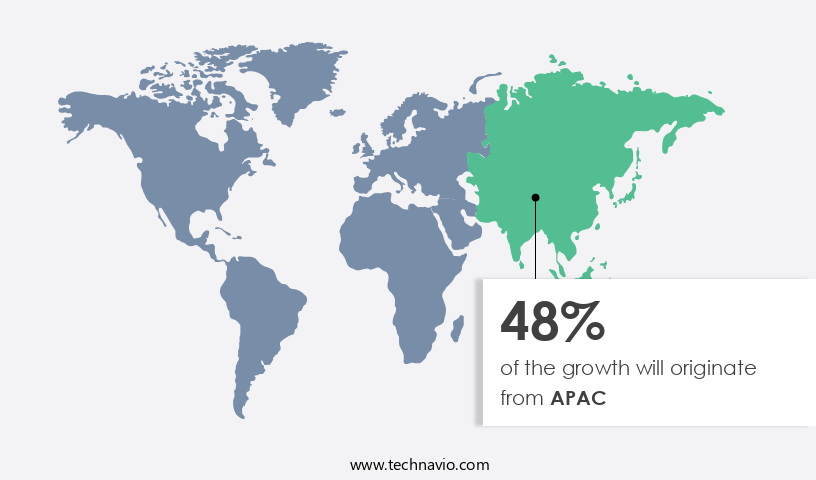

- APAC is estimated to contribute 48% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market is experiencing significant growth due to increasing demand from key countries such as China, Japan, India, and Australia. The expansion of the commercial and residential construction sector, coupled with infrastructure development investments, is driving the market's growth. Additionally, the retail sector in countries like China, India, Japan, South Korea, and Indonesia is witnessing growth, leading to an increased need for industrial adhesives to enhance product packaging's aesthetic appeal and attract customers. Furthermore, the manufacturing sector's expansion In these countries is also contributing to the market's growth. Industrial adhesives are essential in various industries, including glass bonding, welding, and riveting, to ensure high-quality adhesion.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Industrial Adhesives Industry?

Increasing replacement of mechanical fasteners with industrial adhesives is the key driver of the market.

- Industrial adhesives have gained significant traction in various sectors, surpassing traditional methods like cohesion and adhesion through welding, rivets, and glass bonding. The shift is driven by the increasing demand for high-quality adhesion, fuel economy, and environmental concerns. In industries such as construction, consumer durables, electronics, aerospace, packaging, and heavy manufacturing, adhesives are increasingly preferred for their superior performance and operational benefits. Adhesives offer several advantages over conventional methods. They provide better bonding strength, reduce weight, and improve fuel economy in vehicles. Moreover, they address environmental issues by reducing the need for solvents and VOC emissions. In sectors like medical devices and non-woven fabrics, adhesives offer unique benefits, such as flexibility, sterilization compatibility, and lightweight properties.

- The choice of adhesive type depends on the substrate and application requirements. Commonly used adhesive types include Polyurethane, Epoxy, Vinyl, Acrylic, Hot-melt Adhesives, and Eco-friendly alternatives. As petrochemicals are the primary raw materials for most adhesives, oil prices and their availability can impact the market dynamics. However, the lack of awareness about the benefits of adhesives and their high initial cost may act as restraints. Overall, the market is expected to continue growing, driven by the increasing demand for lightweight vehicles, fuel efficiency, and high-performance applications.

What are the market trends shaping the Industrial Adhesives Industry?

Rise in automation and implementation of Industry 4.0 is the upcoming market trend.

- The market is experiencing significant growth due to the increasing adoption of automation and Industry 4.0 technologies. These advancements have led to heightened demand for adhesives that can effectively bond components and materials in automated assembly lines. Industrial adhesives offer fast and reliable bonding solutions, with desirable properties such as rapid curing times, high strength, and compatibility with robotic application systems. Moreover, Industry 4.0 technologies, including IoT sensors and data analytics, are revolutionizing manufacturing processes by enabling optimized adhesive usage and enhanced production efficiency. The automotive industry is a major consumer of industrial adhesives, with applications ranging from glass bonding and welding to the replacement of rivets.

- Furthermore, the demand for lightweight vehicles and fuel economy is driving the adoption of high-quality adhesives that can reduce the weight of vehicles while maintaining structural integrity. In addition, environmental concerns are prompting the development of eco-friendly adhesives, such as those derived from renewable resources, to address VOC emissions and other environmental issues. Industrial adhesives find extensive applications in various industries, including medical devices, furniture, non-woven fabrics, and petrochemicals. Popular adhesive types include Polyurethane, Epoxy, Vinyl, Acrylic, Hot-melt Adhesives, and Eco-friendly alternatives. As the market continues to evolve, the focus on innovation and sustainability is expected to shape the future of industrial adhesives.

What challenges does the Industrial Adhesives Industry face during its growth?

Rise in price of industrial adhesives is a key challenge affecting the industry growth.

- The market growth is strong, driven by the need for high-quality adhesion in various industries such as glass bonding, welding, and fuel economy restraints. However, the market faces challenges due to the high cost of industrial adhesives, particularly in price-sensitive markets. The primary raw materials for industrial adhesives are derived from crude oil and petrochemicals, including silicone, polyurethane, epoxy, vinyl, acrylic, hot-melt adhesives, and others.

- The volatility of crude oil prices influences the cost of raw materials, potentially impacting the profitability of market participants. Some manufacturers have responded by increasing the prices of industrial adhesives to offset these costs. Additionally, environmental concerns and the shift towards lightweight vehicles are driving the demand for eco-friendly, low-VOC emission adhesives. Applications in medical devices, furniture, and non-woven fabrics further expand the market's scope.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Applied Products Inc.

- Arkema Group

- Avery Dennison Corp.

- BASF SE

- Beacon Adhesives Inc.

- Covestro AG

- DuPont de Nemours Inc.

- H.B. Fuller Co.

- Henkel AG and Co. KGaA

- Hernon Manufacturing Inc.

- Hexcel Corp.

- Hitachi Ltd.

- Huntsman International LLC

- Jowat SE

- Permabond LLC

- Pidilite Industries Ltd

- Sika AG

- Solvay SA

- Wacker Chemie AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Industrial adhesives play a crucial role in various industries by ensuring high-quality cohesion and adhesion between substrates. These bonding agents have gained significance due to their ability to replace traditional joining methods such as welding, rivets, and glass bonding. The demand for industrial adhesives is driven by several factors, including the need for fuel economy, environmental concerns, and the production of lightweight vehicles. One of the primary factors fueling the growth of the market is the increasing focus on reducing fuel consumption and improving fuel economy. Adhesives offer a viable solution by reducing the weight of vehicles through the elimination of heavy joining methods like welding and rivets.

Additionally, the use of eco-friendly adhesives further contributes to the reduction of carbon emissions, making them an attractive alternative for automotive manufacturers. Another factor driving the market is the increasing production of medical devices and the need for high-quality adhesion. In the medical industry, adhesives are used to bond various components of medical devices, ensuring their functionality and reliability. The demand for medical devices is expected to grow due to an aging population and increasing healthcare expenditures, leading to an increase In the demand for industrial adhesives. Moreover, the use of industrial adhesives In the production of non-woven fabrics is also on the rise.

Furthermore, these fabrics are widely used in various industries, including furniture manufacturing, due to their lightweight and durable properties. Adhesives play a crucial role in bonding the layers of non-woven fabrics, ensuring their strength and longevity. The market is diverse, with various types of adhesives catering to different applications. Some of the commonly used adhesives include polyurethane, epoxy, vinyl, acrylic, and hot-melt adhesives. Each type of adhesive has its unique properties and applications. For instance, epoxy adhesives offer excellent strength and durability, making them suitable for bonding metal substrates. On the other hand, hot-melt adhesives offer fast curing times and are commonly used in packaging applications.

Despite the numerous benefits of industrial adhesives, there are certain restraints that limit their growth. One of the significant restraints is the high cost of some types of industrial adhesives, particularly those based on petrochemicals. Additionally, the lack of awareness about the benefits of industrial adhesives and the availability of alternative joining methods are other factors that hinder market growth. Additionally, the growing demand for medical devices and the use of industrial adhesives in various industries, including furniture manufacturing, further contribute to the market growth. Despite the numerous benefits, the high cost of some types of industrial adhesives and the lack of awareness about their benefits are significant restraints. Overall, the market for industrial adhesives is diverse, with various types of adhesives catering to different applications.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

194 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.38% |

|

Market growth 2024-2028 |

USD 22.17 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.89 |

|

Key countries |

US, China, Japan, Germany, and UK |

|

Competitive landscape |

Leading Companies, market growth and forecasting, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the market growth of industry companies

We can help! Our analysts can customize this market research report to meet your requirements.

RIA -

RIA -